China

Our Portfolio Allocation Summary for September 2024.

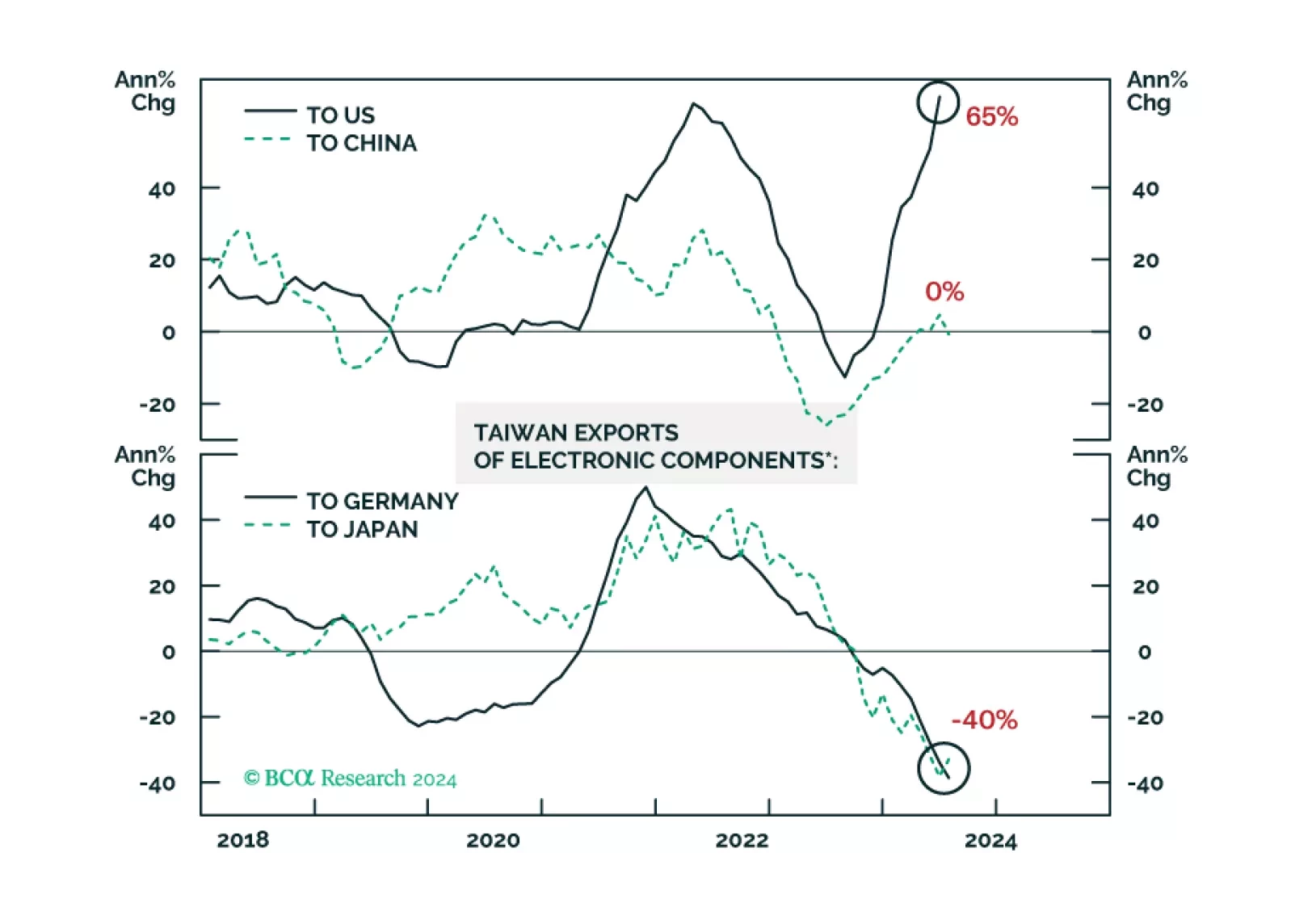

There has been a decoupling within the global semiconductor industry. Demand for AI and advanced chips has been booming. Yet, sales of legacy and non-AI semiconductors have failed to recover. Given their spectacular run-up, share prices of high-end and AI-chip producers might continue selling off even if their sales continue to grow rapidly.

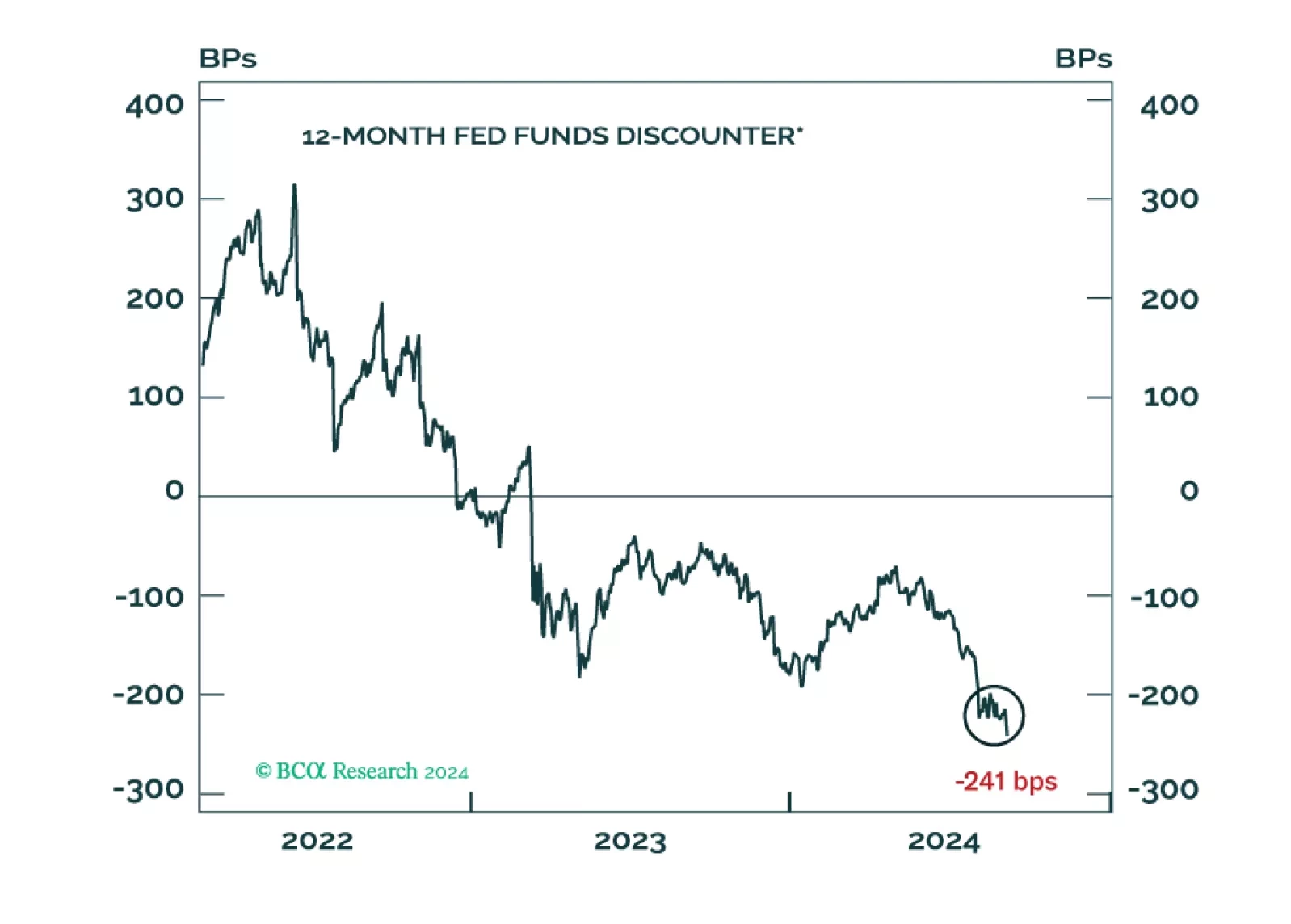

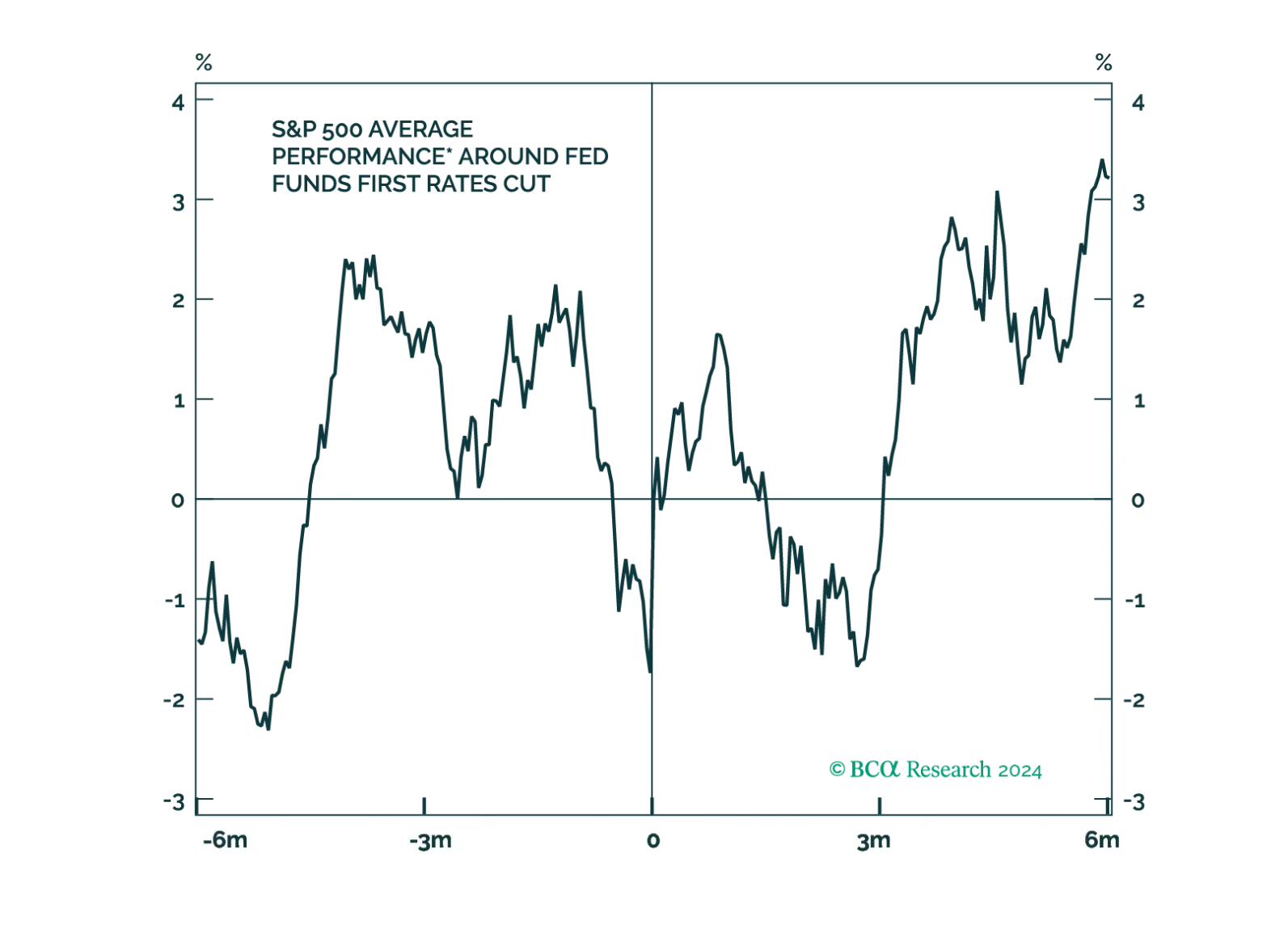

Even after the Fed cuts rates, policy will remain restrictive for some time. Moreover, in history, stocks have tended to fall around the first rate cut. We remain cautious on the outlook for the economy and risk assets.

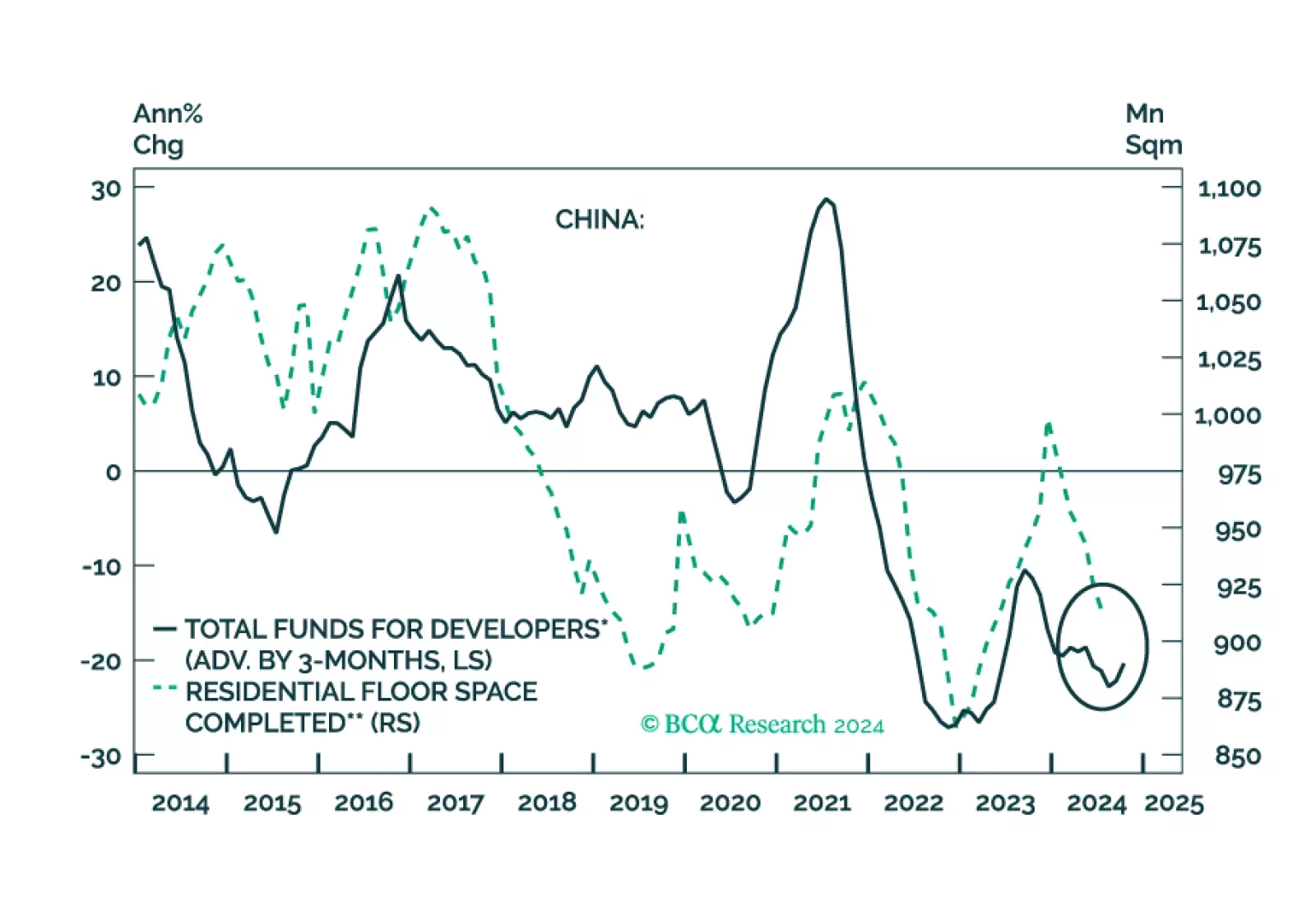

Chinese property developers will require at least RMB 500 billion in additional government funding to prevent further declines in housing completions for the rest of 2024. However, without addressing the underlying challenges, any new rescue measures similar to those announced in May are unlikely to effectively support the real estate market.