China

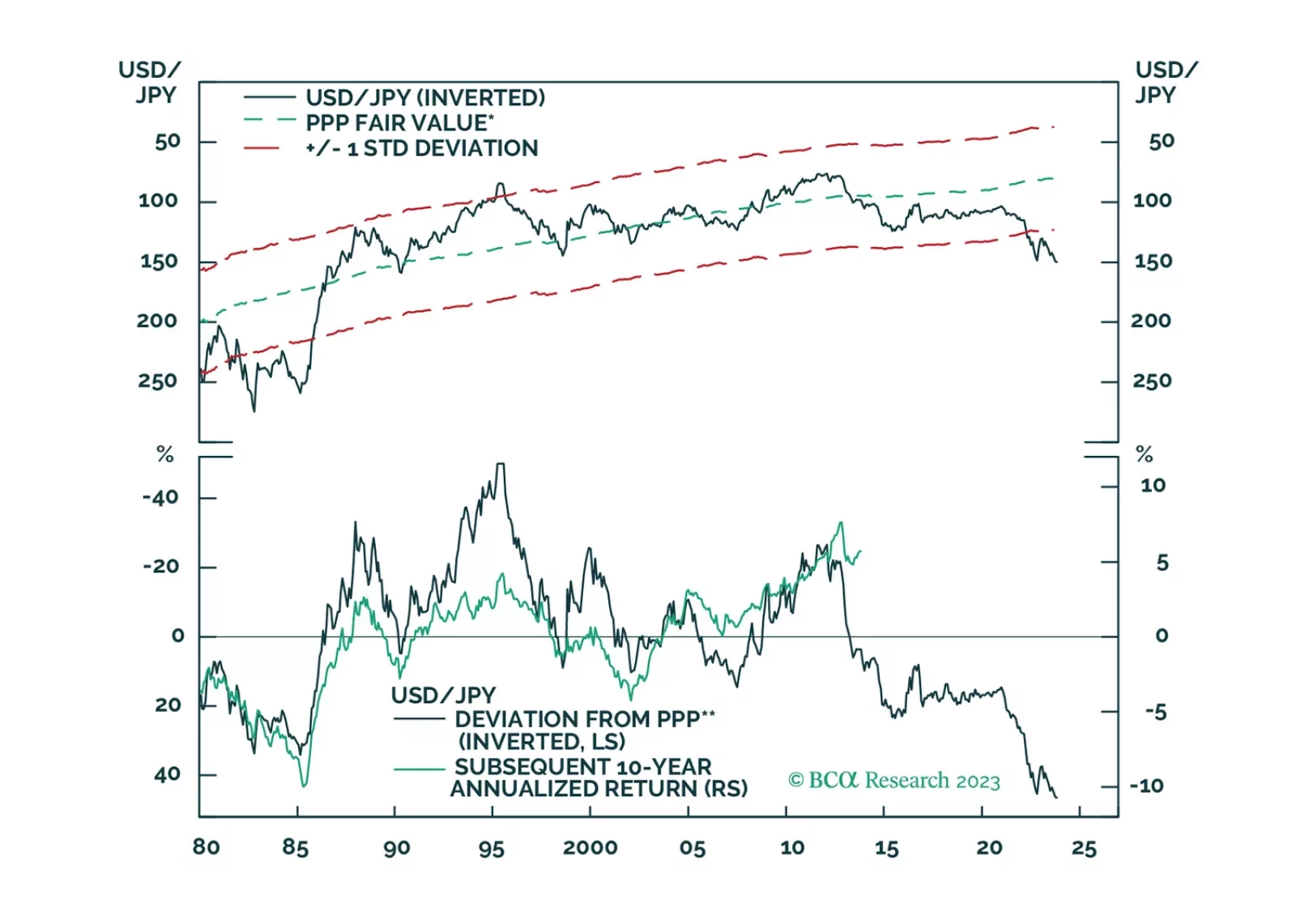

There is a high probability that the global economy will tip into recession in the second half of 2024. A long yen position is an excellent hedge against that risk.

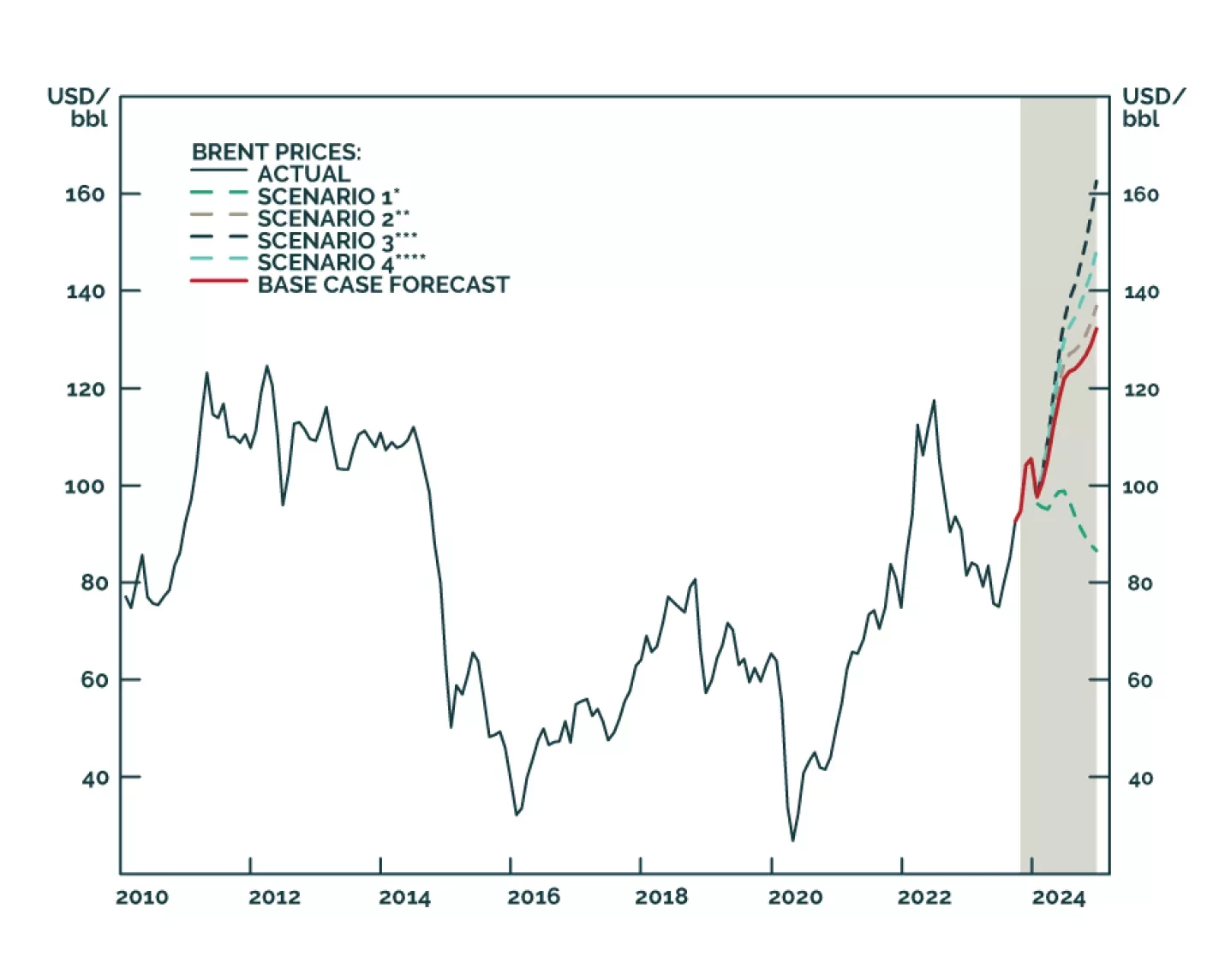

Despite higher uncertainty, our Brent price forecasts remain unchanged at just over $101/bbl for 4Q23 and $118/bbl for next year. We remain long equity exposure to oil and gas producers via the XOP ETF, and commodity exposure via the COMT ETF. We also remain long $100 Dec24 Brent calls and long 1Q24 Brent futures vs. short 1Q25 Brent futures in anticipation of stronger backwardation.

Domestic auto sales in China will likely have anemic growth over the next three years. Yet, Chinese automakers are set to gain a larger share of the global market. Go long Chinese automakers / short global ones.

As global financial institutions like the IMF draw attention to the real-estate crisis in China, the CCP will be forced to step up regulatory and restructuring efforts to contain its spread and limit further contagion domestically and globally. The Party also will be forced to deliver stronger fiscal- and monetary-policy support to beleaguered banks and developers. We expect it to do so, which keeps us bullish energy and metals. Failure raises the odds of a collapse in the property markets, which would be socially destabilizing, and lead to greater risk aversion and volatility globally.