China

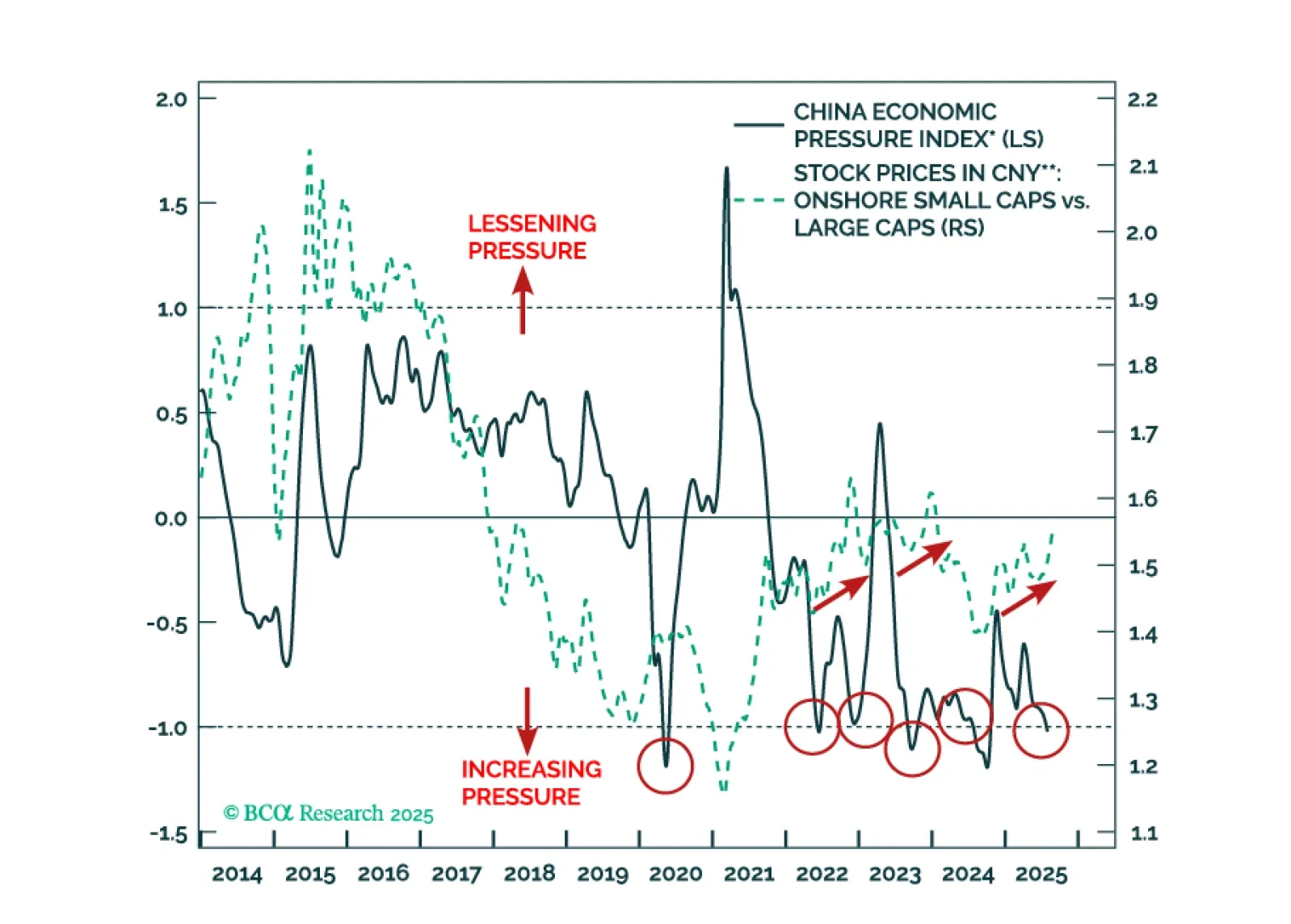

Our newly constructed China Economic Pressure Indicator shows intensifying household stress, raising the likelihood of new policy support in the coming months. We recommend a tactical trade as a stimulus hedge.

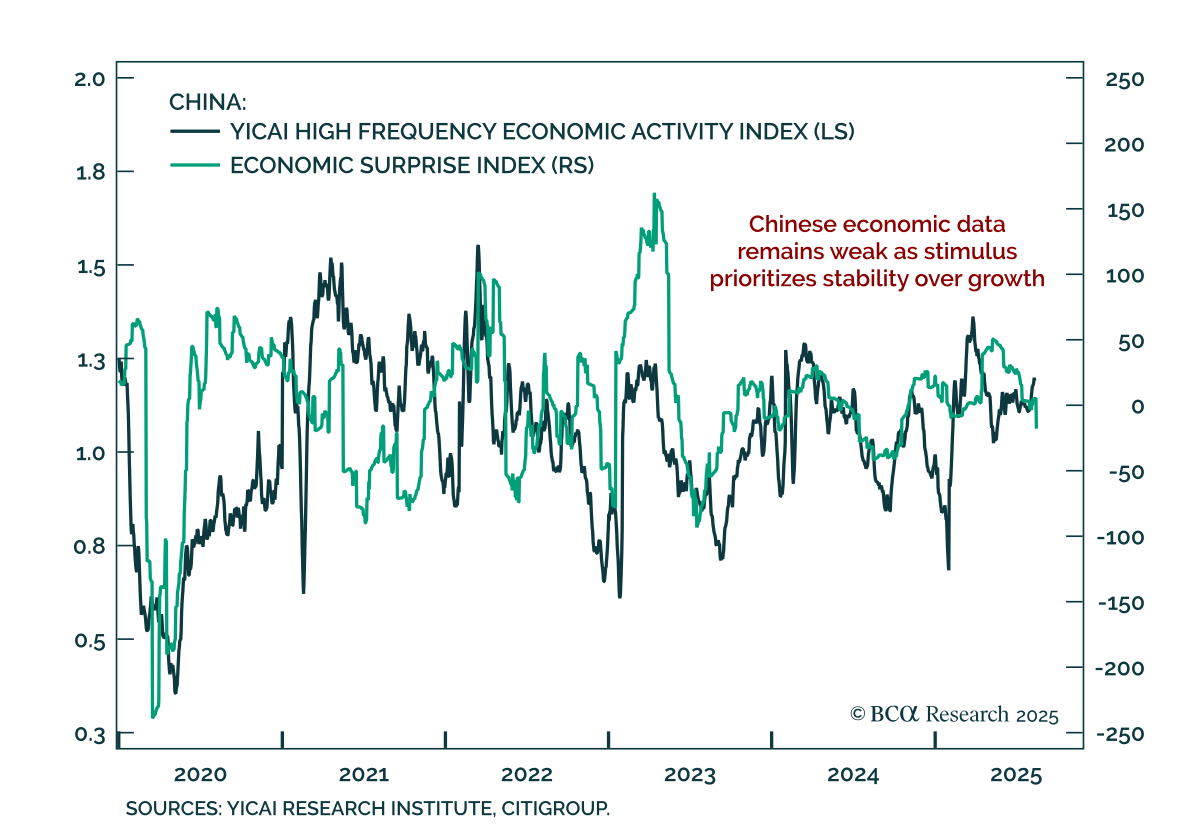

July data confirm China’s weak growth, with no near-term shift toward meaningful stimulus. New home prices fell 0.31% m/m, retail sales slowed to 3.7% y/y from 4.8%, and industrial production eased. Flooding in July disrupted infrastructure spending…

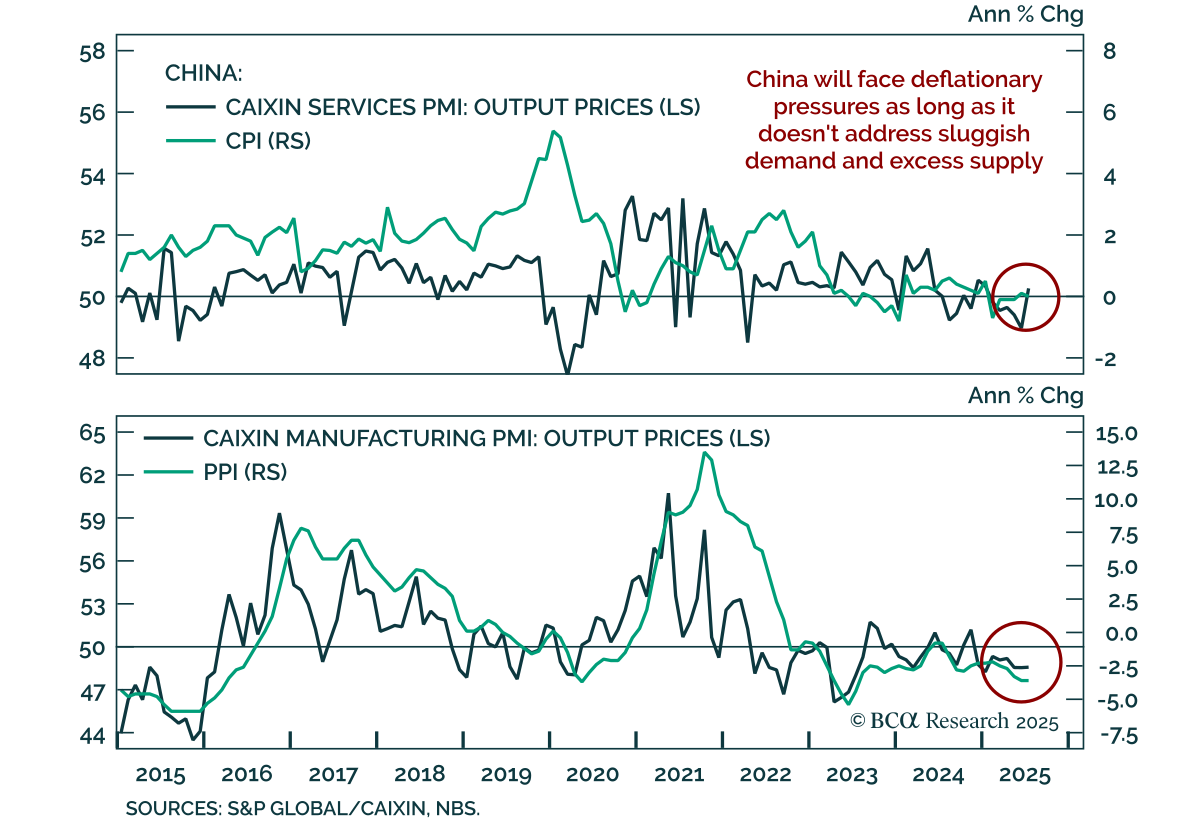

China’s July inflation data confirmed entrenched deflation, reinforcing our defensive stance on Chinese equities and overweight in onshore bonds. CPI slowed to 0% y/y from 0.1%, while factory-gate prices stayed deeply negative at -3.6% y/y. Weak…

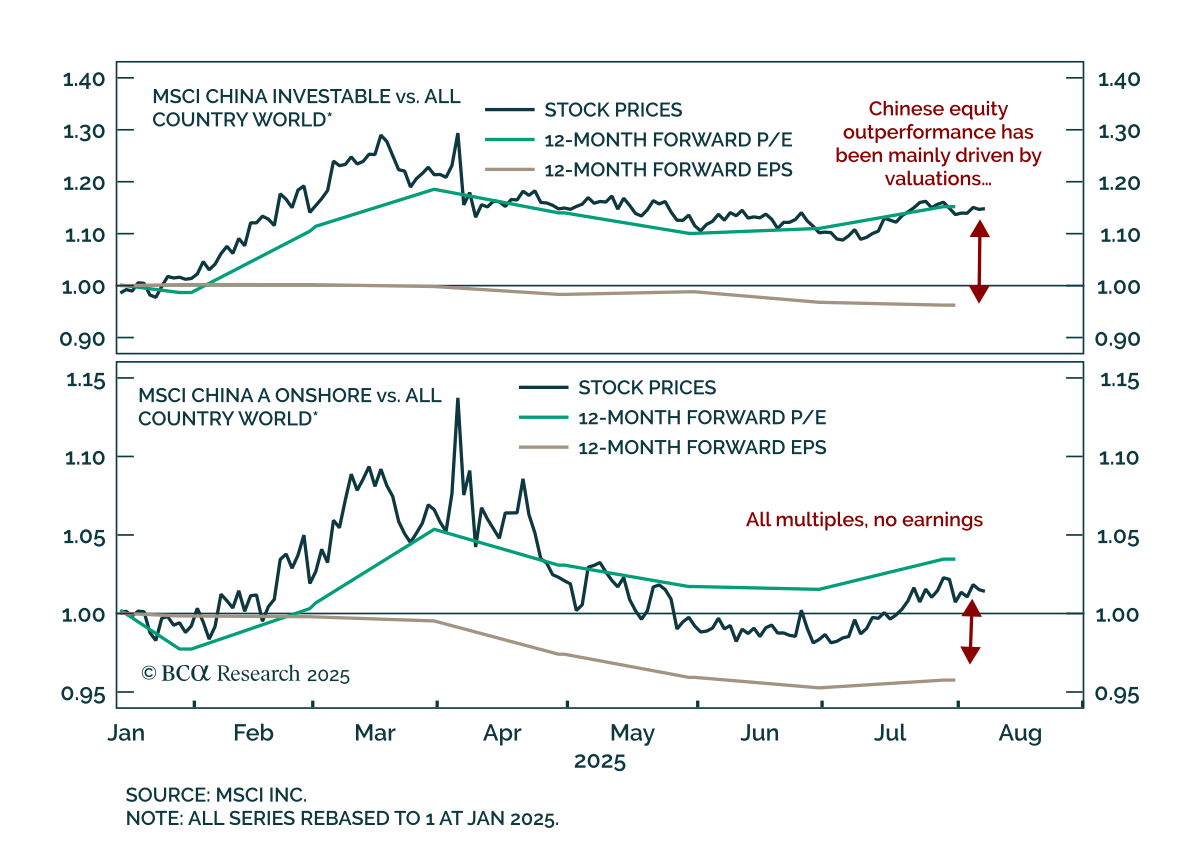

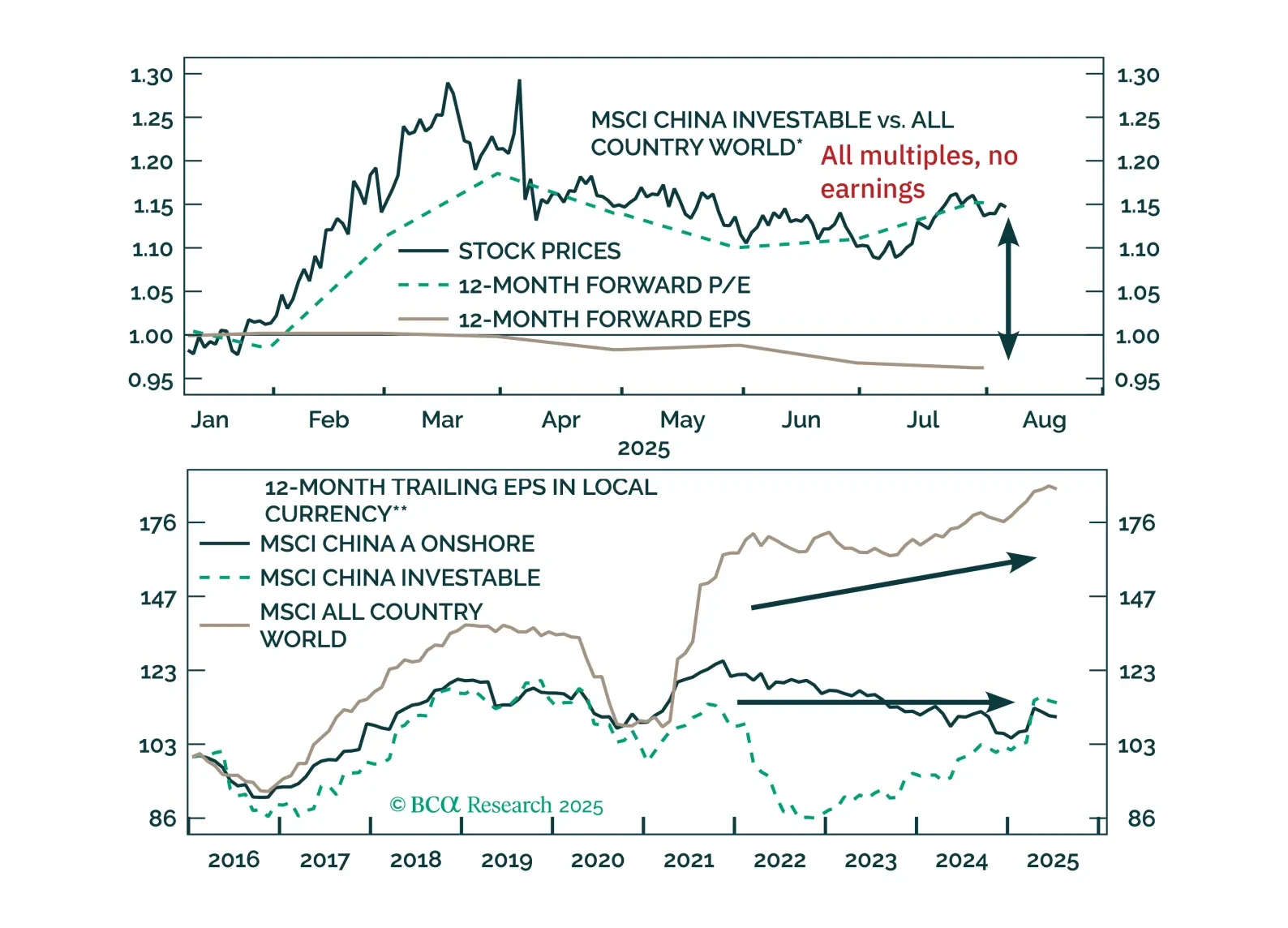

Our China Investment strategists maintain a defensive stance on Chinese equities, favoring A-shares over offshore markets. The earnings outlook remains weak, and the full impact of US tariffs has yet to be felt. Chinese equities have decoupled from the…

Chinese stock prices have significantly decoupled from the country’s business cycle, with the full impact of US tariffs yet to be realized. The valuation-driven equity gains without a cyclical economic recovery will be vulnerable to a reversal.

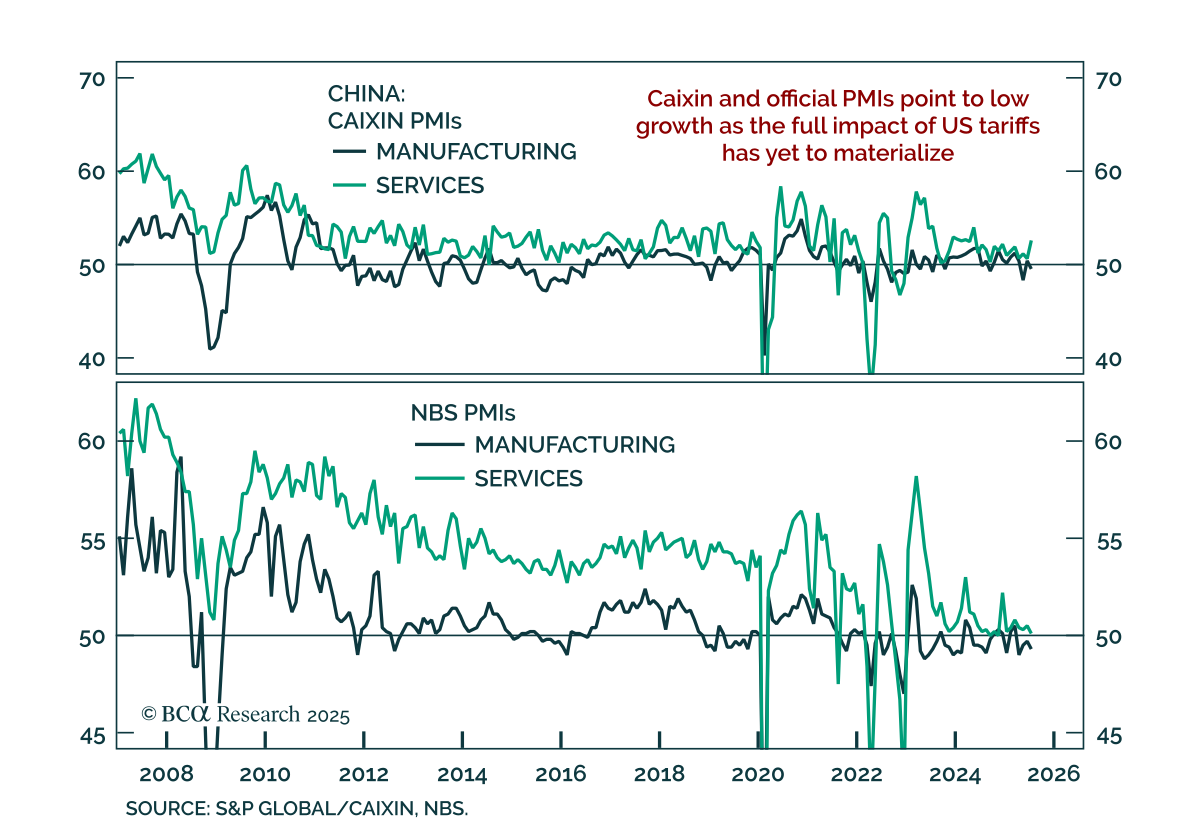

The July PMIs and inflation data confirm that China faces a persistent low-growth, deflationary backdrop, with weak demand and tariff risk warranting defensive equity positioning. The Caixin manufacturing PMI fell to 49.5, while services ticked up at 52.6.…

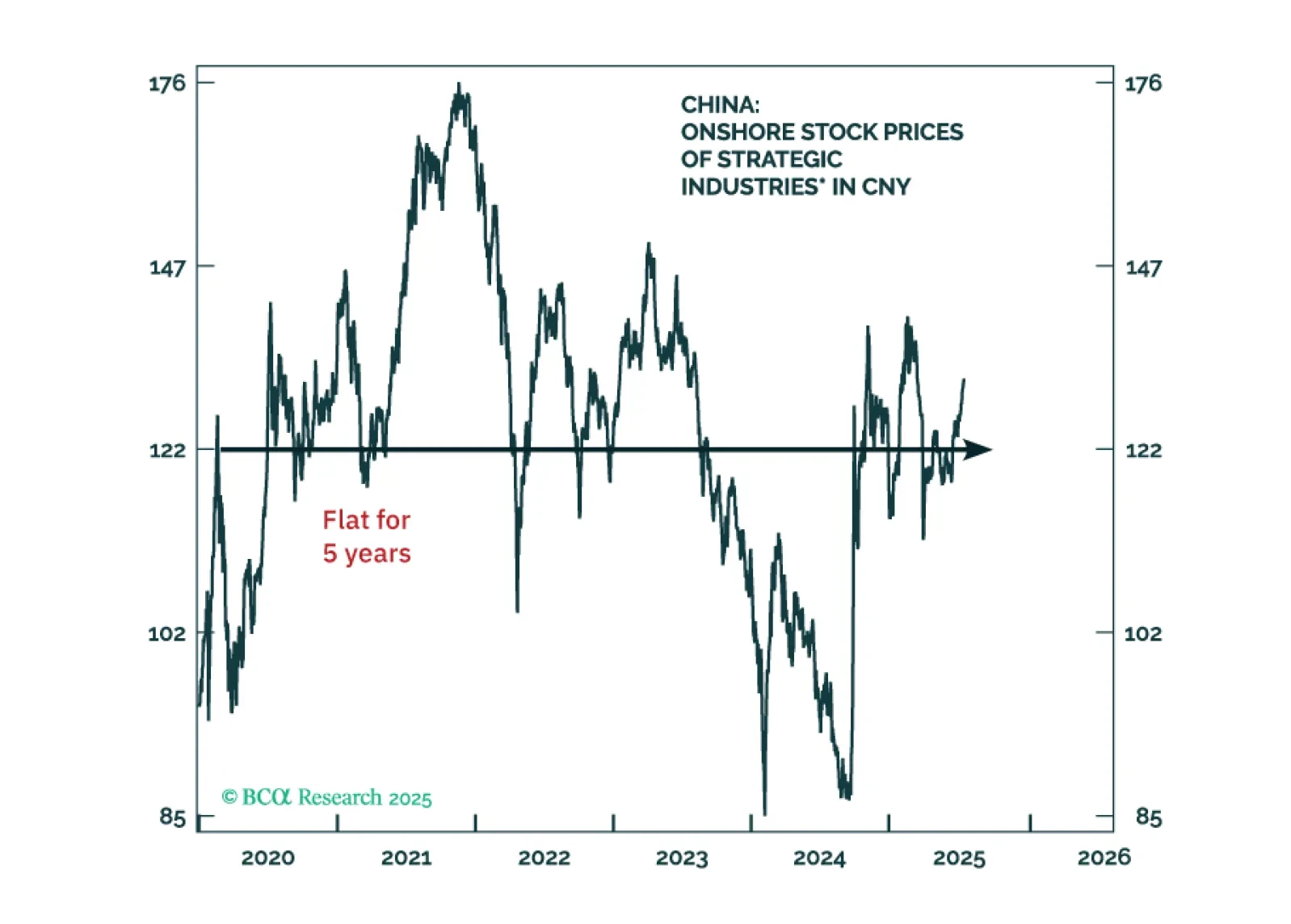

Investors often ask us which industries the Chinese government is prioritizing for expansion. The assumption is that investing in sectors hand-picked authorities will produce solid investment returns. Yet, this assumption has not held over the past decade.

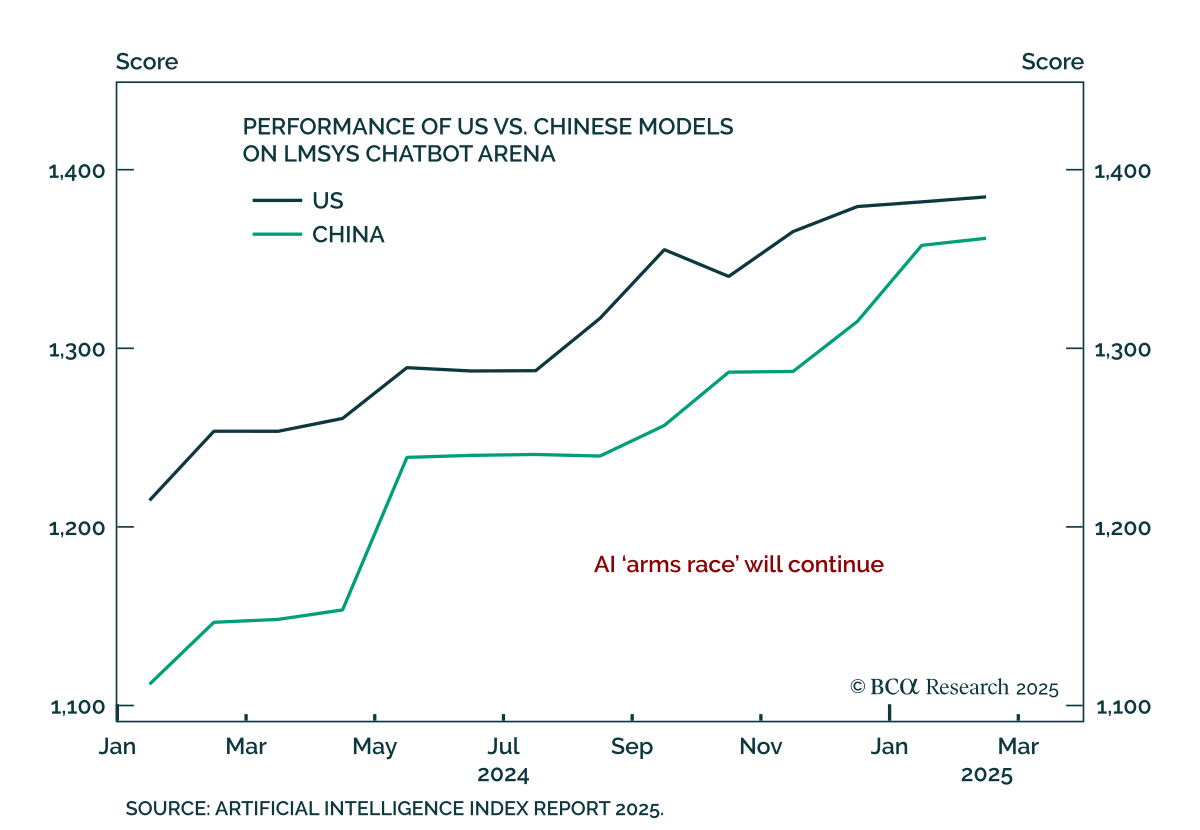

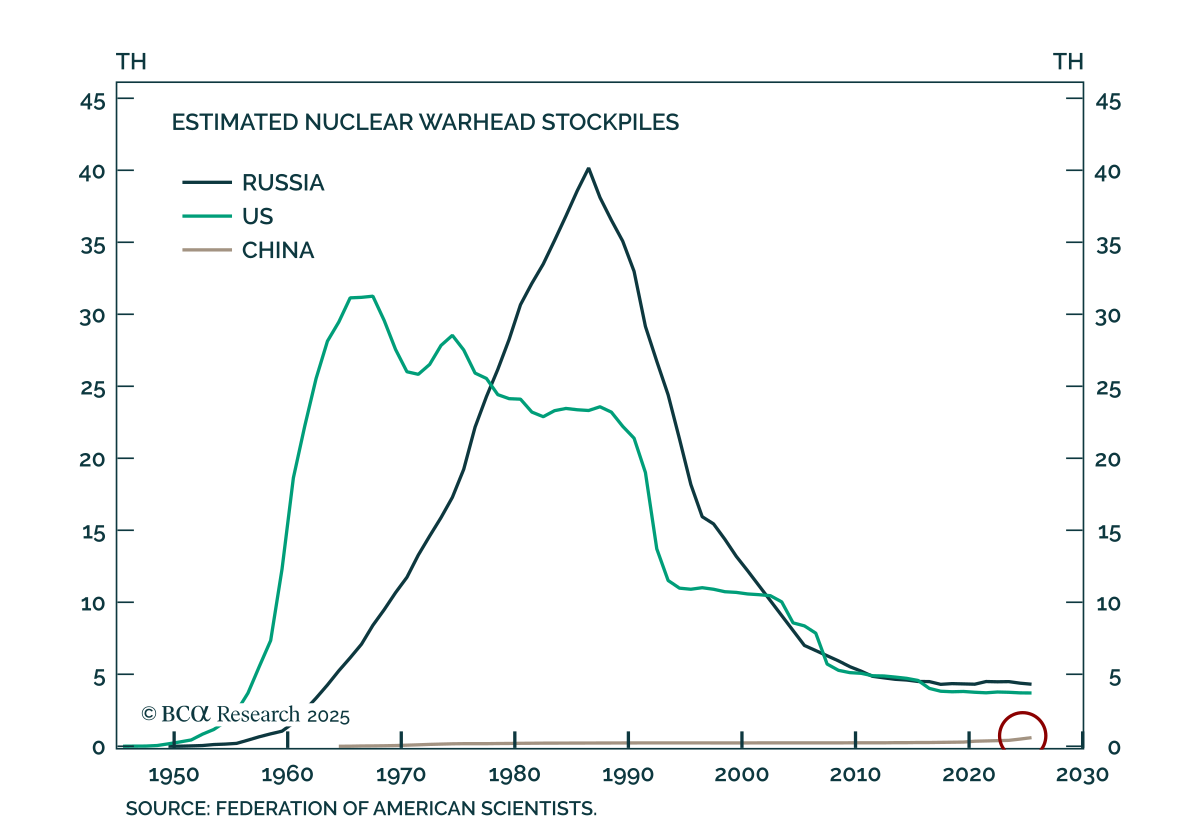

BCA’s Geopolitical strategists argue that artificial intelligence will destabilize both domestic politics and international security, prompting more aggressive fiscal responses. President Trump’s July 23 executive orders to accelerate US AI innovation,…

BCA’s Geopolitical strategists advise investors to remain open to the possibility that a new Cold War dynamic is forming in global trade. While the US-China rivalry does not map perfectly onto the original Cold War, the analogy retains analytical value. US…

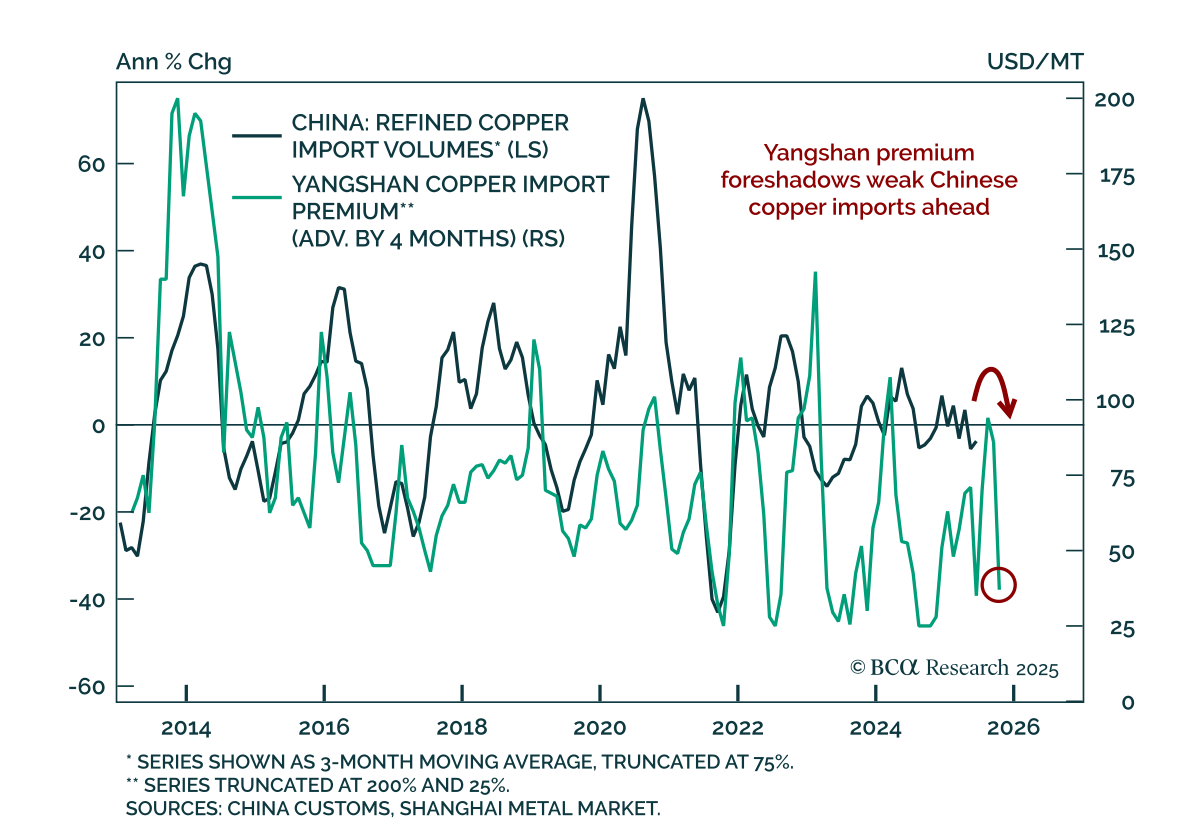

BCA’s Commodity strategists remain long gold/short LME copper and have initiated an outright short in LME copper as a cyclical trade. The US copper tariff will redirect supply away from the US, replenishing depleted inventories elsewhere and exerting downward…