China

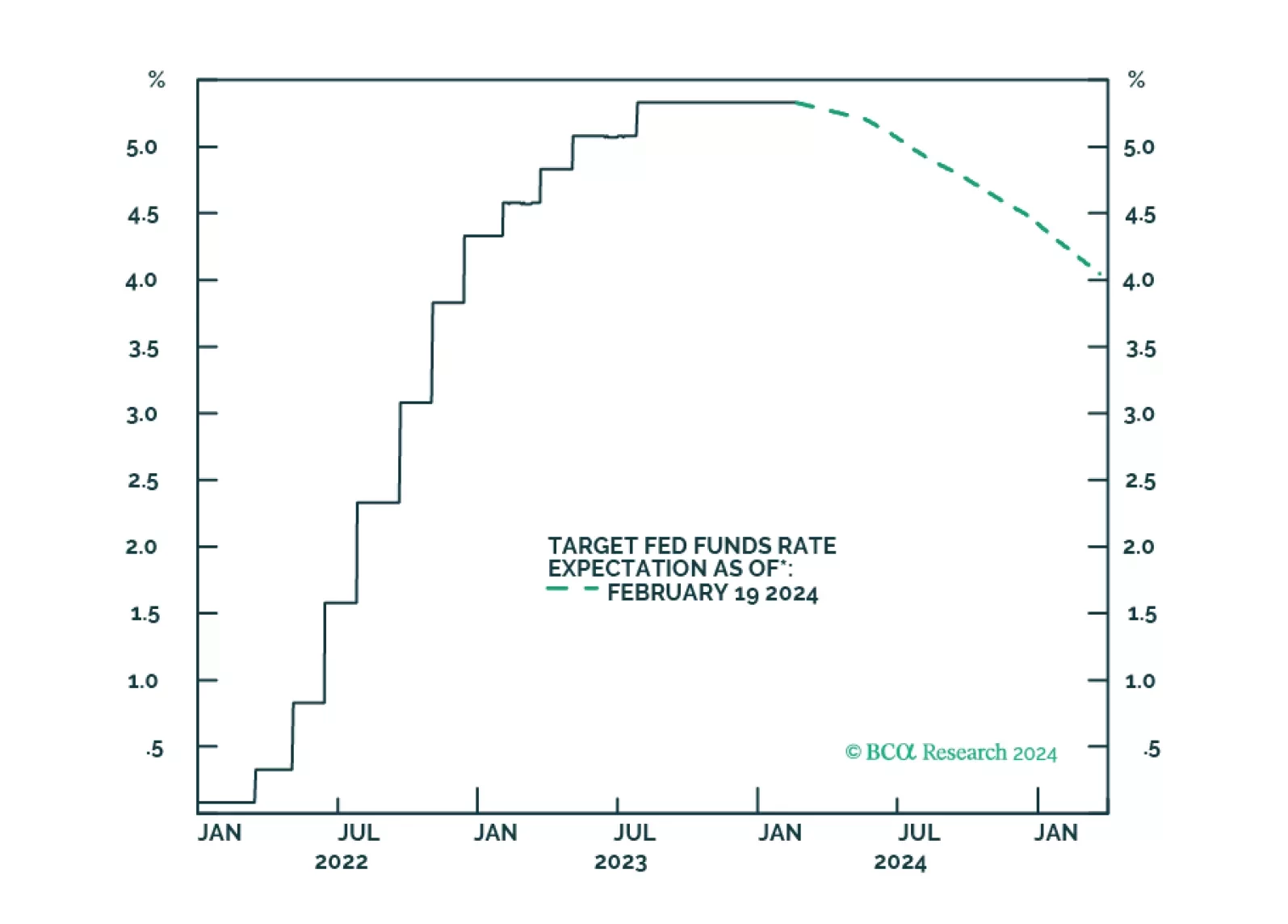

Seasonal weather and price variability in the first quarter will dissipate, which will reduce the agita caused by the recent inflation scare. This will increase the Fed’s comfort level in initiating a rate-cutting cycle in June with a 25 bp cut. With inflation well-behaved, real interest rates will move lower and gold prices will move higher. The rate-cutting cycle also will allow the USD to weaken as assets ex-US become more attractive; this will be bullish for gold. Physical demand for gold is expected to remain robust, along with safe-haven and central-bank diversification demand, due to heightened geopolitical uncertainty. We continue to expect gold to trade above $2,200/oz this year.

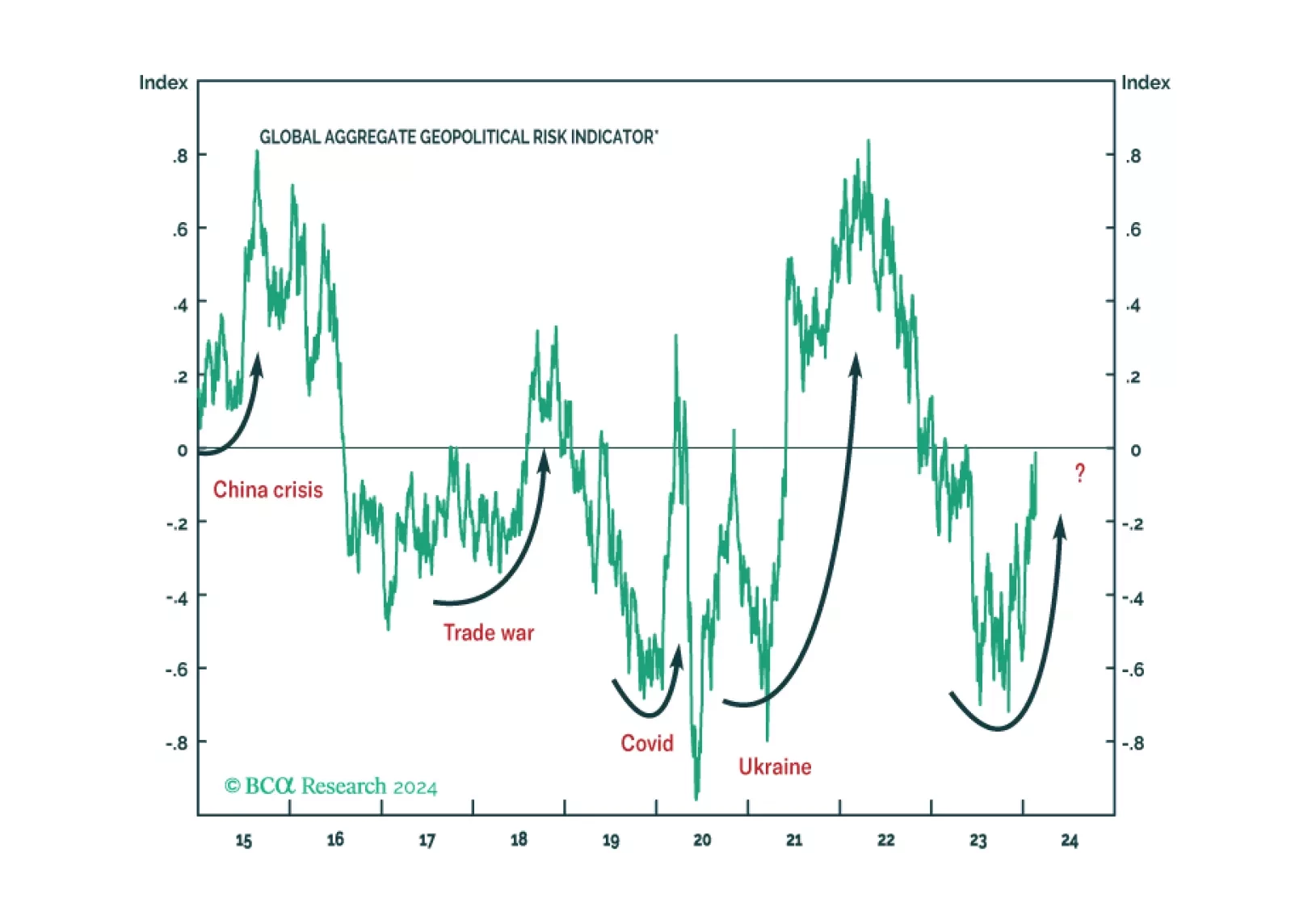

While 2024 will see various election risks, global geopolitical uncertainty is driven by the US election and its struggle with Russia, China, and Iran. The stock market can manage local domestic political risk. But it will correct upon a major outbreak of geopolitical uncertainty.

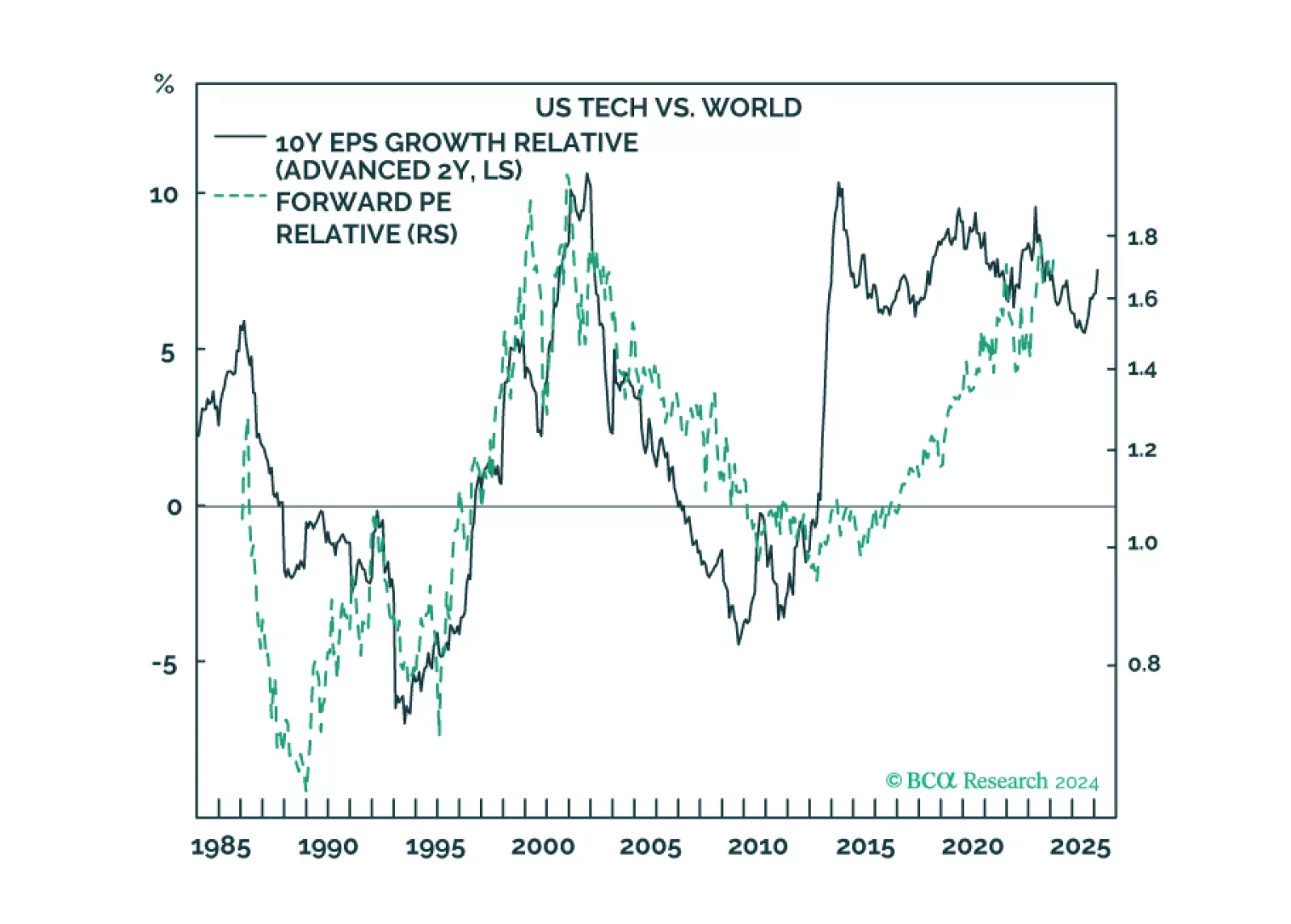

Our Valentine’s Day report is about two love stories: the infatuation with US tech and China’s infatuation with housing. We describe how these love stories will end, and why Europe could be the winner.

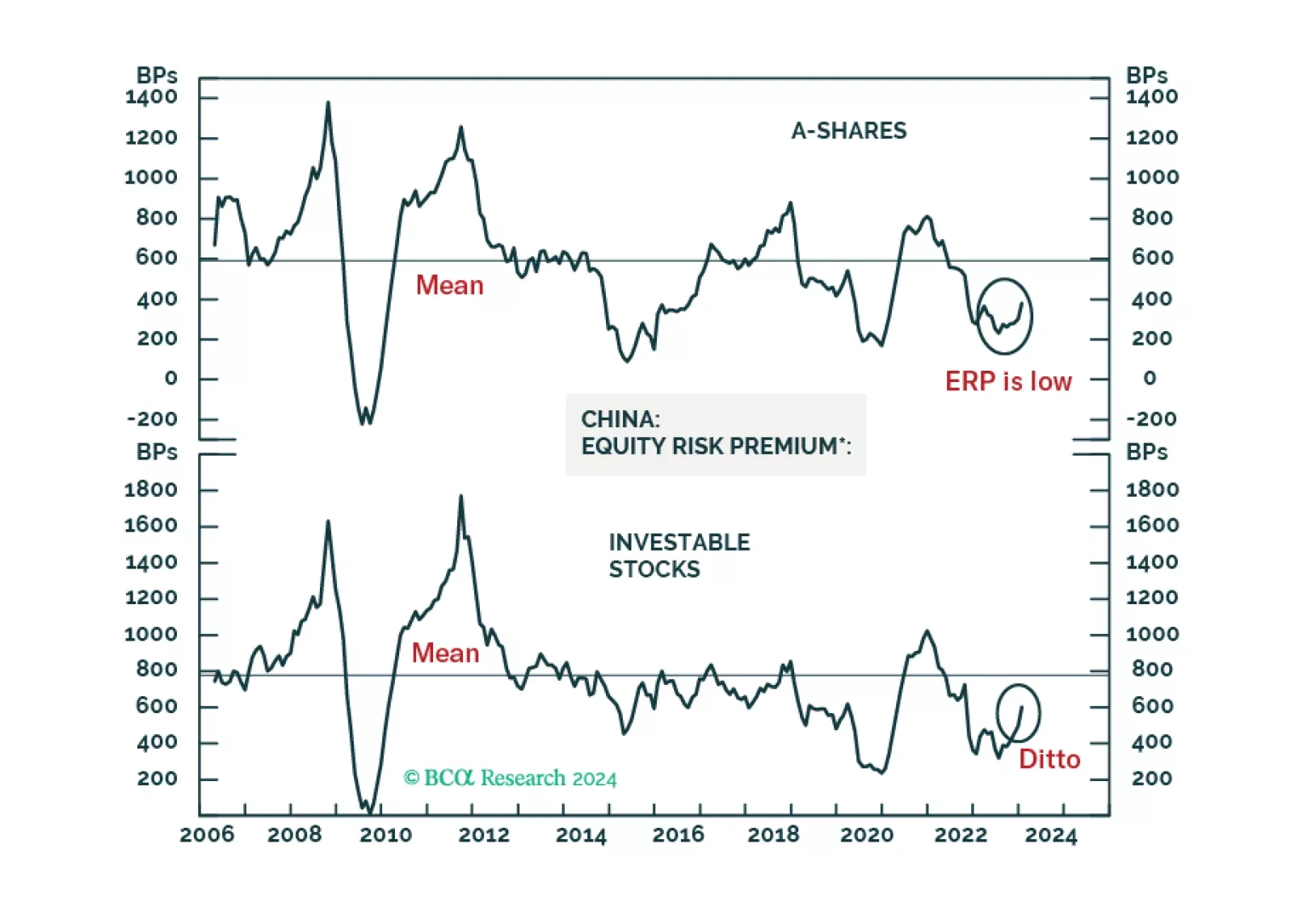

China will continue to suffer from a “triple crisis”. Though there could be a tactical bounce, cyclically we still recommend underweighting Chinese equities.

Chinese A-shares will probably begin forming a volatile bottom. The basis is that authorities will likely throw the kitchen sink at the onshore market in an attempt to stabilize share prices. The same is not true for offshore listed stocks. Hong Kong-traded Chinese share prices will likely continue to fall. Beijing is less concerned with offshore stocks as their holders are primarily foreign investors.