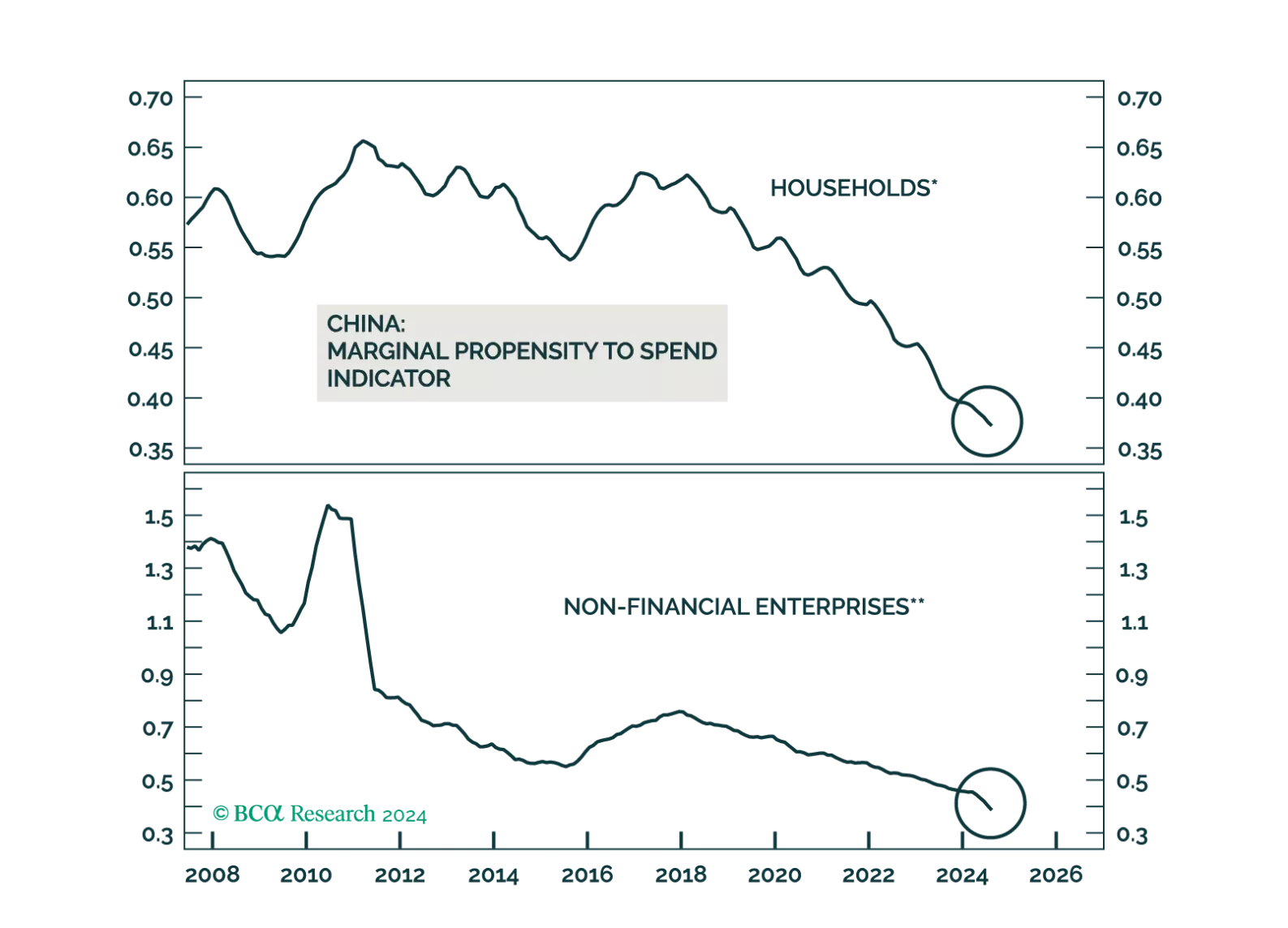

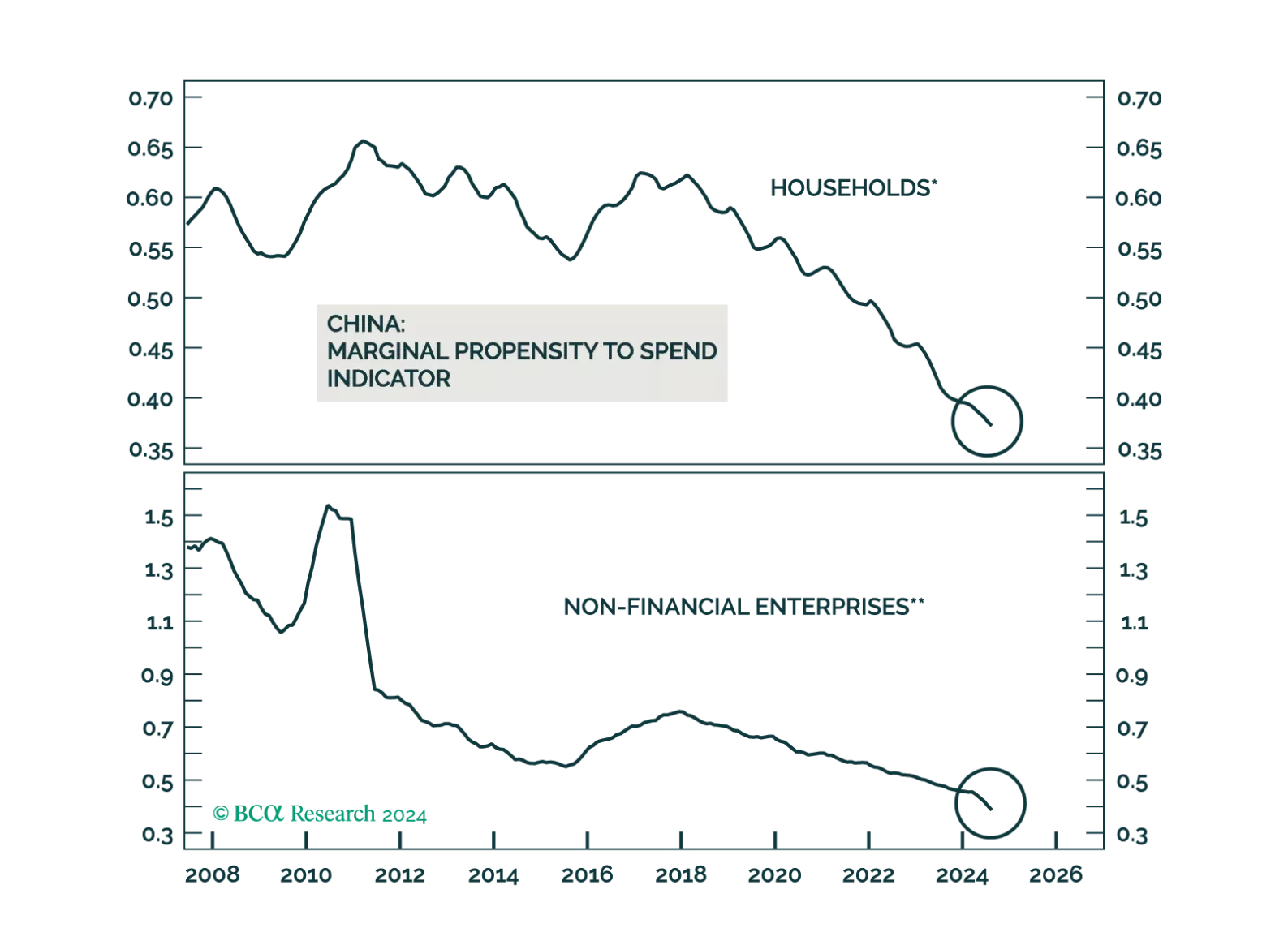

China

China’s Politburo announcement is likely to lead to a repricing of China’s growth in the near-term. Read how investors can hedge against this potent threat to our defensive investment stance.

We believe the PBoC’s recent policy stimulus might bolster investor confidence, potentially stabilize onshore Chinese equity prices, and provide modest support to offshore stocks. However, they are unlikely to significantly boost economic growth in the mainland.

We believe the PBoC’s recent policy stimulus might bolster investor confidence, potentially stabilize onshore Chinese equity prices, and provide modest support to offshore stocks. However, they are unlikely to significantly boost economic growth in the mainland.

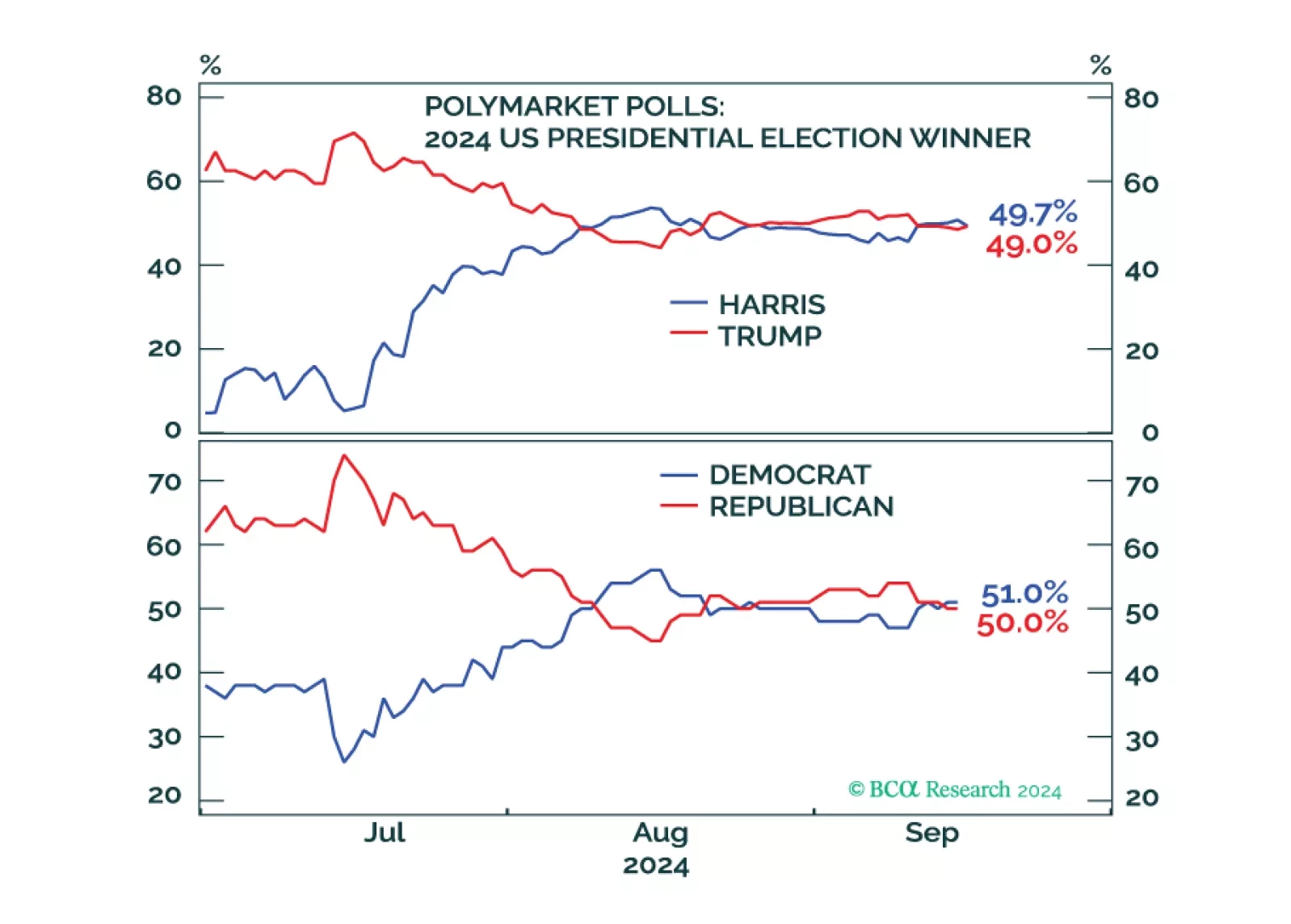

Investors should de-risk tactically in expectation of shocks and surprises ahead of the US election and an uncertain aftermath. Democratic victory with a gridlocked Congress is our base case but would bring minor tax hikes and nuclear brinksmanship with Russia. A Republican single-party sweep offers huge tax cuts but also a global trade war. Recession looms regardless.