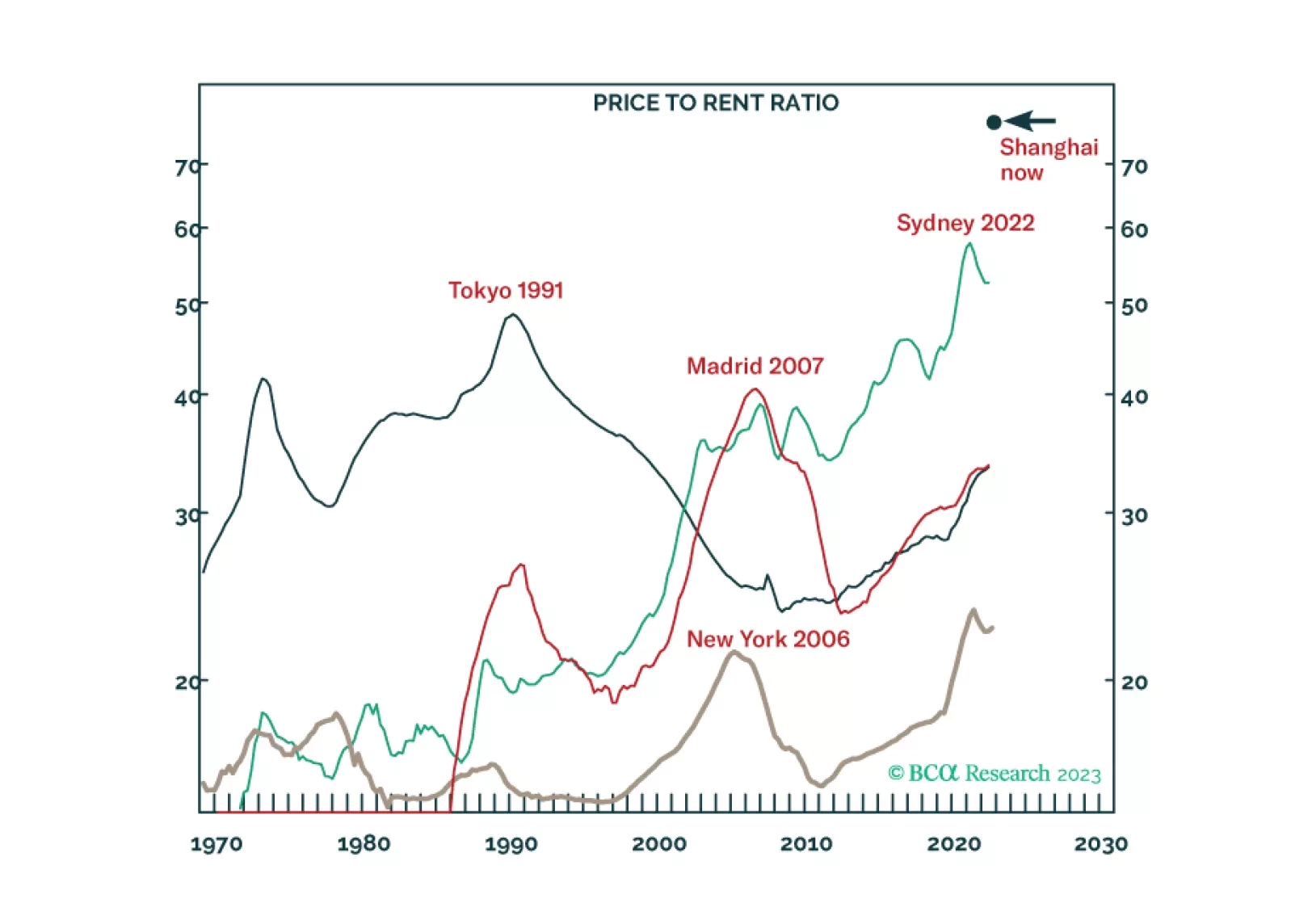

China

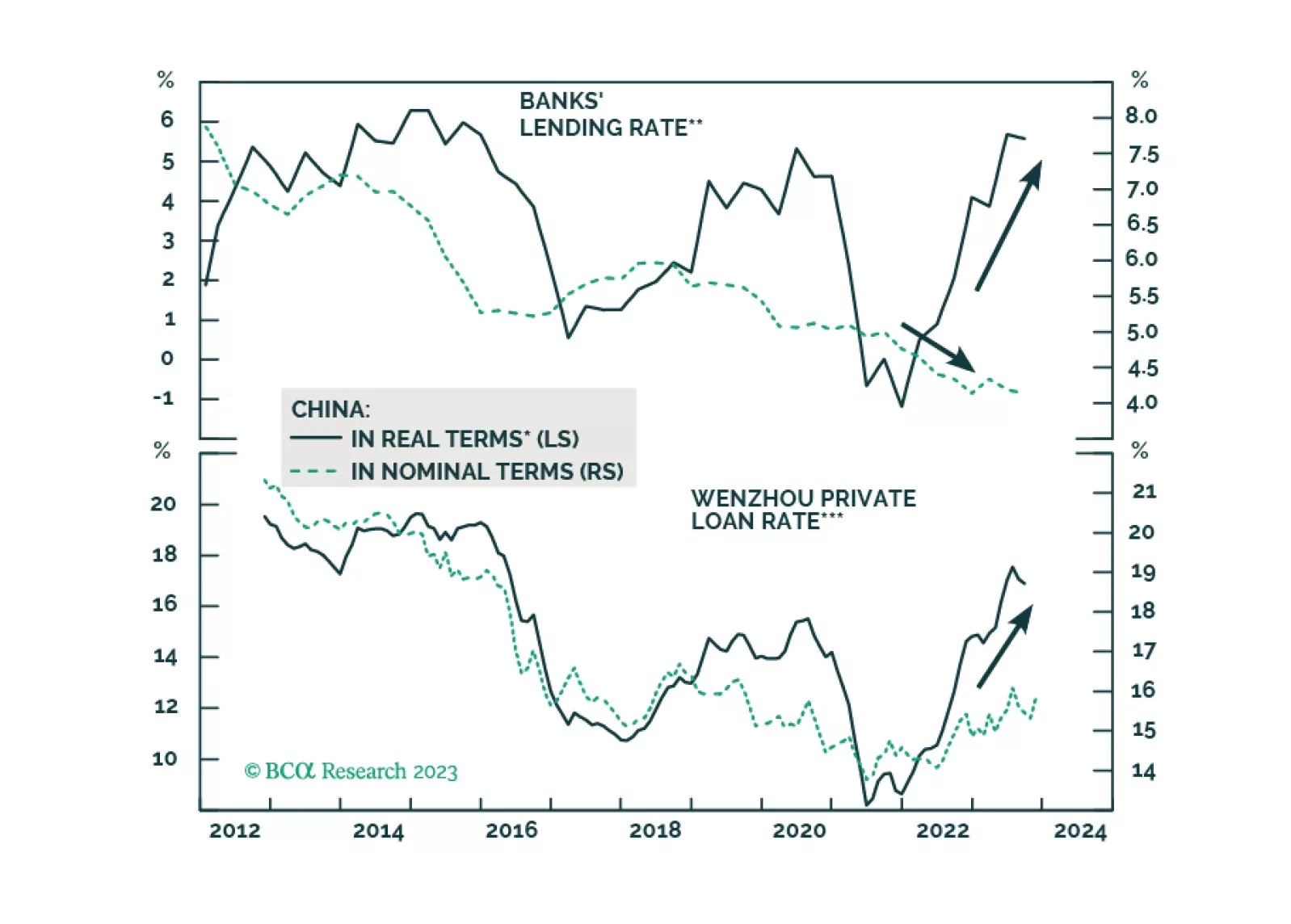

The statement from last week’s Central Economic Work Conference indicates that Chinese authorities are still not considering large-scale stimulus in 2024. Odds are that a full-fledged business cycle recovery in 2024 is unlikely. Chinese share prices remain vulnerable, and strengthening in the RMB will be short-lived.

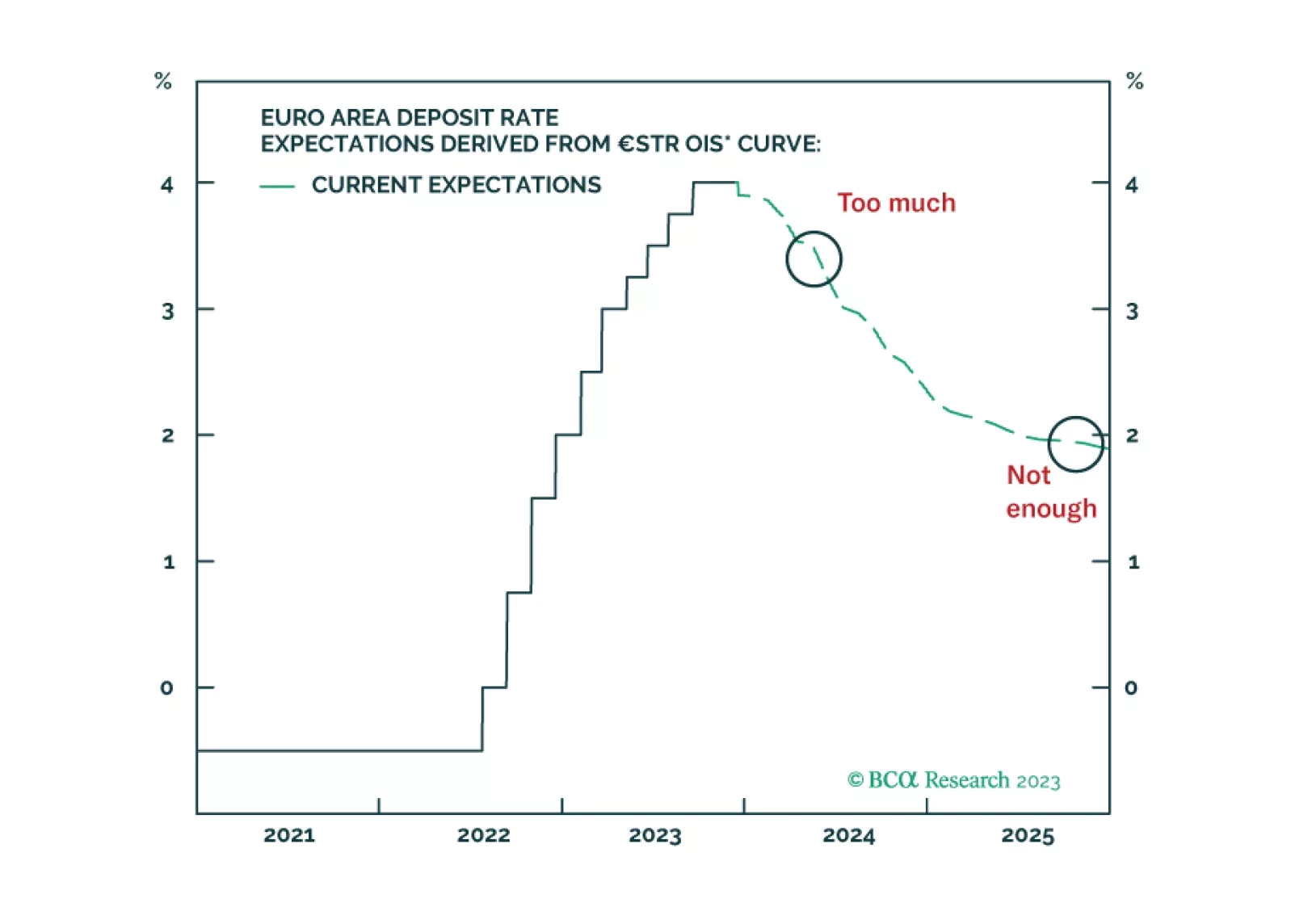

Explore the eight main themes that will drive the returns of European assets in 2024.

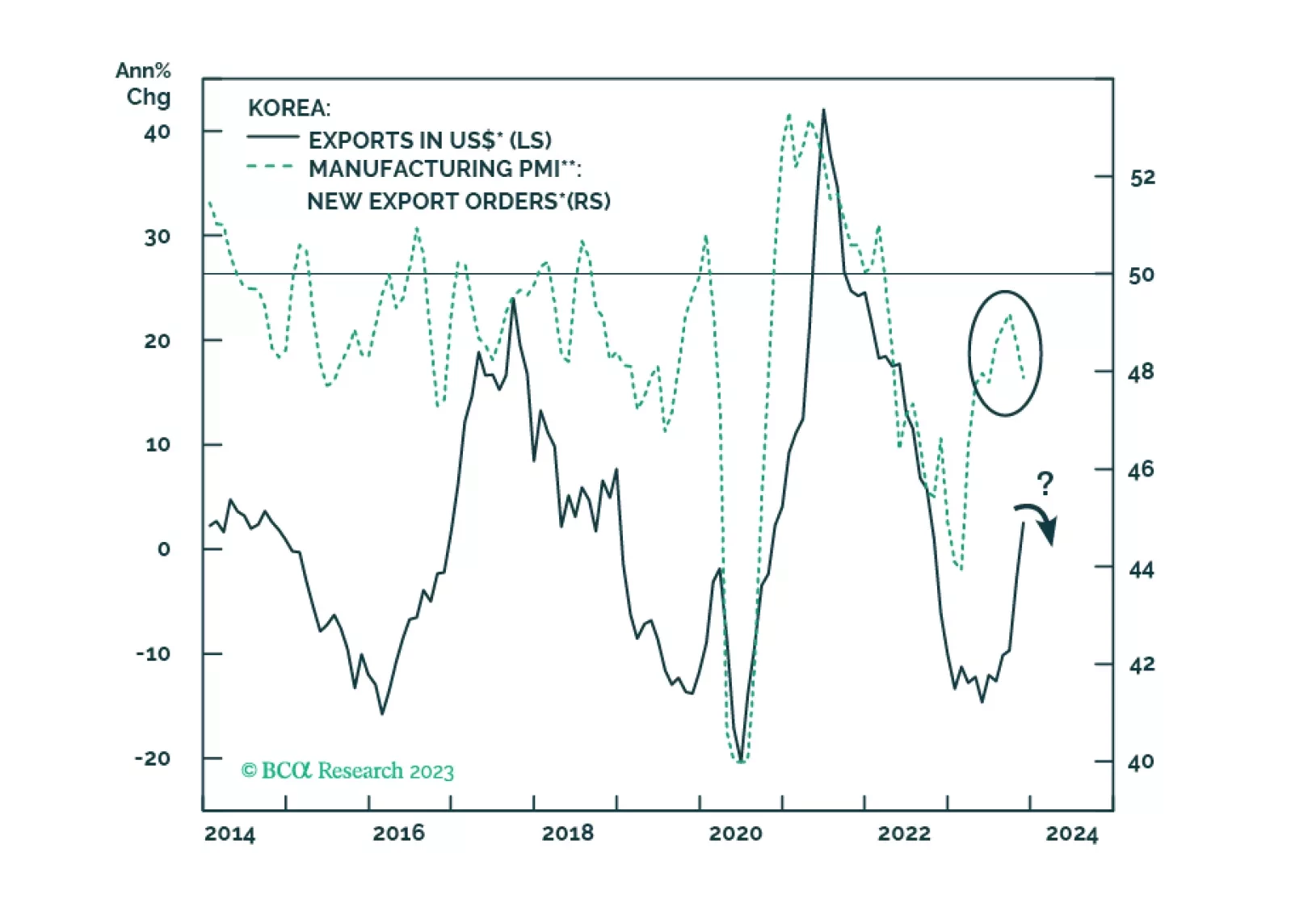

The major question facing EM investors in 2024 is whether or not EM will cross the Rubicon. The path to a soft landing in the US remains elusive. The recent improvement in global manufacturing/trade will likely prove to be a mid-cycle bounce rather than the beginning of a cyclical recovery.

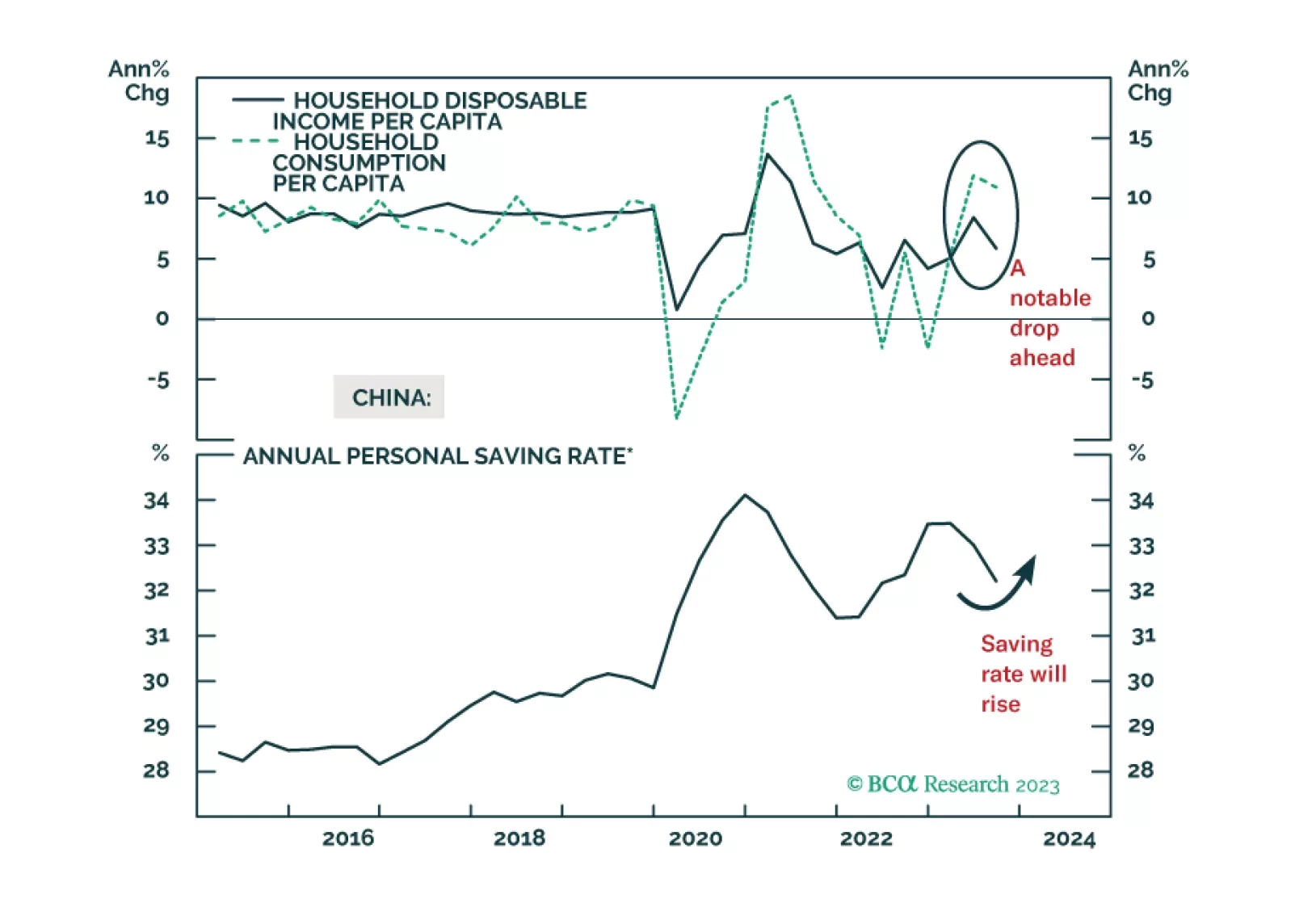

Nominal household spending growth in China will slow in 2024. Strong headwinds will arise from a slower household income expansion, falling house prices, a downbeat employment outlook, and shrinking exports. Spending on healthcare services will post solid gains but durable goods consumption will experience anemic growth in 2024. We favor consumer staples and healthcare stocks versus the domestic benchmark.

Political economy dominates fundamentals going into 2024, as states prepare for war and de-risk supply chains. Asynchronous global growth will elevate commodity-price volatility. We expect oil to trade above $100/bbl in 2024 and continue to favor equity exposure to oil-and-gas producers. Given weak capex, we also favor metals miners and refiners. We remain long the Gold, the XME and COMT ETFs We were stopped out of our XOP ETF with a 12.5% gain; we will re-establish it at tonight’s close.

Our 2024 outlook can be encapsulated into just 39 words and three key views. Key view 1: The end of China’s housing boom means the end of the world’s main growth engine. Key view 2: If the Fed and ECB don’t kill the economy, they won’t kill inflation. Key view 3: The AI gold rush will struggle to find any gold. We go through the investment implications for the year ahead.

Global Investment Strategy predicted the surge of inflation in 2021/22 and the immaculate disinflation of 2023. Now their unique framework is predicting a recession in the second half of 2024.