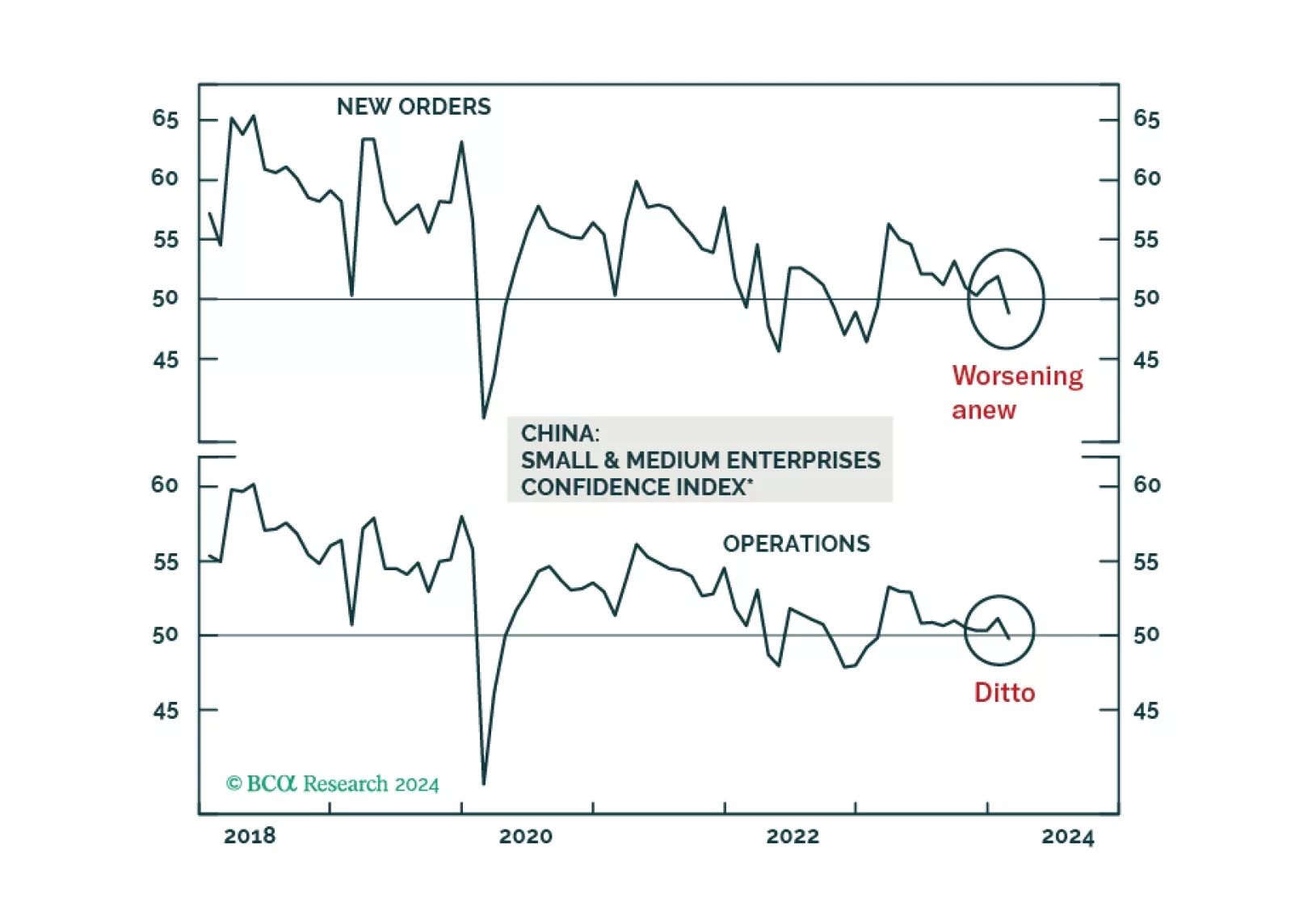

China

Investors around Europe and North America are concerned that the stock market is increasingly overbought and vulnerable to exogenous risks. We agree and have good reasons to fear that festering geopolitical risks and the US election season will deal negative surprises.

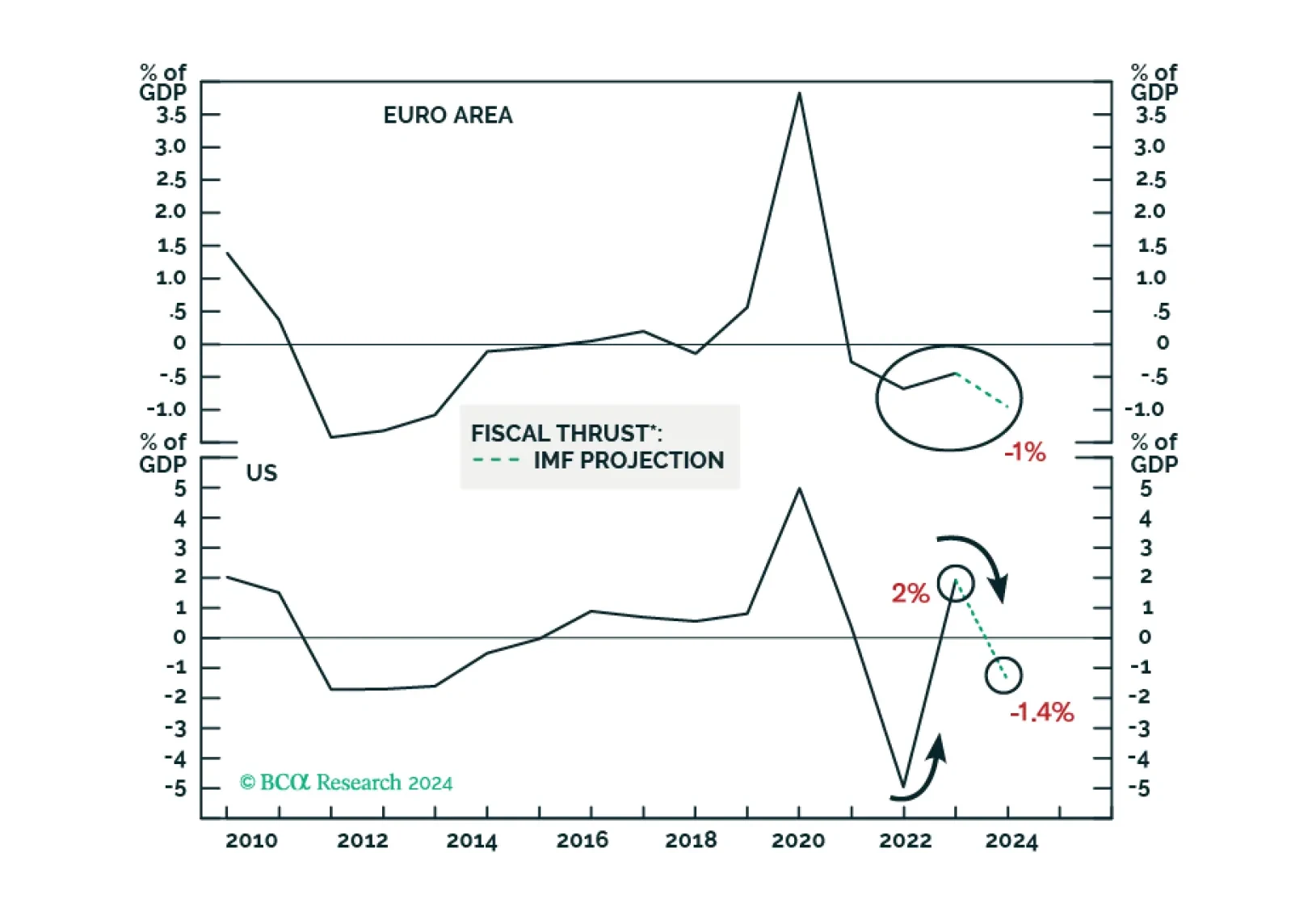

Despite a couple of rate cuts in H2 2024, borrowing costs will remain elevated in real terms amid lower inflation in the US and Europe. This and tightening fiscal policy will hinder domestic demand in advanced economies. Domestic demand in China and EM ex-China will remain very tepid, with risks skewed to the downside.

Deflation remains prevalent in the Chinese economy. The longer authorities delay a big bang-type stimulus, the more entrenched deflation will become. Hence, a cyclical upswing in Chinese stocks is unlikely, although there might be short-term rebounds.