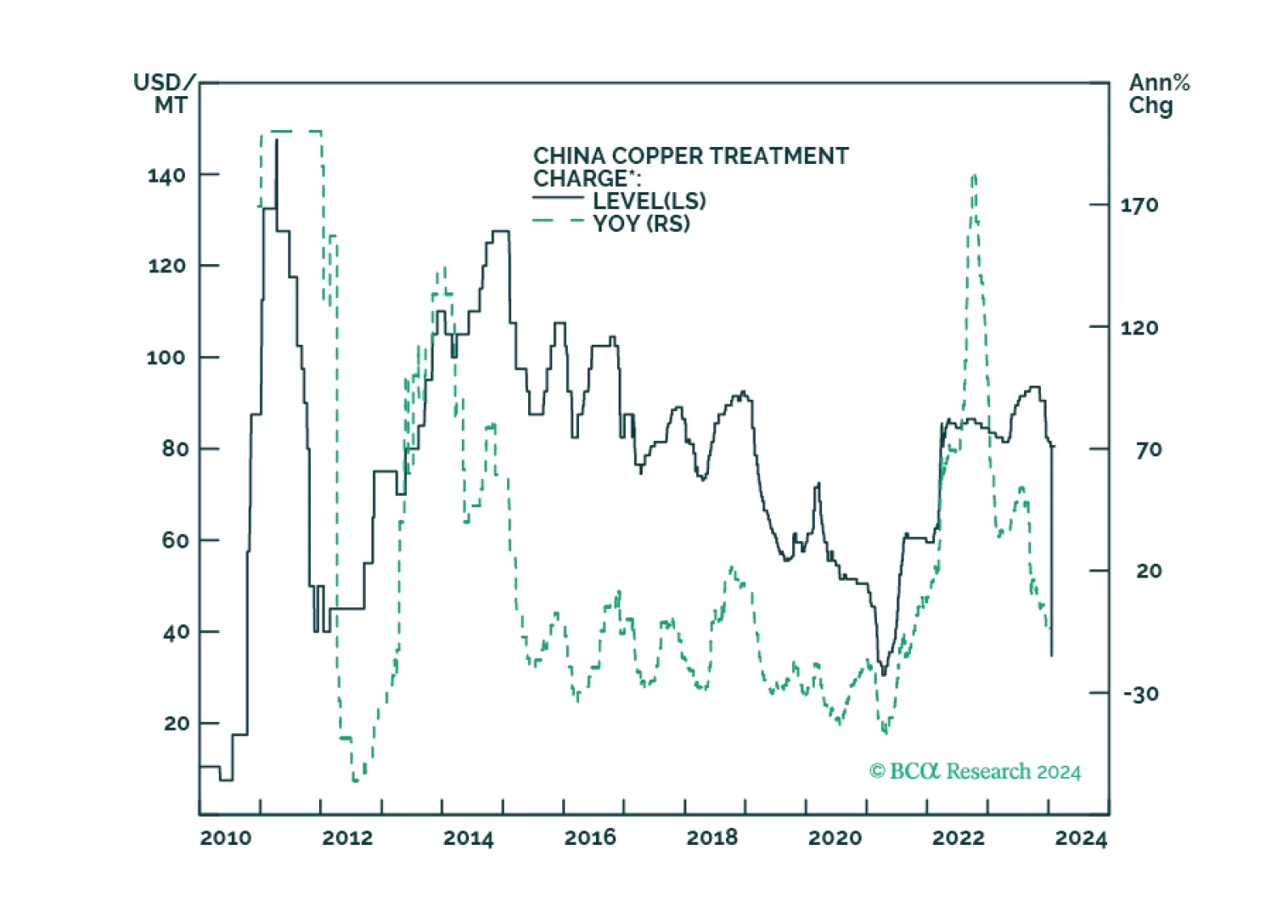

China

Supply and demand shocks in markets critical to the renewable-energy and defense industries will continue to play havoc with prices, which will negatively impact capex. In the short run, this benefits China given its already-dominant position in these markets. Longer term, investors already are providing capital for long-term projects needed for the energy transition. We remain long the XME ETF, given its low exposure to lithium and nickel holdings.

Our Portfolio Allocation Summary for February 2024.

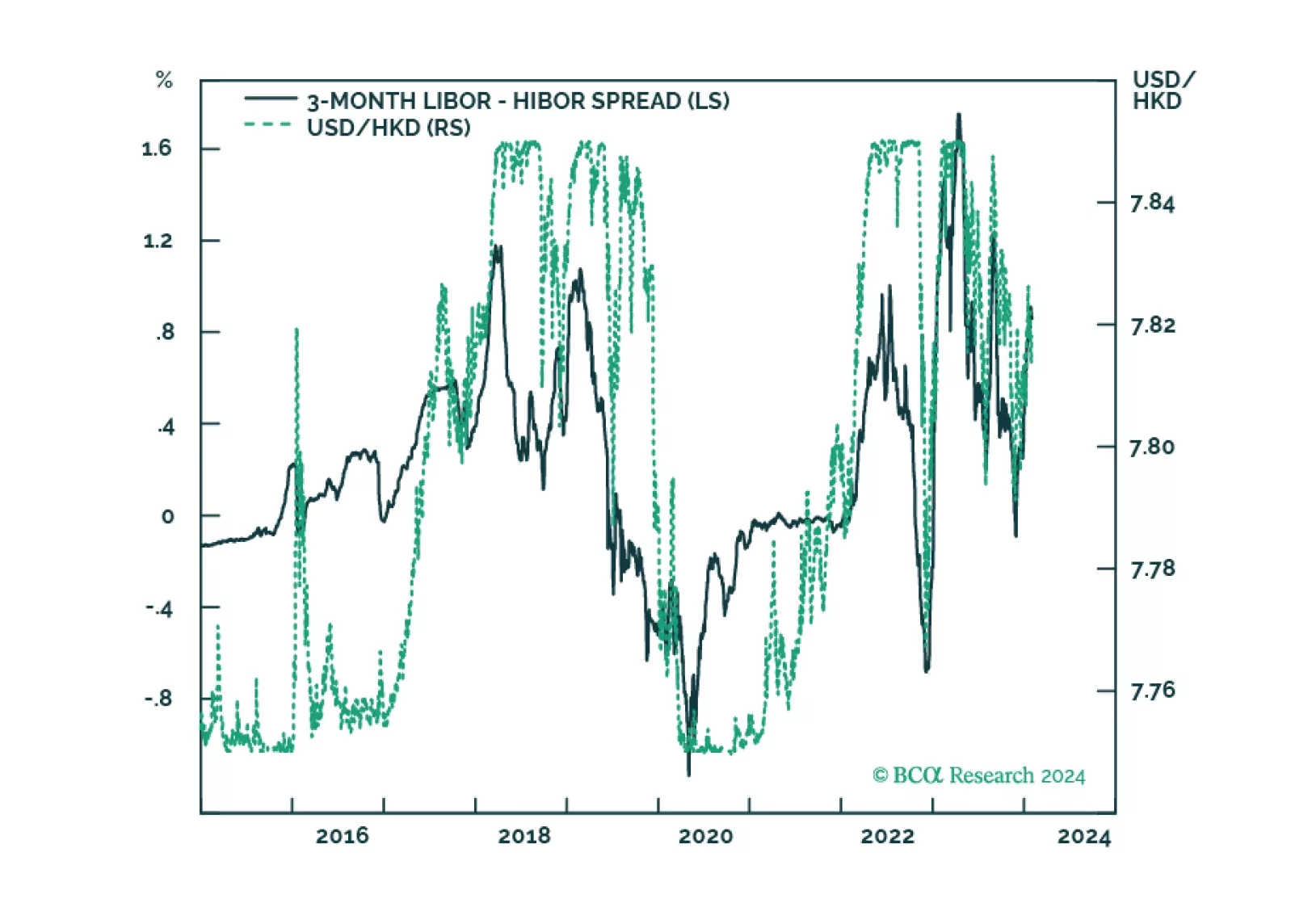

In this Special Report, we update our thinking on the Hong Kong SAR dollar peg, with implications for domestic asset markets.

When will the US also buckle under high rates? We expect a US recession to begin around mid-year. Stay defensive.

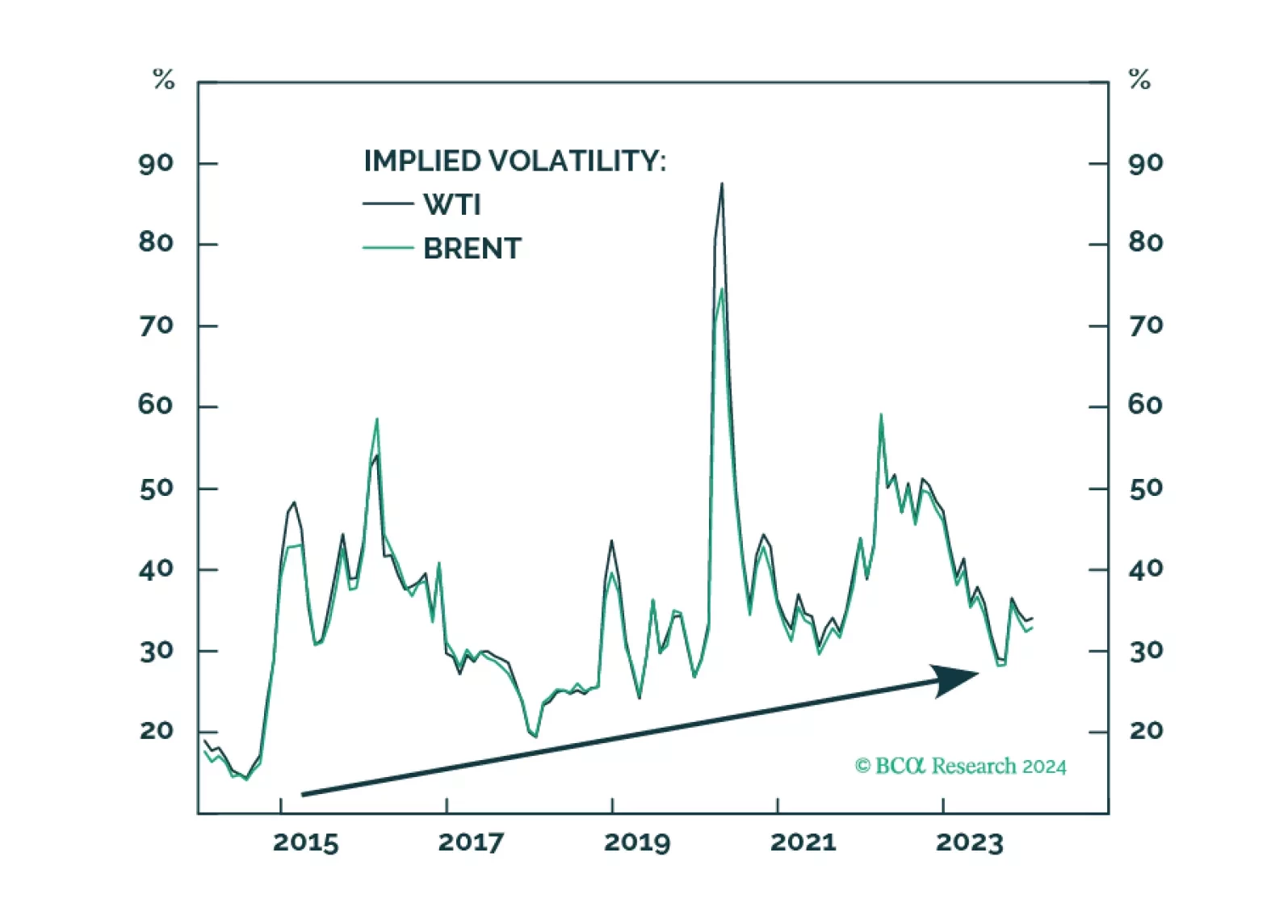

Commodity volatility will continue its rising trend since 2014. The US is on the brink of a major election, the outcome of which could reduce its willingness to engage with the outside world. So, states seeking to carve out their own spheres of influence are incentivized to raise the economic costs to the US and discourage its influence in their regions. These states can do this by interfering in key trading routes in their regions. As a result, geopolitical threats to maritime chokepoints are a structural as well as cyclical problem and will persist due to the revival of superpower competition.