Commodities & Energy Sector

Supply-side risks from the Ukraine conflict are causing extreme volatility in global commodity markets. Crude oil, natural gas, nickel, and wheat are among the commodities caught in the crosshairs of the conflict and have all experienced outsized price moves…

Executive Summary Euro Natgas Soars; LME Nickel Squeezed

Euro Natgas, Nickel Soar

Euro Natgas, Nickel Soar

Russian Energy Minister Alexander Novak's threat to halt shipmentsof natgas on Nord Stream 1 to Europe lifted European gas prices 25% overnight, and will reverberate for years. We make the odds of a cut-off of Russian natgas exports to the EU low but not extremely low. Russia’s war is about the status of Ukraine. Russia needs the EU markets, and the EU needs Russia's gas. However, if Russia follows through on Novak's threat, it would be a major disruption for gas markets in the short term. Over the medium to long term, US shale gas producers, LNG terminal operators and exporters will benefit from new demand. On the import side, China likely benefits most from Russia's need to re-route gas. But this will require substantial infrastructure investment to monetize Russia's gas supplies and as such will take years to realize. Separately, the LME has shut down its nickel markets following an explosive 250% rally over two days that took prices above $100,000/MT. Nickel settled at ~ $80,000/MT before the LME closed the market today for margin calls on shorts squeezed by the surge in prices to make margin calls. Bottom Line: We remain long commodity-index exposure (S&P GSCI and the COMT ETF), along with equity exposure to oil and gas producers via the XOP ETF. We also remain long the XME and PICK ETFs to retain exposure to base metals and bulks.

Executive Summary Will The War Stall The Expected Downturn In Inflation This Year?

Will The War Stall The Expected Downturn In Inflation This Year?

Will The War Stall The Expected Downturn In Inflation This Year?

The Russia/Ukraine conflict is impacting financial markets across numerous channels – uncertainty, risk aversion, growth expectations & inflation expectations – but all have a common link through soaring commodity prices, most notably for oil. For global bond investors, allocations to inflation-linked bonds are a necessary hedge to the war and the associated commodity shock, particularly with breakevens in most countries re-establishing the link to oil prices. We recommend investors maintain neutral allocations to inflation-linked bonds versus nominal government bonds across the developed world until there is greater clarity on future global oil production. Markets are discounting a peak in interest rates at the low end of the Bank of Canada’s neutral range, which is reasonable given high household debt levels in Canada. This creates an opportunity for bond investors to go long Canadian government bonds versus US Treasuries. Bottom Line: The supply premium on global oil prices will persist until there are signs of more global oil production or less chaos in the Ukraine – neither of which is imminent. Maintain neutral allocations to inflation-linked bonds versus nominal government debt across the developed markets. Feature Chart 1A Broad-Based Surge In Commodity Prices

A Broad-Based Surge In Commodity Prices

A Broad-Based Surge In Commodity Prices

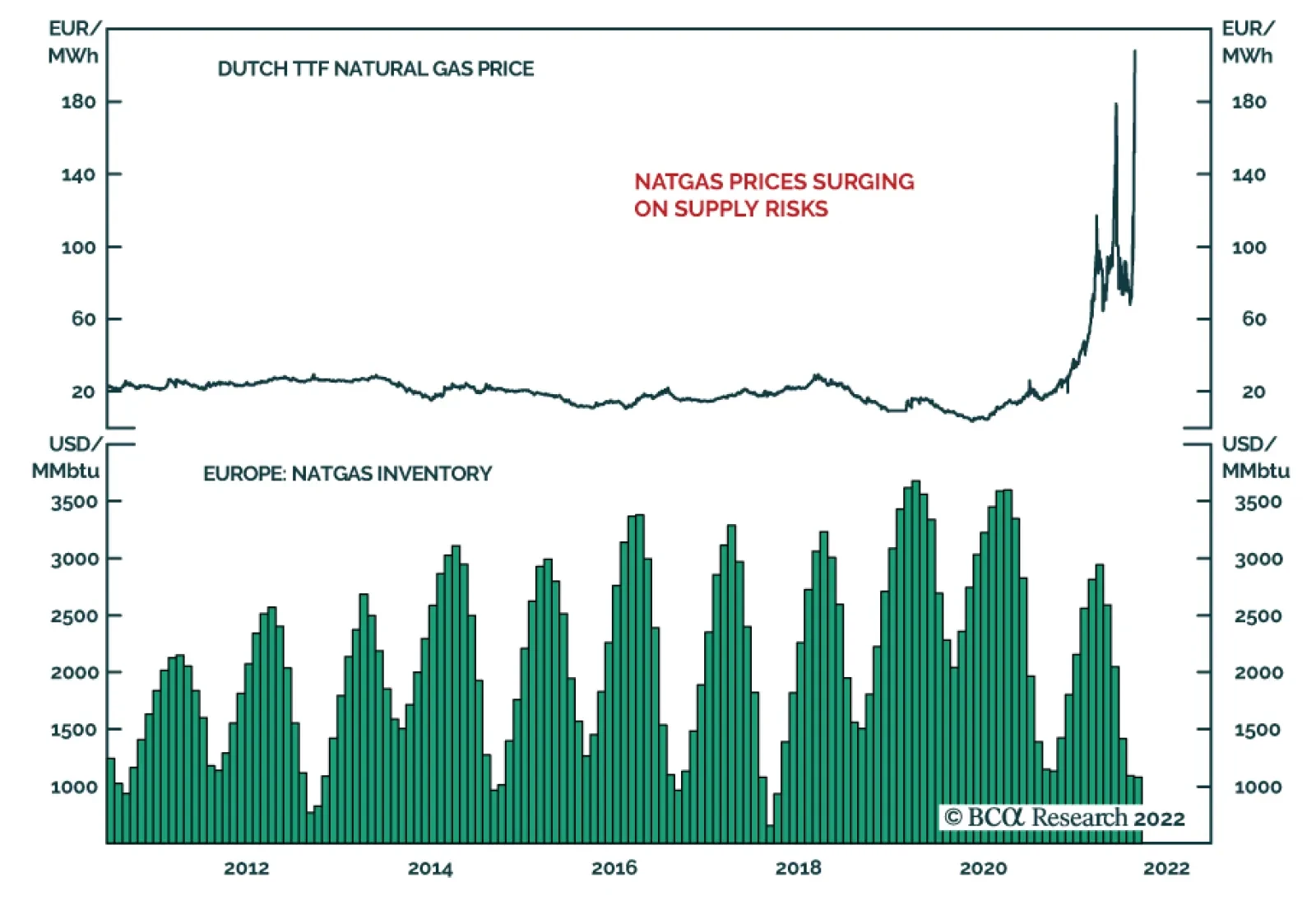

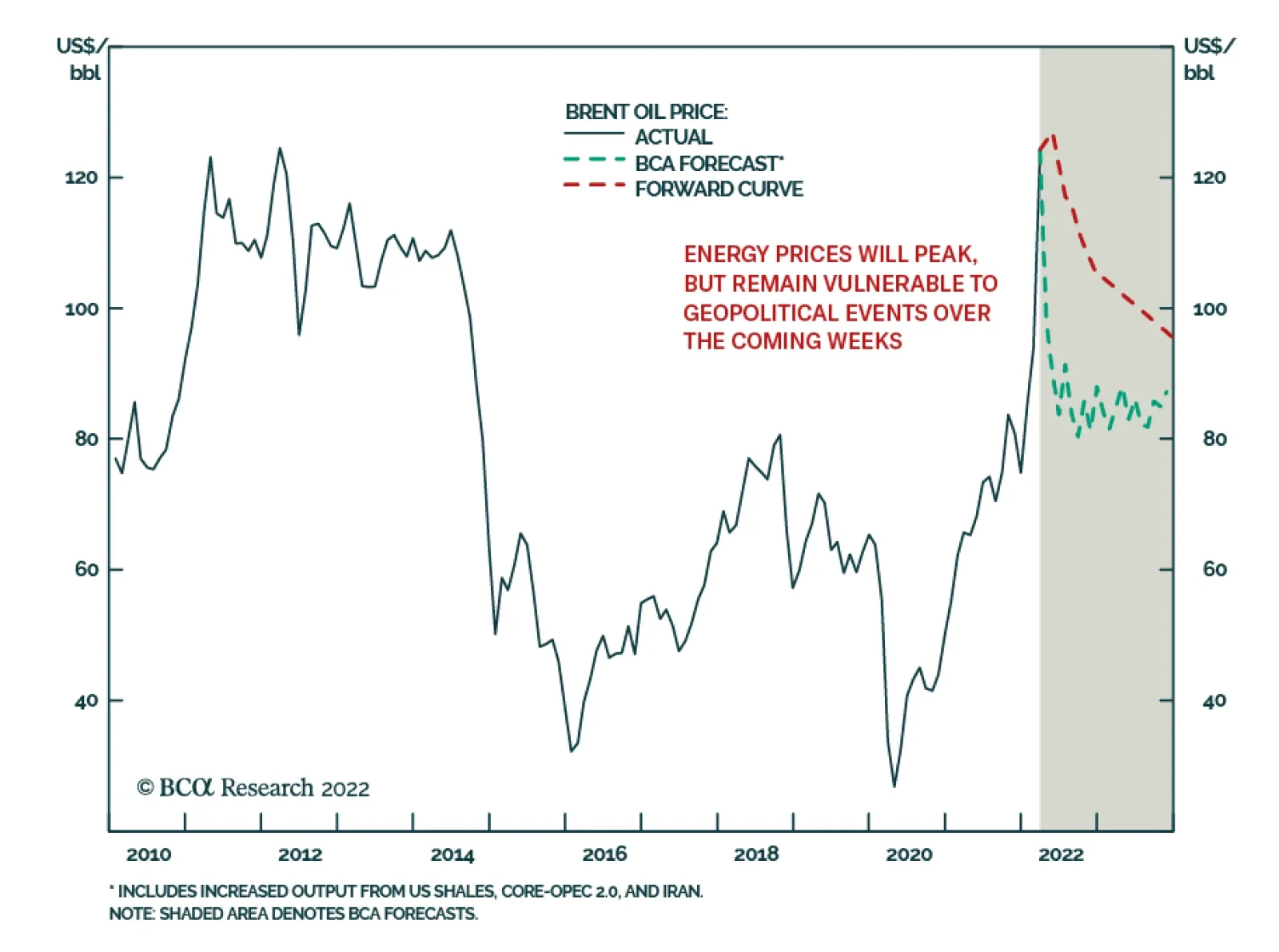

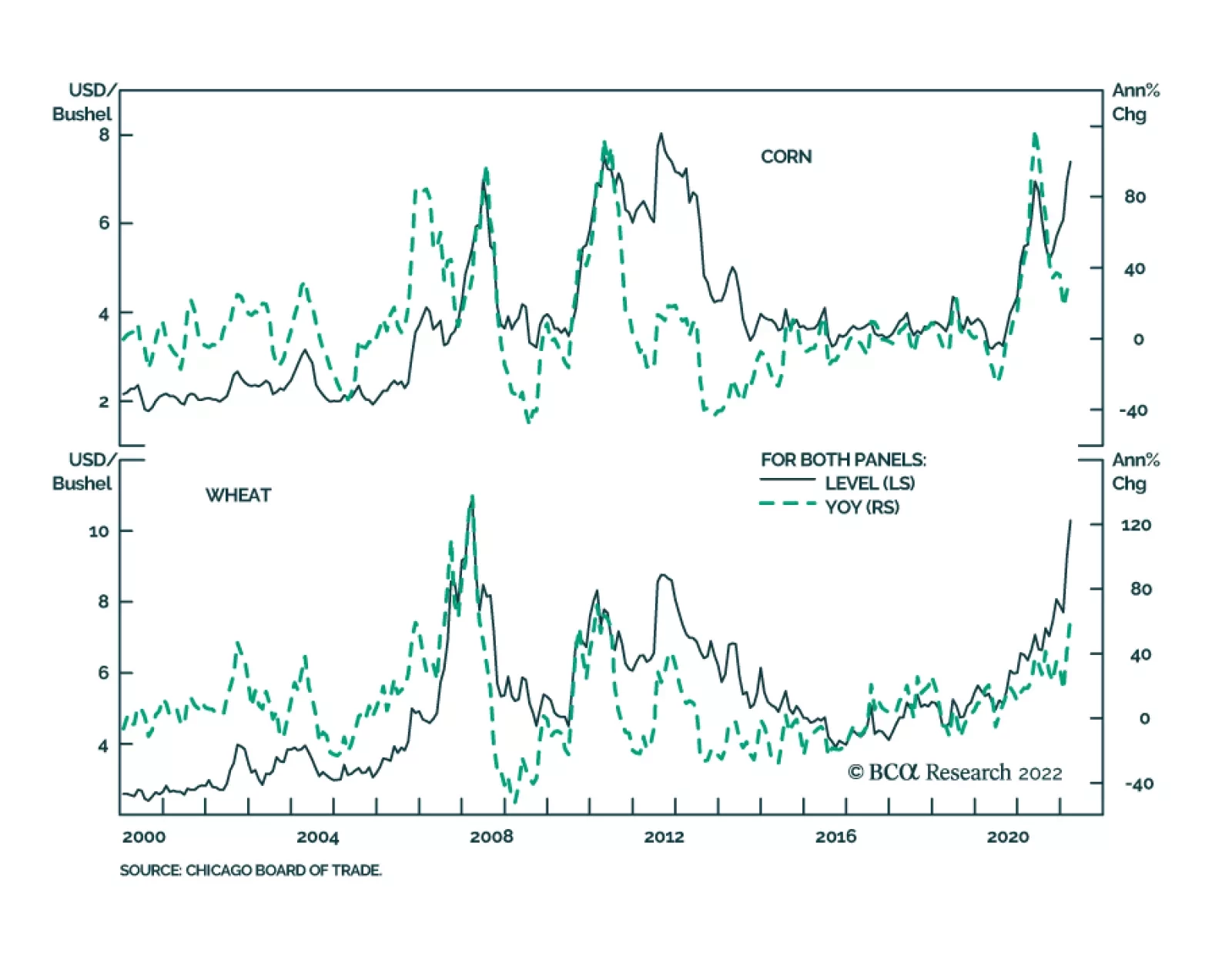

The Russia/Ukraine war has sent an inflationary shock though the world through a very traditional source – rising commodity prices. Energy prices are getting most of the attention, with oil prices back to levels last seen in 2008 and US gasoline prices now above $4 per gallon. The commodity rally is not just in energy, though. Industrial metals prices have also gone up substantially, with the spot prices for copper and aluminum hitting an all-time-high and 16-year-high, respectively (Chart 1). Agricultural commodities have seen even larger increases, with the price of wheat up 22% and the price of corn up 11% since the Russian invasion began on February 24th. Europe is acutely exposed to the war-driven spike in energy prices given its reliance on Russia for natural gas supplies. Natural gas prices in Europe have spiked a staggering 117% since the invasion started, exacerbating a sharp demand/supply imbalance dating back to the reopening of Europe’s economy from COVID lockdowns one year ago (Chart 2). To date, booming energy prices have fueled a huge rise in headline inflation rates in the euro area – producer prices were up 31% on a year-over-year basis in January – but with little trickle down to core inflation which was only up 2.3% in January. High energy prices are not only a problem for global growth and inflation, but also for the future policy moves by central banks. Inflation rates boosted over the past year by commodity supply squeezes and supply chain disruptions were set to decline this year, but the Ukraine shock has thrown that into question. If the benchmark Brent oil price were to hit $150/bbl, this would end the decelerating trend for energy price inflation momentum, on a year-over-year basis, that has been in place since mid-2021 (Chart 3). That means a higher floor for the energy component of inflation indices, and thus overall headline inflation rates, throughout the major economies in the coming months. Chart 2Europe's Reliance On Russian Natural Gas Is A Big Problem

Europe's Reliance On Russian Natural Gas Is A Big Problem

Europe's Reliance On Russian Natural Gas Is A Big Problem

Chart 3Will The War Stall The Expected Downturn In Inflation This Year?

Will The War Stall The Expected Downturn In Inflation This Year?

Will The War Stall The Expected Downturn In Inflation This Year?

Chart 4The Oil Price Spike Makes Life More Difficult for CBs

The Oil Price Spike Makes Life More Difficult for CBs

The Oil Price Spike Makes Life More Difficult for CBs

How will bond markets respond to higher-than-expected inflation? Rate hike expectations have been highly correlated to the trend of headline inflation in the US, Europe, UK, Canada and Australia over the past year (Chart 4). Currently, overnight index swap (OIS) curves are still discounting between 5-6 rate hikes from the Fed, the Bank of England, the Bank of Canada and the Reserve Bank of Australia before the end of 2022. A single rate hike is still priced into the European OIS curve, even with the Ukraine shock. Global bond yields have been volatile, but surprisingly resilient despite the worries about war and commodity inflation. The 10-year Treasury yield has been trading in a range between 1.7% and 2% since the Russian offensive began, while the 10-year German Bund yield has hovered around 0%. Bond markets are pricing in a stagflation-type outcome of slowing growth and rising inflation, as multiple rate hikes are still discounted despite the geopolitical risks from the war. That reduces the value of using increased duration exposure to position for risk-off moves in a bond portfolio. At the same time, real bond yields are falling and breakeven rates are rising for global inflation-linked bonds – a part of the fixed income universe that looks to offer good protection against the uncertainties of war. Inflation-Linked Bonds – A Good Hedge Against War Risks Since the Russian invasion began, breakeven inflation rates on 10-year inflation-linked bonds have moved higher in the US (+13bps), Canada (+19bps), Australia (+15bps) and even Japan (+15bps). The moves have been even more significant on the European continent – 10-year breakevens have shot up in the UK (+23bps), Germany (+45bps), France (+31bps) and Italy (+36bps). Chart 5Inflation Breakevens Are Rising, Especially In Europe

Inflation Breakevens Are Rising, Especially In Europe

Inflation Breakevens Are Rising, Especially In Europe

The absolute levels of breakevens in Europe are high in the context of recent history (Chart 5). However, breakevens also look a bit stretched in other countries like the US. Our preferred metric to evaluate the upside potential for inflation-linked bonds is our Comprehensive Breakeven Indicators (CBI). The CBI for each country is comprised of three components: the deviation of 10-year breakevens from our model-implied fair value, the spread between 10-year breakevens and longer-term survey-based inflation expectations (the “inflation risk premium”) and the gap between actual inflation and the central bank inflation target. Those three components are all standardized and added together with equal weights to come up with the CBI. A higher CBI reading suggests less potential for inflation breakevens to widen, and vice versa. Currently, the CBIs for the eight countries in our Model Bond Portfolio universe are close to or above zero, suggesting more limited scope for breakevens to widen further (Chart 6). Only in Canada is the CBI below zero, and only slightly so as high realized Canadian inflation is offset by breakevens trading below both fair value and survey-based measures of inflation (Chart 7). Chart 6Global Inflation Breakeven Valuations Are Not That Cheap

A Crude Awakening For Bond Investors

A Crude Awakening For Bond Investors

In the US, the CBI is above zero mostly because of high realized US inflation. In Europe, the CBIs of the UK, Germany and Italy all are well above zero, while in France the CBI is close to zero. The UK has the highest CBI in our eight-country universe, with all three components contributing roughly equally (Chart 8). The Japanese CBI is also just above the zero line. Chart 7Some Mixed Signals On Inflation Breakeven Valuations

Some Mixed Signals On Inflation Breakeven Valuations

Some Mixed Signals On Inflation Breakeven Valuations

Chart 8European Breakevens Have Adjusted Sharply To The Energy Shock

European Breakevens Have Adjusted Sharply To The Energy Shock

European Breakevens Have Adjusted Sharply To The Energy Shock

We have been recommending a relative cautious allocation to global breakeven bonds in recent months. We saw the upside potential on breakevens as capped given the dearth of “cheap” signals on breakevens from our CBIs, especially with central banks moving towards monetary tightening in response to elevated inflation – moves intended to restore inflation-fighting credibility with bond markets. Yet the Ukraine commodity shock has boosted inflation breakevens even in countries with modest underlying (non-commodity) inflation like Japan and the euro area. We now see greater value in owning inflation-linked bonds in global bond portfolios as a hedge against the inflation risks stemming from the Ukraine and the worsening geopolitical tensions between the West and Russia. This is true even without the typical positive signal for breakevens from having CBIs below zero. We recommend that fixed income investors maintain a neutral allocation to inflation-linked bonds in dedicated government bond portfolios across the entire developed market “linker” universe. In our model bond portfolio, we had been allocating to linkers based off the signal from the CBIs, but in the current stagflationary war environment, we see country allocations as secondary to having neutral exposure to linkers in all countries. The new weightings to inflation-linked bonds are shown in the model bond portfolio tables on pages 12-14.1 Bottom Line: For global fixed income investors, allocations to inflation-linked bonds are a necessary hedge to the war and the associated commodity shock, particularly with breakevens in most countries re-establishing the link to oil prices. Canada Update: BoC Liftoff At Last The Bank of Canada (BoC) raised its policy interest rate by 25bps to 0.5% last week, commencing the start of the first rate hike cycle since 2018. The move was no surprise after BoC Governor Tiff Macklem signaled at the January monetary policy meeting that the start of a rate hiking cycle was imminent. The Canadian Overnight Index Swap (OIS) curve is discounting another 171bps of hikes in 2022, with a peak rate of 1.98% reached by March 2023 - near the low-end of the BoC’s range of neutral rate estimates between 1.75% and 2.75% (Chart 9). Chart 9Markets Discounting A Shallow BoC Rate Hiking Cycle, Even With High Inflation

Markets Discounting A Shallow BoC Rate Hiking Cycle, Even With High Inflation

Markets Discounting A Shallow BoC Rate Hiking Cycle, Even With High Inflation

The BoC noted that the Canadian economy was recovering faster than expected from the effects of the Omicron variant and the associated restrictions on activity, coming off a robust 6.7% annualized real GDP growth rate in Q4/2021. The BoC now estimates that economic slack created by the pandemic shock has been fully absorbed, with the unemployment rate at 6.5%. Canadian headline inflation reached a 32-year high of 5.1% in January (Chart 10) – a level that Governor Macklem bluntly called “too high” in a speech the day following the rate hike. The BoC’s CPI-trim measure that excludes the most volatile components is also at an elevated reading of 4%, suggesting that the higher inflation is broad based. The BoC sees persistent high inflation as a risk to the stability of medium-term inflation expectations, thus justifying tighter monetary policy. According the latest BoC Survey of Consumer Expectations, Canadians expect inflation to be 4.1% over the next two years and 3.5% over the next five years, both of which are above the BoC’s 1-3% inflation target band. So with a robust economy, tight labor market, inflation well above the BoC target and elevated consumer inflation expectations showing no signs of settling, why is the OIS curve discounting such a relatively low peak in the BoC policy rate? The answer lies with Canada’s housing bubble and the associated high household debt levels. In a recent Special Report, our colleagues at The Bank Credit Analyst estimated that the neutral rate in Canada was no higher than 1.75%- the previous peak in rates during the 2017-2018 tightening cycle. A big reason for that was the high level of Canadian household debt, which now sits at 180% of disposable income. This compares to the equivalent measure in the US of 124%, showing that unlike their southern neighbors, Canadian households had little appetite for deleveraging after the 2008 financial crisis (Chart 11). Chart 10Good Reasons For A More Aggressive BoC

Good Reasons For A More Aggressive BoC

Good Reasons For A More Aggressive BoC

Chart 11A Big Reason For A Less Aggressive BoC

A Big Reason For A Less Aggressive BoC

A Big Reason For A Less Aggressive BoC

Chart 12Position For Narrower Canada-US Bond Spreads

Position For Narrower Canada-US Bond Spreads

Position For Narrower Canada-US Bond Spreads

The Bank Credit Analyst report estimated that if the BoC hiked rates to 2.5% over the next two years – just below the high end of the BoC neutral range – the Canadian household debt service ratio would climb to a new high of 15.5% (bottom panel). This would greatly restrict Canadian consumer spending and likely trigger a sharp pullback in both housing demand and real estate prices. The conclusion: the neutral interest rate in Canada is likely closer to the peak seen during the previous 2018/19 hiking cycle around 1.75%. We have been recommending an underweight stance on Canadian government bonds in global fixed income portfolios dating back to the spring of 2021. However, with markets now discounting a peak in rates within plausible estimates of neutral, the window for additional underperformance of Canadian government bonds may be closing - but not equally versus all developed economies. We have found that a useful leading indicator of 10-year cross-country government bond yield spreads is the differential between our 24-month discounters. The discounters measure the cumulative amount of short-term interest rate increases over the next two years priced into OIS curves. Currently the “discounter gaps” are signaling room for Canadian spread widening versus the UK and Japan and, to a lesser extent, core Europe (Chart 12). However, the discounter gap is pointing to significant potential for narrowing of the Canada-US 10-year spread over the next year (top panel). This would occur even if the BoC follows the Fed with rate hikes in 2022, as the Fed is likely to deliver more increases in 2023/24 than the BoC. This week, we are introducing two new recommended positions to benefit from narrower Canada-US government bond spreads: We are reducing the size of our underweight position in our model bond portfolio in half, offset by a reduction in the allocation to US Treasuries (see the table on page 13). We are introducing a new trade in our Tactical Overlay, going long Canadian 10-year government bond futures versus selling 10-year US Treasury futures on a duration-matched basis (the specific details of the trade can be found in the table on page 15) We are maintaining our cyclical underweight recommendation on Canada, in a global bond portfolio context, given the potential for Canadian yield spreads to widen versus core Europe, Japan and the UK. That underweight recommendation will be more concentrated versus countries relative to the US. Bottom Line: Markets are discounting a peak in interest rates at the low end of the Bank of Canada’s neutral range, which is reasonable given high household debt levels in Canada. This creates an opportunity for bond investors to go long Canadian government bonds versus US Treasuries. Robert Robis, CFA Chief Fixed Income Strategist rrobis@bcaresearch.com Footnotes 1 The allocations to inflation-linked bonds shown in the model bond portfolio reflect both the recommended country weights and the recommended weighting of linkers versus nominal bonds within each country. For example, we are neutral US TIPS versus nominal bonds within the US Treasury component of the portfolio, but since we are also underweight the US as a country allocation, the TIPS allocation is below the custom benchmark index weight. GFIS Model Bond Portfolio Recommended Positioning Active Duration Contribution: GFIS Recommended Portfolio Vs. Custom Performance Benchmark

A Crude Awakening For Bond Investors

A Crude Awakening For Bond Investors

The GFIS Recommended Portfolio Vs. The Custom Benchmark Index Global Fixed Income - Strategic Recommendations* Cyclical Recommendations (6-18 Months)

A Crude Awakening For Bond Investors

A Crude Awakening For Bond Investors

Tactical Overlay Trades

The outsized moves in the price of Brent on Monday underscore the vulnerability of crude oil markets to extreme geopolitical uncertainty, especially amid tight supply-demand fundamentals. The price of a barrel of Brent hit an intraday high of nearly…

Executive Summary US Can Do Without Russia's Oil, EU, NATO … Not So Much

US Will Ban Russian Oil Imports

US Will Ban Russian Oil Imports

The US will ban Russian oil imports shortly. This is not as big a deal markets had feared over the weekend, when news of a possible ban of Russian oil and refined products into the US and Europe was telegraphed by US officials, powering prices to $140/bbl.1 The US imported a combined 400k b/d of Russian crude oil and refined products in December 2021, the EIA reports, which accounted for less than 5% of the 8.6mm b/d of imports. Europe is another story. Roughly 60% of Russia's 11.3mm b/d of crude oil and refined-products output goes to OECD Europe, according to the IEA. Russia considers Western sanctions to be on an equal footing with a declaration of war.2 President Putin has threatened a nuclear response if the West interferes with invasion of Ukraine, which could elicit a similar response from the West.3 US shale producers will be highly incentivized to increase output given high prices. Our view continues to include a production increase from core OPEC 2.0 – Saudi Arabia, UAE and Kuwait. We also anticipate a return of 1mm b/d from Iran, following a nuclear deal with the US. Bottom Line: We remain long commodity-index exposure (S&P GSCI and the COMT ETF), along with equity exposure to oil and gas producers via the XOP ETF. Footnotes 1 Please see Crude price jumps on talk of US oil ban as Russia steps up shelling of civilian areas, published by the Financial Times on March 6, 2022. 2 Please see Putin says Western sanctions are akin to declaration of war, published on March 5, 2022. 3 Please see How likely is the use of nuclear weapons by Russia?, published by Chatham House on March 1, 2022. The report notes, " If Russia were to attack Ukraine with nuclear weapons, NATO countries would most likely respond on the grounds that the impact of nuclear weapons crosses borders and affects the countries surrounding Ukraine. NATO could respond either by using conventional forces on Russian strategic assets, or respond in kind using nuclear weapons as it has several options available."

Executive Summary A Perfect Metals Storm

A Perfect Metals Storm

A Perfect Metals Storm

The bitter truth at the heart of the Ukraine conflict is that the constraints the US and Europe are willing to impose on Russia are not enough to deter it from completing its conquest of the eastern and coastal parts of the country and installing a puppet government in Kiev. The conflict will reduce the available supplies of oil and gas, base metals and grains. Increasing commodity costs will add to existing inflation pressures and threaten to aggravate slowing growth trends in Europe. However, we expect that the net effect in the US will be more inflationary than deflationary, as flush consumers are well positioned to withstand upward price pressure. BCA has turned tactically neutral on equities as it does not appear that stock markets have yet come to terms with the glum reality of the military campaign. We foresee increased near-term market turbulence as investors experience periodic episodes of panic in response to developments on the ground. We are making several moves to dial down the risk in our ETF portfolio for the time being. We plan to unwind the moves before too long to align the portfolio with our bullish 12-month view but are relieved to have adopted a more defensive position while financial markets digest the implications of the geopolitical shock. Bottom Line: Financial market moves seem to be lagging the course of events in Ukraine. We recommend that investors position more defensively until markets catch up. Feature Chart 1Extreme Volatility

Extreme Volatility

Extreme Volatility

Ukraine has dominated the news since Russia invaded it a week and a half ago. The fighting has already triggered huge single-day swings in global financial markets with Russian equities falling nearly 40% the day the invasion began and rising 26% the next day before failing to open all of last week (Chart 1, top panel), western European sovereign 10-year bond yields falling by over six standard deviations across the board last Tuesday before retracing much of the move the next day (Chart 1, second panel) and Brent crude moving more than three standard deviations on several days (Chart 1, third panel). The S&P 500’s reversal from losing 3.5% in overnight futures markets to closing up 3% during the New York session on the day of the invasion is modest by comparison, as is the 10-year Treasury yield’s 2-3-standard deviation moves (Chart 1, bottom panel), though they show that the US is not immune. The inevitability that US markets and the US economy will be affected by events seven time zones away has led us to devote this week’s report to Ukraine and its potential consequences. This report is not meant to be the definitive guide to the conflict. It simply synthesizes the views expressed within BCA under the leadership of our Geopolitical Strategy team and adds our own thoughts about market implications and how investors in US markets might prepare to manage their way through the crisis. What’s The Endgame? BCA does not expect Russia to halt its offensive until Kiev is captured and Ukraine’s government is toppled. We therefore view any rallies on hopes for a negotiated settlement to be premature and vulnerable to subsequent reversals. Despite their stirring courage, resolve and pluck, the Ukrainians are massively outgunned and the ultimate military outcome is not in doubt. The cities that are under siege will fall unless Russian forces relent. No one within BCA imagines that Russia will relent until it achieves its aim of establishing a buffer between NATO forces and its own territory. It appears as if the only logical option for Russia’s Vladimir Putin is to proceed until Kiev has fallen. Now that he has already triggered nearly all the economic retaliation that the US and a surprisingly united Europe is likely to muster, there is very little reason not to complete his objective. As dispiriting as it is for humankind, conditions on the ground are likely to get worse. BCA’s base-case scenario is that the military campaign will continue until the coast and all the major cities east of the Dnieper River have succumbed (Map 1). At that point, we expect that the de facto political outcome will leave Russia in control of the eastern half of the country and its southern coast while the remnants of Ukraine’s democratically elected officials establish a new federal government in the country’s west. Once the political borders are redrawn, the active conquest can end. Russia will remain a pariah state, and heated rhetoric between Washington and Moscow and various European capitals and Moscow will wax and wane, but no party will have an incentive to disturb the fragile and uneasy equilibrium. Map 1Tightening The Noose

Ukraine’s Grim Tidings

Ukraine’s Grim Tidings

We are saddened by the Ukrainian peoples’ grim plight. We are dismayed by the way that events have laid bare multilateral institutions’ weaknesses. We lament the clinical tone with which we are discussing events that involve extreme human suffering. As we’ve said before, albeit in more comfortable contexts, our job is bullish or bearish, not good or bad and not right or wrong. The coldly objective bottom line is that the US and Europe are unwilling to interpose their own troops or risk escalating tensions with the possessor of the world’s second largest nuclear arsenal over the integrity of Ukraine’s borders. The constraints they are willing to impose on Russia’s actions are insufficient to preserve Kiev and the other cities within its crosshairs. Economic And Market Implications The most immediate economic consequence will be a reduction in the supply of crude oil, natural gas, several base metals and wheat and corn. Russia is the world’s third-largest oil producer; second-largest natural gas producer; a major source of aluminum, copper and nickel; and Russia and Ukraine together account for one-seventh of global wheat and corn production. Banks and shipping companies are increasingly unwilling to finance and transport Russian exports and Ukraine’s ability to cultivate and ship crops will likely be limited by ground-level hazards and Russian control of its ports. Crop and metals prices will rise at least temporarily while alternatives to established trade flows are developed and energy prices could spike if either side cuts off flows between Russia and Europe. Increased energy prices are properly viewed as a tax on economic activity for oil importing economies and the 1973-74 Arab oil embargo’s contribution to the November 1973 to March 1975 recession and the grinding 1973-74 equity bear market loom large in American minds. There are two key distinctions between then and now, however. First, the American economy is far less energy intensive than it was in the early seventies (Chart 2). Second, now that the US is the world’s largest oil producer, rising oil prices lead to increased employment (Chart 3), greater income and marginally better credit performance, given that the energy sector is the plurality issuer of high-yield bonds. Higher oil prices are no longer unadulteratedly negative for the US economy. Chart 3... And Higher Prices Now Mean More Jobs

... And Higher Prices Now Mean More Jobs

... And Higher Prices Now Mean More Jobs

Chart 2Oil Ain't What It Used To Be ...

Oil Ain't What It Used To Be ...

Oil Ain't What It Used To Be ...

There is a threat, however, that rising commodity prices could push up long-run inflation expectations, forcing the Fed to take a harder line on rate hikes than it otherwise might. Although the 10-year Treasury yield fell last week, inflation expectations rose (Chart 4). Fortunately, American households are unusually well positioned to confront higher inflation, thanks to their modest debt burden, enormous savings cushion and robust pandemic wealth gains powered by advances in financial markets and home prices. We therefore expect that events in Ukraine will prove to be more inflationary than deflationary in the US, though risk-off moves may make it look like the economy is slowing in a worrisome way in the near term. Chart 4Longer-Run Inflation Expectations Have Perked Up

Longer-Run Inflation Expectations Have Perked Up

Longer-Run Inflation Expectations Have Perked Up

From Investment Strategy … Though we are still constructive on financial markets and the economy, we expect that markets will be subject to downdrafts as investors come to terms with the likely course of events in Ukraine. Although our base-case scenario does not include an expansion of the conflict beyond Ukraine’s borders, financial markets will experience additional turbulence as they price in the non-zero probability that it might. Against that backdrop, we are tactically reducing risk in our ETF portfolio and recommend that investors follow suit. … To Portfolio Construction To reduce our near-term exposure to what our Global Investment Strategy colleagues describe as “panic events,” we are temporarily closing out our equity overweight. We are also reducing our cyclicals-over-defensives, value and small-cap positions as a further way of trimming the sails. We are directly investing in two sub-industry groups that will help protect the portfolio against lower interest rates and higher metals prices. To get our overall equity exposure down by 500 basis points (bps), we are reducing our four remaining equal weight sector exposures (Table 1). Table 1Tactical Equity Adjustments In The ETF Portfolio

Ukraine’s Grim Tidings

Ukraine’s Grim Tidings

To reduce our cyclicals-over-defensives exposure, we are closing out the respective 160- and 100-bps overweights in Industrials (XLI) and Financials (XLF) while reducing our Consumer Staples (XLP) underweight by 230 bps. Those moves have the effect of reducing our net equity exposure by 30 bps. We are dialing back our Value (RPV) overweight by 250 bps to defend against the potential drag on the Financials-heavy position from lower interest rates and a flatter yield curve. We are trimming our small-cap exposure (IJR) by 100 bps. These moves free up 350 bps of capital. The potential for further war-inspired disruptions leads us to drill down from sectors to sub-industry groups to tailor exposure to homebuilders and miners of metals and alternative fuels. Consumer Discretionaries are rate-sensitive but homebuilders are hyper sensitive, as their customers typically finance 80 to 90% of their purchase price. Every penny of the group’s revenue is earned in the US, which is less exposed to Ukraine disruptions than Europe, Japan (which imports all of its oil and gas) and emerging markets (vulnerable to a rising dollar). Demand is robust (Chart 5), supply will remain limited and the group’s low P/E multiple stands out in a world with few cheap stocks. We are selling 100 bps of our overall sector exposure (XLY) to fund the targeted purchase of ITB, the ETF offering the purest play on homebuilders. We follow the same targeted-exposure playbook in zeroing out our overall Materials position (XLB) to initiate a 150-bps position in XME, a pure-play metals and mining ETF which our Commodity and Energy Strategy team recommends to profit from tight base metals markets (Chart 6). As a tactical move, we are effectively swapping exposure to chemicals, which use natural gas as a feedstock, for base metals, precious metals and coal and uranium. XLB is vulnerable to higher natural gas prices while XME would benefit from them, as well as from base metals supply interruptions and flight-to-safety demand for gold and silver. Given our commodity colleagues’ expectation that alternative energy ambitions will keep base metals well bid for an extended period, XME may remain in the portfolio after markets fully digest Ukraine implications. Chart 5The Homebuilding Outlook ##br##Is Bright

The Homebuilding Outlook Is Bright

The Homebuilding Outlook Is Bright

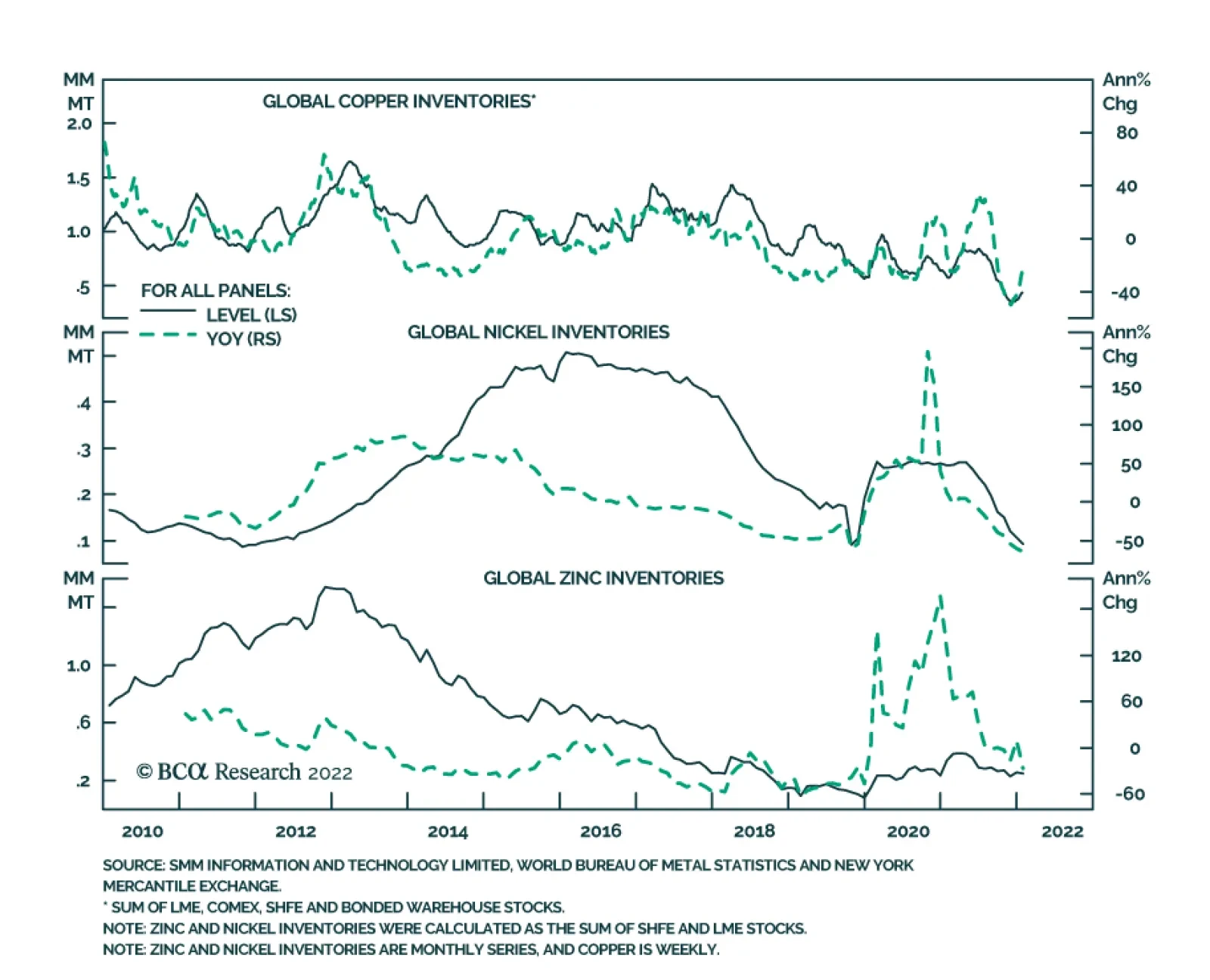

Chart 6Metals Inventories Were Tight Before Russian Resources Went Offline

Metals Inventories Were Tight Before Russian Resources Went Offline

Metals Inventories Were Tight Before Russian Resources Went Offline

The foregoing equity moves reduce our net holdings by 380 bps; we trim each of our four remaining equal weight positions – in Communication Services (XLC), Health Care (XLV), Real Estate (XLRE) and Tech (XLK) – by 30 bps to shed the remaining 120 bps needed to reset equities to equal weight to ride out temporary market turbulence. We also reduce our hybrid preferred stock position (VRP), as there’s less need for variable-rate protection if yields are going to decline and the preferred space may become more volatile as retail investors react to unsettling headlines. The 250-bps hybrid drawdown will be allocated to traditional fixed income, along with 250 bps of the equity sales proceeds, to bulk up our Treasury positions (SHY, IEI and IEF) in the proportion required to maintain benchmark duration (Appendix Table, shown at the back of the report). The remaining 250 bps raised by equity sales will be parked in cash to await an opportunity to re-risk the portfolio in line with our bullish cyclical view. Our relative equity sector positioning as of today is shown in Chart 7 and our relative fixed income positioning is shown in Chart 8. Chart 7Narrowing Our Sector Tilts

Ukraine’s Grim Tidings

Ukraine’s Grim Tidings

Chart 8Shrinking Our Treasury Underweight

Ukraine’s Grim Tidings

Ukraine’s Grim Tidings

Doug Peta, CFA Chief US Investment Strategist dougp@bcaresearch.com Cyclical ETF Portfolio

Ukraine’s Grim Tidings

Ukraine’s Grim Tidings

Executive Summary Nuclear Worries Take Center Stage

Rising Risk Of A Nuclear Apocalypse

Rising Risk Of A Nuclear Apocalypse

Vladimir Putin has now committed himself to orchestrating a regime change in Kyiv. Anything less would be seen as a defeat for him. Assuming he succeeds, and it is far from obvious that he will, the resulting insurgency will drain Russian resources. Along with continued sanctions, this will lead to a further deterioration in Russian living standards and growing domestic discontent. If Putin concludes that he has no future, the risk is that he will decide that no one else should have a future either. Although there is a huge margin of error around any estimate, subjectively, we would assign an uncomfortably high 10% chance of a civilization-ending global nuclear war over the next 12 months. These odds place some credence on Brandon Carter’s highly controversial Doomsday Argument. Even if World War III is ultimately averted, markets could experience a freak-out moment over the next few weeks, similar to what happened at the outset of the pandemic. Google searches for nuclear war are already spiking. Despite the risk of nuclear war, it makes sense to stay constructive on stocks over the next 12 months. If an ICBM is heading your way, the size and composition of your portfolio becomes irrelevant. Thus, from a purely financial perspective, you should largely ignore existential risk, even if you do care about it greatly from a personal perspective. Bottom Line: The risk of Armageddon has risen dramatically. Stay bullish on stocks over a 12-month horizon. All In on Sanctions In the criminal justice system, there is a reason why the punishment for armed robbery is lower than for murder. If the punishment were the same, an armed robber would have a perverse incentive to kill his victim in order to better conceal his crime. The same logic applies, or at least used to apply, to geopolitics: You do not impose maximum sanctions from the get-go because that removes your ability to influence your enemy with the threat of further sanctions. Following Russia’s invasion of Ukraine, the West chose to go all in on sanctions, levying every type imaginable with the exception of those entailing a big cost to the West (such as cutting off Russian energy exports). Most notably, many Russian banks have been blocked from the SWIFT messaging system while the Russian central bank’s foreign exchange reserves have been frozen. Even FIFA has barred Russia from international competition, just weeks before it was set to participate in the qualifying rounds of the 2022 World Cup. At this point, there is not much more that can be done on the sanctions front. This leaves military intervention as the only avenue available to further pressure Russia. A growing chorus of Western pundits, some of whom could not have picked out Ukraine on a map two weeks ago, have begun clamoring for regime change… this time, in Moscow. As one might imagine, this is not something that sits well with Putin. Last week, he declared that “No matter who tries to stand in our way or … create threats for our country and our people, they must know that Russia will respond immediately, and the consequences will be such as you have never seen in your entire history.” To ensure there was no uncertainty about what he was talking about, he proceeded to place Russia’s nuclear forces on “special regime of combat duty.” Yes, It’s Possible The Putin regime has used nuclear weapons of a sort in the past. The FSB likely orchestrated the poisoning of Alexander Litvinenko with polonium-210 in 2006, leaving traces of the radioactive substance scattered in dozens of places across London. As former US presidential advisor and Putin biographer Fiona Hill said in a recent interview with Politico, “Every time you think, “No, he wouldn’t, would he?” Well, yes, he would.” Admittedly, there is a big difference between dropping polonium into a cup of tea at the Millennium hotel in Mayfair and dropping a 10-megaton nuclear bomb on London or any other major Western city. Still, if Putin feels that he has no future, he may try to take everyone down with him. The collapse in the ruble, and what is sure to be a major plunge of living standards across Russia, could foment internal opposition to Putin. A quiet retirement is not an option for him. Based on the latest exchange rates, Russia’s GDP is smaller than Mexico’s and barely higher than that of Illinois (Chart 1). While denying gas to Europe is a very real threat, it has a limited shelf life. Europe will aggressively build out infrastructure to process LNG imports. Chart 1Russia's Economic Power Has Faded

Rising Risk Of A Nuclear Apocalypse

Rising Risk Of A Nuclear Apocalypse

In a few years, the one viable weapon that Russia will have at its disposal is its nuclear arsenal. As Dutch historian Jolle Demmers has said, “It is precisely the decline and contraction of Russian power, coupled with the possession of nuclear weapons and a tormented repressive president, that poses great risks.” Some of the world’s most prominent strategic thinkers flagged these risks before the invasion, but with little effect. The Mother of All Risks In simulated war games, it is generally difficult to get participants to cross the nuclear threshold, but once they do, a full-blown nuclear exchange usually ensues.1 The idea of “limited” nuclear war is a mirage. How high are the odds of such a full-blown war? I must confess that my own feelings on the matter are heavily colored by my writings on existential risk. As I argued in Section XII of my special report, “Life, Death, and Finance in the Cosmic Multiverse,” we are probably greatly understating existential risk, especially when we look prospectively into the future. Although there is a huge margin of error around any estimate, subjectively, we would assign an uncomfortably high 10% chance of a civilization-ending global nuclear war over the next 12 months. These odds place some credence on Brandon Carter’s highly controversial Doomsday argument (See Box 1). A Paradox for Investors For investors, existential risk represents a paradoxical concept. If an ICBM is heading your way, the question of whether you are overweight or underweight stocks would be pretty far down on your list of priorities. And even if you were inclined to think about your portfolio, how would you alter it? In a full-blown global nuclear war, most stocks would go to zero while governments would probably be forced to default or inflate away their debt. Gold might retain some value – provided that you kept it in your physical possession – but even then, you would still have trouble exchanging it for anything of value if nothing of value were available to purchase. This means that from a purely financial perspective, you should largely ignore existential risk, even if you do care greatly about it from a personal perspective. What, then, can we say about the current market environment? I touched on many of the key issues in Monday’s Special Alert, in which we tactically downgraded global equities from overweight to neutral. I encourage readers to consult that report for our latest market views. In the remainder of today’s report, allow me to elaborate on a couple of key themes. A Freak-Out Moment Is Coming Chart 2Nuclear Worries Take Center Stage

Rising Risk Of A Nuclear Apocalypse

Rising Risk Of A Nuclear Apocalypse

The market today reminds me of early 2020. We wrote a report on February 21 of that year entitled “Markets Too Complacent About The Coronavirus,” in which we noted that a full-blown pandemic “could lead to 20 million deaths worldwide,” and that “This would likely trigger a global downturn as deep as the Great Recession of 2008/09, with the only consolation being that the recovery would be much more rapid than the one following the financial crisis.” Many saw that report as alarmist, just as they saw our subsequent decision to upgrade stocks in March as cavalier. Even if you knew in February 2020 that the S&P 500 would reach an all-time high later that year, you should have still shorted equities aggressively on a tactical basis. I feel the same way about the present. Google searches for nuclear war are spiking (Chart 2). A freak-out moment is coming, which will present a good buying opportunity for investors. Just to be on the safe side, I picked up a couple of bottles of Potassium Iodide earlier this week. When I checked the pharmacy again yesterday, all the bottles were sold out. They are now being hawked on Amazon for ten times the regular price. From Cold War to Hot Economy? The spike in commodity prices – especially energy prices – will have a negative near-term impact on global growth, while also limiting the ability of central banks to slow the pace of planned rate hikes (Chart 3). In general, inflation expectations and oil prices move together (Chart 4). Chart 3Central Banks: Caught Between A Rock And A Hard Place

Central Banks: Caught Between A Rock And A Hard Place

Central Banks: Caught Between A Rock And A Hard Place

Chart 4Inflation Expectations And Oil Prices Go Hand-In-Hand

Inflation Expectations And Oil Prices Go Hand-In-Hand

Inflation Expectations And Oil Prices Go Hand-In-Hand

Assuming the geopolitical situation stabilizes in a few months, oil prices should come down. The forward curve for oil is heavily backwardated now: The spot price for Brent is $111/bbl while the December 2022 price is $93/bbl (Chart 5). BCA’s commodity strategists expect the price of Brent oil to fall to $88/bbl by year-end. The decline in energy prices should provide some relief to global growth and risk assets in the back half of the year, which is one reason we are more constructive on equities over a 12-month horizon than a 3-month horizon. Looking out beyond the next year or two, the new cold war will lead to higher, not lower, interest rates. Increased spending on defense and alternative energy sources will prop up aggregate demand, especially in Europe where the need to diversify away from Russian gas is greatest. As Chart 6 shows, capex in the euro area cratered following the euro debt crisis. Capital spending via the Recovery Fund and other sources will rise significantly over the next few years. Chart 5The Brent Curve Is Heavily Backwardated

Rising Risk Of A Nuclear Apocalypse

Rising Risk Of A Nuclear Apocalypse

Chart 6European Capex Is Poised To Increase

European Capex Is Poised To Increase

European Capex Is Poised To Increase

In addition, the shift to a multipolar world will expedite the retreat from globalization. Rising globalization was an important force restraining inflation – and interest rates – over the past few decades. Lastly, the ever-present danger of war could prompt households to reduce savings. It does not make sense to save for a rainy day if that day never arrives. Lower savings implies a higher equilibrium rate of interest. As we discussed in our recent report entitled “A Two-Stage Fed Tightening Cycle,” after raising rates modesty this year, the Fed will resume hiking rates towards the end of 2023 or in 2024, as it becomes clear that the neutral rate in nominal terms is closer to 3%-to-4% rather than the 2% that the market assumes. The secular bull market in equities will likely end at that point. In summary, equity investors should be somewhat cautious over the next three months, more optimistic over a 12-month horizon, but more cautious again over a longer-term horizon of 2-to-5 years. Box 1The Doomsday Argument In A Nutshell

Rising Risk Of A Nuclear Apocalypse

Rising Risk Of A Nuclear Apocalypse

Peter Berezin Chief Global Strategist peterb@bcaresearch.com Footnotes 1 For example, an article from the Center for Arms Control and Non-Proliferation discusses a Reagan administration war game called “Proud Prophet,” an exercise the Americans hatched to test the theory of limited nuclear strikes. The result of this exercise was that the “Soviet Union perceived even a low-yield nuclear strike as an attack, and responded with a massive missile salvo.” Global Investment Strategy View Matrix

Rising Risk Of A Nuclear Apocalypse

Rising Risk Of A Nuclear Apocalypse

Special Trade Recommendations Current MacroQuant Model Scores

Rising Risk Of A Nuclear Apocalypse

Rising Risk Of A Nuclear Apocalypse

The Russia-Ukraine crisis is unfolding against the backdrop of extremely low base metals inventories, as the post-pandemic recovery coincided with global supply chain bottlenecks. Low inventories mean there is a smaller buffer to absorb price shocks caused by…

Russia’s attack on Ukraine threatens shipping in the Black Sea region, which is where much of Russia's and Ukraine's wheat and corn is exported. In addition, Russian attacks could disrupt the ability of Ukrainian farmers to plant and harvest crops in 2022. …

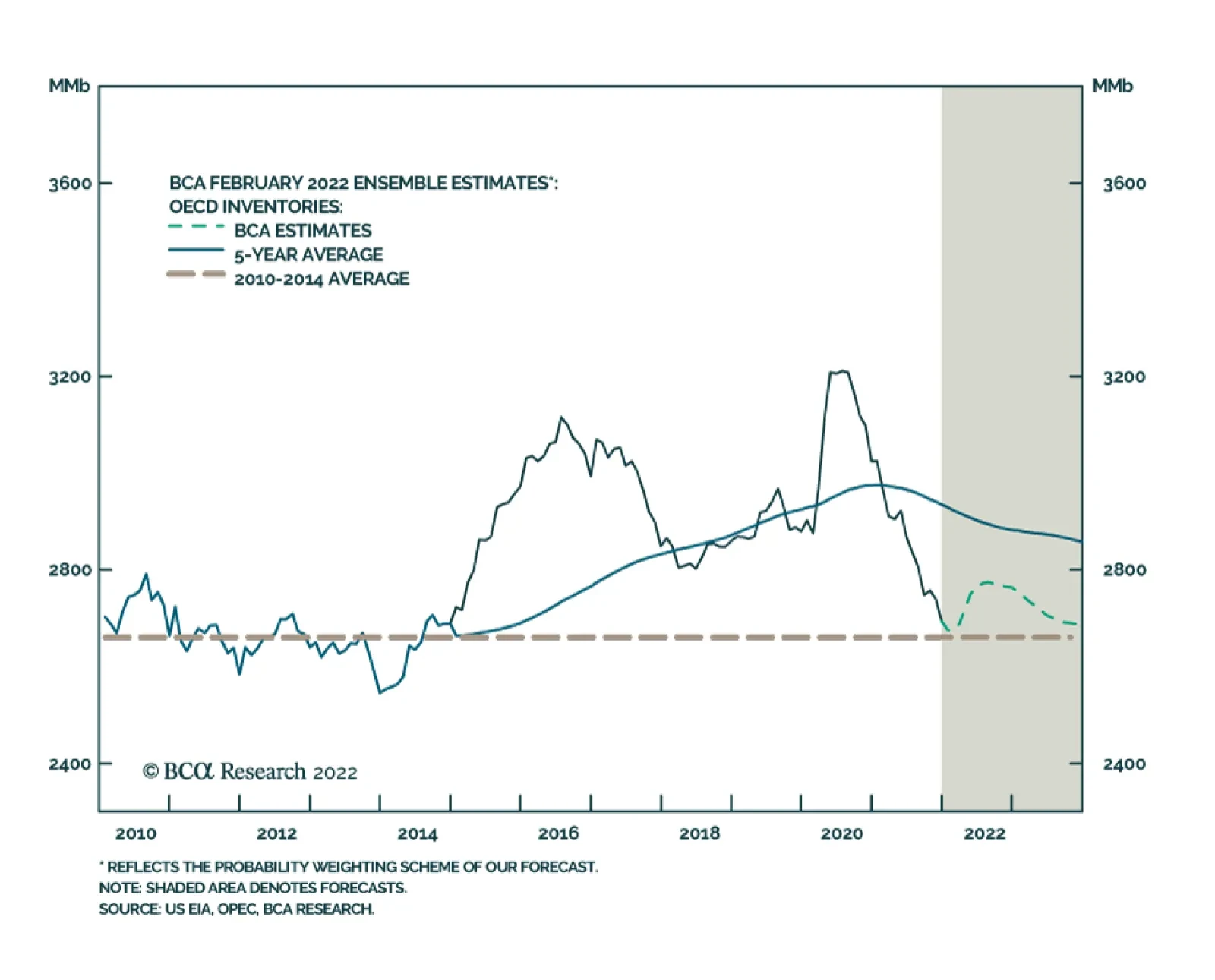

According to BCA Research's Commodity & Energy Strategy service, global oil markets were tight before the invasion of Ukraine. Now, with the trade-flow shifts that we are already seeing, the team expects inventories will be drawn further to cover…