China

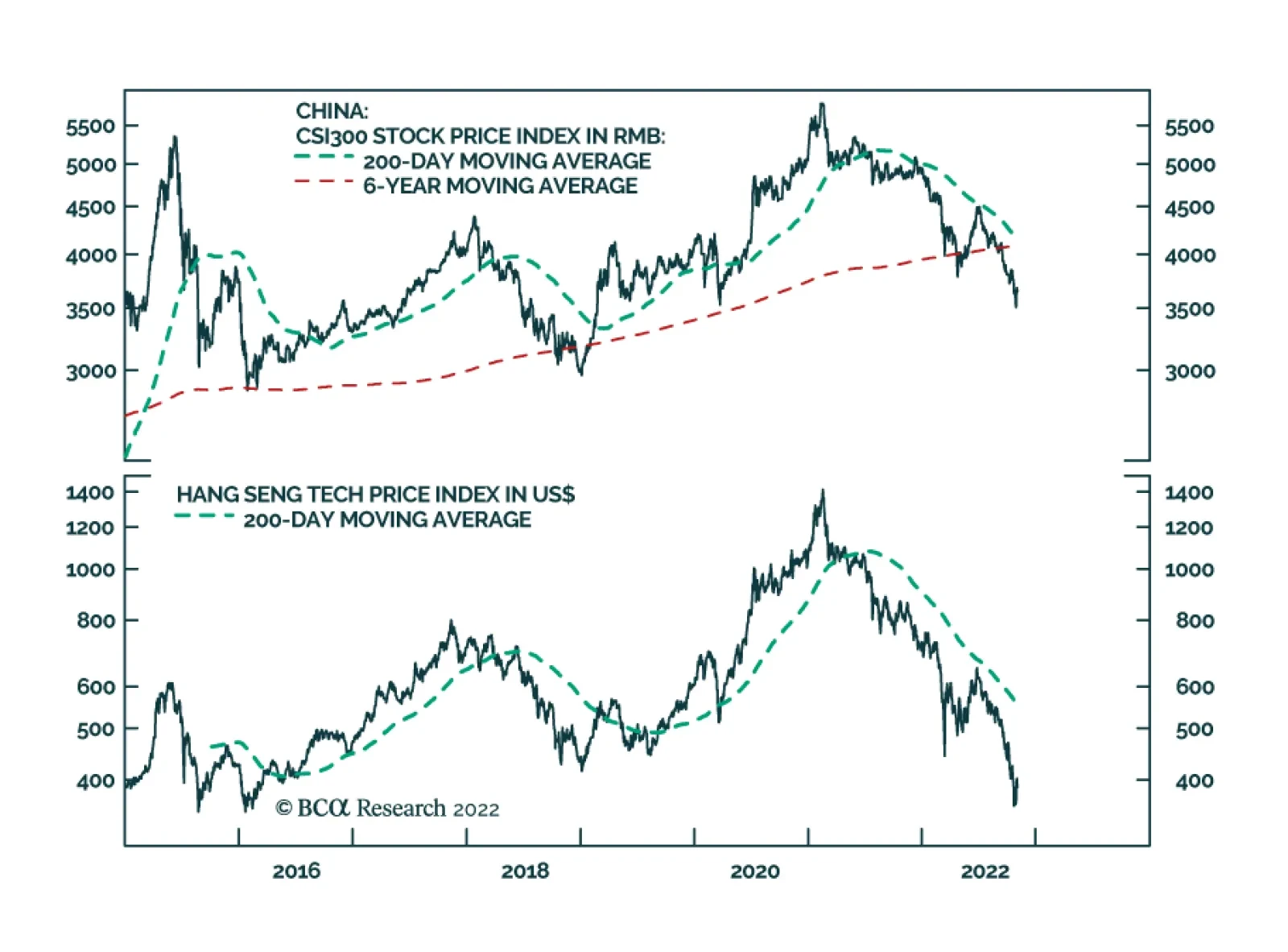

The conditions for a sustainable rally in Chinese stocks have not been met. In this report we discuss the four signposts which we will closely monitor to gauge when it will be warranted to upgrade our stance on Chinese equities both in absolute terms and relative to the global stock benchmark.

Global oil supply will slightly exceed demand in the next six months, resulting in a small surplus. Brent oil prices will trade in a range with a floor at $80 per barrel, barring any geopolitical turmoil in the Middle East and/or escalation in the West-Russia conflict.

The HK dollar is under an assault from rising US interest rates and a weak economy. To defend the exchange rate peg, the HKMA will continue to tighten liquidity, which will boost HK interest rates above those in the US across the entire yield curve. That will cause major damage to this economy and HK-domiciled companies' stocks. Downgrade the MSCI HK equity index within a global portfolio from neutral to underweight.

Copper markets will remain tight on the back of growing physical deficits and pressure on capex. Policy-rate increases by central banks, uncertainty over re-opening in China and its fiscal-stimulus plans in the short run restrain risk taking. In the long run, the implications of China’s inward turn will keep supply-concentration risk for metals high, given its dominance of base-metals refining globally. Notwithstanding the disconnect between physical and futures markets, we remain bullish metals mining equities, and remain long the XME ETF.

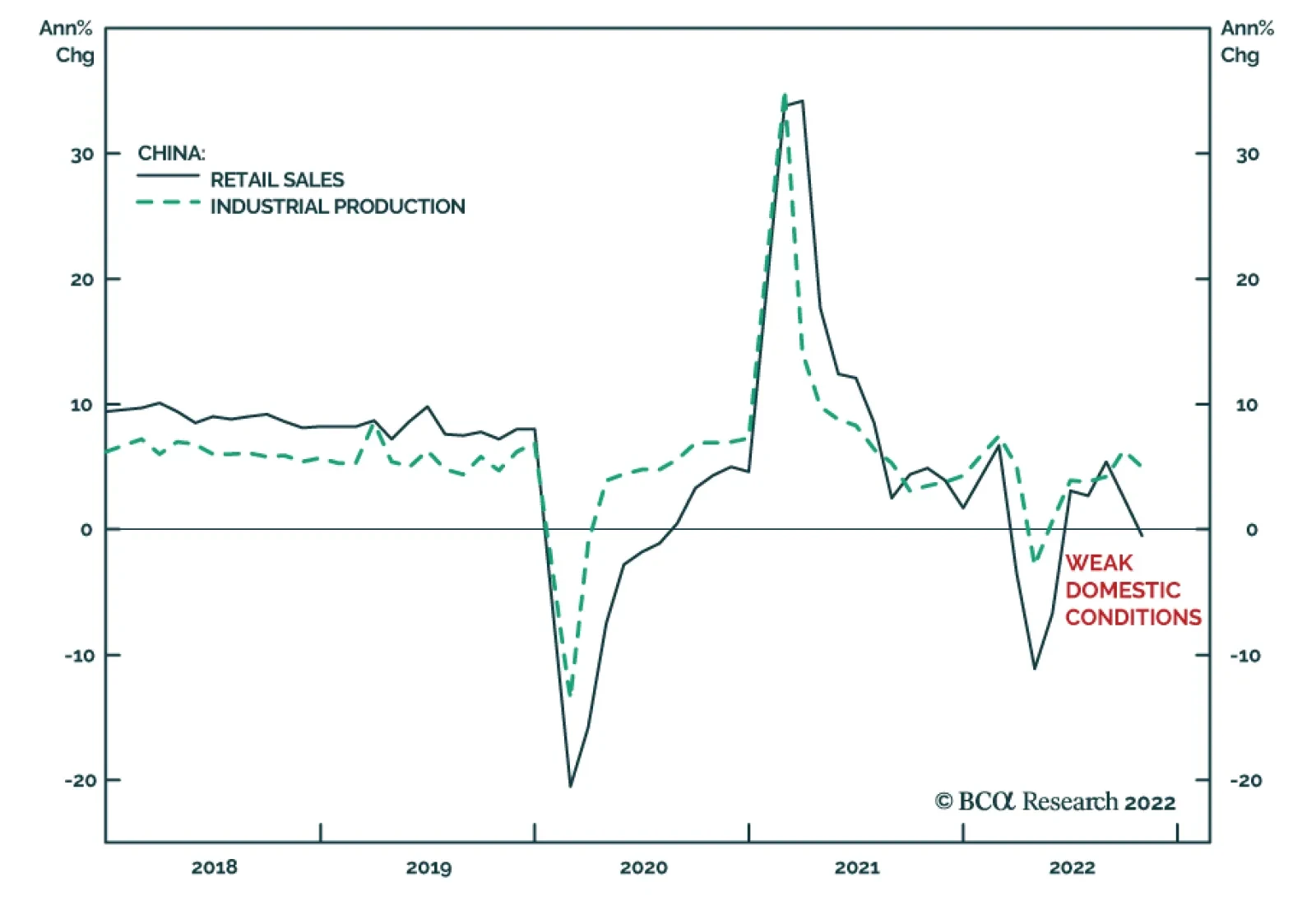

Provided that US inflation is due to excess demand rather than supply constraints, demand destruction will likely be needed to bring core inflation below 3.5%. Such growth contraction is positive for counter-cyclical currencies like the US dollar. In China, the Party's focus is to alleviate structural inequality and a long-term confrontation with the US; and authorities are not yet panicking about the cyclical state of the economy. Hence, an economic recovery is unlikely in the coming months.