China

Several economic releases out of China disappointed in April. Retail sales decelerated from 3.1% y/y to 2.3% y/y and fixed asset investment growth slowed from 4.5% YTD y/y to 4.2% YTD y/y. Both were expected to accelerate. Although industrial production…

The stock market will suffer a setback from the weakening labor market and a rebound in US and global policy uncertainty.

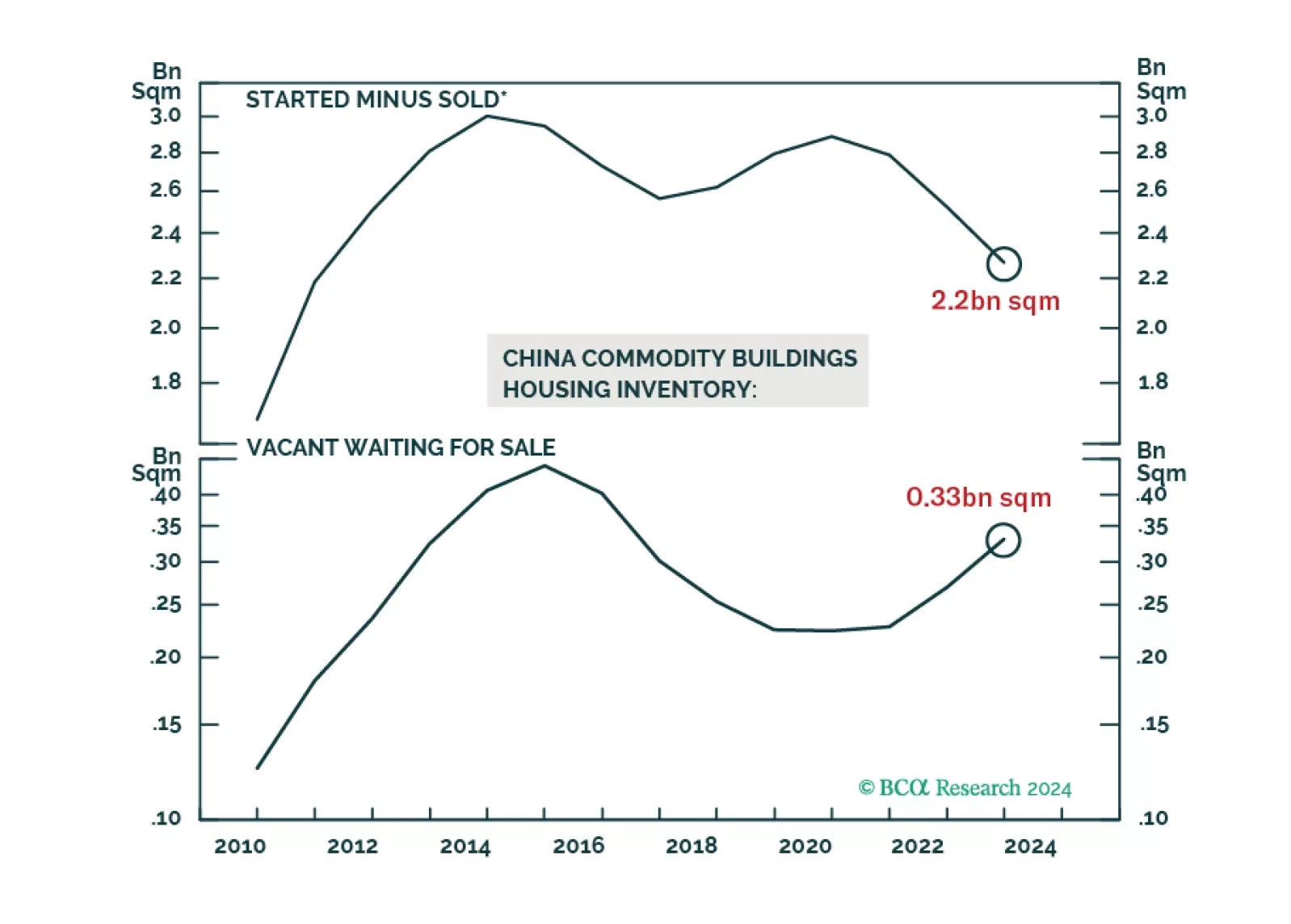

According to BCA Research’s China Investment Strategy service, a decisive turnaround in China’s economy hinges on a revival in the country’s property market. The April 30th Politburo meeting signaled policymakers' intent to restore housing demand and…

A reality check on credit data and announced property sector support measures indicates that the recent surge in Chinese share prices is unjustified based on the country's economic fundamentals.

Chinese aggregate financing, a broad measure of credit, declined on a YTD basis, from CNY 12.9tr to CNY 12.7tr in April, disappointing expectations that it would grow to CNY 13.9tr. Moreover, new loan growth missed expectations (from CNY 9.5tr to CNY 10.2tr)…

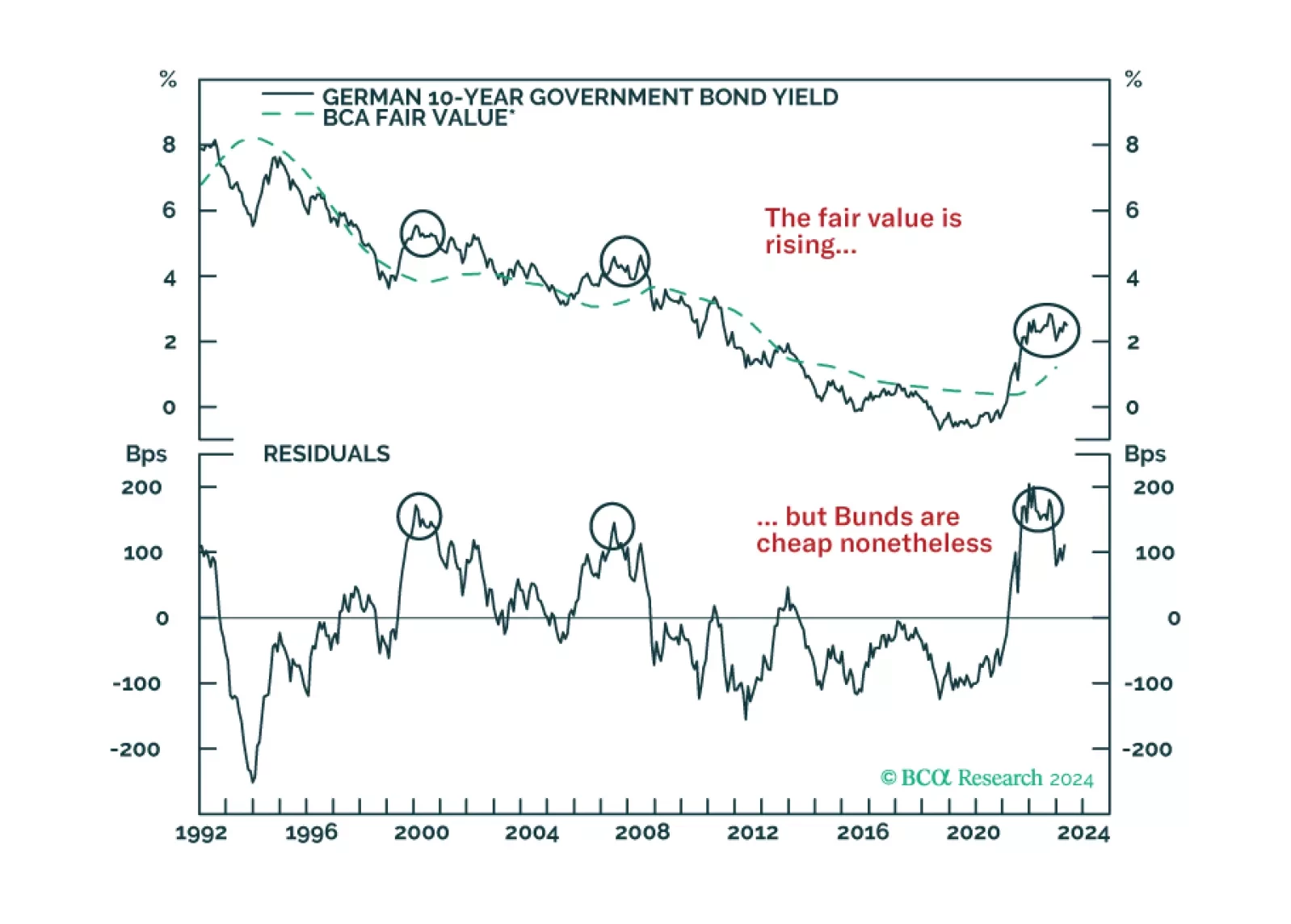

German Bunds have cheapened considerably, and the ECB is about to start cutting rates. Does this combination guarantee immediate profits from buying these bonds?

Upward growth revisions for China and India have led the IMF to recently upgrade its 2024 growth forecast for Asia to 4.5% from 4.2%. The regional growth forecast for 2025 remains unchanged at 4.3%. The IMF now expects the Chinese economy to grow at a 4.6%…

The S&P GSCI broad commodity index has returned 8% year-to-date. Improving investor sentiment has significantly broadened the rally since the beginning of the year. Over 65% of commodities in the index are now trading above their 200-day moving averages,…

The Caixin services and composite PMIs were broadly unchanged in April. The services PMI decreased from 52.7 to 52.5, in line with expectations, while the composite PMI increased from 52.7 to 52.8. Details underscored positive dynamics. New business growth…

Chinese investable stocks have rallied on a combination of investors’ hopes for stimulus, revival in the global manufacturing cycle and cheap valuations. The MSCI China index and the Hang Seng have both gained close to 15% since mid-April. However, our…