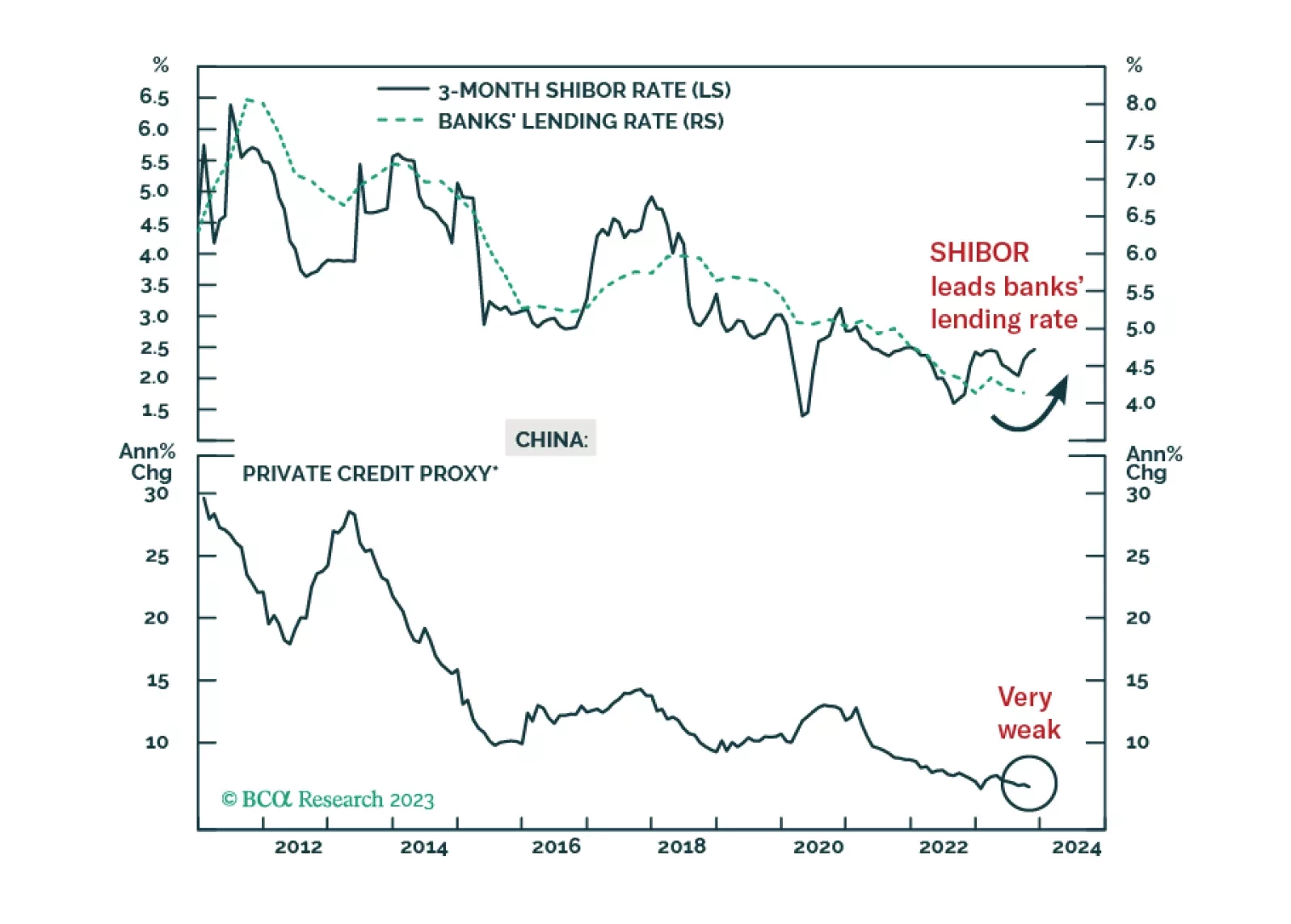

China

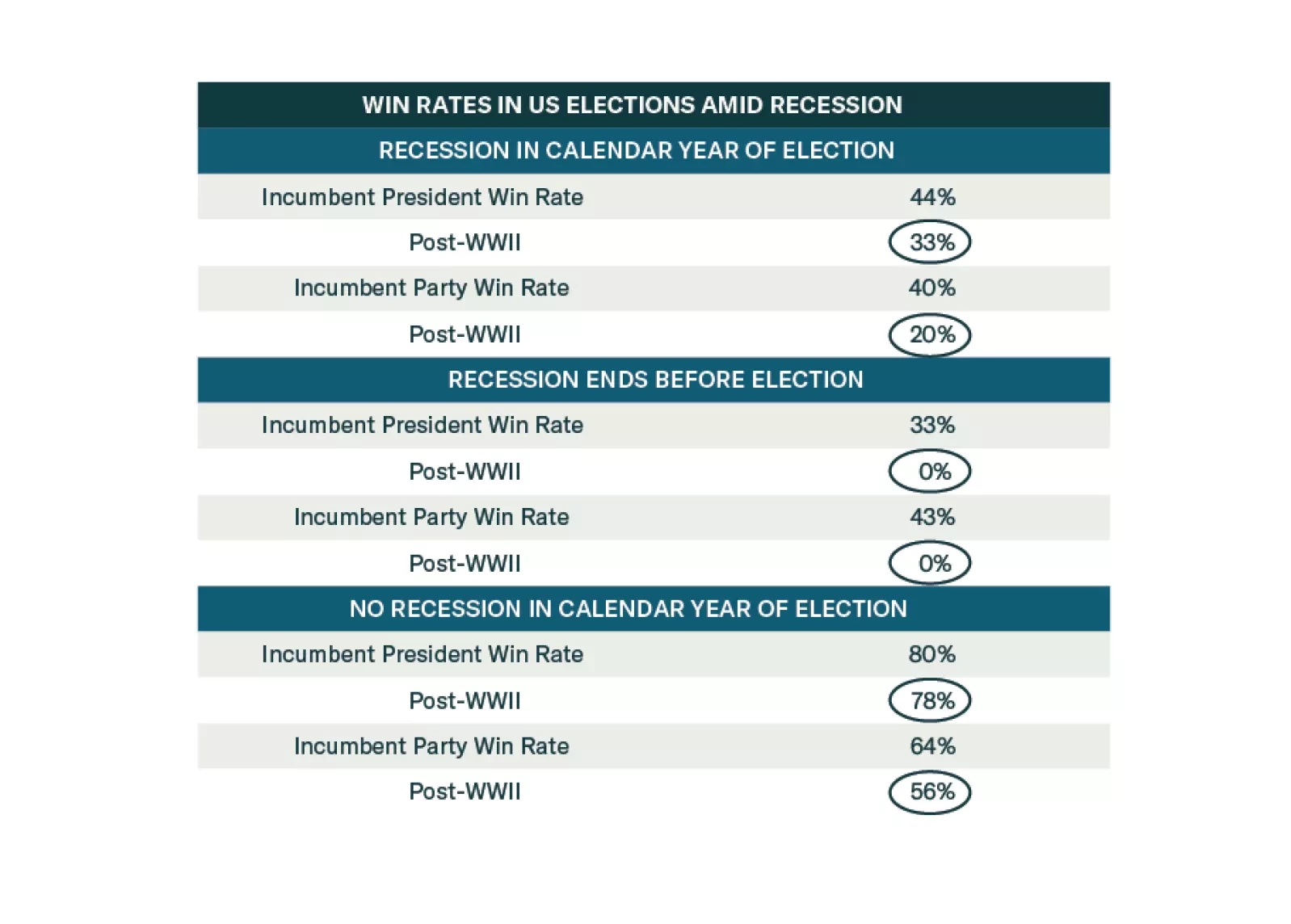

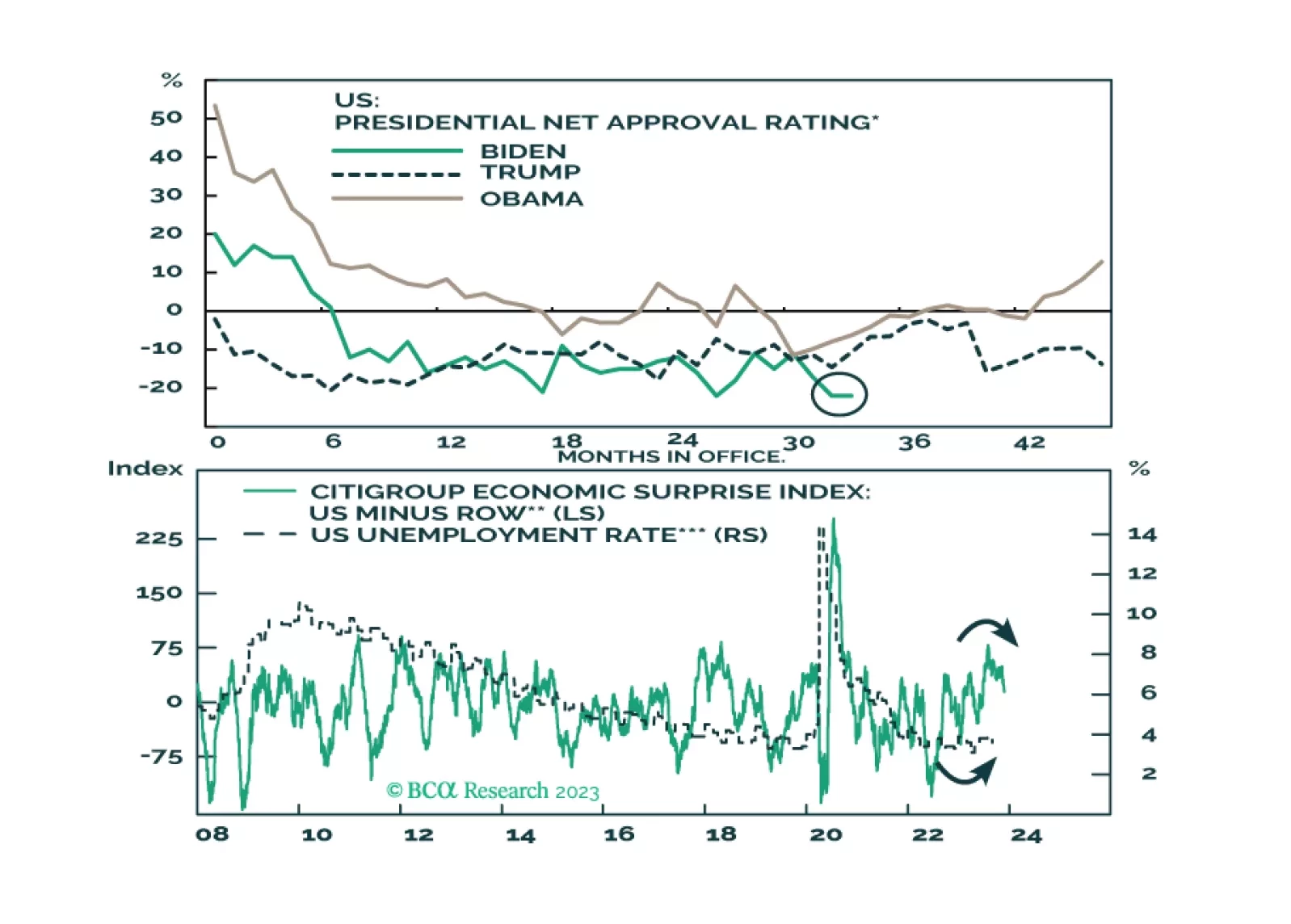

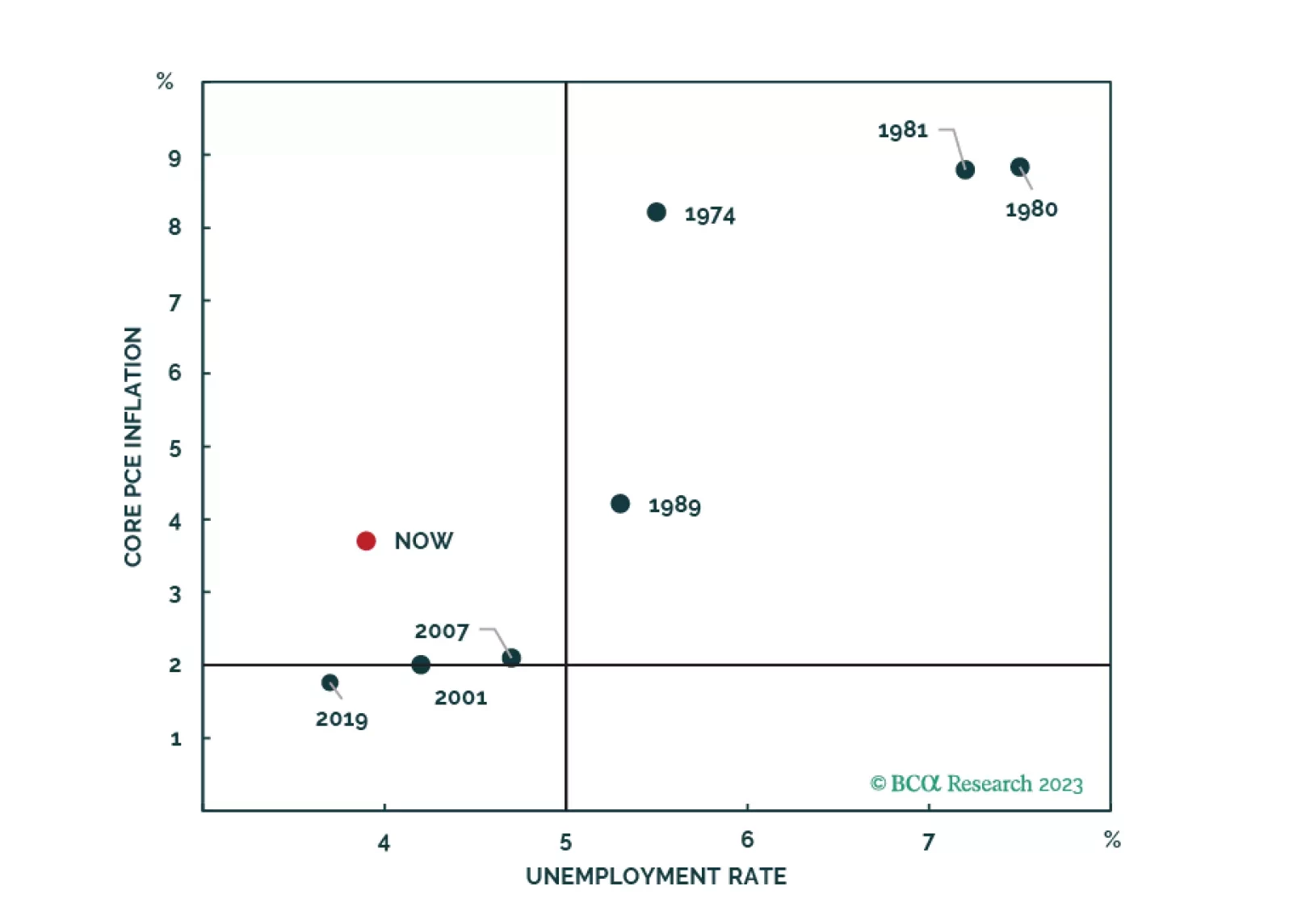

Democrats are favored to win the election until recession materializes. But recession risks are high. Investors should adopt a defensive and conservative strategy in 2024 amid extreme US policy uncertainty.

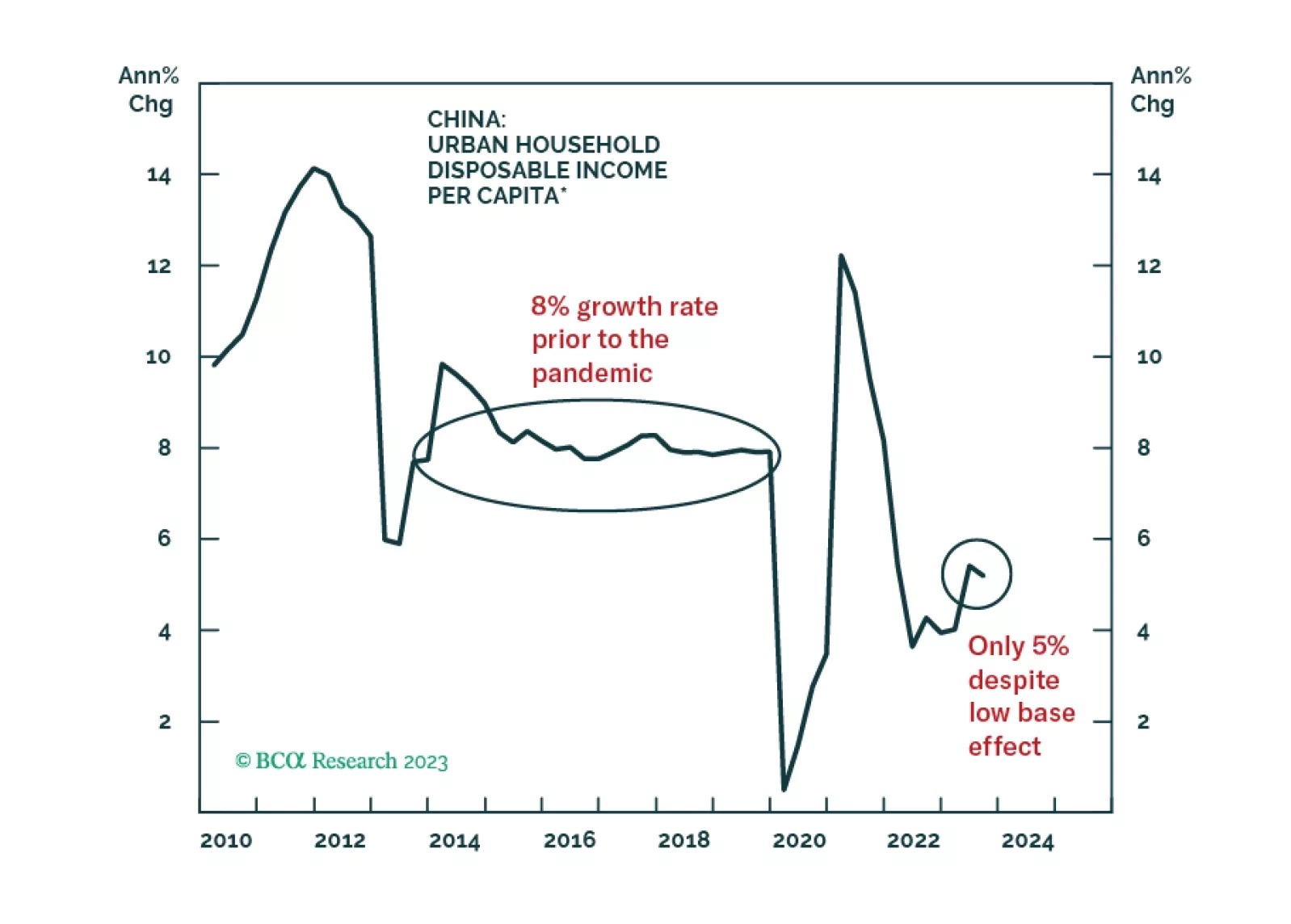

The overarching macro theme for China in 2024 will be deflation and its impact on the economy, macro policies, and financial markets. Widespread deflation, in combination with high debt levels and falling real estate prices, has unleashed debt deflation and balance sheet recession dynamics. The latter are rendering monetary policy inefficient.

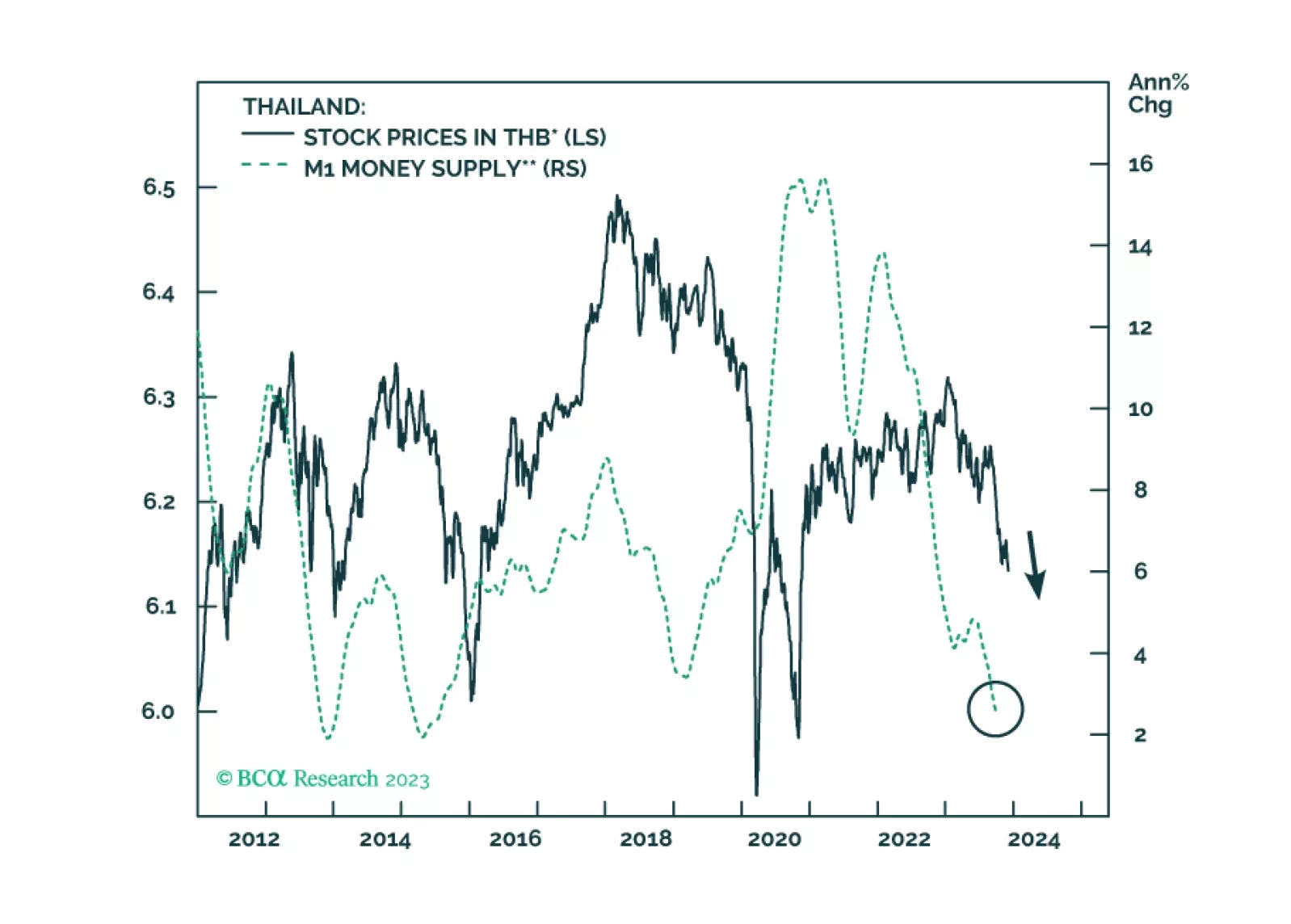

Meager credit growth and shrinking real wages will keep Thai inflation very low in the coming months. The currency will get support from an improving current account surplus. Fixed-income investors should upgrade Thailand from neutral to overweight within EM domestic bond portfolios.

Global instability will continue in 2024 – whatever happens afterward. Slowing economies will exacerbate already high geopolitical risk and policy uncertainty stemming from the US election and foreign challenges to US leadership. Overweight government bonds, defensive sectors, the Americas versus other regions, aerospace/defense stocks, and cyber-security stocks.

Inflation won’t fall fast enough for the Fed to cut rates preemptively before recession arrives. The risk/rewards balance is unfavorable for risk assets. Stay overweight bonds versus equities.

A cyclical recovery in China’s economy is still not imminent. The PBoC has tightened interbank liquidity to stabilize the exchange rate since late August. This does not bode well for the real economy. The uptick in onshore bond yields and the RMB’s appreciation will be transient. Equity investors should stay cautious.