China

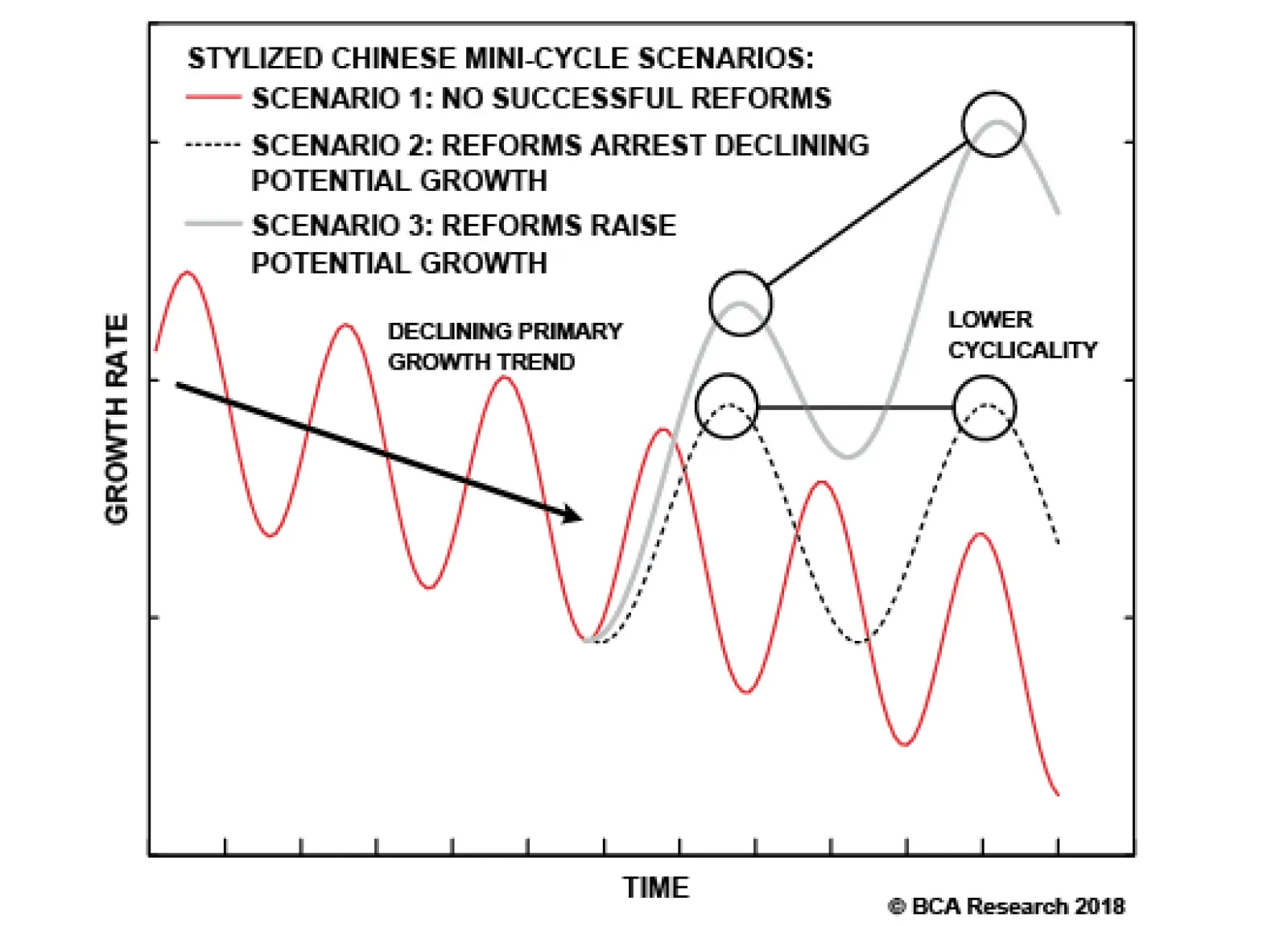

The chart presents three stylized scenarios as a possible multi-year roadmap for investors faced with a “mini-cycle world”. Scenario 1 represents the pessimistic case articulated by Arthur Budaghyan, our chief emerging markets strategist, which involves a set…

Dear Clients, This is the final publication for the year. The Emerging Markets Strategy team wishes you a very happy holiday season and a prosperous New Year! Best regards, Arthur Budaghyan Highlights The recent EM outperformance is a mid-bear market stabilization, and is at its late stage. Market signals and economic data are consistent with a further slowdown in global growth emanating from China/EM. We reiterate that global trade is heading for a period of contraction and investors should position accordingly. EM will sell off even as U.S. bond yields drop further. Feature Global investors have been increasing their absolute exposure to EM equities over the past two months, despite the ongoing drop in DM share prices.1 The common narrative is that a potential pause by the Fed next year, the trade truce between the U.S. and China and the latter’s ongoing stimulus measures are together sufficient to propel EM risk assets higher on a tactical and even cyclical horizon. In contrast, we believe the recent EM outperformance is a mid-bear market stabilization, and is at a late stage. We have written at length that neither the Fed nor the trade wars were the main culprit behind the EM selloff early this year. The key reason behind the EM and commodities selloff was the slowdown in Chinese/EM economies and global trade. China’s policy stimulus has so far been insufficient to reverse the economy’s growth slump. As such, the odds are that China/EM growth and global trade will continue to disappoint, and the EM selloff and underperformance will resume sooner than later. Market Signals EM risk assets are sensitive to China’s growth and global trade. Market signals remains downbeat on both. In particular: Global cyclicals continue to send a bleak message about the global business cycle. Global machinery, chemicals, freight and logistics as well as semiconductor stocks have been underperforming the global equity index in a falling market (Chart I-1). This is consistent with an ongoing slowdown in global growth. Chart I-1AGlobal Cyclicals Are Underperforming In A Falling Market

Global Cyclicals Are Underperforming In A Falling Market

Global Cyclicals Are Underperforming In A Falling Market

Chart I-1BGlobal Cyclicals Are Underperforming In A Falling Market

Global Cyclicals Are Underperforming In A Falling Market

Global Cyclicals Are Underperforming In A Falling Market

EM relative equity performance versus DM has historically been tightly correlated with global materials’ share prices versus the overall global stock benchmark (Chart I-2, top panel). Remarkably, the recent EM outperformance has not been corroborated by outperformance of global materials (Chart I-2, bottom panel). This is additional evidence that suggests investors should fade this EM rebound/outperformance. Chart I-2EM Vs. DM Is Akin To Global Materials Vs. Benchmark Index

EM Vs. DM Is Akin To Global Materials Vs. Benchmark Index

EM Vs. DM Is Akin To Global Materials Vs. Benchmark Index

EM risk assets are very sensitive to both global trade and commodities prices. The majority of forward-looking indicators on global trade remain dismal (please refer to the section below for a more detailed discussion on this topic). Interestingly, the current trajectory of global equities – including the run-up in share prices before January 2018’s peak, the top formation itself, and the subsequent decline – impeccably track the same trajectory that occurred between 1998 and 2000 in terms of both oscillations and magnitude (Chart I-3). Chart I-3Are Global Equities In A Bear Market?

Are Global Equities In A Bear Market?

Are Global Equities In A Bear Market?

The top in 2000 was followed by a devasting, three-year bear market. We are not arguing this global equity selloff will last that long nor be that large. What we are saying is that this turbulence will last another several months, and that there is still considerable potential for further drawdowns. Finally, the silver-gold ratio is breaking below its previous lows, including its early 2016 low (Chart I-4). Such a breakdown could be a precursor of a deflationary shock stemming from the Chinese economy. Chart I-4Beware Of Breakdown In The Silver-Gold Ratio

Beware Of Breakdown In The Silver-Gold Ratio

Beware Of Breakdown In The Silver-Gold Ratio

Global Trade: A Contraction Ahead? This section elaborates on the fundamental rationale behind the selloff – the deepening global business cycle downturn stemming primarily from China/EM economies: There are several indications that the global slowdown is already hurting American manufacturing. In the U.S., the CASS Freight Shipment Index, which measures North American freight volumes and is published by the Saint Louis Federal Reserve is foretelling an impending slump in the manufacturing sector (Chart I-5, top panel). Chart I-5U.S. Growth Is Slowing

U.S. Growth Is Slowing

U.S. Growth Is Slowing

Consistently, the growth rates of both total intermodal carloads and railroad carloads excluding petroleum and coal have rolled over decisively (Chart I-5, middle and bottom panels). As U.S. manufacturing slows, U.S. Treasury yields will drop further. In China, the slowdown is occurring not only in the industrial parts of the economy but also in household spending (Chart I-6). Chart I-6Chinese Consumer Is In A Soft Spot

Chinese Consumer Is In A Soft Spot

Chinese Consumer Is In A Soft Spot

In the case of the industrial segments, falling new and backlog orders are heralding further deterioration in nominal manufacturing output growth (Chart I-7). Accordingly, the construction and installation component of fixed asset investment is already very weak, while equipment and instrument purchases are contracting. Chart I-7Chinese Manufacturing: Deepening Slump

Chinese Manufacturing: Deepening Slump

Chinese Manufacturing: Deepening Slump

The key channel in which China impacts the rest of the world is through its imports. In turn, the latter are driven by the nation’s credit and fiscal spending impulse (Chart I-8, top panel). That explains the linkage between the Chinese credit and fiscal impulse and EM corporate profits (Chart I-8, bottom panel). Chart I-8The Linkages Between Chinese Credit & Fiscal Spending, Imports And EM Profits

The Linkages Between Chinese Credit & Fiscal Spending, Imports And EM Profits

The Linkages Between Chinese Credit & Fiscal Spending, Imports And EM Profits

Crucially, the import sub-component of mainland manufacturing PMI has plunged well below the 50 boom-bust line and signals further downside in EM equities and industrial metals prices (Chart I-9). Chart I-9Chinese Imports Versus EM Stocks And Industrial Metals

Chinese Imports Versus EM Stocks And Industrial Metals

Chinese Imports Versus EM Stocks And Industrial Metals

This is consistent with contracting Chinese imports from various countries (Chart I-10). This is how China’s negative growth shock is promulgating throughout the rest of the world. Chart I-10German And Japanese Shipments To China To Contract

German And Japanese Shipments To China To Contract

German And Japanese Shipments To China To Contract

Finally, the growth rate of Korean, Japanese, Taiwanese and Singaporean aggregate exports is approaching zero, which is typically a bad omen for EM share prices (Chart I-11). Chart I-11Asian Exports And EM Stocks

Asian Exports And EM Stocks

Asian Exports And EM Stocks

What’s more, Taiwanese shipments of electronic products parts are begining to contract, which hearalds a bleak outlook for both the global trade cycle and EM technology sector profits (Chart I-12). Consistently, semiconductor prices have continued to fall precipitously. Chart I-12Prepare For More Weakness in Global Trade

Prepare For More Weakness in Global Trade

Prepare For More Weakness in Global Trade

Bottom Line: We reiterate that global trade is heading for a period of contraction due to the deepening growth slump in China/EM. Chinese Stimulus and U.S. Growth: Lost In Translation? We endeavor to tackle two critical questions: (1) Why has policy stimulus in China failed to stabilize growth? We have written about this extensively in previous reports and will review our key points briefly. First, regulatory tightening on banks and non-bank financial institutions is overwhelming the benefits of lower interbank rates. New regulations are constraining banks’ and financial intermediaries’ ability to expand their balance sheets as aggressively as before. Slowing credit growth has so far offset robust fiscal spending – please refer to Chart I-8. Second, in a system saddled with extreme leverage, non-performing loans and very weak capacity to service debt, the impact of lower interest rates on credit origination is likely to be minimal. This diminishes the efficacy of monetary policy easing on credit growth. China’s credit excesses are enormous, and deleveraging is probably in the very early innings (Chart I-13, top panel). Notably, company and household credit are still expanding at a 10% pace from a year ago (Chart I-13, bottom panel). Chart I-13Has China Started Deleveraging? Not Really

Has China Started Deleveraging? Not Really

Has China Started Deleveraging? Not Really

Third, the authorities are facing a formidable dilemma between opting for lower interest rates and/or maintaining a stable exchange rate. We have been highlighting the tight correlation between the CNY/USD exchange rate and interest rates. The recent stabilization in the CNY/USD may have been due to the latest rise in Chinese interbank rates (Chart I-14). Chart I-14China's Monetary Policy Dilemma

China's Monetary Policy Dilemma

China's Monetary Policy Dilemma

Yet, the real economy in China and its numerous indebted entities require lower (and probably zero) interest rates for a couple of years, as occurred in Japan, the U.S. and the euro area in the years following the peaks in their respective credit bubbles. All in all, it is not clear if the authorities can reduce interest rates without eliciting currency depreciation. For now, the jury is still out. Fourth, net liquidity injections into the banking system by the People’s Bank of China (PBoC) have been minimal in recent years (Chart I-15, top panel). In fact, commercial banks’ excess reserves at the PBoC have been flattish over the past three years (Chart I-15, bottom panel). While the media and many commentators have been focused on the reserve requirement ratio reductions that have infused a lot of excess reserves into the banking system, there have also been many expired lending facilities from the PBoC to banks. The net result has been flattish liquidity trend in the banking system. Chart I-15Chinese Banking System's Excess Reserves Are Flattish

Chinese Banking System's Excess Reserves Are Flattish

Chinese Banking System's Excess Reserves Are Flattish

While there is no limit on a central bank’s ability to provide more excess reserves to the banking system, spare liquidity could push interbank rates lower and possibly trigger currency depreciation. Finally, monetary and fiscal policies work with varying time lags. Critically, the aggregate credit and fiscal impulse remains in a downtrend, pointing to less imports and hence a downbeat outlook for EM corporate earnings (please refer to Chart I-8). (2) Why has global trade decelerated amid robust U.S. demand? U.S. import growth has been very robust, yet global trade has slowed (Chart I-16). Chart I-16Robust U.S. Imports Have Not Precluded Global Manufacturing Slowdown

Robust U.S. Imports Have Not Precluded Global Manufacturing Slowdown

Robust U.S. Imports Have Not Precluded Global Manufacturing Slowdown

The reason behind this is very simple: U.S. and EU annual merchandize goods imports amount to $2.5 trillion and $2.2 trillion, respectively – dwarfed by EM (including China) imports of $6 trillion (Chart I-17). Chart I-17EM Imports Are Larger Than Combined U.S. And EU Imports

EM Imports Are Larger Than Combined U.S. And EU Imports

EM Imports Are Larger Than Combined U.S. And EU Imports

This value of EM imports excludes China’s imports for processing and re-exporting as well as all the imports of Mexico and central Europe, which also include a lot of inputs that are processed and re-exported. In spite of these adjustments, EM imports are still considerably larger than U.S. and EU imports combined. Hence, robust U.S. final demand is in and of itself insufficient to both offset and support global trade growth when EM/China demand falters. This is especially pertinent to commodities and industrial goods, where China/EM are large consumers. Chart Patterns: Reading Market Tea Leaves There is no magical formula that can guarantee making money in financial markets. Economic data are lagging, markets can change direction abruptly, and indicators can break down or give false signals from time to time. Besides, financial markets do not move in straight lines, and differentiating the noise from the signal is not a simple exercise. The odds of making money or outperforming are higher when investors are correct in their big- picture judgements – i.e., when their thematic views on the global economic and investment landscapes are accurate. Markets can be very noisy and volatile in the short term, yet there are several critical chart patterns that we are taking comfort with as they are consistent with our macro themes. The latter are the following: Sagging China/EM growth, a deepening global trade slump, lower commodities prices and a stronger U.S. dollar/weaker EM currencies. Our Risk-On versus Safe-Haven Currency Ratio2 has relapsed since early this year after failing to break above its previous top (Chart I-18). In and of itself, this is already a bearish chart formation. Besides, it seems this market indicator is forming a potential head-and-shoulders pattern. Chart I-18A Bear Market In Risk-On Versus Safe-Haven Currencies Ratio

bca.ems_wr_2018_12_20_s1_c18

bca.ems_wr_2018_12_20_s1_c18

Any relapse from current levels will validate the head-and-shoulders profile. As a result, the odds of a major plunge will rise, which would be consistent with our themes and outlook. EM share prices in dollar terms have also struggled to break above their 2007 highs in the past 10 years, despite the bull market in the S&P 500 during this period (Chart I-19). Remarkably, the EM stock index is presently sitting on several of its long-term moving averages. They make a formidable technical support. Box 1 elaborates why we use these long-term moving averages in our regular reports. Chart I-19EM Equities Are Facing An Air Pocket

EM Equities Are Facing An Air Pocket

EM Equities Are Facing An Air Pocket

If these technical supports give in, EM equities will hit an air pocket – with the next technical support lying 25% below the current level. It is no surprise that an intense battle between bulls and bears is currently being waged. Provided EM corporate profits are set to contract in the first half of 2019, as per our analysis above, we believe these technical supports will be violated and that a major plunge in share prices is very likely. Finally, share prices of global energy and mining companies rolled over early this year at their long-term moving averages (Chart 20, top and middle panels). These long-term moving averages acted as a support in bull markets; now they have become a resistance. Hence, it makes sense to argue that energy and mining stocks remain in a secular bear market, and the 2016-‘17 advance was a bear market rally. If so, further downside in their share prices could be substantial. Meantime, global semiconductor share prices rolled over at their 2000 peak earlier this year (Chart I-20, bottom panel). This is a bad technical sign and might signify that a non-trivial slowdown in global growth may last for quite some time. Chart I-20Global And Mining Stocks Remain In A Secular Bear Market

Global And Mining Stocks Remain In A Secular Bear Market

Global And Mining Stocks Remain In A Secular Bear Market

Typically, in the periods when resources and technology stocks sell off, EM equities and other risk assets perform badly. It appears we are currently in such a phase, and it will not be short-lived. Investment Strategy China/EM growth conditions continue to worsen. Tactically and cyclically, risks to EM stocks, currencies, credit and high-yielding local bonds are skewed to the downside. We continue to recommend playing EM on the short side. Playing a market on the long side when fundamentals are deteriorating and valuations are not cheap is akin to collecting pennies in front of a steamroller. The recent outperformance of EM equities and credit versus DM is unsustainable. Continue to underweight EM. For dedicated EM equity portfolios, our overweights are Brazil, Chile, Mexico, Russia, central Europe, Korea and Thailand, while our underweights are Indonesia, the Philippines, Peru and South Africa. We are considering to upgrade India from underweight to neutral. Our preferred short currency basket versus the U.S. dollar consists of the ZAR, the IDR, the CLP, the COP and the KRW. Box 1 - Our Long-Term Moving Average Framework “All through time, people have basically acted and re-acted the same way in the market as the result of: Greed, Fear, Ignorance & Hope. That is why numeric formations and patterns recur on a constant basis.” - Jesse Livermore, in Reminiscences of a Stock Operator The basis for examining price patterns with their 200-, 400-, 800-, 1600- and 3200-day moving averages (MA) – corresponding to nine months, 18 months, 3-, 6-, 12 and 24-year moving averages – is as follows: The 200-day MA is a very widely known and well-used measure. We have observed that when the 200-day MA breaks in a bull market, the next support could occur at the 400- or 800-day MA levels – i.e., the multiples of the 200-day MA. Following the same logic, we examined even longer-term moving averages such as 6-, 12- and 24-year MAs. Interestingly, we discovered that the 3- and 6-year MAs worked very well during the S&P 500 bull run of the 1950s and 1960s (Chart I-21, top panel). Besides, during the bull market of the 1980s-‘90s, the S&P 500 selloffs also found support at the 3- and 6-year MAs (Chart 21, bottom panel). Chart I-21The S&P 500 And Long-Term Moving Averages

The S&P 500 And Long-Term Moving Averages

The S&P 500 And Long-Term Moving Averages

Meanwhile, the bear market bottoms in 1982 and 2002-‘03 in the U.S. equity market occurred at a very long-term (12-year) MA (Chart I-21, bottom panel). Similarly, in the fixed-income universe, throughout the more than 35-year- strong U.S. bond bull market, the rise in bond yields often topped out when 10-year Treasury yields reached their 6-year MA (Chart I-22). Chart I-22U.S. Bond Yields And Long-Term Moving Averages

U.S. Bond Yields And Long-Term Moving Averages

U.S. Bond Yields And Long-Term Moving Averages

These observations have led us to infer that structural trends cannot be considered completely broken as and when markets cross their 200-day MA. Large selloffs (or cyclical bear markets) within structural bull markets can push prices to their very long-term moving averages such as 3- or 6-year MAs. The opposite holds true for tactical and cyclical rallies within bear markets. Besides, we have also observed that when a financial market in a selloff finds support at a particular long-term MA, it usually resumes its rally and often advances to new highs. On the contrary, when a market rallies but fails to break above its long-term MA (resistance), it often experiences a breakdown. We often apply this long-term moving average framework to analyze trends in various financial markets, and contrast and evaluate these with our fundamental economic themes. As to the question of why these numbers work, the quote above from Reminiscences of a Stock Operator could be the answer. Arthur Budaghyan, Senior Vice President Emerging Markets Strategy arthurb@bcaresearch.com Footnote 1 BoA December survey 2 Average of CAD, AUD, NZD, BRL, CLP & ZAR total return indices relative to average of JPY & CHF total returns (including carry). Equity Recommendations Fixed-Income, Credit And Currency Recommendations

Highlights So What? Our best and worst calls of 2018 cast light on our methodology and 2019 forecasts. Why? Our clients took us to task for violating our own methodology on the Iranian oil sanctions. Sticking to our guns would have paid off with long Russian equities versus EM. We correctly called China’s domestic policy, the U.S.-China trade war, Europe, the U.S. midterms, and relative winners in emerging markets. Feature It has been a tradition for BCA’s Geopolitical Strategy, since our launch in 2012, to highlight our best and worst forecasts of the year.1 This will also be the final publication of the year, provided that there is no global conflagration worthy of a missive between now and January 9, when we return to our regular publication schedule. We wish all of our clients a great Holiday Season. And especially all the very best in 2019: lots of happiness, health, and hefty returns. Good luck and good hunting. The Worst Calls Of 2018 A forecasting mistake is wasted if one learns nothing from the error. This is why we take our mistakes seriously and why we always begin the report card with our zingers. Our overall performance in 2018 was … one of our best. The successes below will testify to this. However, we made three notable errors. A Schizophrenic Russia View Our worst call of the year was to panic and close our long Russian equities relative to emerging markets trade in the face of headline geopolitical risks. In early March, we posited that Russia was a “buy” relative to the broad EM equity index due to a combination of cheap valuations, strong macro fundamentals, orthodox policy, and an end to large-scale geopolitical adventurism. This call ultimately proved to be correct (Chart 1). Chart 1Russian Stocks Outperformed In The End

Russian Stocks Outperformed In The End

Russian Stocks Outperformed In The End

What went wrong? The main risk to our view, that the U.S. Congress would pursue an anti-Russia agenda regardless of any Russian sympathies in the Trump White House, materialized in the wake of the poisoning of former Russian military intelligence officer Sergei Skripal with a Novichok nerve agent in the United Kingdom. As fate would have it, the incident occurred just before our bullish report went to clients! The ensuing international uproar and sanctions caused a selloff. Our bullish thesis did not rest exclusively on geopolitics, but a thaw in West-Russia relations did form the main pillar of the view. Our Russia Geopolitical Risk Index, which had served us well in the past, was pricing as low of a level of geopolitical risk as one could hope for in the post-Crimea environment (Chart 2). Naturally the measure jumped into action following the Skripal incident. Chart 2Geopolitical Risk Was Low Prior To Skripal

Geopolitical Risk Was Low Prior To Skripal

Geopolitical Risk Was Low Prior To Skripal

The timing of our call was therefore off, but we should have stuck with the overall view. The U.S. imposed preliminary sanctions that lacked teeth. While Washington accepted the U.K.’s assessment that Moscow was behind the poisoning, the weakness of the sanctions also signaled that the U.S. did not consider the incident worthy of a tougher position. There are now two parallel sanction processes under way. The first round of sanctions announced in August gave Russia 90 days to comply and adopt “remedial measures” regarding the use of chemical and biological weapons. On November 9, the U.S. State Department noted that Russia had not complied with the deadline. The U.S. is now expected to impose a second round of sanctions that will include at least three of six punitive actions: Opposition to development aid and assistance by international financial institutions (think the IMF and the World Bank); Downgrading diplomatic relations; Additional restrictions on exports to Russia (high-tech exports have already been barred by the first round of sanctions); Restrictions on imports from Russia; A ban on landing rights in the U.S. for Russian state-owned airlines; Prohibiting U.S. banks from purchasing Russian government debt. While the White House was expected to have such sanctions ready to go on the November 9 deadline, it has dragged its feet for almost two months now. This suggests that President Trump continues to hold out for improved relations with President Putin. A visit by President Putin to Washington remains possible in Q1 2019. As such, we would expect the White House to adopt some mix of the first five items on the above list, hardly a crushing response from Moscow’s perspective. The U.S. Congress, however, has a parallel process in the form of the Defending American Security from Kremlin Aggression Act of 2018 (DASKAA). Introduced in August by Senator Lindsey Graham, a Russia hawk, the legislation would put restrictions on Americans buying Russian sovereign debt and curb investments in Russian energy projects. The bill also includes secondary sanctions on investing in the Russian oil sector, which would potentially ensnare European energy companies collaborating with Russia in the energy sector. There was some expectation that Congress would take up the bill ahead of the midterm election, but nothing came of it. Even with the latest incident – the seizing of two Ukrainian naval vessels in the Kerch Strait – we have yet to see action. While we expect the U.S. to do something eventually, the White House approach is likely to be tepid while the congressional approach may be too draconian to pass into law. And with Democrats about to take over the House, and likely demand even tougher sanctions against Russia, the ultimate legislation may be too bold for President Trump to sign into legislation. The point is that Russia has acted antagonistically towards the West in 2018, but in small enough increments that the response has been tepid. Given the paucity of Russian financial and trade links with the U.S., Washington’s sanctions would only bite if they included the dreaded “secondary sanction” implications for third party sovereigns and firms – particularly European, which do have a lot of business in Russia. This is highly unlikely without major Russian aggression. We cannot completely ignore the potential for such aggression in 2019, especially with President Putin’s popularity in the doldrums (Chart 3) and a contentious Ukrainian election due for March 31. However, we outlined the constraints against Russia in 2014, amidst the Ukrainian crisis, and we do not think that these constraints have been reduced (they may have only grown since then). Chart 3Non-Negligible Risk Of Russian Aggression

Non-Negligible Risk Of Russian Aggression

Non-Negligible Risk Of Russian Aggression

Regardless of the big picture for 2019, we could have faded the risks in 2018 and stuck to the fundamentals. Russia is up 17.2% against EM year-to-date. The lesson here, therefore, is to find re-entry points into a well-founded view despite market volatility. Chart 1 shows that Russian equities climbed the proverbial “wall of worry” relative to EM in 2018. Doubting Jair Bolsonaro Our list of mistakes keeps us in the EM universe where we underestimated Jair Bolsonaro’s chances of winning the presidency in Brazil. The answer to the question we posed in the title of our September report – “Brazil: Can The Election Change Anything?” – was a definitive “yes.” Since the publication of that report, BRL/USD is up 2.9% and Brazilian equities are up 18.5% relative to EM (Chart 4). Chart 4Bolsonaro Rally Losing Its Luster Already

Bolsonaro Rally Losing Its Luster Already

Bolsonaro Rally Losing Its Luster Already

To our credit, the question of Bolsonaro’s electoral chances elicited passionate and pointed internal debate. But our clients did not see the internal struggle, just the incorrect external output! A bad call is a bad call, no matter how it is assembled on the intellectual assembly line. That said, we still think that our report is valuable. It sets out the constraints facing Bolsonaro in 2019. He has to convince the left-leaning median voter that meaningful pension reform is needed; bully a fractured Congress into painful structural reforms; and overcome an unforgiving macro context of tepid Chinese stimulus and a strong USD. If the Bolsonaro administration wastes the good will of the investment community over the next six months, we expect the market’s punishment to be swift and painful. In fact, Chart 4 notes that the initial Bolsonaro rally has already lost most of its shine. Brazilian assets are still up since the election, but the gentle slope could become a steep fall if Bolsonaro stumbles. The market is priced for political perfection. To be clear, we are not bearish on Bolsonaro. We believe that, relative to EM, he will be a positive for Brazil. However, the market is currently betting that he will win by two touchdowns, whereas we think he will squeak by with a last-second field goal. The difference between the two forecasts is compelling and we have expressed it by being long MXN/BRL.2 Not Sticking To Our Method In The Case Of Iran Throughout late-2017 and 2018 we pointed out that President Trump’s successful application of “maximum pressure” against North Korea could become a market-relevant risk if he were emboldened to try the same strategy against Iran. For much of the year, this view was prescient. As investors realized the seriousness of President Trump’s strategy, a geopolitical risk premium began to seep into oil prices, as illustrated in Chart 5 by the red bar.

Chart 5

Every time we spoke to clients or published reports on this topic, we highlighted just how dangerous a “maximum pressure” strategy would be in the case of Iran. We stressed that Iran could wreak havoc across Iraq and other parts of the Middle East and even drive up oil prices to the point of causing a “geopolitical recession in 2019.” In other words, we stressed the extraordinary constraints that President Trump would face. To their credit many of our clients called us out on the inconsistency: our market call was über bullish oil prices, while our methodology emphasized constraints over preferences. We were constantly fielding questions such as: Why would President Trump face down such overwhelming constraints? We did not have a very good answer to this question other than that he was ideologically committed to overturning the Iranian nuclear deal. In essence, we doubted President Trump’s own ideological flexibility and realism. That was a mistake and we tip our hat to the White House for recognizing the complex constraints arrayed against it. President Trump realized by October how dangerous those constraints were and began floating the idea of sanction waivers, causing the geopolitical risk premium to drain from the market (Chart 6). To our credit, we highlighted sanction waivers as a key risk to our view and thus took profit on our bullish energy call early. Chart 6Sanction Waivers Caused A Collapse In Oil Prices

Sanction Waivers Caused A Collapse In Oil Prices

Sanction Waivers Caused A Collapse In Oil Prices

That said, our clients have taken the argument further, pointing out that if we were wrong on Trump’s ideological flexibility with Iran, we may be making the same mistake when it comes to China. However, there is a critical difference. Americans are more concerned about conflict with North Korea than with Iran (Chart 7), while China is the major concern about trade (Chart 8).

Chart 7

Chart 8

Second, railing against the Iran deal did not get President Trump elected, whereas his protectionist rhetoric – specifically regarding China – did (Chart 9). Getting anything less than the mother-of-all-deals with Beijing will draw down Trump’s political capital ahead of 2020 and open him to accusations of being “weak” and “surrendering to China.” These are accusations that the country’s other set of protectionists – the Democrats – will wantonly employ against him in the next general election. Chart 9Protectionism, Not Iran, Helped Trump Get Elected

Protectionism, Not Iran, Helped Trump Get Elected

Protectionism, Not Iran, Helped Trump Get Elected

Ultimately, if we have to be wrong, we are at least satisfied that our method stood firm in the face of our own fallibility. We are doubly glad to see our clients using our own method against our views. This is precisely what we wanted to accomplish when we began BCA’s Geopolitical Strategy in March 2012: to revolutionize finance by raising the sophistication with which it approaches geopolitics. That was a lofty goal, but we do not pretend to hold the monopoly on our constraint-based methodology. In the end, our market calls did not suffer due to our error. We closed our long EM energy-producer equities / EM equities for a gain of 4.67% and our long Brent / short S&P 500 for a gain of 6.01%. However, our latter call, shorting the S&P 500 in September, was based on several reasons, including concerns regarding FAANG stocks, overstretched valuations, and an escalation of the trade war. Had we paired our S&P 500 short with a better long, we would have added far more value to our clients. It is that lost opportunity that has kept us up at night throughout this quarter. We essentially timed the S&P 500 correction, but paired it with a wayward long. The Best Calls Of 2018 BCA’s Geopolitical Strategy had a strong year. We are not going to list all of our calls here, but only those most relevant to our clients. Our best 2018 forecast originally appeared in 2017, when in April of that year we predicted that “Political Risks Are Understated In 2018.” Our reasoning was bang on: U.S. fiscal policy would turn strongly stimulative (the tax cuts would pass and Trump would be a big spender) and thus cause the Fed to turn hawkish and the USD to rally, tightening global monetary policy; Trump’s trade war would re-emerge in 2018; China would reboot its structural reform efforts by focusing on containing leverage, thus tightening global “fiscal” policy. In the same report we also predicted that Italian elections in 2018 would reignite Euro Area breakup risks, but that Italian policymakers would ultimately be found to be bluffing, as has been our long-running assertion. Throughout 2018, our team largely maintained and curated the forecasts expressed in that early 2017 report. We start the list of the best calls with the one call that was by far the most important for global assets in 2018: economic policy in China. The Chinese Would Over-Tighten, Then Under-Stimulate Getting Chinese policy right required us, first, to predict that policy would bring negative economic surprises this year, and second, once policy began to ease, to convince clients and colleagues that “this time would be different” and the stimulus would not be very stimulating. In other words, this time, China would not panic and reach for the credit lever of the post-2008 years (Chart 10), but would maintain its relatively tight economic, financial, environmental, and macro-prudential oversight, while easing only on the margin. Chart 10No Massive Credit Stimulus In 2018

No Massive Credit Stimulus In 2018

No Massive Credit Stimulus In 2018

This is precisely what occurred. BCA Foreign Exchange Strategy’s “China Play Index,” which is designed to capture any reflation out of Beijing, collapsed in 2018 and has hardly ticked up since the policy easing announced in July (Chart 11). Chart 11Weak Reflation Signal From China

Weak Reflation Signal From China

Weak Reflation Signal From China

Our view was based on an understanding of Chinese politics that we can confidently say has been unique: From March 2017, we highlighted the importance of the 2017 October Party Congress, arguing that President Xi Jinping would consolidate his power and redouble his attempts to “reform” the economy by reining in dangerous imbalances. We explicitly characterized the containment of leverage as the most market-relevant reform to focus on. We stringently ignored the ideological debate about the nature of reform in China, focusing instead on the major policy changes afoot. We identified very early on how the rising odds of a U.S.-China conflict would embolden Chinese leadership to double-down on painful structural reforms. Will China maintain this disciplined approach in 2019? That is yet to be seen. But we are arming ourselves and clients with critical ways to identify when and whether Beijing’s policy easing transforms into a full-blown “stimulus overshoot”: First, we need to see a clear upturn in shadow financing to believe that the Xi administration has given up on preventing excess debt. Assuming that such a shift occurs, and that overall credit improves, it will enable us to turn bullish on global growth and global risk assets on a cyclical, i.e., not merely tactical, horizon (Chart 12). Chart 12A Shadow Lending Surge Would Mean A Big Policy Shift

A Shadow Lending Surge Would Mean A Big Policy Shift

A Shadow Lending Surge Would Mean A Big Policy Shift

Second, our qualitative checklist will need to see a lot more “checks” in order to change our mind. Short of an extraordinary surge in bank and shadow bank credit, there needs to be a splurge in central and especially local government spending (Table 1). The mid-year spike in local governments’ new bond issuance in 2018 was fleeting and fell far short of the surge that initiated the large-scale stimulus of 2015. Frontloading these bonds in 2019 will depend on timing and magnitude. Table 1A Credit Splurge, Or Government Spending Splurge, Is Necessary For Stimulus To Overshoot

BCA Geopolitical Strategy 2018 Report Card

BCA Geopolitical Strategy 2018 Report Card

Third, we would need to see President Xi Jinping make a shift in rhetoric away from the “Three Battles” of financial risk, pollution, and poverty. Having identified systemic financial risk as the first of the three ills, Xi needs to make a dramatic reversal of this three-year action plan if he is to clear the way for another credit blowout. Trade War Would Reignite In 2018 It paid off to stick with our trade war alarmism in 2018. We correctly forecast that the U.S. and China would collide over trade and that their initial trade agreement – on May 20 – was insubstantial and would not last. In the event it lasted three days. Our one setback on the trade front was to doubt the two sides would agree to a trade truce at the G20. However, by assigning a subjective 40% probability, we correctly noted the fair odds of a truce. We also insisted that any truce would be temporary, which ended up being the case. We may yet be vindicated if the March 1 deadline produces no sustainable deal, as we forecast in last week’s Strategic Outlook. That said, correct geopolitical calls do not butter our bread at BCA. Rather, we are paid to make market calls. To that end, we would point out that we correctly assessed the market-relevance of the trade conflict, fading S&P 500 risks and focusing on the effect on global risk assets. Will this continue into 2019? We think so. We do not see trade conflict as the originator of ongoing market turbulence (Chart 13) and would expect the U.S. to outperform global equities again over the course of 2019 (Chart 14). This view may appear wrong in Q1, as the market digests the Fed backing off from hawkish rhetoric, the ongoing trade negotiations, and the likely seasonal uptick in Chinese credit data in the beginning of the calendar year. Chart 13Yields, Not Trade War, Drove Stocks

Yields, Not Trade War, Drove Stocks

Yields, Not Trade War, Drove Stocks

Chart 14U.S. Stocks Will Resume Outperformance

U.S. Stocks Will Resume Outperformance

U.S. Stocks Will Resume Outperformance

However, any stabilization in equity markets would likely serve to ease financial conditions in the U.S., where economic and inflation conditions remain firmly in tightening territory (Chart 15). As such, the Fed pause is likely to last no more than a quarter, maybe two at best, leading to renewed carnage in global risk assets if our view on Chinese policy stimulus – tepid – remains valid through the course of 2019. Chart 15If Financial Conditions Ease, Tightening Will Be Back On

If Financial Conditions Ease, Tightening Will Be Back On

If Financial Conditions Ease, Tightening Will Be Back On

Europe (All Of It… Again) In 2017, our forecasting track record for Europe was stellar. This continued in 2018, with no major setbacks: Populism in Italy: Our long-held view has been that Europe’s chief remaining risks lay in Italian populists coming to power. We predicted in 2016 that this would eventually happen and that they would then be proven to be bluffing. This is essentially what happened in 2018. Matteo Salvini’s Lega is surging in the polls because its leader has realized that a combination of hard anti-immigrant policy and the softest-of-soft Euroskepticism is a winning combination. We believe that investors can live with this combination. Our only major fault in forecasting European politics and assets this year was to close our bearish Italy call too early: we booked our long Spanish / short Italian 10-year government bond trade for a small loss in August, before the spread between the two Mediterranean countries blew out to record levels. That missed opportunity could have also made it on our “worst calls” list as well.

Chart 16

Pluralism in Europe: To get the call on Italy right, we had to dabble in some theoretical work. In a somewhat academic report, we showed that political concentration was on the decline in the developed world (Chart 16), but especially in Europe (Chart 17). Put simply, lower political concentration suggests that a duopoly between the traditional center-left and center-right parties is breaking down. Contrary to the conventional wisdom, we argued that Europe’s parliamentary systems would enable centrist parties to adopt elements of the populist agenda, particularly on immigration, without compromising the overall stability of European institutions. As such, political pluralism, or low political concentration, is positive for markets.

Chart 17

Immigration crisis is over: For centrist parties to be able to successfully adopt populist immigration policy, they needed a pause in the immigration crisis. This was empirically verifiable in 2018 (Chart 18). Chart 18European Migration Crisis Is Over

European Migration Crisis Is Over

European Migration Crisis Is Over

Merkel’s time has run out: Since early 2017, we had cautioned clients that Angela Merkel’s demise was afoot, but that it would be an opportunity, rather than a risk, when it came. It finally happened in 2018 and it was not a market moving event. The main question for 2019 is whether German policymakers, and Europe as a whole, will use the infusion of fresh blood in Berlin to reaccelerate crucial reforms ahead of the next global recession. Brexit: Since early 2016, we have been right on Brexit. More specifically, we were corrent in cautioning investors that, were Brexit to occur, “the biggest loser would be the Conservative Party, not the EU.” As with the previous two Conservative Party prime ministers, it appears that the question of the U.K.’s relationship with the EU has completely drained any political capital out of Prime Minister Theresa May’s reign. We suspect that the only factor propping up the Tories in the polls is that Jeremy Corbyn is the leader of Her Majesty’s Most Loyal Opposition. We have also argued that soft Brexit would ultimately prove to be “illogical” and that “Bregret” would begin to seep in, as it now most clearly has. We parlayed these rising geopolitical risks and uncertainties by shorting cable in the first half of the year for a 6.21% gain. Malaysia Over Turkey And India Over Brazil Not all was lost for our EM calls this year. We played Malaysia against Turkey in the currency markets for a 17.44% gain, largely thanks to massively divergent governance and structural reform trajectories after Malaysia’s opposition won power for the first time in the country’s history. Second, we initiated a long Indian / short Brazilian equity view in March that returned 27.54% by August. This was a similar play on divergent structural reforms, but it was also a way to hedge our alarmist view on trade. Given India’s isolation from global trade and insular financial markets, we identified India as one of the EM markets that would remain aloof of protectionist risks. We could have closed the trade earlier for greater gain, but did not time the exit properly. Midterm Election: A Major Democratic Victory Our midterm election forecast was correct: Democrats won a substantial victory. Even our initial call on the Senate, that Democrats had a surprisingly large probability of picking up seats, proved to be correct, with Republicans eking out just two gains in a year when Democrats were defending 10 seats in states that Trump carried in 2016. What about our all-important call that the election would have no impact on the markets? That is more difficult to assess, given that the S&P 500 has in fact collapsed in the lead-up to and aftermath of the election. However, we see little connection between the election outcome and the stock market’s performance. Neither do our colleagues or clients, who have largely stopped asking about the Democrats’ policy designs. In 2019, domestic politics may play a role in the markets. Impeachment risk is low, but, if it rears its head, it could prompt President Trump to seek relevance abroad, as his predecessors have done when they lost control of domestic policy. In addition, the Democratic Party’s sweeping House victory may suggest a political pendulum swing to the left in the 2020 presidential election. We will discuss both risks as part of our annual Five Black Swans report in early 2019. U.S. domestic politics was a collection of Red Herrings during much of President Obama’s presidency, and has produced strong tailwinds under President Trump (tax cuts in particular). This may change in 2019, with considerable risk to investors, and asset prices, ahead. Marko Papic, Senior Vice President Chief Geopolitical Strategist marko@bcaresearch.com Matt Gertken, Vice President Geopolitical Strategy mattg@bcaresearch.com Roukaya Ibrahim, Editor/Strategist roukayai@bcaresearch.com Ekaterina Shtrevensky, Research Analyst ekaterinas@bcaresearch.com Footnotes 1 For our 2019 Outlook, please see BCA Geopolitical Strategy Strategic Outlook, “2019 Key Views: Balanced On A Knife’s Edge,” dated December 14, 2018, available at gps.bcaresearch.com. For our past Strategic Outlooks, please visit gps.bcaresearch.com. 2 In part we like this cross because we also think that Mexico’s newly elected president, Andrés Manuel López Obrador, is priced to lose by two touchdowns, whereas he may merely lose by a last-second field goal.

Highlights Dear Clients, This is the final publication for the year, in which we recap some of the key developments in 2018. We will resume our regular publishing schedule on January 2, 2019 with a Special Report on urbanization/industrialization. The China Investment Strategy team wishes you a very happy holiday season and a prosperous New Year! Best regards, Jonathan LaBerge, CFA, Vice President Special Reports The evidence over the past year raises the odds that China’s economy has entered a multi-year period of frequent mini-cycles. A mini-cycle world would be a difficult one for investors to navigate, particularly if the boom and bust phases are asymmetrical in length or magnitude. There is no magic wand to quickly transform China into a services-oriented economy, and it is not clear that the gains in tertiary sector GDP since 2010 are sustainable. A slow transition would raise deep questions about China’s growth model over the coming 2-3 years, and would create a major dilemma for policymakers. Chinese stocks are considerably cheaper than they were a year ago, yet they may be cheap for a reason (even over the very long term). On a risk-adjusted basis, we do not find the value proposition to be compelling, meaning that our recommended multi-year allocation to Chinese stocks is neutral barring even lower prices or tangible evidence of successful structural reforms. Feature Following the publication of our special year end Outlook report for 2019,1 BCA's China Investment Strategy service recently expanded on our global view by outlining our three key themes for China over the coming year.2 As a year-end tradition, we dedicate this week's report to recapping some important developments of the past year and their longer-term implications. Mini-Cycles, And The Policy Trade-Off Between Growth And Leveraging Over the past year we have described the progression of Chinese growth as part of an economic “mini-cycle”, one that actually began in early-2014 (we have focused on the expansion period of the cycle that started in mid-2015). While this is the first clear mini-cycle in China after a prolonged period of slowing activity that followed the enormous stimulus of 2008/2009, many investors and market participants have speculated about whether these types of events will become more prevalent in the future. In a March 2017 BCA Special Report,3 my colleague Arthur Budaghyan speculated about the potential for such cycles within the context of a falling primary growth trend. Arthur’s argument was that cyclical growth could hold up in China over the coming few years only if the government allows credit growth to continue booming, but that this would entail creeping socialism/statism that would cripple the country’s productivity and thus its potential growth. In fact, the experience of the past three years suggests that mini-cycles may occur over the coming few years even if policymakers do try to prevent a falling primary growth trend. Chart 1 shows that the slowdown in domestic demand that investors only began to price in the middle of this year has clearly been caused by a slowing in money & credit growth (as represented by our leading indicator), which in turn strongly appears to have occurred because of monetary tightening that began at the end of 2016 (panel 2). This tightening has been closely linked to the government’s attempt to de-risk the financial sector. Chart 1Tighter Monetary Policy Caused The Recent Mini-Cycle Slowdown

Tighter Monetary Policy Caused The Recent Mini-Cycle Slowdown

Tighter Monetary Policy Caused The Recent Mini-Cycle Slowdown

In addition, we presented evidence in our August 29 Special Report suggesting that Chinese state-owned enterprises (SOEs) now have a negative net return on borrowed funds (Chart 2), underscoring that Chinese authorities now face a policy trade-off between growth and leveraging.4 The inference is that investors can expect more of these episodes so long as policymakers stay committed to reforming the financial sector, a policy that appears to remain a strong priority of the Xi government. Chart 2SOEs Now Have A Negative Net Return On Borrowed Funds

SOEs Now Have A Negative Net Return On Borrowed Funds

SOEs Now Have A Negative Net Return On Borrowed Funds

Chart 3 presents three stylized scenarios as a possible multi-year roadmap for investors faced with a “mini-cycle world”. Scenario 1 represents the pessimistic case articulated by Arthur, a set of frequent cycles occurring against the backdrop of a falling primary (or potential growth) trend. Scenarios 2 and 3 represent possible outcomes emerging from successful structural reform: in scenario 2 the downtrend in potential growth is arrested and the primary growth trend becomes flat, whereas scenario 3 depicts the optimistic case, where reform initiatives unleash productivity gains that result in a net increase in potential growth. In both scenarios 2 and 3, the frequency of economic cycles is reduced to be more akin to that of typical business cycles in the developed world, ending the more rapid mini-cycle phase that preceded the success of the reforms. Chart 3A Potential Roadmap For Investors Living In A "Mini-Cycle World"

A Potential Roadmap For Investors Living In A "Mini-Cycle World"

A Potential Roadmap For Investors Living In A "Mini-Cycle World"

For an investor primarily concerned with cyclical asset allocation, one response to Chart 3 might be that any of the scenarios are acceptable because there is money to be made in each case by shifting one’s investment stance in advance of key inflection points. However, as Arthur alluded to in last year’s report, the cycles depicted in Chart 3 are highly stylized and will not repeat themselves over regular, predictable intervals. In addition, even in scenarios 2 and 3, the higher frequency of oscillations depicted in the chart prior to the positive impact of structural reforms means that a mini-cycle world will be a difficult one for investors to navigate, particularly if the boom and bust phases are asymmetrical in length or magnitude. From a longer-term perspective, Chart 3 clearly outlines two key questions that investors should be asking themselves about China if we truly have entered a multi-year period of frequent mini-cycles: Is there tangible evidence of a falling primary growth trend in China, and can this be detected ex-ante rather than ex-post? What are the markers for successful structural reform, and how can progress be tracked in real-time? These are of course difficult questions to answer, and our thoughts are likely to evolve as more evidence presents itself. However, for now, we note the following: Chart 4 presents some evidence of declining potential growth in China, or more precisely a decline in the natural rate of interest. The chart shows that the rise in the weighted average lending rate since late-2016 was relatively minor compared with levels that have prevailed over the past decade, and yet it is clear that it succeeded in materially slowing the investment-driven sectors of China’s economy. Chart 4There Is Some Evidence That China's Natural Rate Of Interest Has Declined

There Is Some Evidence That China's Natural Rate Of Interest Has Declined

There Is Some Evidence That China's Natural Rate Of Interest Has Declined

We also presented some evidence in our November 21 Weekly Report showing that China’s monetary policy transmission mechanism is impaired.5 Chart 5 shows that the recent decline in interbank repo rates implies that average lending rates are set to decline materially over the coming months; measuring the strength of the reaction in the old economy to this decline will provide investors with another crucial observation about the responsiveness of the economy to interest rates. Chart 5More Information On The Responsiveness Of The Economy To Interest Rates Will Soon Emerge

More Information On The Responsiveness Of The Economy To Interest Rates Will Soon Emerge

More Information On The Responsiveness Of The Economy To Interest Rates Will Soon Emerge

Concerning potential signposts of successful structural reform, signs that the government is about to undertake a big-bang cleanup and reorganization of China’s SOEs, one that involves the large-scale transfer of bad SOE debts to the public sector, would obviously be the primary event for investors to watch for. We assume that this will not occur over the coming few years barring a major crisis. At the firm level, non-trivial deleveraging, privatization/incorporation, material capital injection/withdrawal, material divestment of non-core fixed assets and (to a lesser degree) reduction in the wage bill relative to the industry have all shown themselves to be significantly related to the odds of a “zombie” firm returning to a healthy financial state.6 Even quiet signs that SOEs may be going through this process would be a positive indication of the potential for reform. At the macro level, our signposts of successful structural reform would be indications that SOE return on assets is set to rise back above borrowing costs (because of a material rise in the former, not a significant decline in the latter), tangible evidence of passive deleveraging (debt to nominal GDP falling because of a sustained rise in the latter), and a structural rise in the presence of private firms in China’s economy. Chart 6 shows that, at least in the case of the latter, progress appears elusive. Chart 6The Size Of The Private Sector In China Is Now Moving In The Wrong Direction

The Size Of The Private Sector In China Is Now Moving In The Wrong Direction

The Size Of The Private Sector In China Is Now Moving In The Wrong Direction

Over the shorter-term, global investors are strongly focused on whether we are about to enter another mini-cycle upswing, a view that we have recently argued against. We presented our base case view for 2019 in our December 5 Weekly Report2, which is that growth will modestly firm in the second half of 2019 and will provide a somewhat stronger demand backdrop for commodities and emerging economies that sell goods to China. But we underscore that the character of the improvement is likely to be materially different than what occurred in 2016, implying that investors betting on substantial returns from China-related financial assets next year are likely to be disappointed. Transitioning To A Services-Oriented Economy: There Is No Magic Wand Part of the structural reform agenda articulated by Xi Jinping involves transitioning China's economy towards the tertiary sector (services). Services activity, in general, tends to have higher added value than manufacturing, construction, and raw material extraction, and it is hoped that a more services-oriented economy will increase China’s per capita GDP and help the country escape the middle-income trap. Chinese policymakers have been very clear about their intention to promote this shift and have emphasized their need to do so quickly, but have not been very clear about how they plan to do so. Admittedly, there is some evidence to suggest that this trend has already begun: Chart 7 shows that tertiary industry GDP has risen as a share of overall GDP by about 7.5 percentage points since 2010, tertiary industry electricity consumption as a share of total is rising steadily, and the market capitalization of information and communication technology-related sectors has risen in China’s domestic and investable equity market (sharply in the case of the latter).7 Chart 7Some Signs Of A Move Towards Services...

Some Signs Of A Move Towards Services...

Some Signs Of A Move Towards Services...

However, BCA’s China Investment Strategy service has been and remains quite skeptical about the likely pace of this transition, which raises deep questions about China’s growth model over the coming 2-3 years: Chart 8 breaks down the increase in tertiary industry GDP as a share of total from 2010 – 2017 into individual sectors.8 The chart shows that finance-related sectors (financial intermediation, leasing & business services, and real estate) accounted for nearly half of the increase in services GDP over the period. It seems difficult to expect that this trend will continue in an environment where the government is trying to contain financial sector risk.

Chart 8

Chart 8 shows that tech-related sectors accounted for the second largest increase in tertiary industry GDP over the period, which is not surprising given the data shown in panel 3 of Chart 7. However, there are three problems with assuming that China’s tech sector will expand at a very rapid pace from current levels. First, Chart 9 makes it clear that the incubation period for China’s largest two technology companies by market capitalization was quite long. Alibaba and Tencent were both formed nearly 20 years ago, and only recently gained significant traction. Second, neither of these firms appears to have succeeded because of Chinese industrial policy, underscoring the importance of dynamic, competitive, private markets in driving innovation. Third, other successful examples of “breakthrough” state support for industries show that the process is not a rapid one. In the U.S. between 1978 and 1992, the U.S. Department of Energy invested in the Eastern Gas Shale Program, which contributed somewhat to the development of fracking technology used in shale oil & gas production today. Chart 10 shows how long it took for this program to bear fruit: gas production began to trend higher 12 years after the end of the program, whereas it took nearly two decades for oil production to begin to move higher. And even in this case, the role of private industry in commercializing the technology was overwhelmingly dominant. Chart 9The Incubation Period Of China's Major Tech Success Stories Was Quite Long

The Incubation Period Of China's Major Tech Success Stories Was Quite Long

The Incubation Period Of China's Major Tech Success Stories Was Quite Long

Chart 10The Dividends From State-Assisted R&D Can Take A Long Time To Occur

The Dividends From State-Assisted R&D Can Take A Long Time To Occur

The Dividends From State-Assisted R&D Can Take A Long Time To Occur

It is encouraging to see that education spending in China has increased as a share of GDP over the past several years, as services activity typically requires a highly educated workforce as an input. But China’s post-secondary educational attainment (defined here as the share of 25-34 year olds with tertiary education) appears to be too low to make a meaningful leap over the next 2-3 years (Chart 11). We acknowledge that China’s educational achievement ranks quite highly relative to the world, and this speaks to the high quality of skilled labor in China. However, for now, China’s attainment rate appears to be too low for the country to rapidly shift to services.

Chart 11

Finally, Chart 12 shows that while tertiary industry electricity consumption is rising as a share of total, it remains small compared with secondary industry consumption. This underscores that China’s shift to a truly-services oriented economy is something that will take a considerable amount of time. What does a slow transition from secondary to tertiary industry mean for investors? To us, it either raises the risk that: Chart 12A Long Way To Go

A Long Way To Go

A Long Way To Go

policymakers will have to rely on China’s old growth model for longer than they intend, or that Chinese growth will slow considerably more over the coming few years than investors currently expect. In the first case, policymakers may be on a collision course with the reality of poor financial health among SOEs, which as we noted earlier already have a negative net return from leveraging. In the second case, the threat is clear: China’s contribution to global growth could decline sharply, with potentially severe consequences for China-related financial assets. Cheap(er) Chinese Stocks: A Great Long-Term Buying Opportunity? We have received several questions from clients over the past few months asking whether they have been presented with a great long-term buying opportunity for Chinese stocks, even if cyclical economic conditions are set to weaken from current levels. Chart 13In The U.S., Valuation Predicts Long-Term Returns Quite Successfully

In The U.S., Valuation Predicts Long-Term Returns Quite Successfully

In The U.S., Valuation Predicts Long-Term Returns Quite Successfully

This is a valid line of inquiry. Over a 6-12 month time horizon, valuation rarely drives asset returns, and we recently argued against the view that valuation could act as an overwhelming rally catalyst for Chinese stocks in 2019. However, we agree that valuation should be increasingly considered as one’s time horizon expands. Chart 13 shows that valuation has been a powerful predictor of 10-year future performance for the U.S. equity market, and Chart 14 shows that the forward P/E ratio for both domestic and investable Chinese stocks has certainly improved over the past several months. In relative terms, Chinese stocks are not as cheap as they have ever been, but haven’t usually been cheaper (at least over the past decade). This is particularly true for the A-share market (Chart 15). Chart 14Chinese Stocks Are Now Considerably Cheaper Than A Year Ago...

Chinese Stocks Are Now Considerably Cheaper Than A Year Ago...

Chinese Stocks Are Now Considerably Cheaper Than A Year Ago...

Chart 15...Although They Have Been Cheaper In Relative Terms

...Although They Have Been Cheaper In Relative Terms

...Although They Have Been Cheaper In Relative Terms

We struggle to answer the question, because while valuation usually predicts future returns quite well, deviations from this relationship can exist. Chart 13 shows that material differences between the actual and predicted 10-year returns existed during the 1970s/early-1980s and as well during the late-1990s, and would have as well in 2008/2009 had the valuation extremes of the late-1990s not lined up so well with the timing of the global financial crisis a decade later. In short, cheap stocks can be cheap for a reason, and the structural issues that we noted above certainly highlight the potential for the next 10-years of Chinese equity market performance to be anomalous relative to what would normally be implied by current valuation. For now, the best answer we can provide is that Chinese stocks are a great long-term buy for investors who do not share our structural concerns. On a risk-adjusted basis, we do not find the value proposition to be compelling, meaning that our recommended multi-year allocation to Chinese stocks is neutral. But we will be watching closely over the coming few years for signs of successful structural reform as detailed above, and we are likely to upgrade our structural recommendation on any material progress, particularly if that progress involves a cyclical deterioration in the economy that further cheapens equities. Stay tuned! Jonathan LaBerge, CFA, Vice President Special Reports jonathanl@bcaresearch.com Footnotes 1 Pease see The Bank Credit Analyst “OUTLOOK 2019: Late-Cycle Turbulence”, dated November 27, 2018, available at cis.bcaresearch.com. 2 Pease see China Investment Strategy Weekly Report “2019 Key Views: Four Themes For China In The Coming Year”, dated December 5, 2018, available at cis.bcaresearch.com. 3 Pease see China Investment Strategy Special Report “The Great Debate: Does China Have Too Much Debt Or Too Much Savings? ”, dated March 23, 2017, available at cis.bcaresearch.com. 4 Pease see China Investment Strategy Special Report “Chinese Policymakers: Facing A Trade-Off Between Growth And Leveraging”, dated August 29, 2018, available at cis.bcaresearch.com. 5 Pease see China Investment Strategy Weekly Report “Trade Is Not China’s Only Problem”, dated November 21, 2018, available at cis.bcaresearch.com. 6 IMF Working Paper WP/17/266 “Resolving China’s Zombies: Tackling Debt and Raising Productivity” 7 Note that we have included the consumer discretionary sector in Chart 8 owing to the recent GICS sector changes that have included e-commerce providers such as Alibaba in the discretionary sector. 8 Note that 2016 is the most recent data point for healthcare & social security, education, scientific research & technology services, public management & social organizations, and miscellaneous others. However, their change from 2010 – 2017 reflects almost all of the change in the sum of these categories from 2010 – 2017. Cyclical Investment Stance Equity Sector Recommendations

Highlights So What? Our best and worst calls of 2018 cast light on our methodology and 2019 forecasts. Why? Our clients took us to task for violating our own methodology on the Iranian oil sanctions. Sticking to our guns would have paid off with long Russian equities versus EM. We correctly called China’s domestic policy, the U.S.-China trade war, Europe, the U.S. midterms, and relative winners in emerging markets. Feature It has been a tradition for BCA’s Geopolitical Strategy, since our launch in 2012, to highlight our best and worst forecasts of the year.1 This will also be the final publication of the year, provided that there is no global conflagration worthy of a missive between now and January 9, when we return to our regular publication schedule. We wish all of our clients a great Holiday Season. And especially all the very best in 2019: lots of happiness, health, and hefty returns. Good luck and good hunting. The Worst Calls Of 2018 A forecasting mistake is wasted if one learns nothing from the error. This is why we take our mistakes seriously and why we always begin the report card with our zingers. Our overall performance in 2018 was … one of our best. The successes below will testify to this. However, we made three notable errors. A Schizophrenic Russia View Our worst call of the year was to panic and close our long Russian equities relative to emerging markets trade in the face of headline geopolitical risks. In early March, we posited that Russia was a “buy” relative to the broad EM equity index due to a combination of cheap valuations, strong macro fundamentals, orthodox policy, and an end to large-scale geopolitical adventurism. This call ultimately proved to be correct (Chart 1). Chart 1Russian Stocks Outperformed In The End

Russian Stocks Outperformed In The End

Russian Stocks Outperformed In The End

What went wrong? The main risk to our view, that the U.S. Congress would pursue an anti-Russia agenda regardless of any Russian sympathies in the Trump White House, materialized in the wake of the poisoning of former Russian military intelligence officer Sergei Skripal with a Novichok nerve agent in the United Kingdom. As fate would have it, the incident occurred just before our bullish report went to clients! The ensuing international uproar and sanctions caused a selloff. Our bullish thesis did not rest exclusively on geopolitics, but a thaw in West-Russia relations did form the main pillar of the view. Our Russia Geopolitical Risk Index, which had served us well in the past, was pricing as low of a level of geopolitical risk as one could hope for in the post-Crimea environment (Chart 2). Naturally the measure jumped into action following the Skripal incident. Chart 2Geopolitical Risk Was Low Prior To Skripal

Geopolitical Risk Was Low Prior To Skripal

Geopolitical Risk Was Low Prior To Skripal

The timing of our call was therefore off, but we should have stuck with the overall view. The U.S. imposed preliminary sanctions that lacked teeth. While Washington accepted the U.K.’s assessment that Moscow was behind the poisoning, the weakness of the sanctions also signaled that the U.S. did not consider the incident worthy of a tougher position. There are now two parallel sanction processes under way. The first round of sanctions announced in August gave Russia 90 days to comply and adopt “remedial measures” regarding the use of chemical and biological weapons. On November 9, the U.S. State Department noted that Russia had not complied with the deadline. The U.S. is now expected to impose a second round of sanctions that will include at least three of six punitive actions: Opposition to development aid and assistance by international financial institutions (think the IMF and the World Bank); Downgrading diplomatic relations; Additional restrictions on exports to Russia (high-tech exports have already been barred by the first round of sanctions); Restrictions on imports from Russia; A ban on landing rights in the U.S. for Russian state-owned airlines; Prohibiting U.S. banks from purchasing Russian government debt. While the White House was expected to have such sanctions ready to go on the November 9 deadline, it has dragged its feet for almost two months now. This suggests that President Trump continues to hold out for improved relations with President Putin. A visit by President Putin to Washington remains possible in Q1 2019. As such, we would expect the White House to adopt some mix of the first five items on the above list, hardly a crushing response from Moscow’s perspective. The U.S. Congress, however, has a parallel process in the form of the Defending American Security from Kremlin Aggression Act of 2018 (DASKAA). Introduced in August by Senator Lindsey Graham, a Russia hawk, the legislation would put restrictions on Americans buying Russian sovereign debt and curb investments in Russian energy projects. The bill also includes secondary sanctions on investing in the Russian oil sector, which would potentially ensnare European energy companies collaborating with Russia in the energy sector. There was some expectation that Congress would take up the bill ahead of the midterm election, but nothing came of it. Even with the latest incident – the seizing of two Ukrainian naval vessels in the Kerch Strait – we have yet to see action. While we expect the U.S. to do something eventually, the White House approach is likely to be tepid while the congressional approach may be too draconian to pass into law. And with Democrats about to take over the House, and likely demand even tougher sanctions against Russia, the ultimate legislation may be too bold for President Trump to sign into legislation. The point is that Russia has acted antagonistically towards the West in 2018, but in small enough increments that the response has been tepid. Given the paucity of Russian financial and trade links with the U.S., Washington’s sanctions would only bite if they included the dreaded “secondary sanction” implications for third party sovereigns and firms – particularly European, which do have a lot of business in Russia. This is highly unlikely without major Russian aggression. We cannot completely ignore the potential for such aggression in 2019, especially with President Putin’s popularity in the doldrums (Chart 3) and a contentious Ukrainian election due for March 31. However, we outlined the constraints against Russia in 2014, amidst the Ukrainian crisis, and we do not think that these constraints have been reduced (they may have only grown since then). Chart 3Non-Negligible Risk Of Russian Aggression

Non-Negligible Risk Of Russian Aggression

Non-Negligible Risk Of Russian Aggression

Regardless of the big picture for 2019, we could have faded the risks in 2018 and stuck to the fundamentals. Russia is up 17.2% against EM year-to-date. The lesson here, therefore, is to find re-entry points into a well-founded view despite market volatility. Chart 1 shows that Russian equities climbed the proverbial “wall of worry” relative to EM in 2018. Doubting Jair Bolsonaro Our list of mistakes keeps us in the EM universe where we underestimated Jair Bolsonaro’s chances of winning the presidency in Brazil. The answer to the question we posed in the title of our September report – “Brazil: Can The Election Change Anything?” – was a definitive “yes.” Since the publication of that report, BRL/USD is up 2.9% and Brazilian equities are up 18.5% relative to EM (Chart 4). Chart 4Bolsonaro Rally Losing Its Luster Already

Bolsonaro Rally Losing Its Luster Already

Bolsonaro Rally Losing Its Luster Already

To our credit, the question of Bolsonaro’s electoral chances elicited passionate and pointed internal debate. But our clients did not see the internal struggle, just the incorrect external output! A bad call is a bad call, no matter how it is assembled on the intellectual assembly line. That said, we still think that our report is valuable. It sets out the constraints facing Bolsonaro in 2019. He has to convince the left-leaning median voter that meaningful pension reform is needed; bully a fractured Congress into painful structural reforms; and overcome an unforgiving macro context of tepid Chinese stimulus and a strong USD. If the Bolsonaro administration wastes the good will of the investment community over the next six months, we expect the market’s punishment to be swift and painful. In fact, Chart 4 notes that the initial Bolsonaro rally has already lost most of its shine. Brazilian assets are still up since the election, but the gentle slope could become a steep fall if Bolsonaro stumbles. The market is priced for political perfection. To be clear, we are not bearish on Bolsonaro. We believe that, relative to EM, he will be a positive for Brazil. However, the market is currently betting that he will win by two touchdowns, whereas we think he will squeak by with a last-second field goal. The difference between the two forecasts is compelling and we have expressed it by being long MXN/BRL.2 Not Sticking To Our Method In The Case Of Iran Throughout late-2017 and 2018 we pointed out that President Trump’s successful application of “maximum pressure” against North Korea could become a market-relevant risk if he were emboldened to try the same strategy against Iran. For much of the year, this view was prescient. As investors realized the seriousness of President Trump’s strategy, a geopolitical risk premium began to seep into oil prices, as illustrated in Chart 5 by the red bar.

Chart 5

Every time we spoke to clients or published reports on this topic, we highlighted just how dangerous a “maximum pressure” strategy would be in the case of Iran. We stressed that Iran could wreak havoc across Iraq and other parts of the Middle East and even drive up oil prices to the point of causing a “geopolitical recession in 2019.” In other words, we stressed the extraordinary constraints that President Trump would face. To their credit many of our clients called us out on the inconsistency: our market call was über bullish oil prices, while our methodology emphasized constraints over preferences. We were constantly fielding questions such as: Why would President Trump face down such overwhelming constraints? We did not have a very good answer to this question other than that he was ideologically committed to overturning the Iranian nuclear deal. In essence, we doubted President Trump’s own ideological flexibility and realism. That was a mistake and we tip our hat to the White House for recognizing the complex constraints arrayed against it. President Trump realized by October how dangerous those constraints were and began floating the idea of sanction waivers, causing the geopolitical risk premium to drain from the market (Chart 6). To our credit, we highlighted sanction waivers as a key risk to our view and thus took profit on our bullish energy call early. Chart 6Sanction Waivers Caused A Collapse In Oil Prices

Sanction Waivers Caused A Collapse In Oil Prices

Sanction Waivers Caused A Collapse In Oil Prices