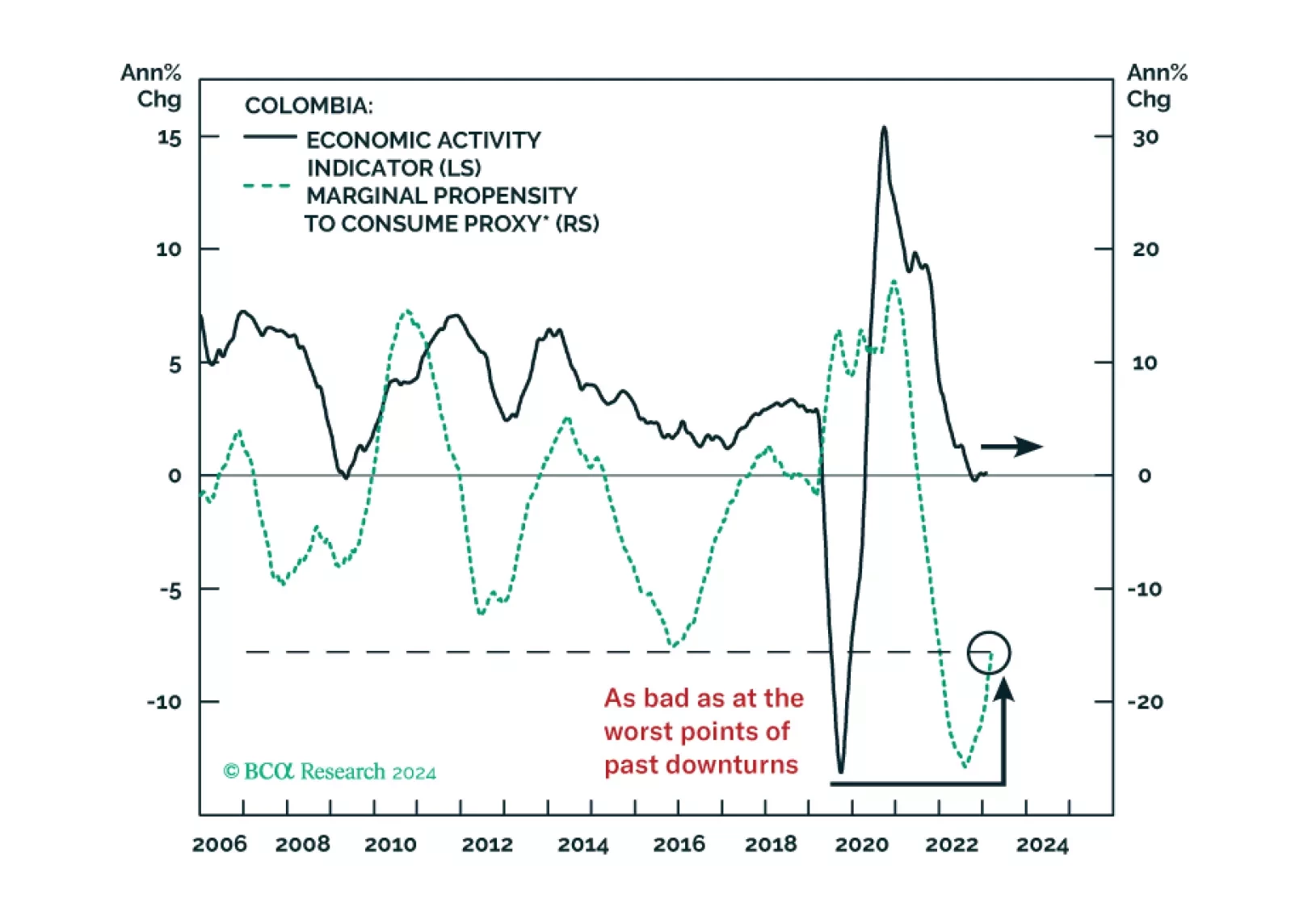

Executive Summary Colombian Stocks Failed To Break Above Technical Resistances The economy is booming, but capacity constraints are already biting. Structurally, the election of leftist Gustavo Petro will entail a permanent increase in fiscal spending, worsening public debt dynamics, and falling export revenues and FDIs into the oil and coal sectors. The new government’s policies alongside its anti-corporate rhetoric will have the perverse effect of diminishing business confidence and thereby gross investment across the whole economy. On the external front, an already large current account deficit, falling commodity prices, capital flight from wealthy Colombians and falling FDIs will continue to weigh on the peso. Recommendation Inception Date RETURN Downgrade Colombian Local Bonds and Sovereign Credit to underweight within EM fixed-income portfolios 2022-08-16 Bottom Line: Expect more pain ahead for Colombian markets. We recommend that investors have an underweight allocation relative to EM across all asset classes: equities, currencies, local bonds and sovereign credit. Feature Colombian assets and the economy are facing cyclical and structural headwinds. On the one hand, the economy is experiencing classic overheating: inflation is at a multi-decade high, the labor market is tight, and growth has run into capacity constraints. In response, the central bank (Banrep) has no choice but to continue tightening policy and engineer a major growth slump. On the other hand, as we have been writing since June of last year, Colombia is undergoing an unprecedented social and political shift to the left. This societal change was cemented in June with the election of the country’s first leftist President, Gustavo Petro. His policies will have negative repercussions in the economy in the form of lower business confidence, falling FDIs, higher government intervention, and ballooning public debt. Nevertheless, Petro’s most radical policies will be challenged by his own broad alliance in Congress established with centrist and traditional parties. All in all, Colombian equities and the currency will continue underperforming versus EM peers, leading us to maintain our underweight stance on stocks and reiterate our short position in the COP versus the US dollar. We are also downgrading our allocation to local bonds and sovereign credit from neutral to underweight. Classic Overheating Colombia is undergoing classic inflationary overheating. Headline and core consumer price inflation have reached a two-decade high, and other core measures of inflation are at similar levels (Chart 1). This implies that rising price pressures are genuine and broad based. Inflation will remain high and persistent going forward, as the Colombian economy has hit capacity constraints and a wage-price spiral is well underway: The labor market is tight, with nominal wages rising rapidly at 13.4% – and quite above core cpi (Chart 2). Further, the unemployment rate has fallen back to reasonably low levels. Chart 1Colombia: Inflation Is High And Broad Based Chart 2Colombia: Nominal Wages Are Outstripping Inflation The levels of activity in various segments of the economy have meaningfully surpassed their pre-pandemic levels in volume terms (Chart 3). As a sign of booming domestic demand and hidden inflation, the current account deficit is almost at historic lows, despite sky-high oil prices (Chart 4, top panel). Accordingly, imports of consumer goods are booming (Chart 4, middle panel). Chart 3The Colombian Economy Is Overextend Chart 4Colombia: Signs of Strong Domestic Demand In addition, real consumer demand has outgrown real capital expenditures (Chart 4, bottom panel). In general, when demand outpaces productive capacity, inflation intensifies. This is what has transpired in Colombia. According to data from Banrep, the country’s output gap is now positive at 1% of potential GDP, entailing the economy is operating above capacity. To add further fuel to the fire, the newly proposed fiscal budget for 2023 is significantly expansive, with total expenditures being 12% higher than the 2022 budget and 43% higher than 2021 expenses. Additionally, the newly elected finance minister, José Antonio Ocampo, wants to revise the 2023 budget even higher. He also plans to delay reducing the fiscal deficit by a year. Consequently, the government balance will remain negative around -5.6% of GDP in 2023. In line with the above, inflation expectations by businesses have skyrocketed (Chart 5). This means they will not only be willing to hike wages but will also raise their selling prices. In short, a wage-price spiral has been put into motion. Given the magnitude of overheating, the central bank has no choice but to continue to hike rates aggressively. Banrep has raised rates by a historic 725 basis points since September 2021 to 9%. However, given headline and core inflation are at 10.2% and 8.4% respectively, monetary policy is not restrictive enough – real interest rates are close to zero. We expect Banrep to continue its rate hiking cycle into the end of the year, particularly in the face of a hawkish Fed and a strong US dollar/local currency depreciation. Given the economy has very strong growth momentum, and the credit impulse is very high, it will not slow down immediately (Chart 6). Chart 5Business Inflation Expectations Are Unhinged Chart 6The Colombian Economy Will Not Slow Down Yet Chart 7Prepare For Further Yield Curve Inversion This and easing fiscal policy will give the central bank strong reasons to continue raising rates in large increments in the months ahead. Eventually, this will produce a major growth slump sometime in 2023. Bottom Line: The economy is booming but capacity constraints are already biting. Surging inflation means the expansion is unsustainable. The upshot is continuous central bank tightening until domestic demand slumps considerably. For now, an overheating economy, runaway inflation, continuous rate hikes and growing prospects of an economic downturn in 2023 warrant a more drastic yield curve inversion (Chart 7). The currency remains at risk of a widening current account deficit and a potential US dollar overshoot. Petro’s Policies Hinder Long-Term Growth The election of leftist outsider Gustavo Petro is consistent with the average voter’s tilt towards the left, as well as the rejection of traditional centrist and right-wing policies. With this historic societal political shift, it is clear the new government will move away from a tradition of small budgets and orthodox fiscal policy towards significant state spending on social programs, particularly on education, health and pensions. Below we analyze Petro’s proposals and relationship with Congress, as well as the implications for businesses and Colombia’s structural outlook. First, Petro’s most radical reforms will be watered down in Congress, but do not expect traditional parties to fully block his proposals. On the one hand, Petro’s original left-wing coalition (the Historic Pact) has only 15% of seats in Congress and 19% in the Senate. This has forced the President to form a broad alliance with traditional centrist parties (such as the Liberal Party and the Union Party). This new alliance holds a small majority of 56% and 58% in Congress and the Senate, respectively. However, many of its individual members are centrists and right wing and might not always support Petro’s government. Therefore, we can expect the traditional political class to push back on Petro’s intentions to overhaul Colombia’s socio-economic model. On the other hand, moderate and right-wing parties have an incentive to support a permanent increase in fiscal spending to not distance themselves even further from the median voter – who has taken a leftward shift. This is evident even within right-wing ex-President Iván Duque’s government, which has submitted an expansionary budget for 2023.1 All in all, we expect Petro and Congress will work together to meaningfully increase government spending, but more radical reforms will be watered down and implemented gradually but not eliminated entirely. While Congress will probably support Pero’s tax reform to increase collection and raise income and wealth taxes on high-earning Colombians, the finance minister has already stated it will be implemented in a gradual manner, reducing the collection target from 5% to 1.7% of GDP in 2023. This suggests the significant increase in government spending will not be offset by higher revenues. Second, fiscal largesse will worsen public debt dynamics. Colombia’s fiscal accounts are already in a precarious position: the fiscal deficit is the widest in history (excluding the peak of the pandemic), and public debt has risen to 71% of GDP (Chart 8, top and middle panels). To make matters worse, 40% of gross public debt is nominated in foreign currency. Going forward, gross public debt will rise meaningfully due to (1) persistent and large fiscal deficits; (2) continuous currency depreciation; and (3) local bond yields hovering significantly above the nominal GDP growth rate (Chart 8, bottom panel). As long as these three conditions remain, the public debt-to-GDP ratio will continue spiking. Further, falling oil prices will negatively impact fiscal accounts, as oil revenues account for 15% of total government revenues. BCA’s Emerging Markets Strategy service believes oil prices have formed a major top and will average well below $100 per barrel in the years to come (Chart 9). Chart 8Colombia: Public Debt Dynamics Will Go From Bad To Worse Chart 9Global Oil Prices And Energy Stocks Are Heading For A Downturn Third, Petro’s environmental proposal of banning new oil explorations and new open pit mining projects will reduce FDIs into the energy and mining sectors, and ultimately curtail export revenues. Colombia’s oil and coal exports account for a massive 34% and a 17% share of total exports, respectively. Worryingly, oil and coal output have not recovered in the past two years (Chart 10). A lack of new investment will accelerate the fall in production and, hence, export revenues. In short, all these will have a perverse effect on the balance of payments. Even if Congress is able to persuade the government to water down the outright ban on new projects, and instead opt for increased regulation and red tape for extractive industries, the economy will experience declining domestic and foreign investment in these sectors. The new finance minister has already proposed imposing a 10% tax on oil and coal exports if their prices exceed $48 per barrel and $87 per ton, respectively. Fourth, there are a myriad of other economic policies in the new government’s wish list which will hurt the nation’s productivity in the long term. The ones that stand out are raising import barriers and re-establishing diplomatic relations with Venezuela. The last one is particularly worrisome because it may undermine the trust and cooperation Colombia has with the US government and multinationals, which have diplomatically and economically shunned the Venezuelan government. Being the most important regional ally with the US, Colombia could miss out on a golden opportunity as an international manufacturing hub for nearshoring efforts away from China and Emerging Asian countries. Finally, all these policies will serve to meaningfully worsen business confidence. As we have seen in Mexico, rising state intervention in the energy sector and anti-corporate rhetoric can hurt business confidence and investment across the entire economy (Chart 11). Chart 10Colombian Commodity Production Has And Will Not Recover Chart 11Poor Business Confidence Will Hurt Gross Investment Across The Whole Economy Bottom Line: Petro’s policies will have negative repercussions for fiscal accounts and meaningfully hinder the country’s productivity and long-term potential growth. This calls for a structural derating in Colombian risk assets. Balance Of Payments Dynamics Will Only Get Worse Colombia’s external environment is also set to deteriorate over the medium- and long-term horizons. Cyclically, falling oil and coal prices resulting from a global slowdown will weigh heavily on the Colombian peso. Additionally, currency depreciation will be aggravated by short-term capital flight from wealthy Colombians as they seek to protect their incomes from tax hikes. Structurally, Petro’s environmental policies against new oil exploration and open pit mining projects will constrict future exports of oil and coal. This will also weigh on FDIs, of which 11% and 8% are destined towards oil and mining projects, respectively. We believe investment in current oil and mining projects will also be curtailed as domestic and foreign investors see less future growth in these industries. Bottom Line: Colombia’s balance of payment dynamics will go from bad to worse (Chart 12). Investment Recommendations Given the bleak cyclical and structural outlook for the Colombian economy, our recommendations are as follows: Equities: A combination of high and persistent inflation, rising interest rates and a troubling structural outlook lead us to maintain an underweight position in Colombian equities within an EM equity portfolio. As a bearish signal, Colombian stocks have nosedived below long-term moving averages in absolute and relative terms (Chart 13). Chart 12Colombia's Current Account Deficit Is The Country's Achille's Heel Chart 13Colombian Stocks Failed To Break Above Technical Resistances Currency: High inflation, falling oil prices and an already large current account deficit make for a dangerous cocktail for the Colombian peso. Stay short versus the US dollar. Fixed Income: Regarding local bonds, the risks of further currency depreciation and worsening fiscal accounts lead us to downgrade their allocation to underweight relative to the EM benchmark. Further, foreigners own 25% of local bonds, so the risk of capital flight can further weigh on domestic bond and currency performance. Rising short-term interest rates and an imminent growth slump in 2023 favor further yield curve inversion. Therefore, we continue to recommend our yield curve flattening trade (Chart 7 above). Concerning sovereign credit, we are also downgrading our allocation to underweight within an EM credit portfolio. While sovereign spreads are the highest in LATAM, expansive fiscal policy and a mushrooming public debt-to-GDP ratio will weigh on their performance. Juan Egaña Associate Editor juane@bcaresearch.com Footnotes 1 Under Colombian law, the departing government must submit the fiscal budget for the first year of the newly elected government. This budget is then debated and revised in Congress.