China

Mainland residents’ investments in gold, other metals, and Hong Kong-traded stocks are a form of capital outflow. Chinese authorities will counter any excessive capital flight with stricter administrative controls. Thus, markets benefiting from these flows will likely be hurt.

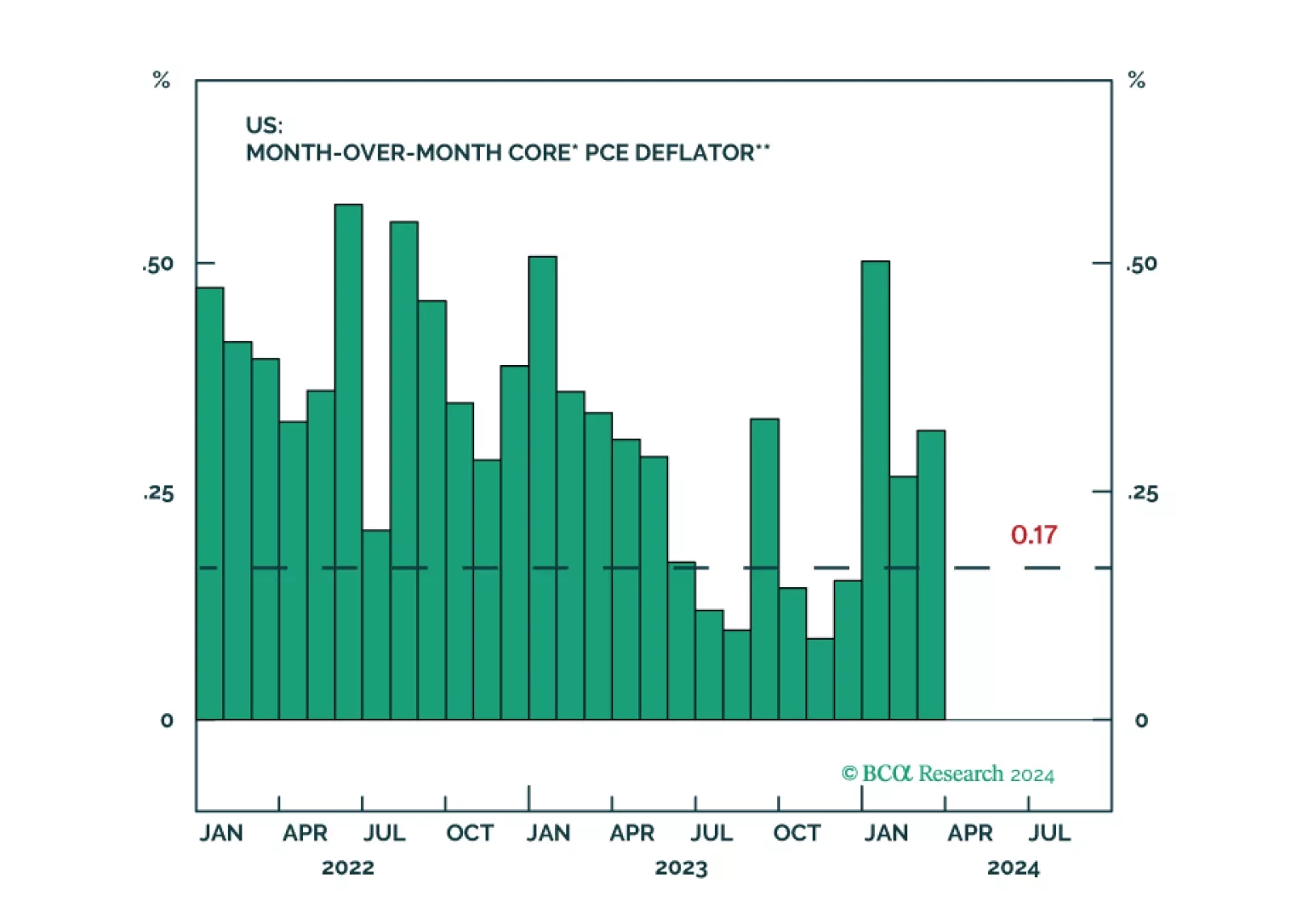

Central banks are in a dilemma whether to prioritize supporting growth or bringing inflation back to target. This is unlikely to end well. Investors should be defensively positioned.

China’s economy is cruising at a very low altitude. The odds are that China’s equity rebound is running out of time. The RMB will continue to depreciate versus the US dollar in the coming months, albeit the pace may be modest.

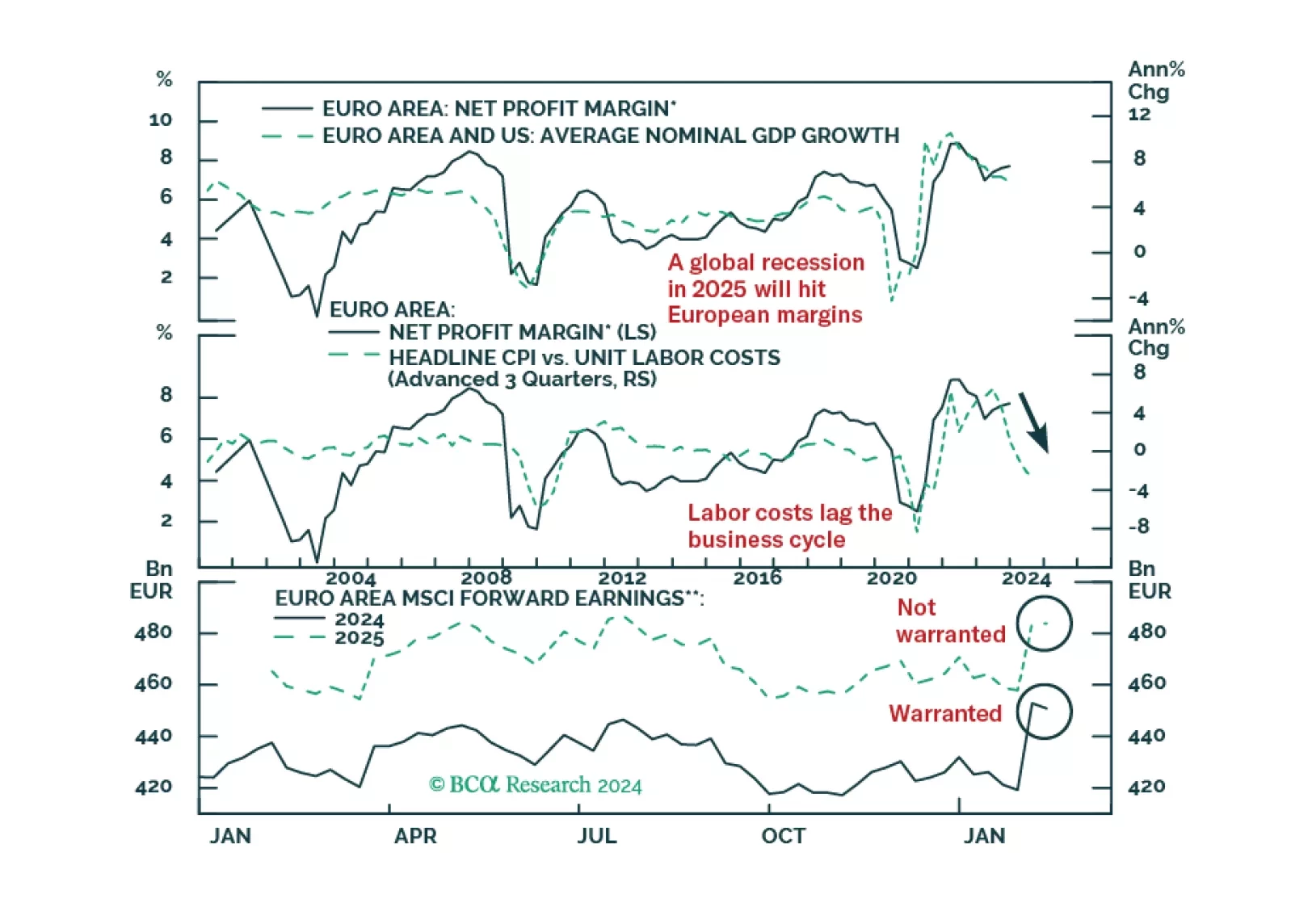

European profits margins are elevated. Will a mild recession be enough to bring them down?

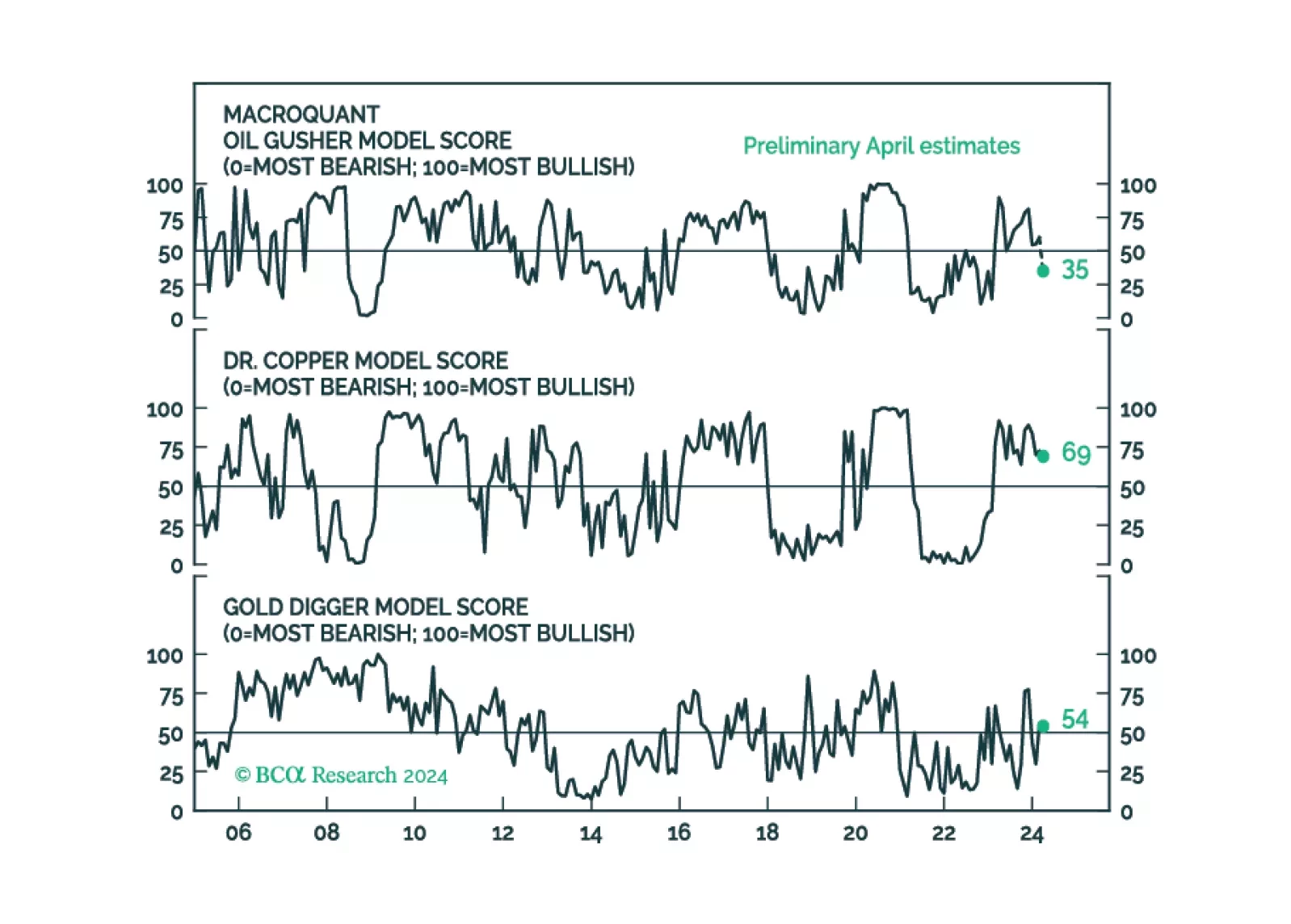

This year’s rise in commodity prices represents a blow-off rally rather than the start of a durable bull market. The global economy is heading for a recession. Stocks, commodities, and other risk assets are vulnerable.

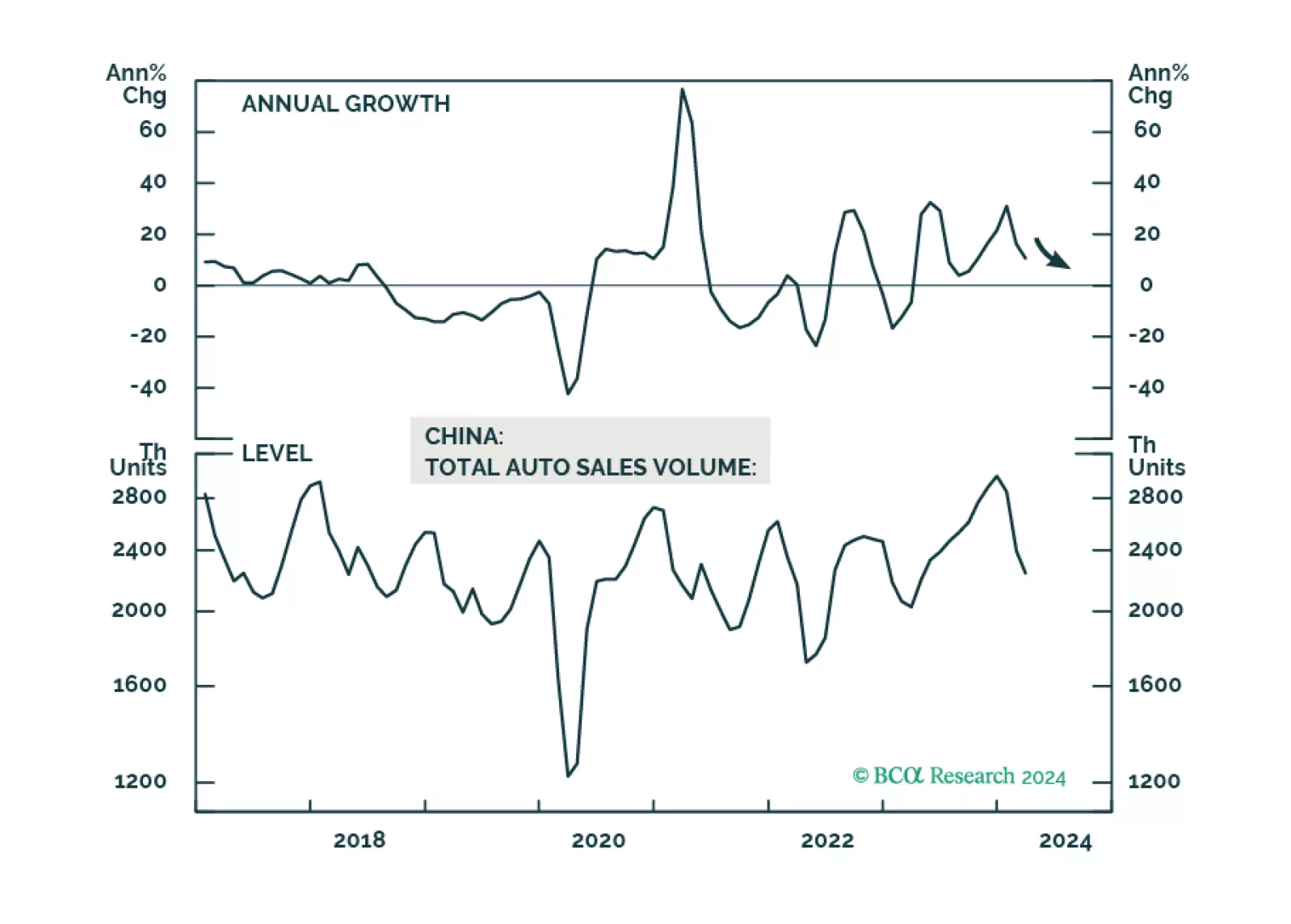

This year’s cash for clunkers program will have only a mildly positive impact on domestic demand for automobiles and home appliances in China. In the meantime, the equipment renewal program will prop up domestic manufacturing moderately as well as help the country reduce its reliance on high-end equipment imports. We recommend continuing to overweight onshore auto stocks relative to the A-Share Index.