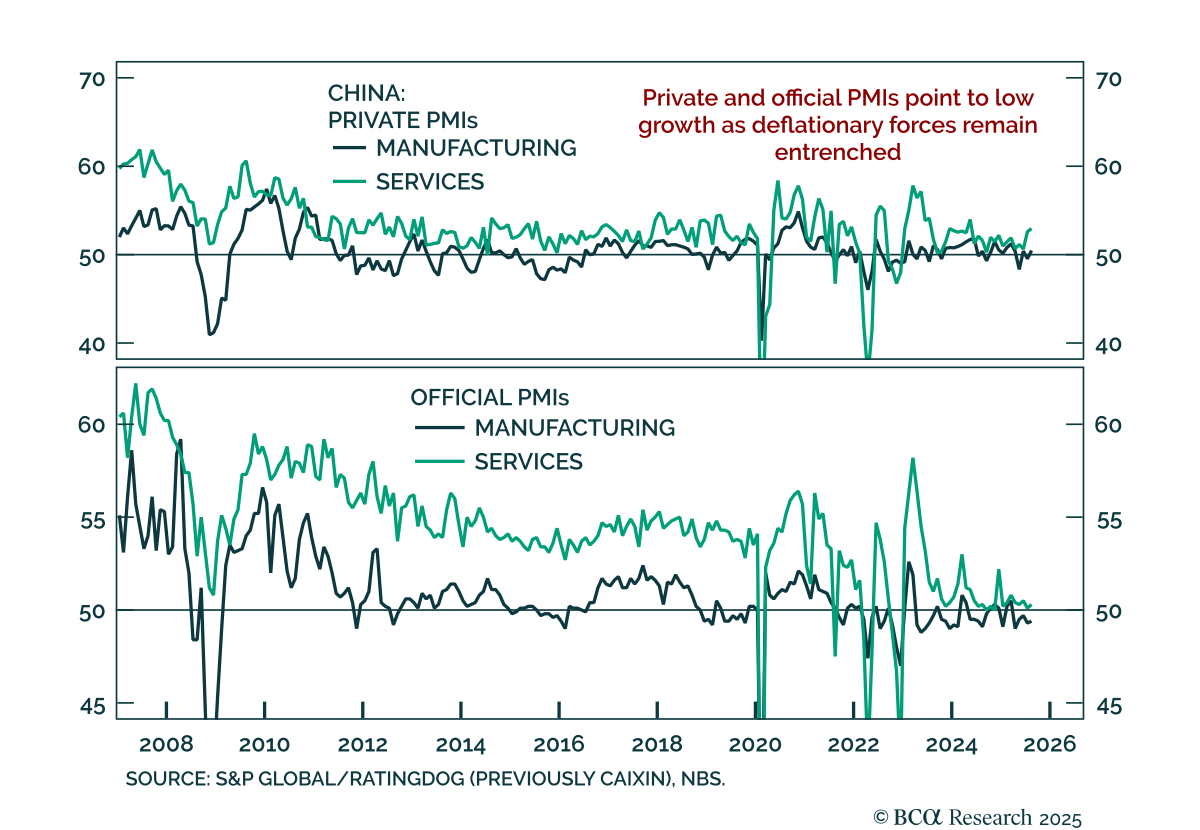

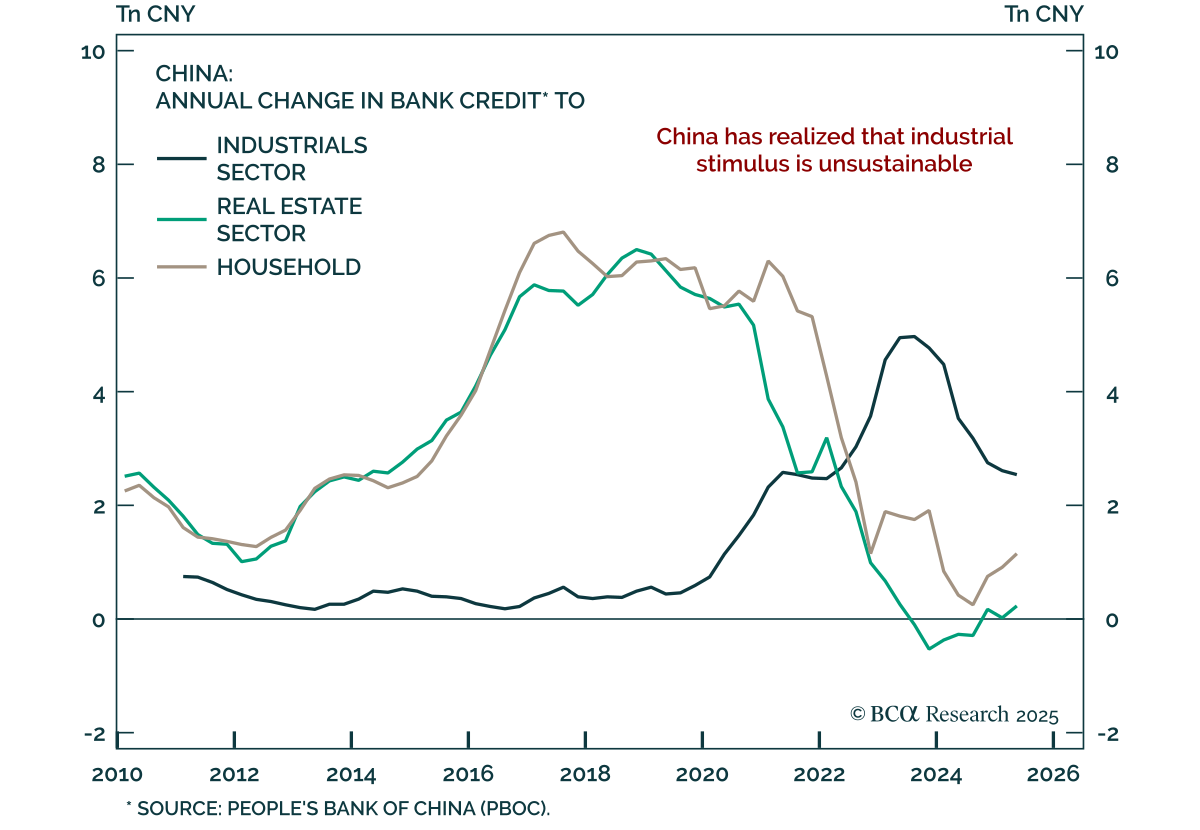

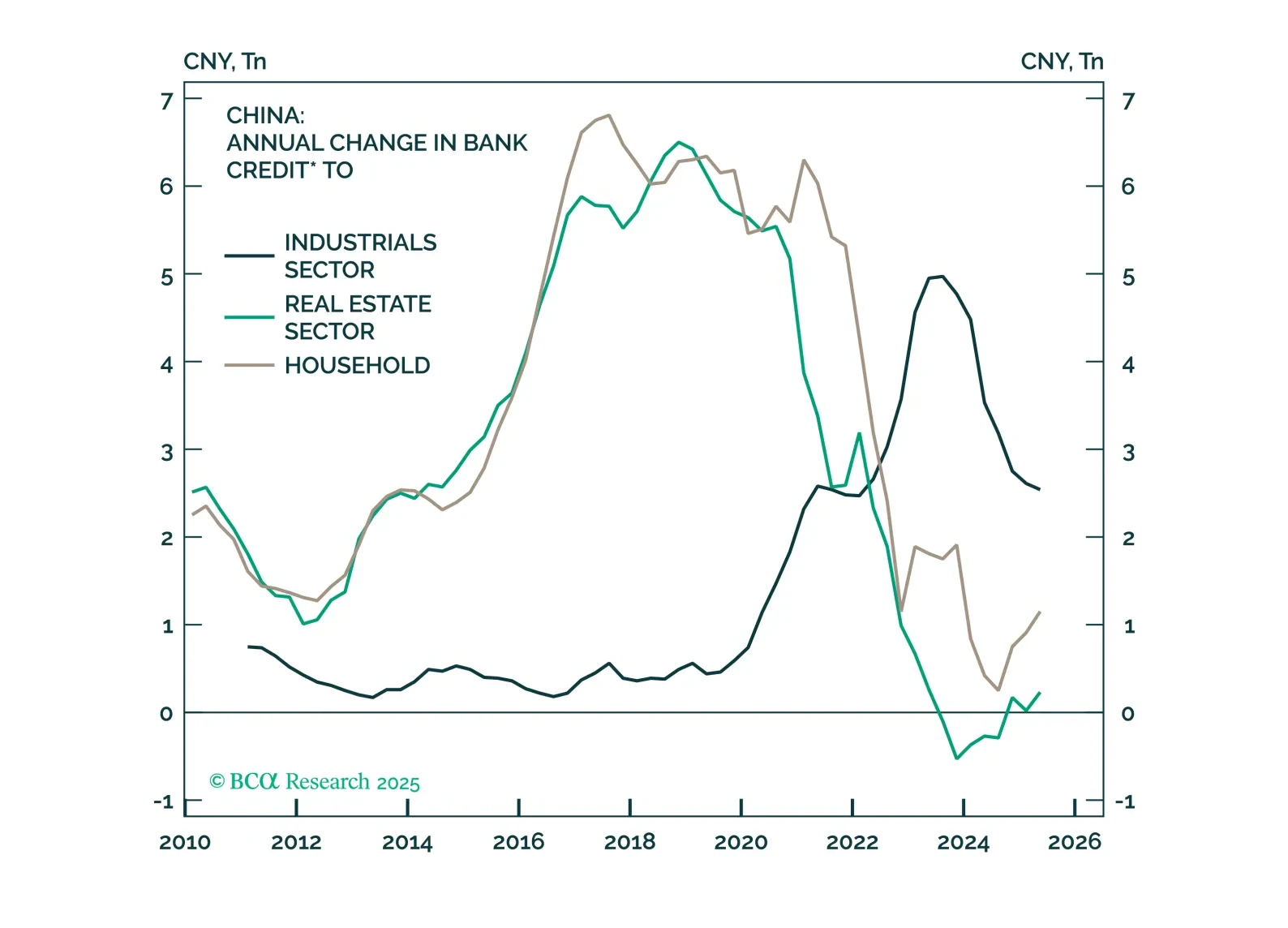

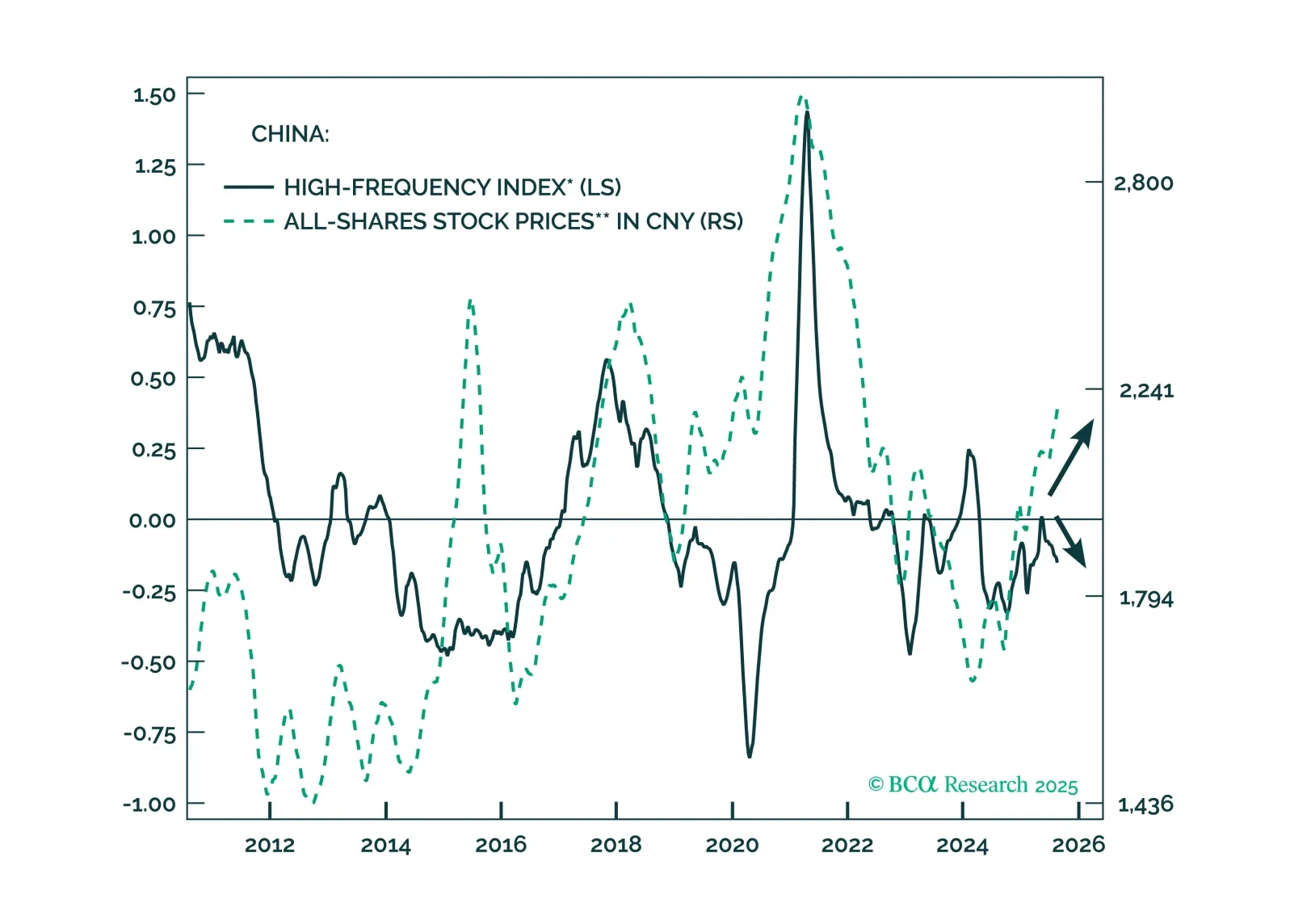

China

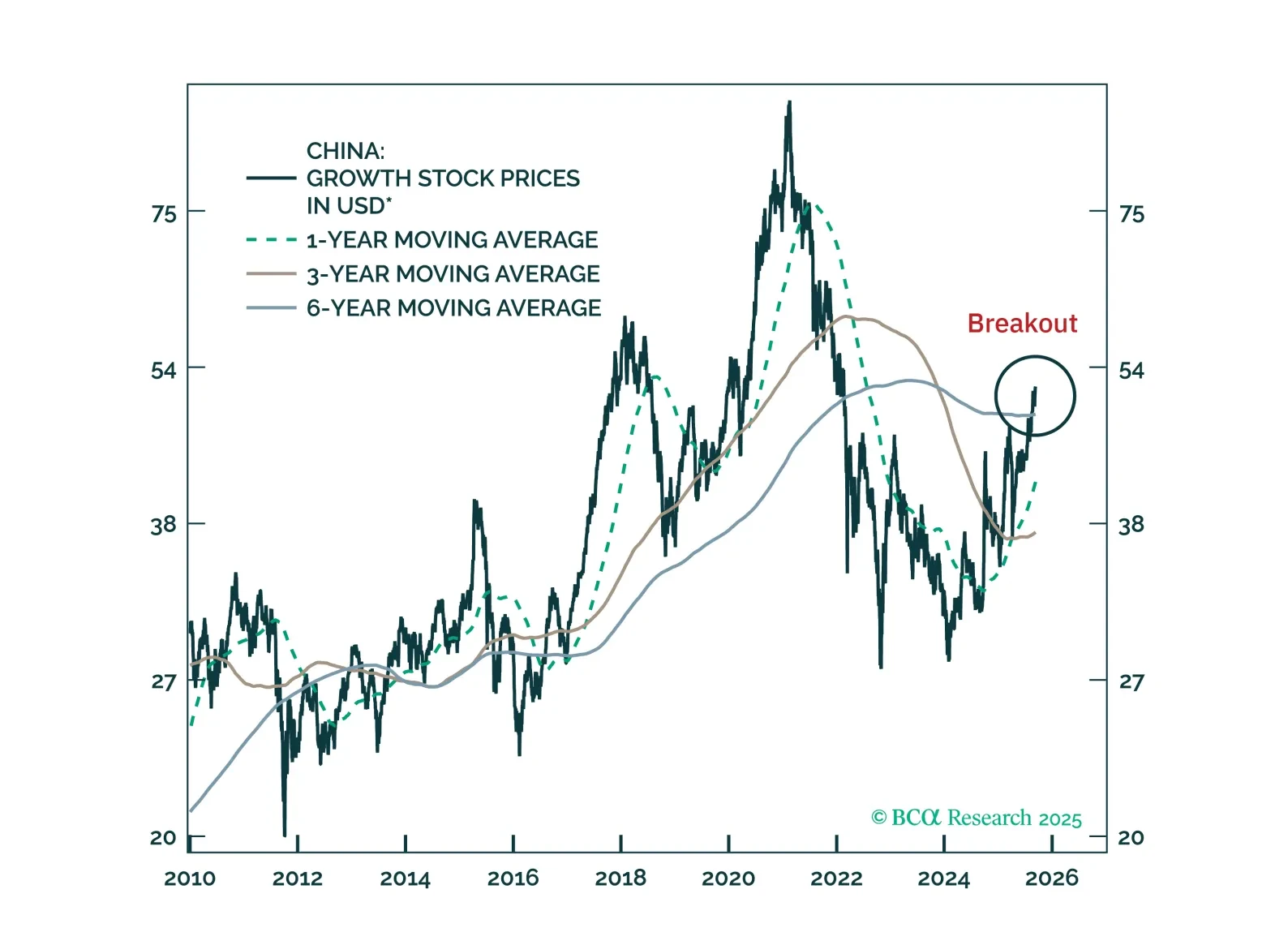

We are turning more constructive on Chinese internet stocks after several years of caution. We recommend going long offshore internet equities in absolute terms and upgrading MSCI China to overweight in a global equity portfolio.

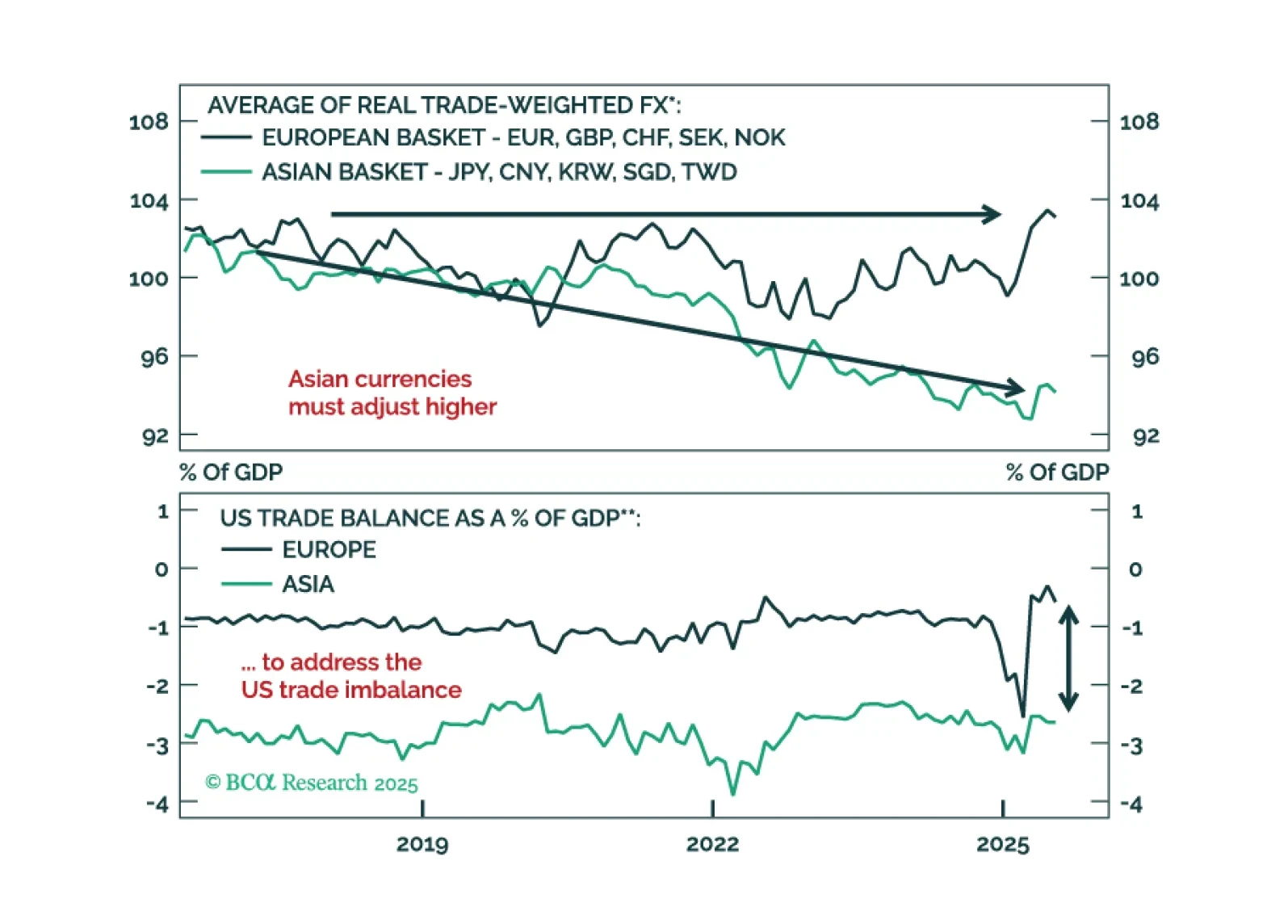

A fleeting greenback rally post Fed rate cut will offer a final chance to reset short dollar exposures. See why undervalued Asian FX are poised to lead the next leg lower in USD and how to position now.

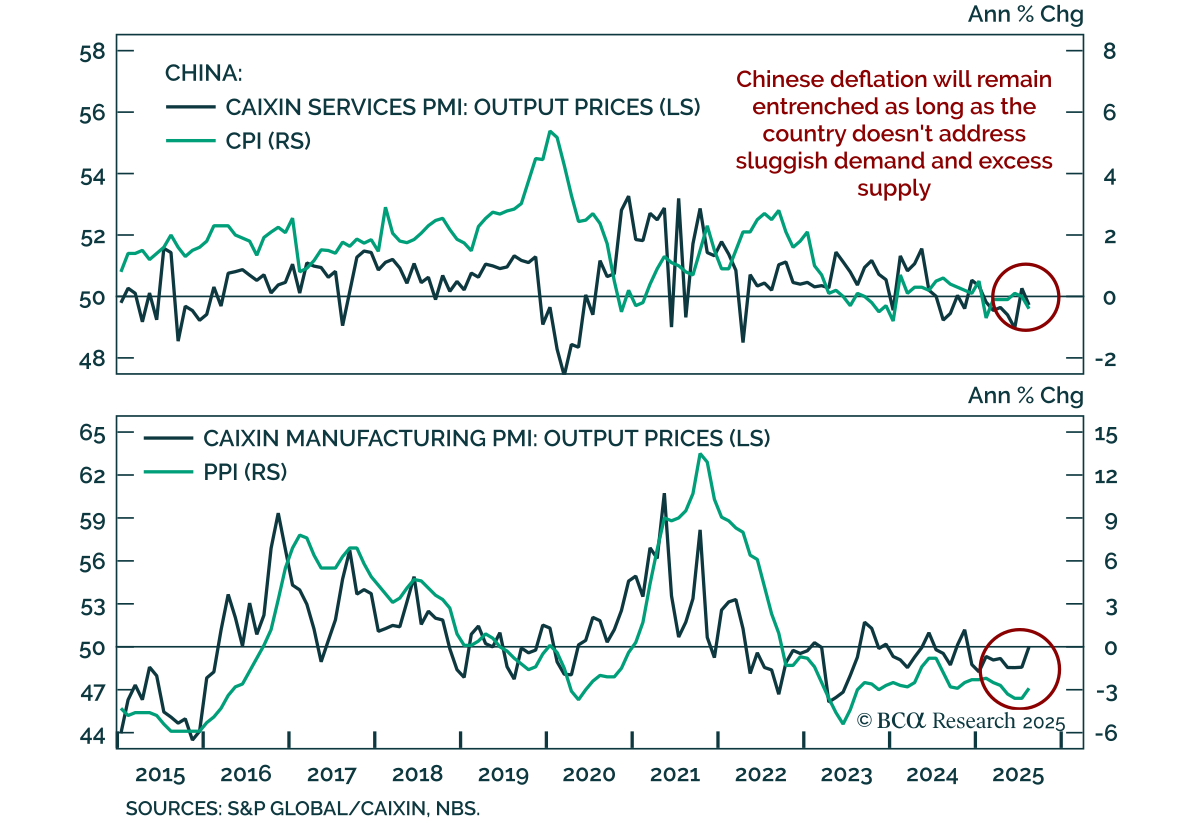

The US overconsumes and underproduces. China overproduces and underconsumes. There are early signs that this decades-old imbalance has peaked and is beginning to reverse. Upgrade the CNY to overweight.

In this week’s Special Report, we introduce our newly constructed China High-Frequency Index (HFI). The HFI provides a timely measurement of China’s current economic conditions, helping investors to gauge cyclical turning points in the economy earlier and identify mini swings within a business cycle.

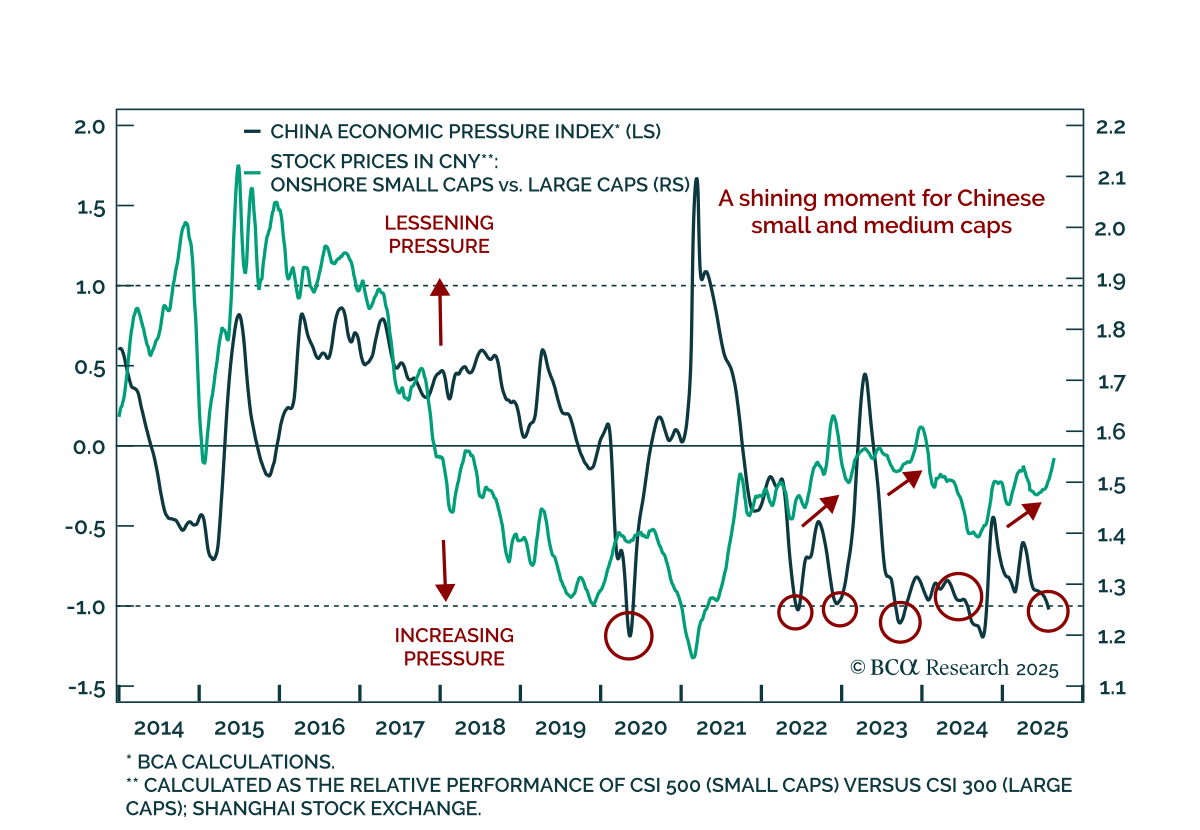

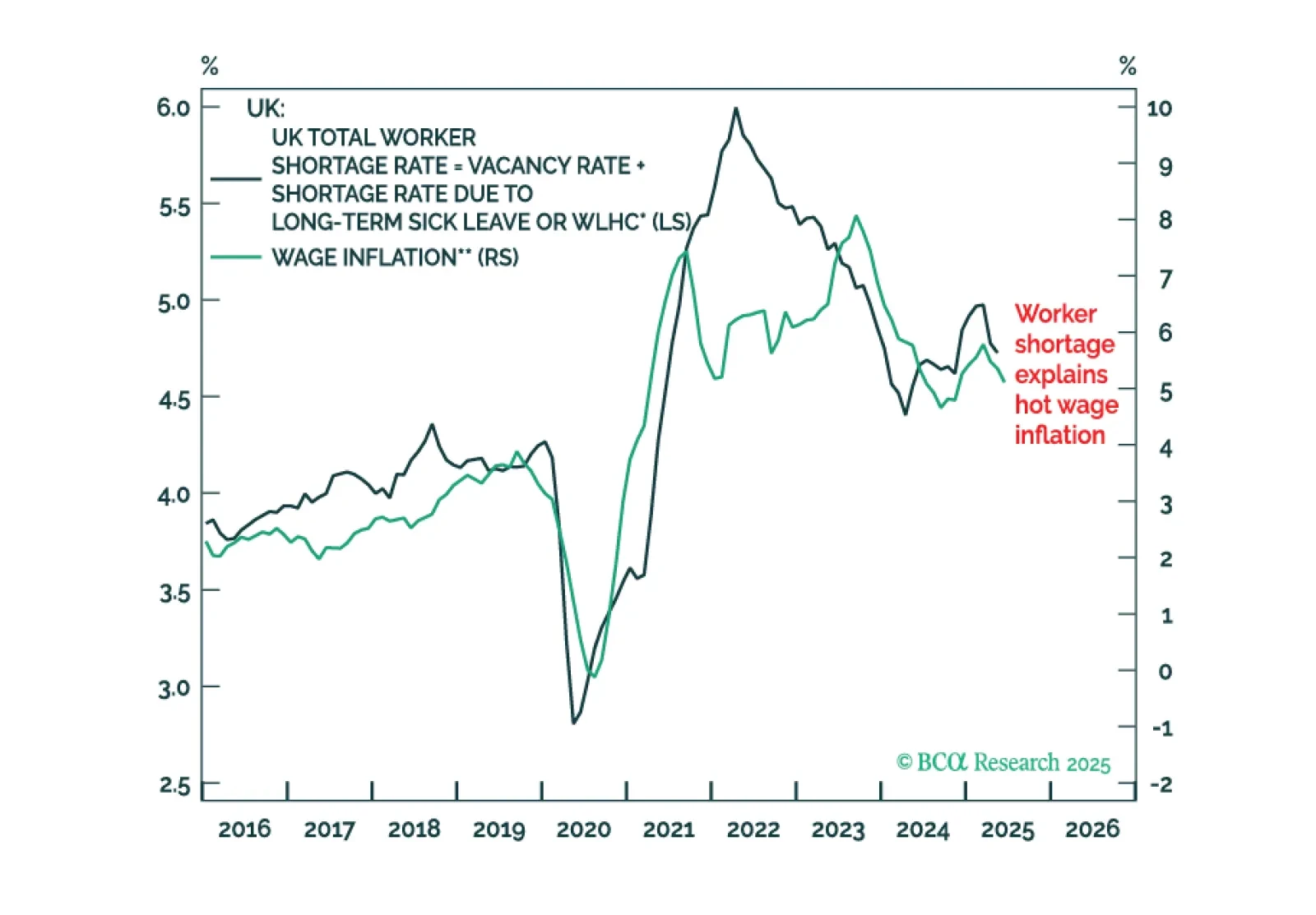

A surge in UK employees on long-term sick leave or with a work limiting health condition explains stubbornly high UK wage inflation. This leaves the Bank of England and the UK government with some tough choices to make in the months ahead. Plus, a new tactical trade is short CSI 300.