Commodities & Energy Sector

MacroQuant sees the risks to US growth as being to the downside and the risks to inflation as being to the upside. Such a stagflationary brew justifies an underweight on stocks.

MacroQuant sees the risks to US growth as being to the downside and the risks to inflation as being to the upside. Such a stagflationary brew justifies an underweight on stocks.

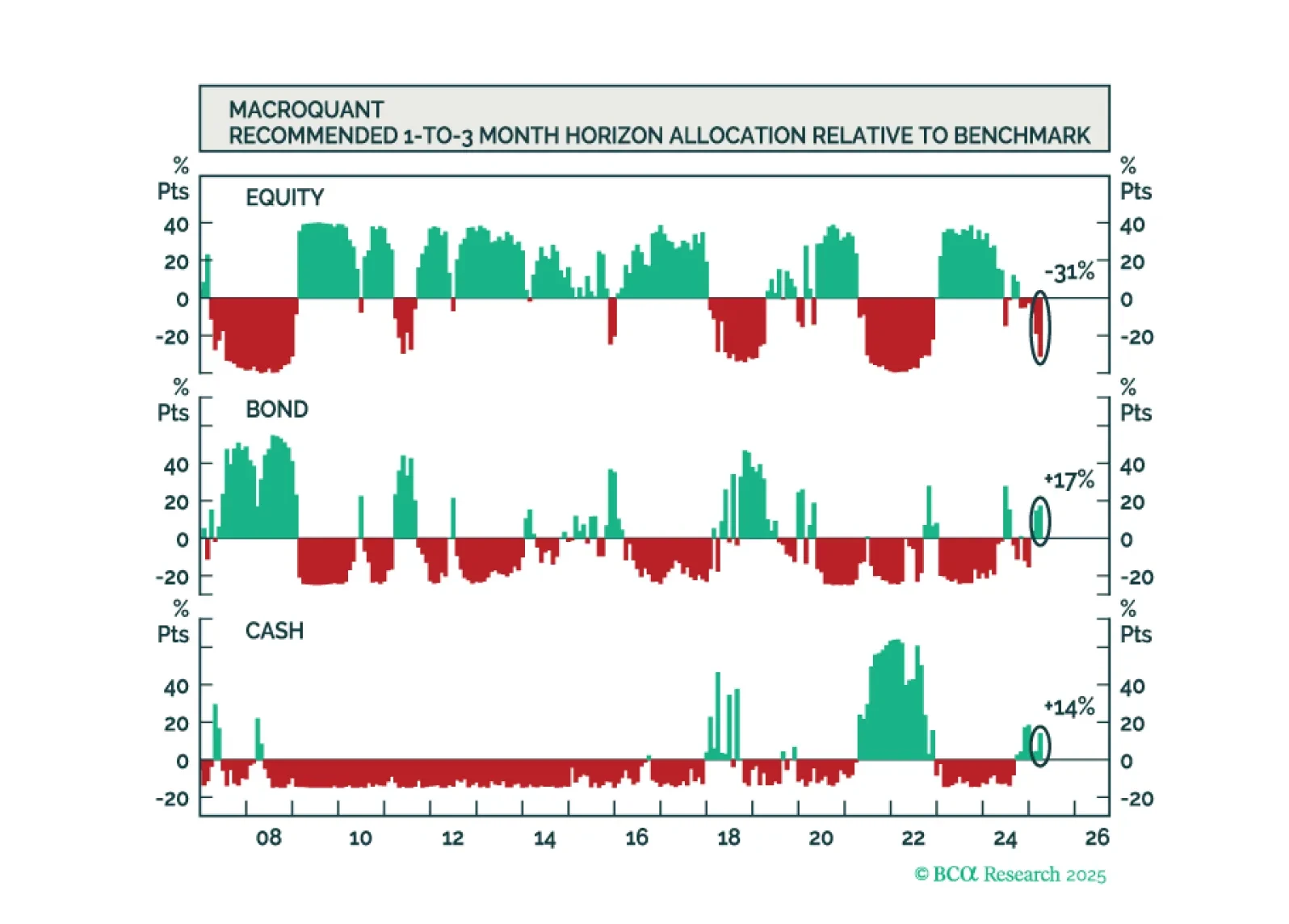

Going into April, MacroQuant recommends a modest underweight on stocks, offset by an overweight on bonds and cash. While MacroQuant is modestly bearish on stocks, we suspect that the downside risks to equities may be greater than what the model assumes.

Going into April, MacroQuant recommends a modest underweight on stocks, offset by an overweight on bonds and cash. While MacroQuant is modestly bearish on stocks, we suspect that the downside risks to equities may be greater than what the model assumes.

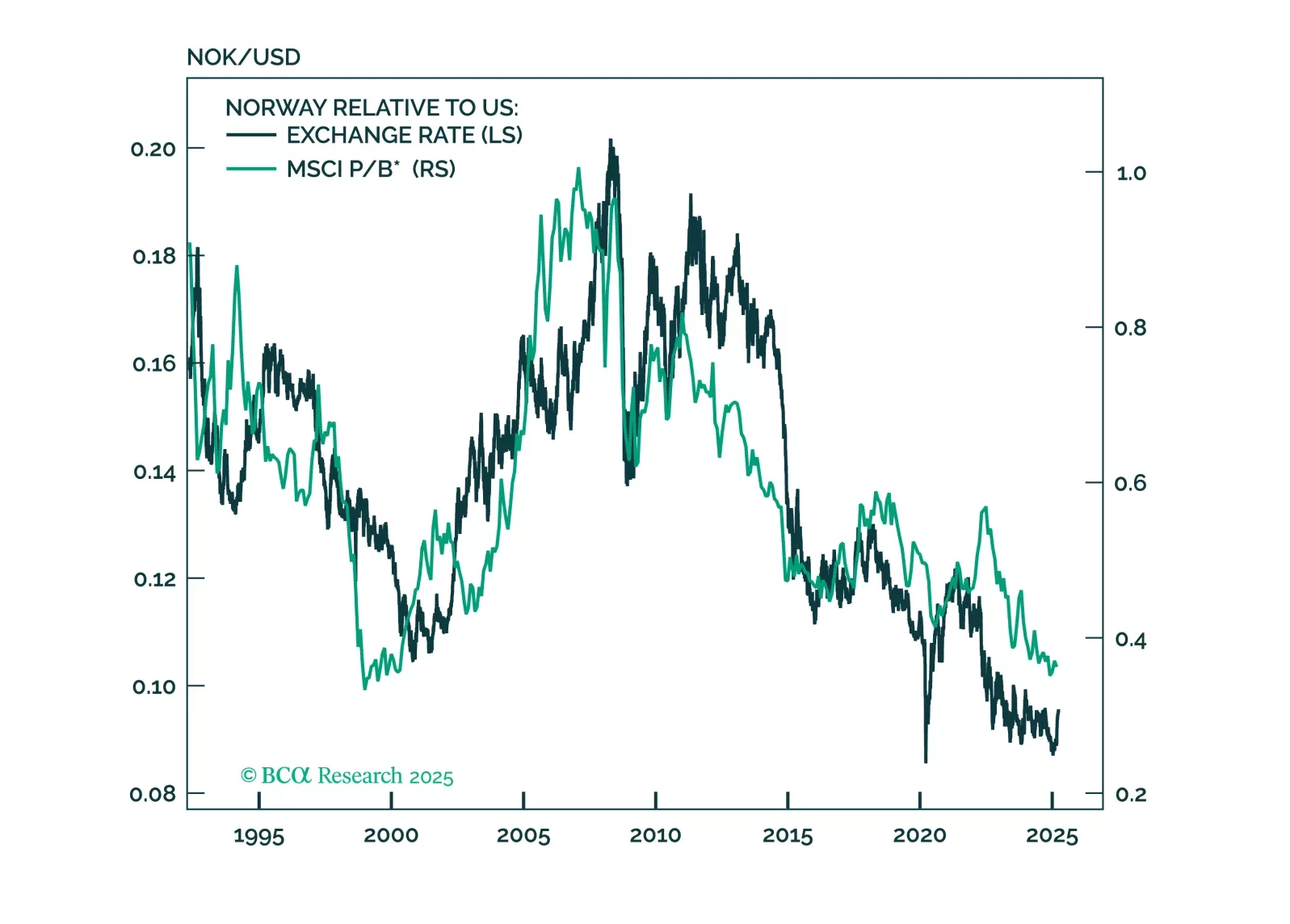

This report looks at investment implications, for Norwegian assets, given the recent meeting, from the Norges Bank.

In this Second Quarter Strategy Outlook, we explore the major trends that are set to drive financial markets for the rest of 2025 and beyond.

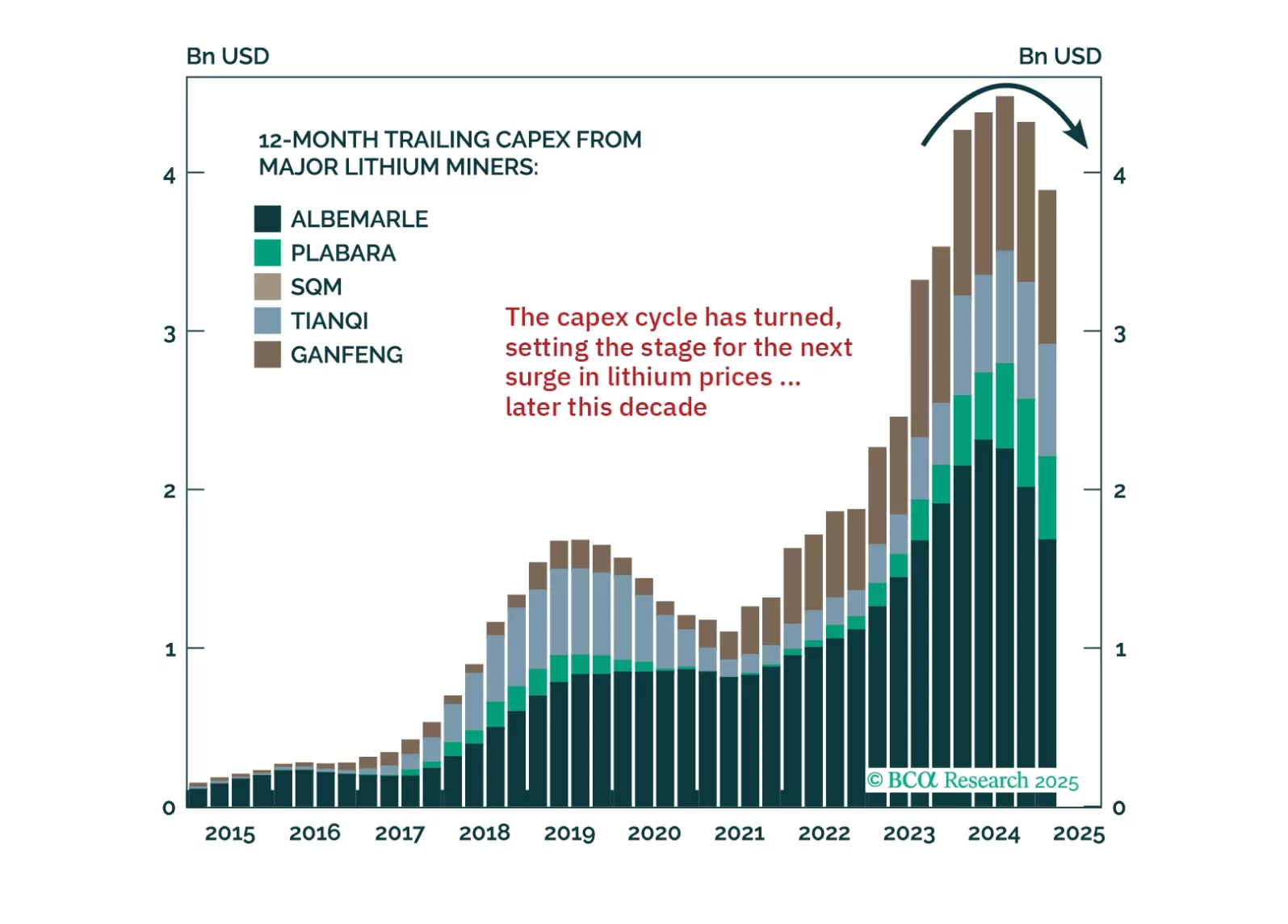

Lithium prices have collapsed by nearly 90% from the late-2022 peak.

How will lithium markets evolve from here?

In this report, we explore the cyclical and structural outlook for supply, demand, and prices.

We conclude that prices are likely to remain contained over the coming 12 to 18 months before facing upside pressure later this decade.