China

In Section I, we explain why we do not see the deceleration in US inflation, the likely near-term pickup in European growth, and the end of China’s dynamic zero-COVID policy as signs of a sustainable rebound in global economic activity over the coming 6-12 months. The key question is not whether inflation will fall back to central bank targets, but rather how quickly this will occur. For now, our indicators point to slower but still elevated inflation this year. In Section II, we explore what it will take for the Fed to cut interest rates, and note that nonrecessionary rate cuts are possible but not especially likely.

It is not unusual for a period of rebounding share prices to occur between an inflation-driven selloff and a growth scare. Initially, stocks rally on falling inflation and prospects of lower interest rates. Then, worries about corporate profits intensify, and equity prices deflate along with falling Treasury yields. This is what happened in the US in 2000-2001 and is likely to occur in the coming months.

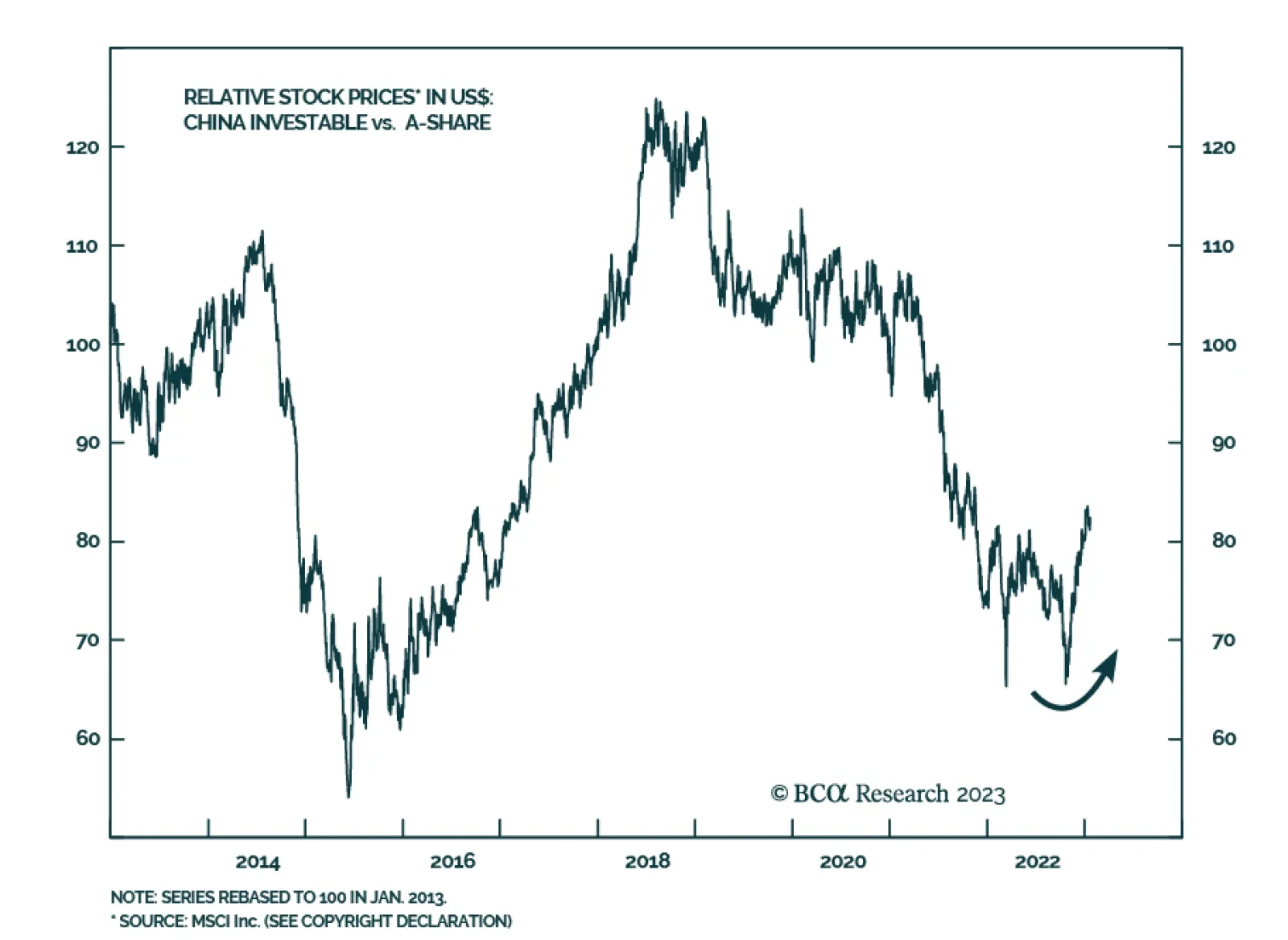

Global investors should sell Chinese assets on strength this year and diversify into other emerging markets. American investors should limit China exposure. Short CNY-USD.

China’s re-opening – powered by the fiscal and monetary stimulus required to achieve at least 5% real GDP growth after flattish 2022 growth – and a weaker USD will catalyze demand growth this year and next, lifting global oil consumption by close to 2mm and 1.7mm b/d in 2023 and 2024. We lowered our Brent forecast slightly for this year to $110/bbl, and expect 2024 prices to average $115/bbl. WTI will trade $4-$6/bbl lower.

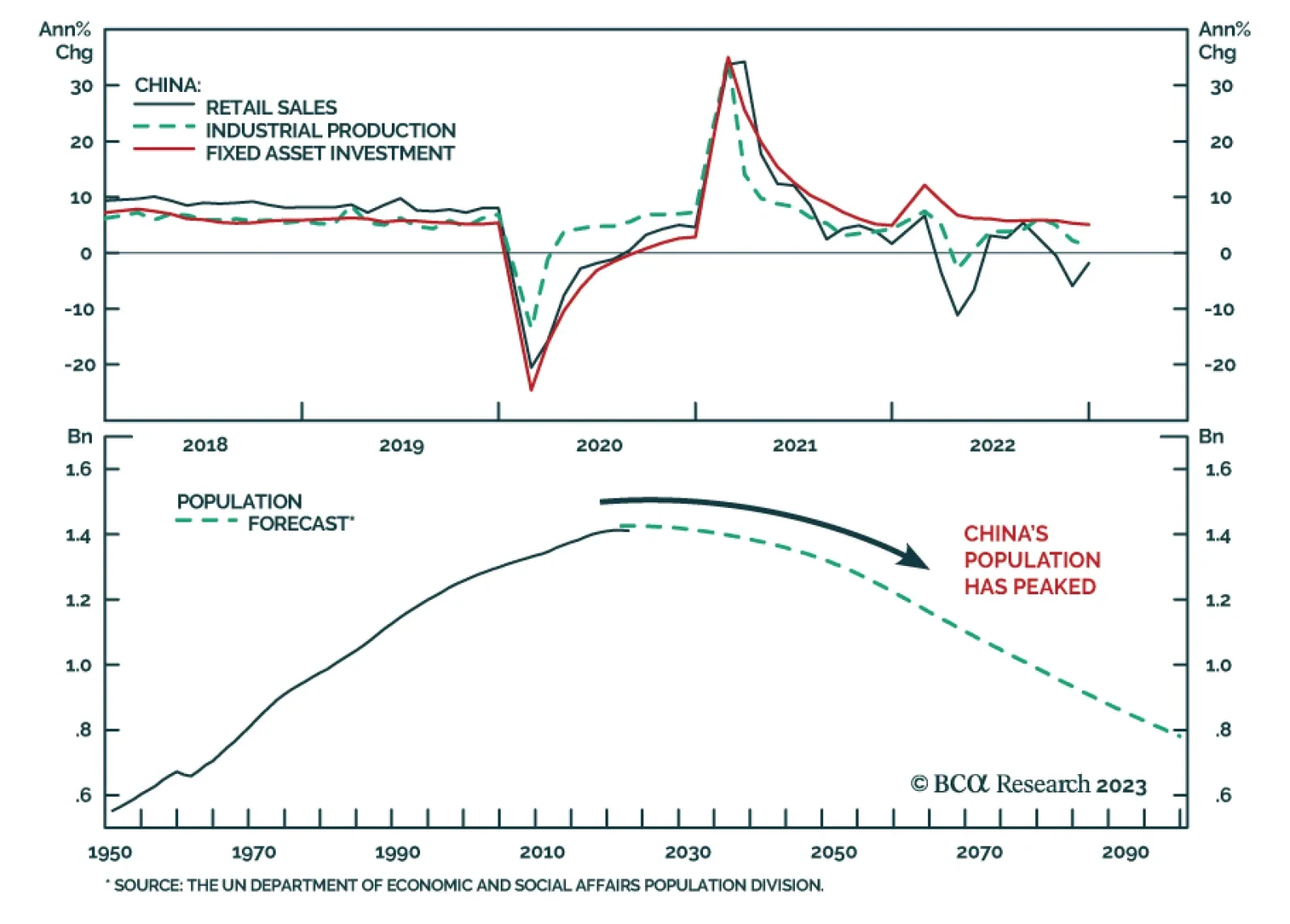

China's reopening is much more positive for the Chinese economy than it is for the rest of the world, as it will boost its domestic service sector activity and consumer spending much more than the industrial economy. A slowdown in Chinese industrial activity will put downward pressure on its demand for raw materials and energy, helping the world avoid another spike in inflation. Upgrade Macau casinos to overweight as the key beneficiaries of reopening. Off-shore TMT and bank shares face structural headwinds.

Investors should bet against the global rally in risk assets and maintain a defensive positioning until recession risks verifiably abate.

Investors should bet against the global rally in risk assets and maintain a defensive positioning until recession risks verifiably abate.

In response to lower energy prices and China’s reopening, European assets prices are outperforming. Will the ECB spoil the party?