China

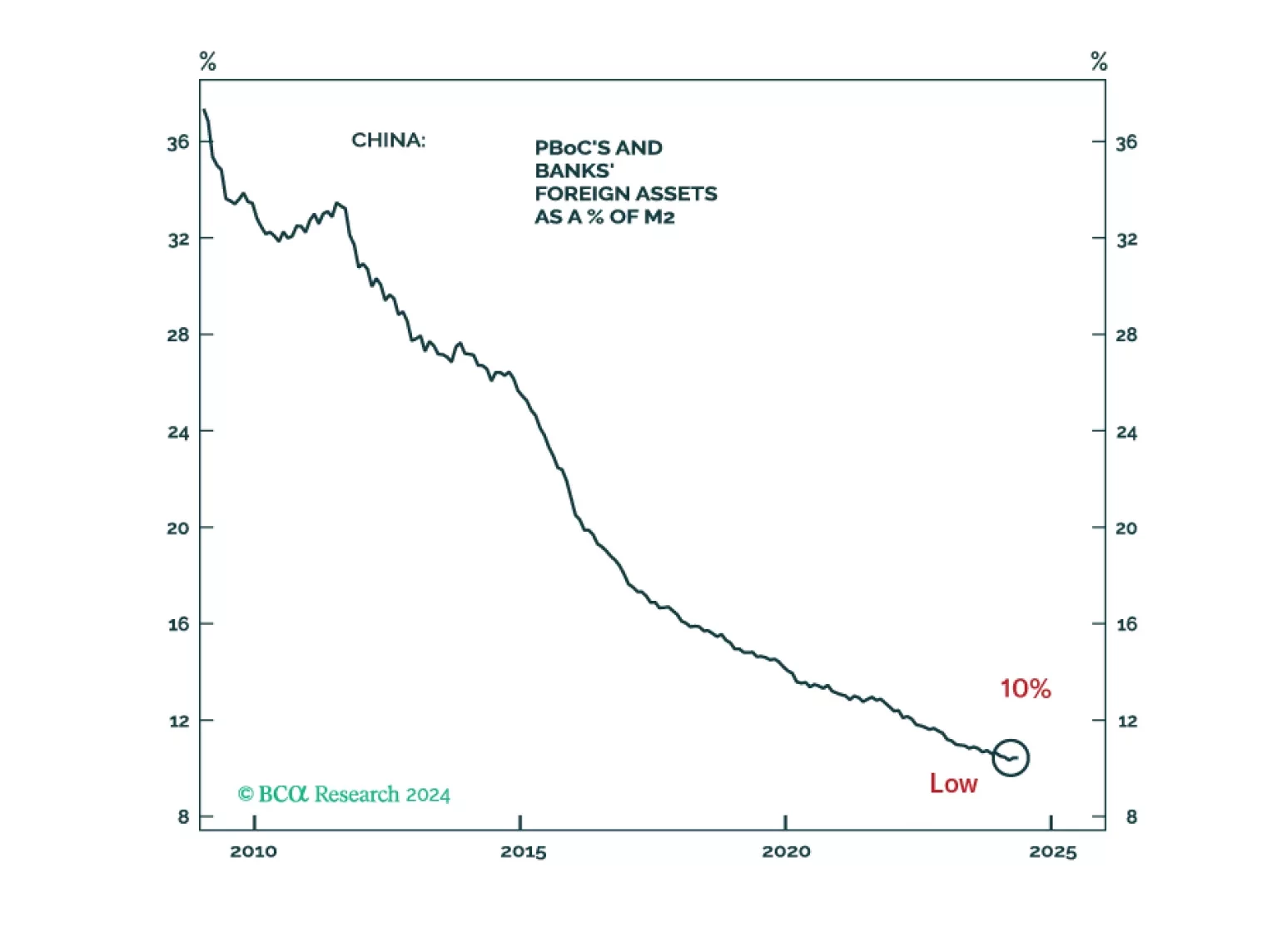

Is the RMB cheap or expensive? Based on trade accounts, the yuan is inexpensive, but the RMB is vulnerable due to capital outflows. Yet, Beijing will not resort to a rapid devaluation for now, and the option of floating the currency is improbable. The PBoC will allow a gradual depreciation of the yuan versus the dollar, say around 5%, in the next six months.

The PBoC appears increasingly uncomfortable with the rapid decline in the Chinese government bond yields. While the PBoC will succeed in temporarily curbing investors’ enthusiasm for bonds, the central bank will be unwilling to raise interest rates and unable to intervene in the bond market in any meaningful and lasting way.

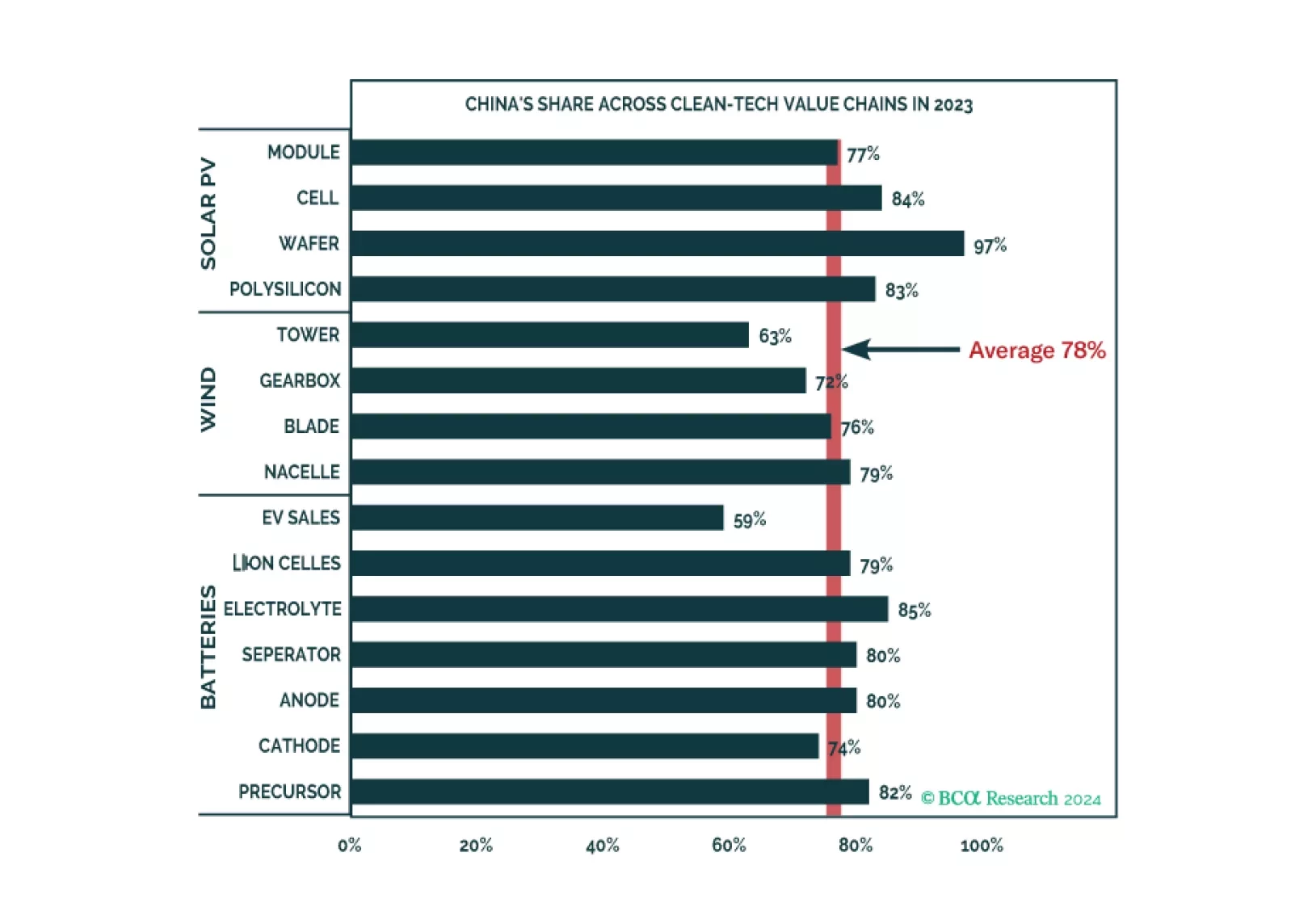

The green energy transition will drive a surge in copper demand over a long-term horizon. However, a better entry point to get long will emerge after the next economic downturn begins.