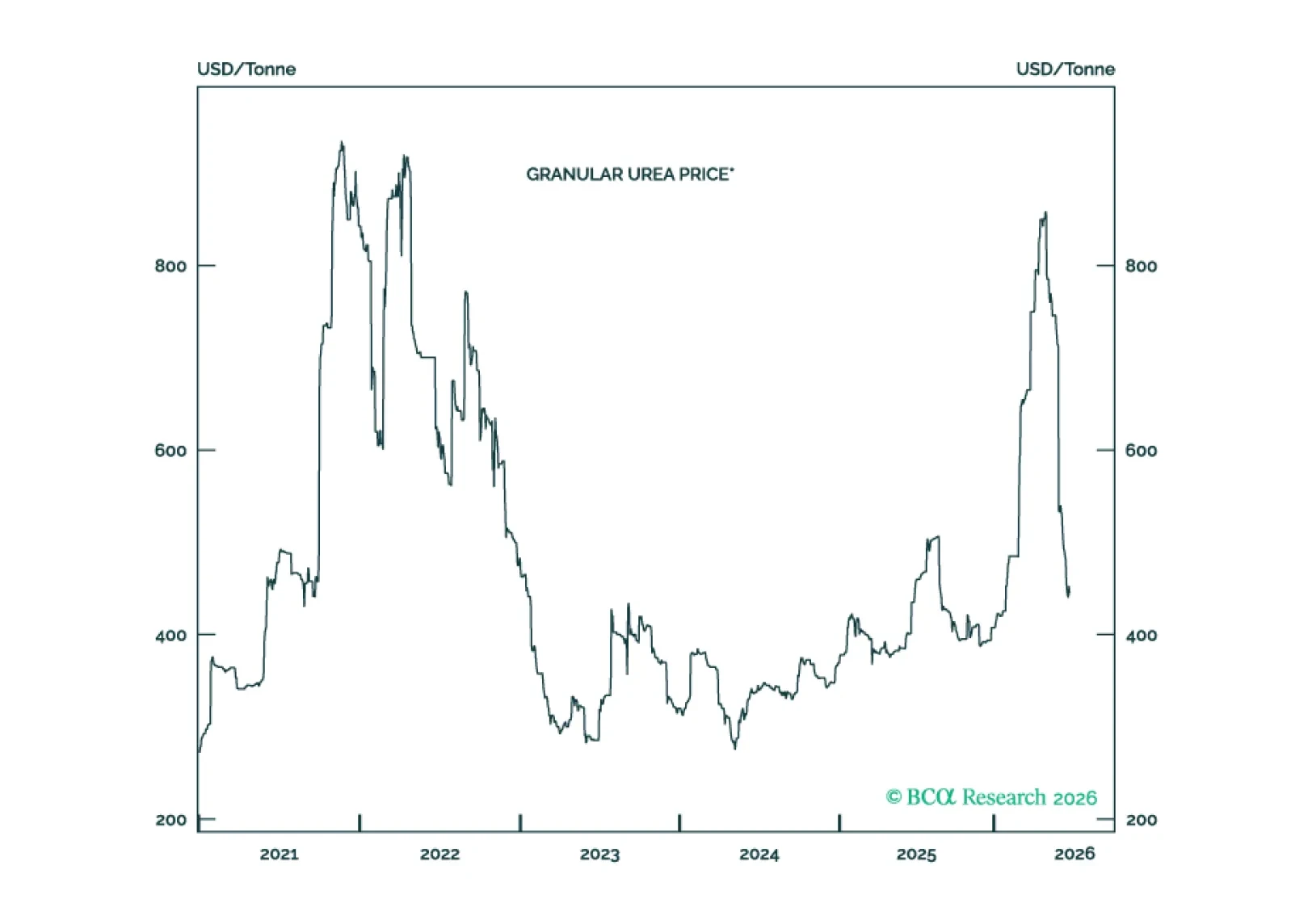

Commodities

Goldilocks, with fault lines underneath. Our first joint FICC outlook lays out where growth, inflation, and policy are headed this quarter and where the calm could crack.

The equity bull market is getting long in the tooth. Bonds should perform well once economic growth begins to slow. The dollar will strengthen over the coming months before resuming its downtrend. While crude has likely found a near-term floor, we favor metals over energy in the long run.

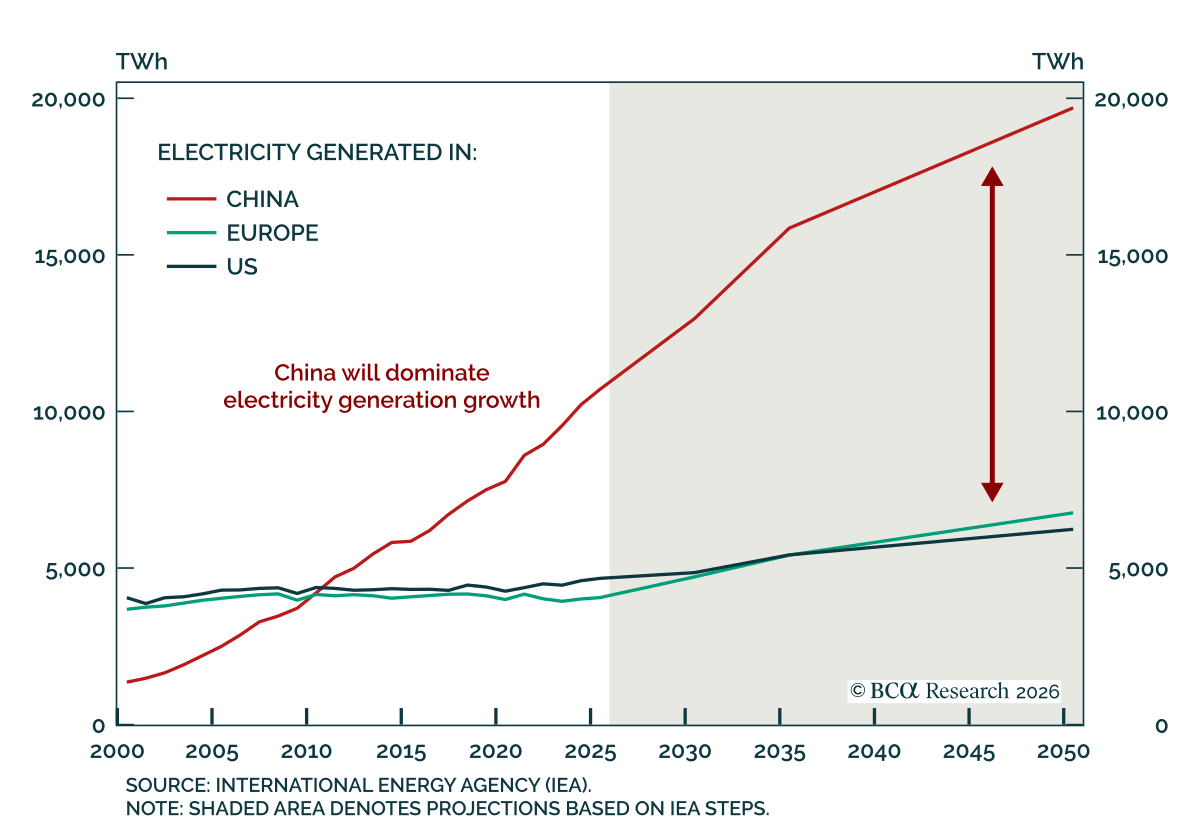

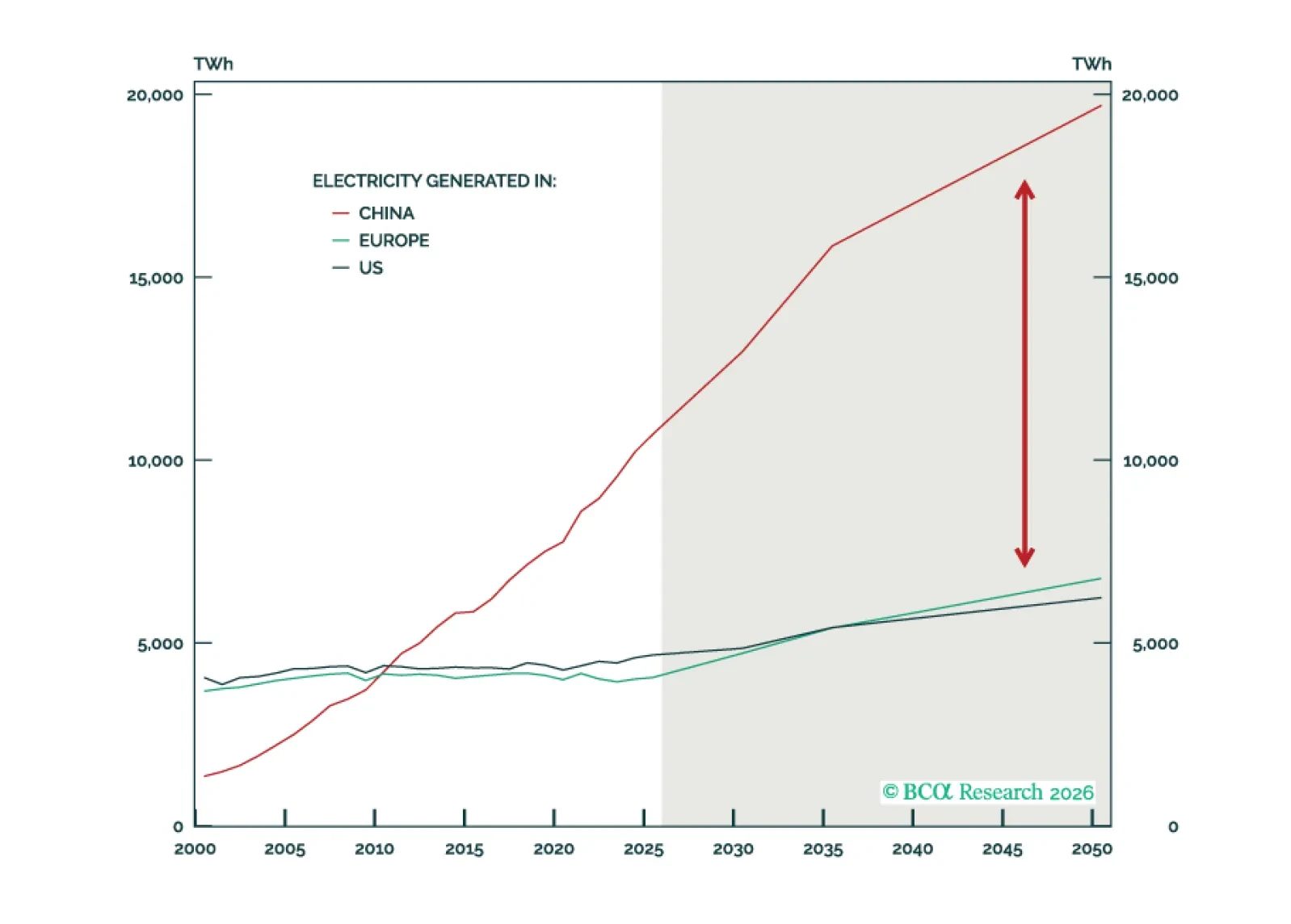

Section I maps how the broad distribution of wealth gains is supporting US consumption. Section II examines how countries can meet swelling electricity demand. The winners will find paths to build the infrastructure needed to power the high-tech future.

China holds a structural advantage in this "Age of Electricity" by operating the world's largest electricity system. However, this advantage has inherent limits, and the US remains competitive despite its challenges.

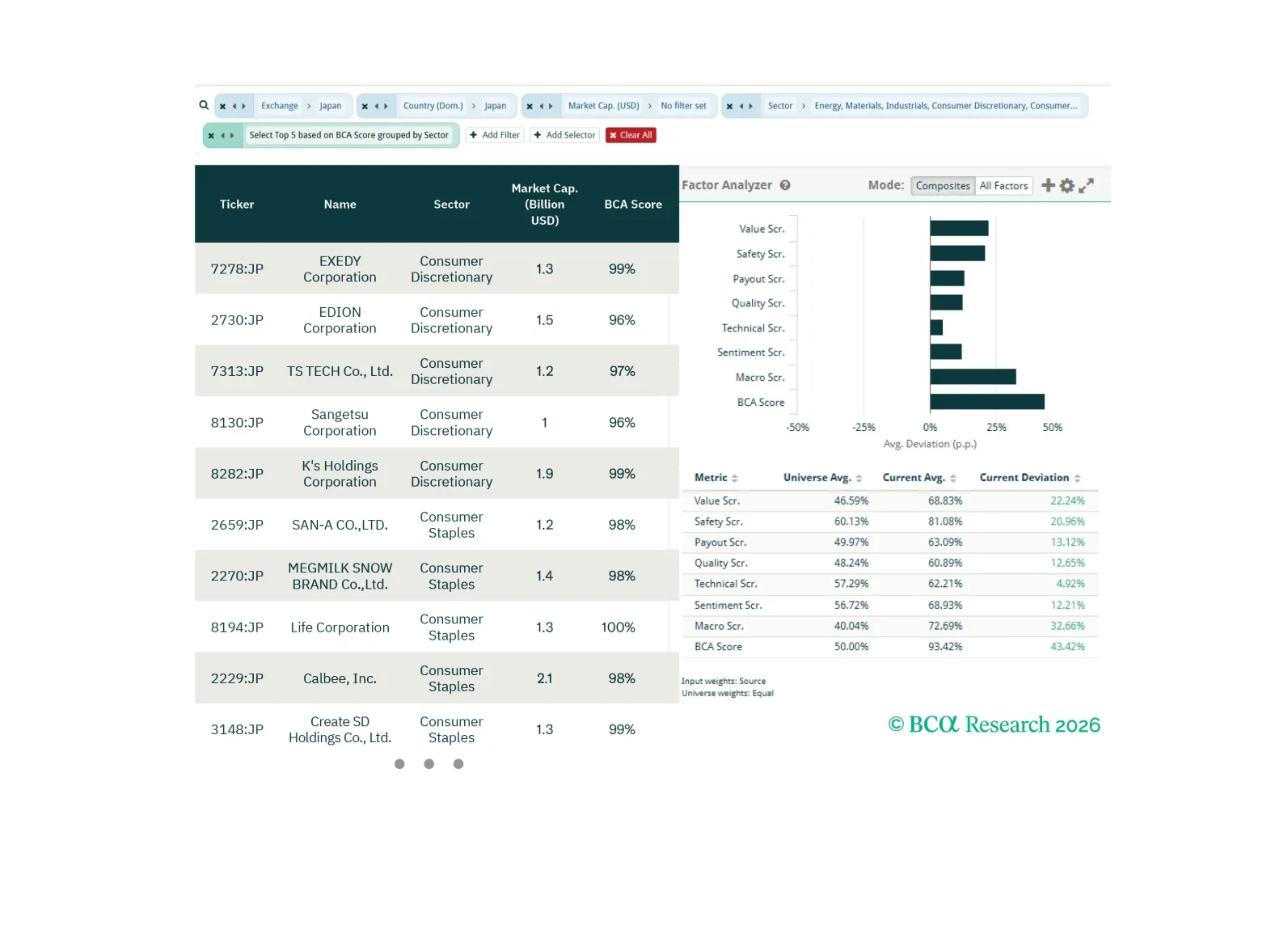

In this screener report, we explore opportunities in Japanese Non-TMT equities, El Niño hedges, and US consumer-facing equities.

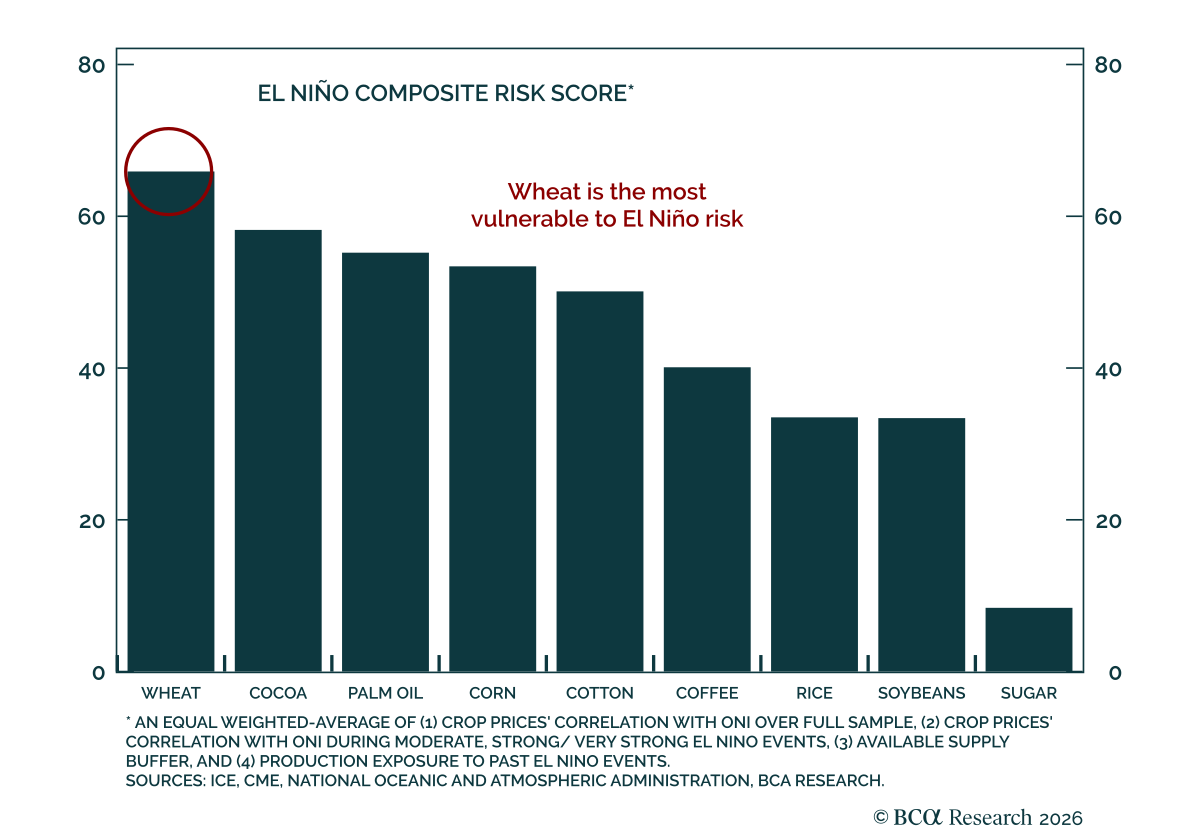

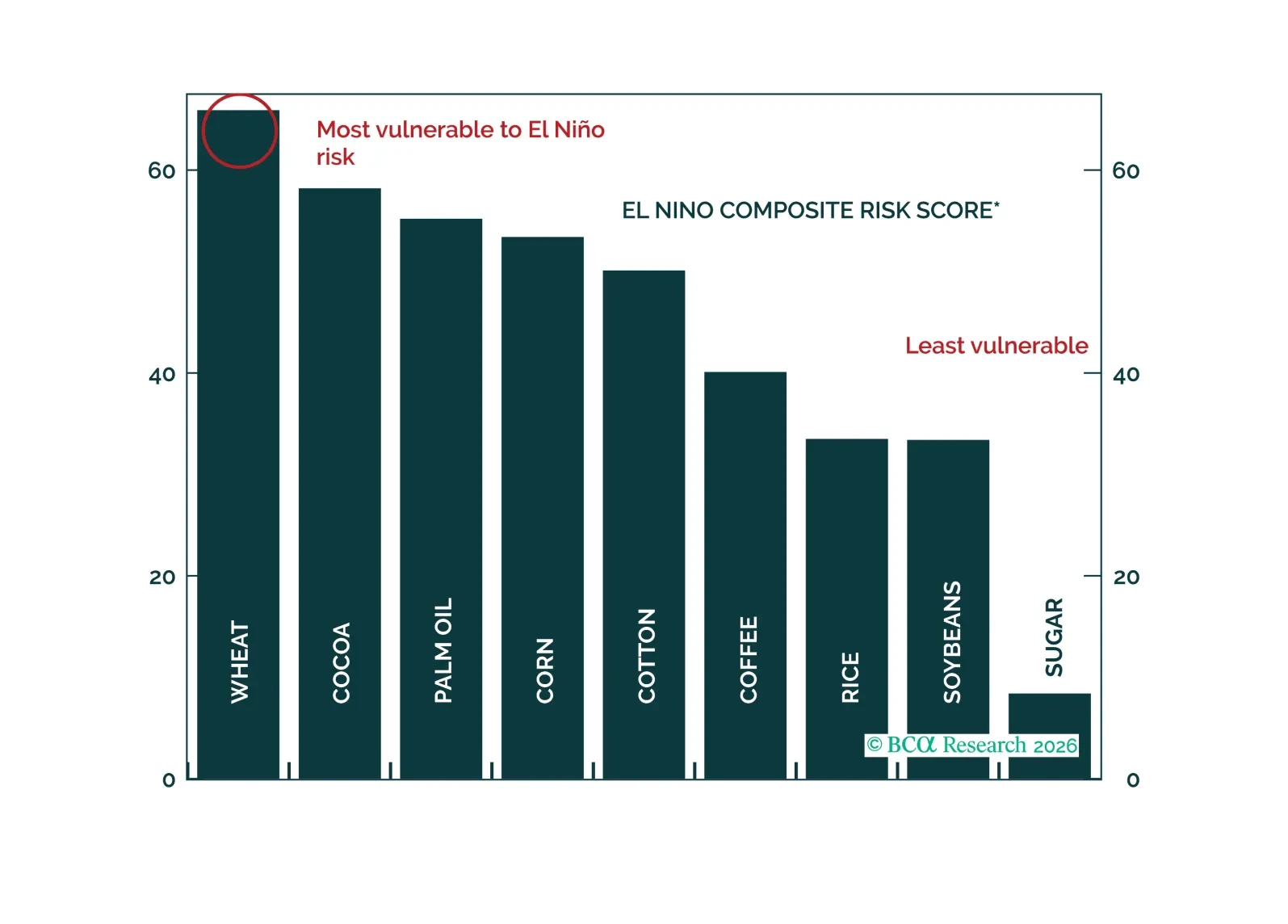

The risk of a “super El Niño” represents a meaningful threat to agricultural markets. Wheat, cocoa, and palm oil appear particularly vulnerable to El Niño-related supply disruptions.

A rise in food prices could also generate political — and potentially geopolitical — reverberations across frontier and emerging markets, where food prices are far more relevant than in developed economies.