China

The Chinese economic data in its totality was uninspiring in August. Industrial production and retail sales growth decelerated year-on-year and corroborate the message from August’s import and credit growth data that domestic demand remains lackluster.…

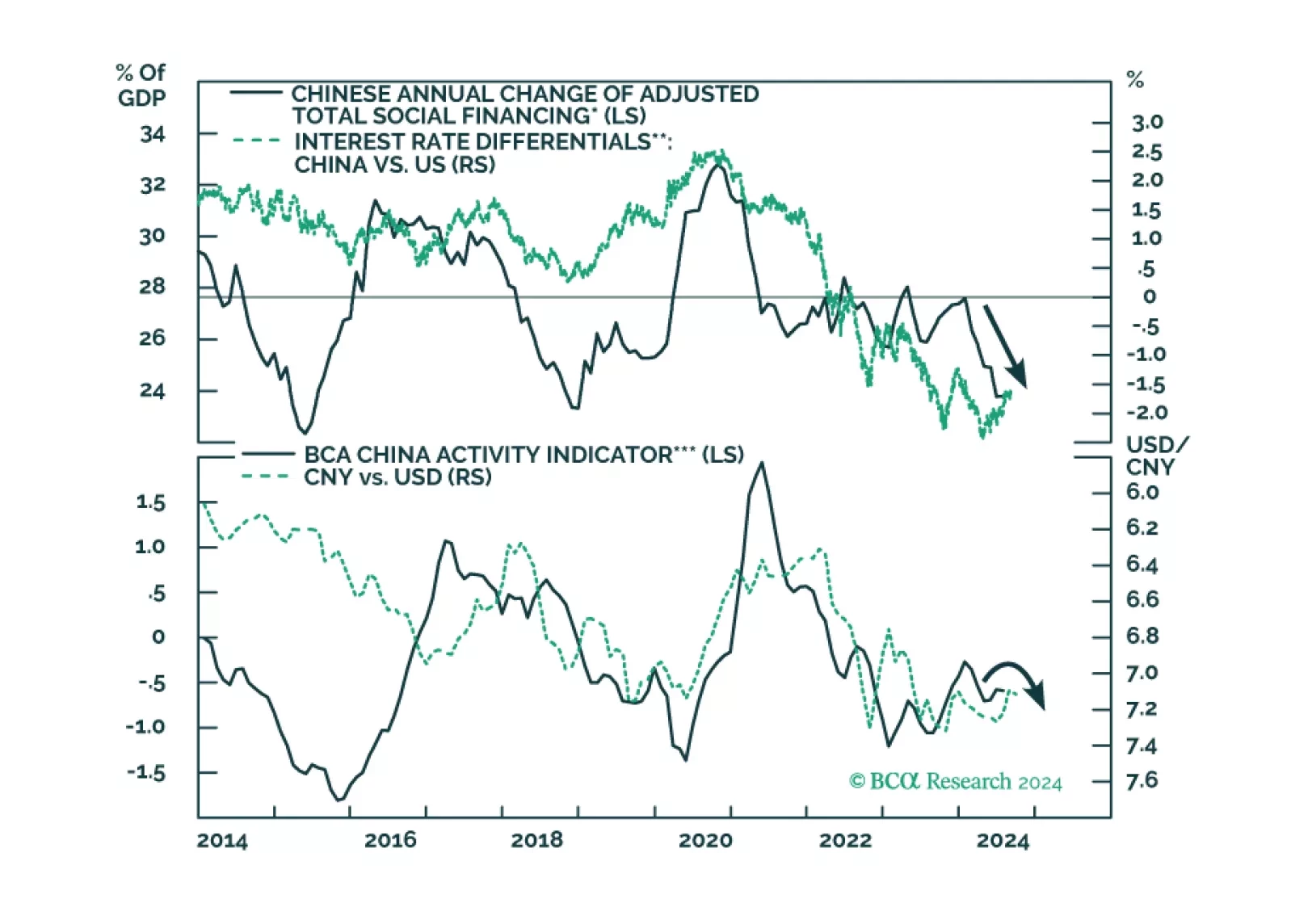

Subdued demand for credit among Chinese private-sector businesses and households persisted through August. Outstanding loan growth decelerated from 8.7% y/y to 8.5%. Moreover, M1’s contraction deepened, from 6.6% to 7.3%. The lackluster appetite for…

Volkswagen’s CEO has been making the point that the market for European carmakers has been deteriorating. Earlier last week, he went on to make a rather pointed reference at Chinese EV manufacturers. He was quoted saying that, "The pie has become…

The US suffers from enough imbalances to produce a mild recession. Unfortunately, such a recession could lead to a significant bear market in stocks, just as it did during the very mild 2001 recession.

According to BCA Research’s China Investment Strategy service, the Fed’s upcoming rate cut will temporarily alleviate some of the downward pressure on the RMB, but beyond the short term the USD will likely rebound in anticipation of a global slowdown. The…

Both the Chinese and US central banks will likely take policy actions in the coming weeks. What is the potential impact of a mortgage rate cut on China’s household consumption and the broader economy? Will the anticipated Fed easing cycle further lift the RMB exchange rate versus the US dollar?

Chinese export growth in USD terms accelerated from 7.0% y/y to a larger-than-expected 8.7% in August. China’s exports to its major trading partners (US, EU and ASEAN) were all growing in August on a year-on-year basis, though at a decelerating pace in the US…

China’s CPI and PPI both surprised to the downside in August. Consumer prices grew from 0.5% y/y to 0.6%, below the 0.7% anticipated. However, a 2.8% y/y surge in food prices (the fastest pace so far this year) overstates this headline figure. Core CPI…

Global semiconductor stocks have returned 50% YTD in USD terms, and a whopping 200% since their September 2022 lows. However, they may have peaked back in July. Our Emerging Market strategists highlight a significant bifurcation between the revenues of…