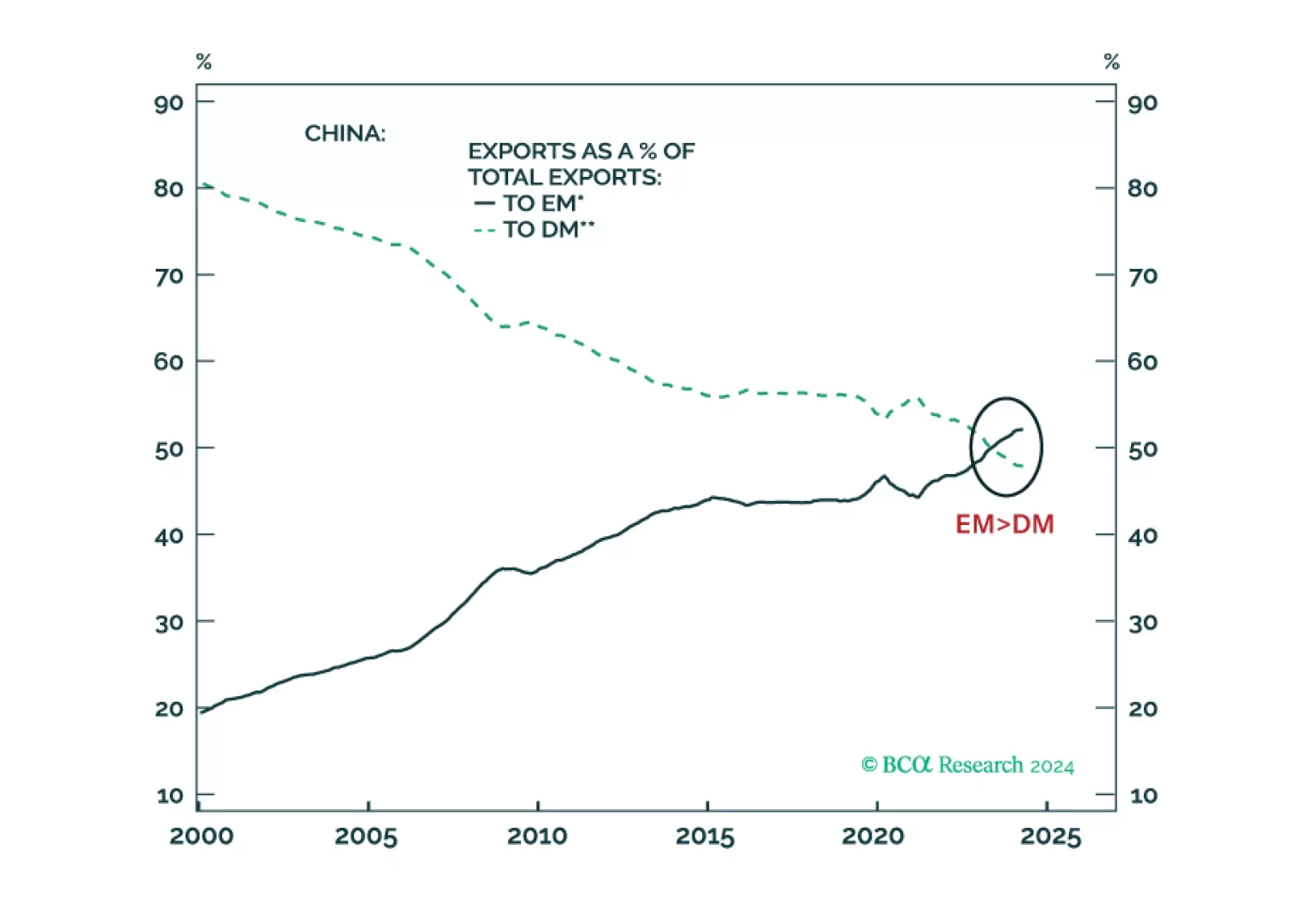

China

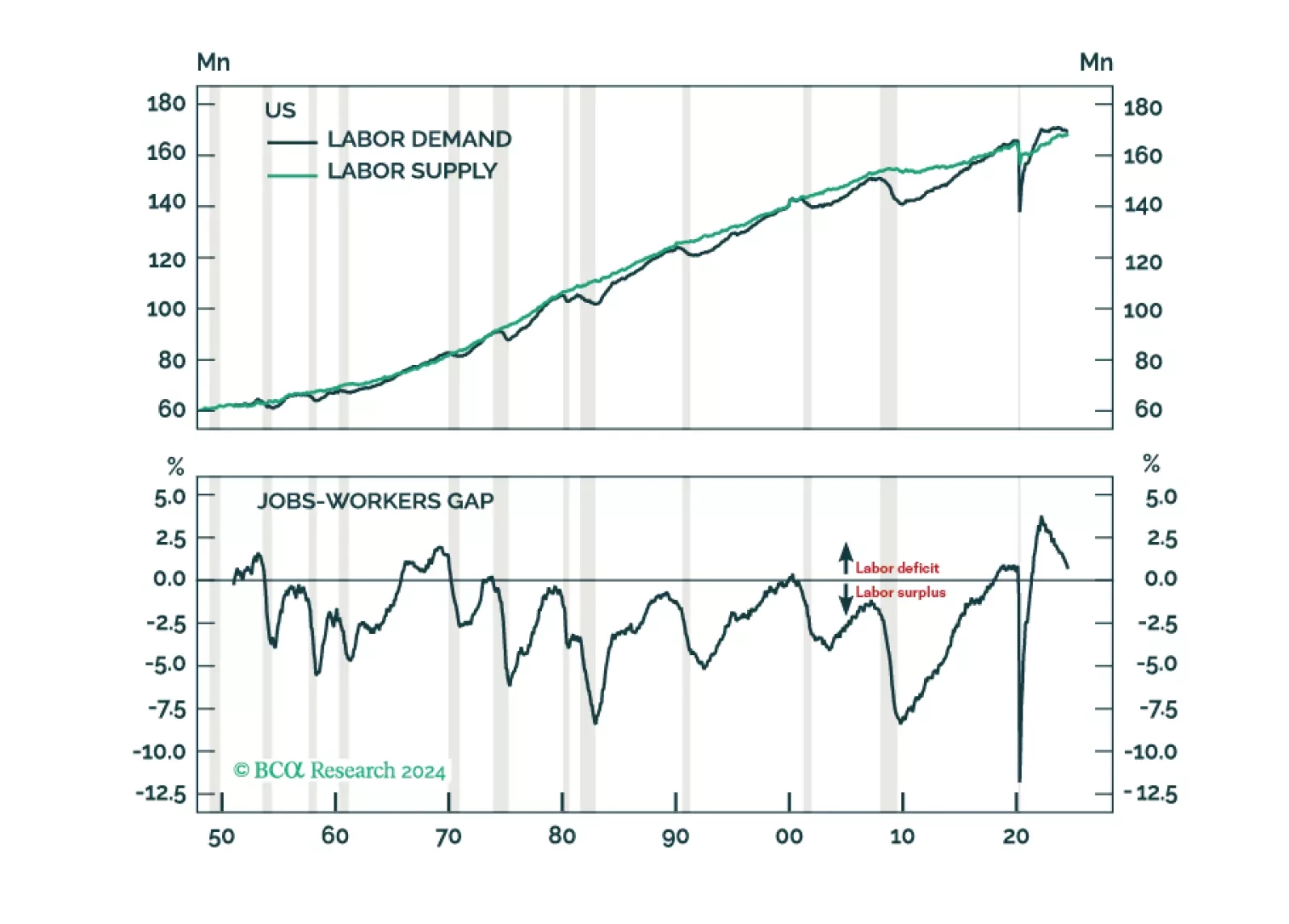

The great US labor market shortage is over. Labor demand will likely fall short of supply by the end of this year, causing unemployment to soar. Neither fiscal nor monetary policy will be able to prevent the coming recession. Investors should underweight stocks and overweight Treasuries.

China has become less reliant on exports to advanced economies, and its products have successfully penetrated developing economies. Exports to the US make up 3% of Chinese GDP, while exports to all developing economies account for 10% of its GDP. China’s trade pivot from advanced to developing economies has economic, political, and geopolitical ramifications.

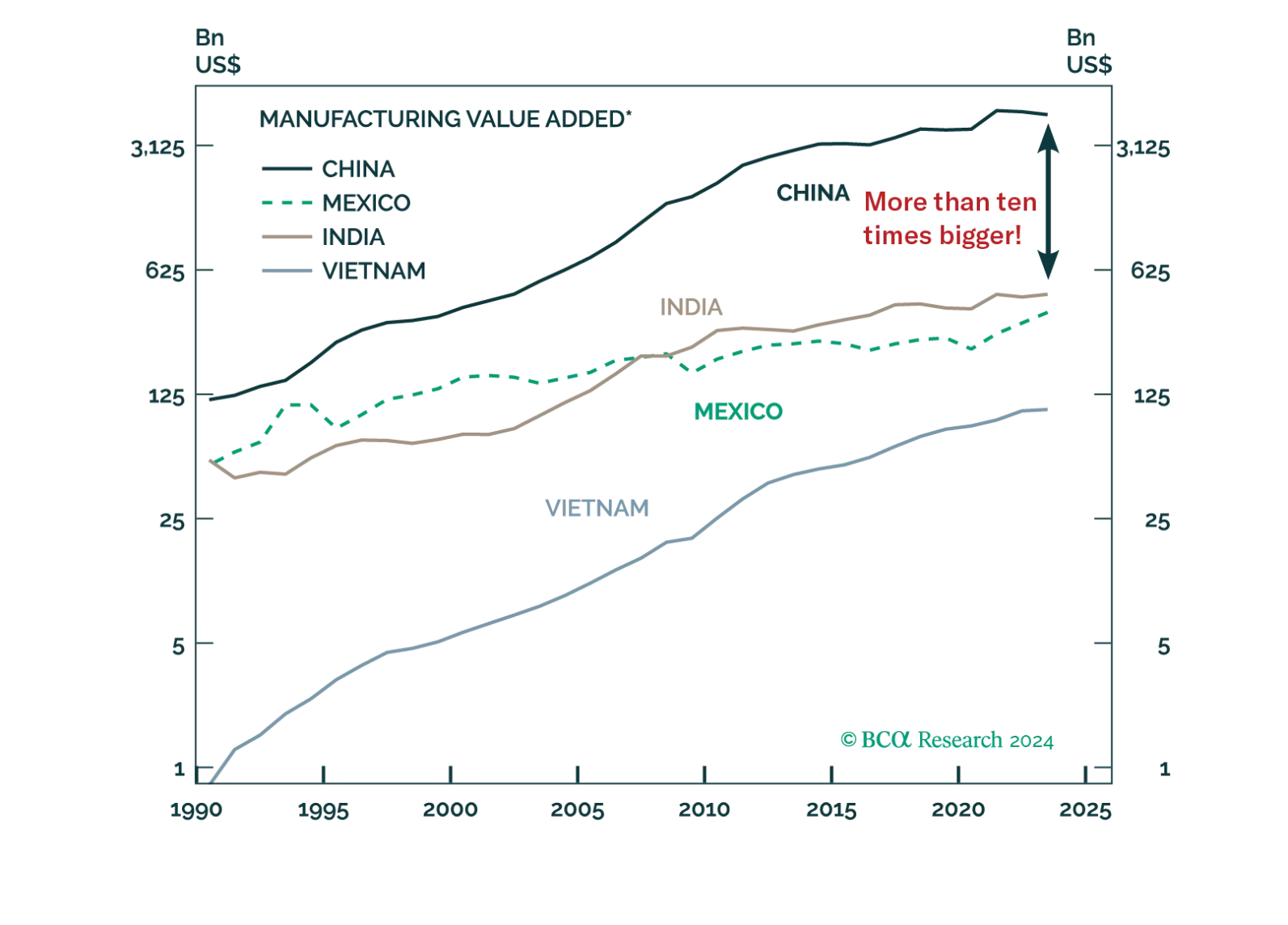

Multinationals are attempting to expand their supply chains beyond China, but the relocation process has been slower than expected. In the coming years, however, geopolitical tensions, changes in China’s business environment, and rising competition from Chinese producers could accelerate multinationals' departure from China.