China

Middle East conflict, extreme US policy uncertainty, Chinese economic slowdown, US-Russian proxy war, and Asian military conflicts do not create a stable investment backdrop for 2024. Our top five “black swan” risks may be highly improbable, but they stem from these underlying trends.

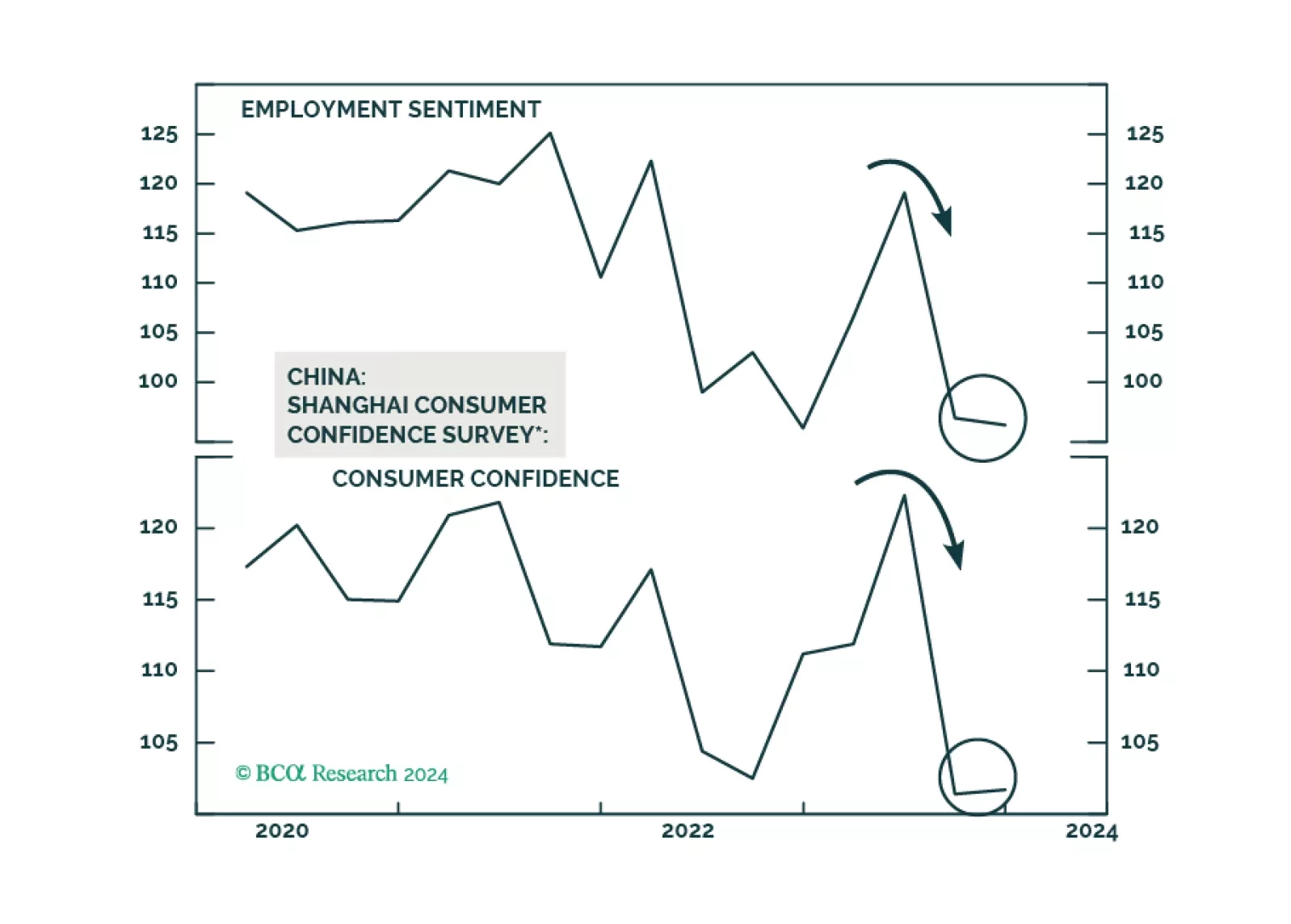

There is no easy way for China to forestall deflation. Provided policymakers are still reluctant to unleash large-size stimulus, more economic disappointments are likely in the coming months, and Chinese stocks will continue to sell off. The yuan is at risk of further depreciation versus the US dollar.

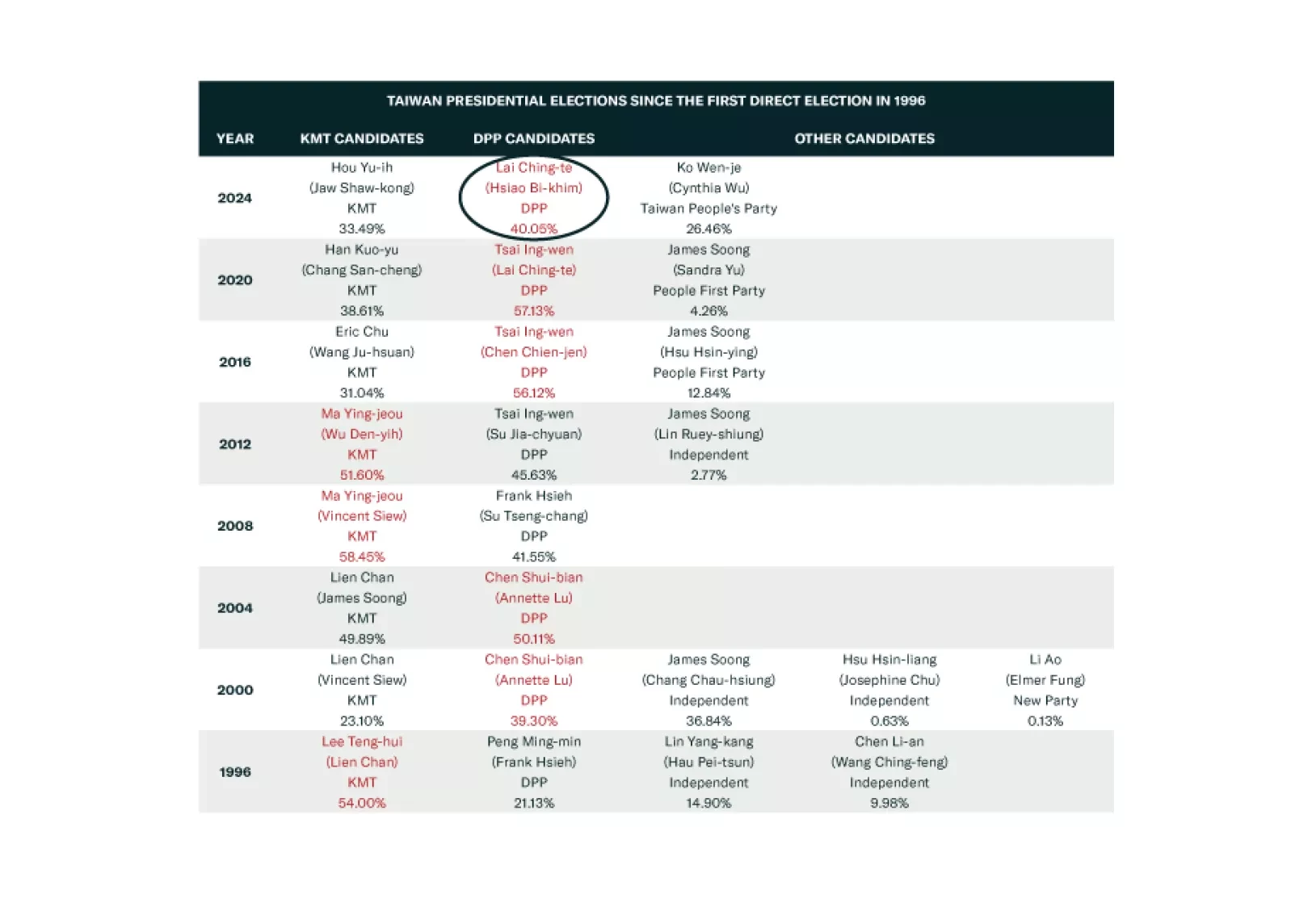

Taiwan’s election will lead to serious Chinese military and economic pressure but not full-scale war. War is a long-term concern. Investors should short TWD-USD.

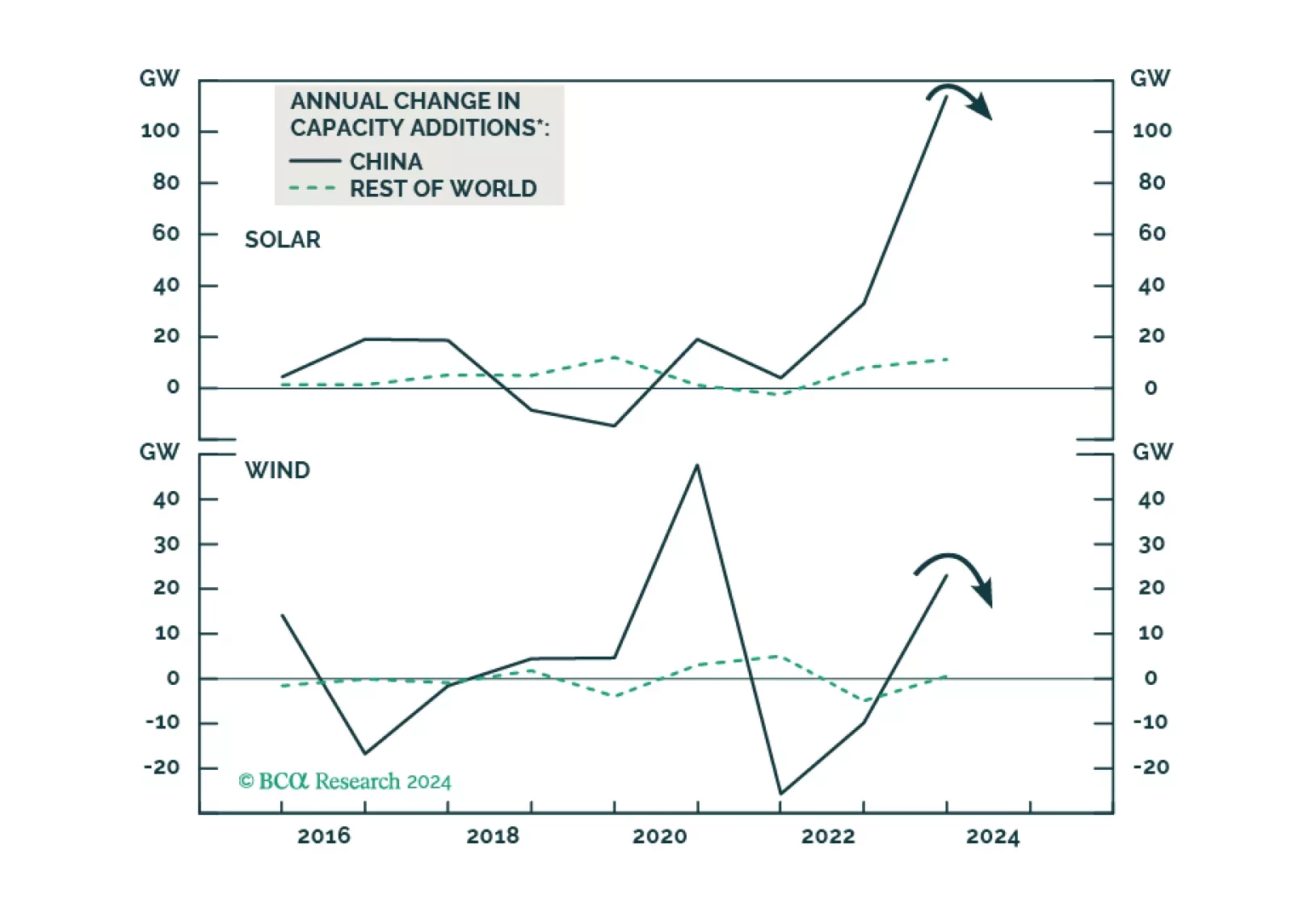

The global green energy rush faces mounting headwinds. Additional global solar and wind capacity installations will have considerable growth reduction this year. Copper prices did not drop much in 2023 due to surging demand from green power build-up. Green power will be less positive for copper demand in 2024 than in 2023. We expect more downside in global renewable energy stocks.

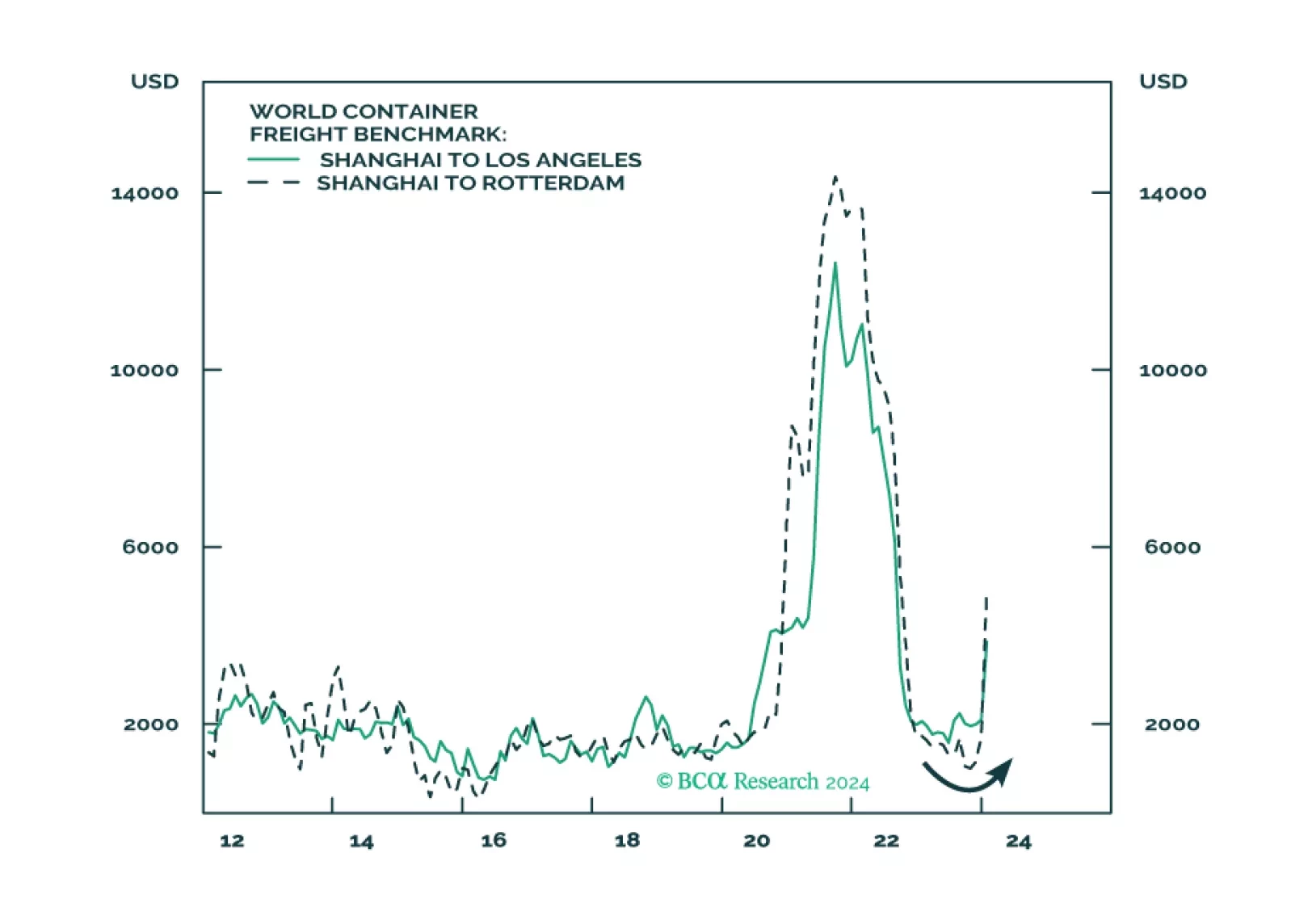

We share the edited transcript of a webinar we participated in discussing global trade, trade wars and tariffs, as well as de-risking strategies.