Commodities & Energy Sector

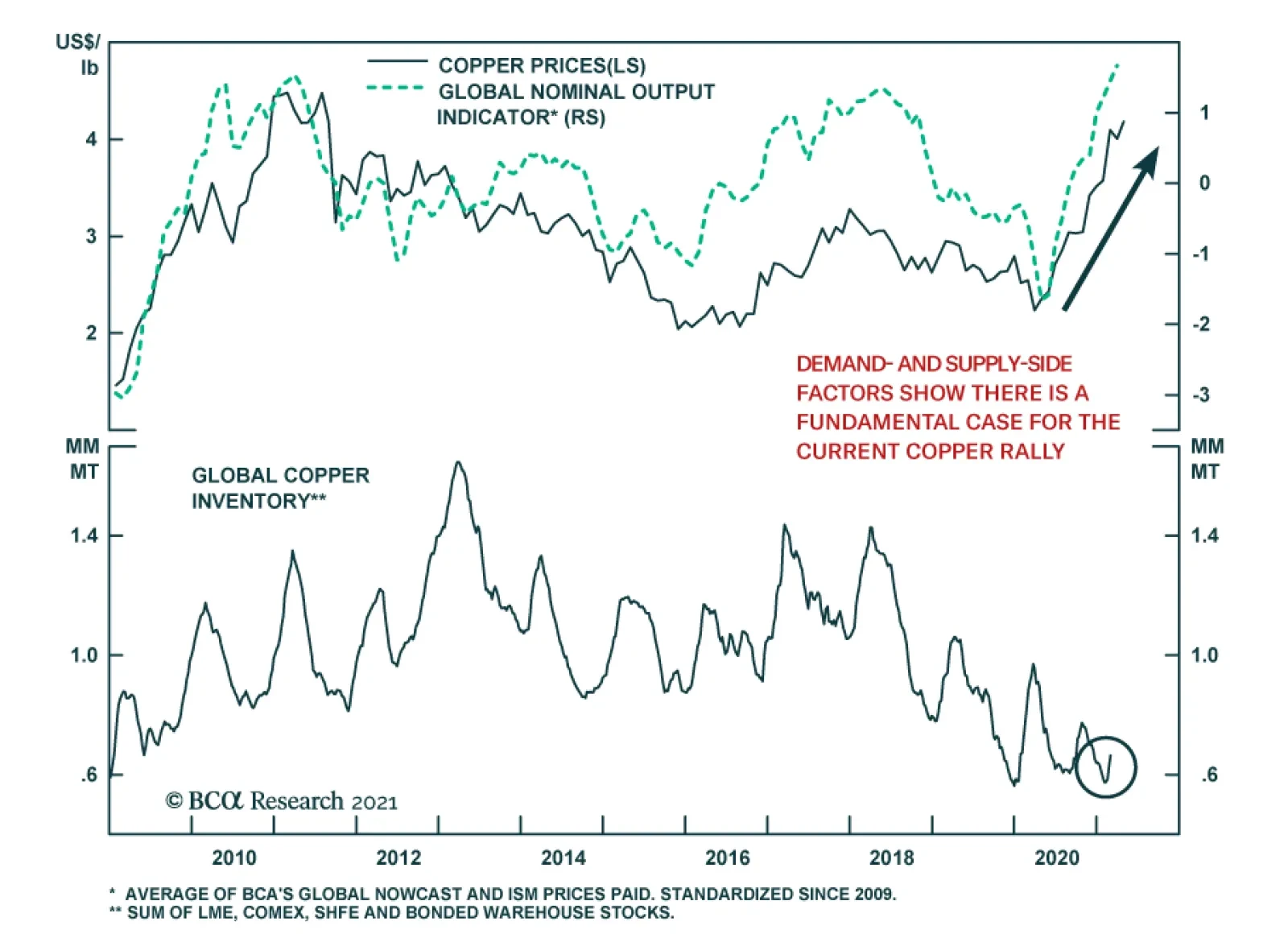

Highlights Higher copper prices will follow in the wake of China's surge in steel demand, which lifted Shanghai steel futures to an all-time high just under 5,200 RMB/MT earlier this month, as building and infrastructure projects are completed this year (Chart of the Week). Copper will register physical deficits this year and next, which will pull inventories even lower and will push demand for copper scrap up in China and globally. High and rising copper prices could prompt government officials to release some of China's massive state holdings of copper – believed to total some 2mm MT – if the current round of market jawboning fails to restrain demand and price increases. Strong steel margins and another round of environmental restraints on mills are boosting demand for high-grade iron ore (65% Fe), which hit a record high of just under $223/MT earlier this week. Benchmark iron ore prices (62% Fe) traded at 10-year highs this week, just a touch below $190/MT. We are lifting our copper price forecast for December 2021 to $5.00/lb from $4.50/lb. In addition, we are getting long 2022 CME/COMEX copper vs short 2023 CME/COMEX copper at tonight's close, expecting steeper backwardation. Feature Government-mandated reductions of up to 30% in steel mill operations for the rest of the year in China's Tangshan steel hub to reduce pollution will tighten an already-tight market responding to a construction and infrastructure boom (Chart 2). This boom triggered a surge in steel prices, and, perforce, in iron ore prices (Chart 3). As it has in the past, this sets the stage for the next leg of copper's bull run. Chart of the WeekSurging Steel Presages Stronger Copper Prices

Surging Steel Presages Stronger Copper Prices

Surging Steel Presages Stronger Copper Prices

In our modeling, we have found a strong relationship between steel prices, particularly for reinforcing bar (rebar), and copper prices, as can be seen in the Chart of the Week. Steel goes into building and infrastructure projects at the front end (in the concrete that is reinforced by steel and in rolled coil products), and then copper goes into the completed project (in the form of wires or pipes). Chart 2Copper Bull Market Will Continue

Copper Bull Market Will Continue

Copper Bull Market Will Continue

In addition to the building and construction boom, continued gains in manufacturing will provide a tailwind for copper prices, which will be augmented by the global recovery in activity 2H21. Chart 4 shows the relationship between nominal GDP levels and copper prices. What's important here is economic growth in Asia (including China) and ex-Asia is, unsurprisingly, cointegrated with copper prices – i.e., economic growth and industrial commodities share a long-term equilibrium, which explains their co-movement. Chart 3Steel Boom Lifts Iron Ore Prices

Steel Boom Lifts Iron Ore Prices

Steel Boom Lifts Iron Ore Prices

Media reports tend to focus on the effects of Chinese government spending as a share of GDP – e.g., total social financing relative to GDP – to the exclusion of the economic, particularly when trying to explain commodity price movements. To the extent the Chinese government is successful in further expanding the private sector – on the goods and services sides – organic economic growth will become even more important in explaining Chinese commodity demand. Chart 4Global Economic Grwoth Will Boost Copper Prices

Global Economic Grwoth Will Boost Copper Prices

Global Economic Grwoth Will Boost Copper Prices

In our copper modeling, we find copper prices to be cointegrated with nominal Chinese GDP, EM Asian GDP and EM ex-Asian GDP, along with steel and iron ore prices, which, from a pure economics point of view, is what would be expected. On the other hand, there is no cointegration – i.e., no economic co-movement or a shared trend – between these industrial commodity prices and total social financing as a percent of nominal China GDP. These models allow us to avoid spurious relationships, which offer no help in explaining or forecasting these copper prices. Chart 5Iron Ore, Copper Demand Will Lift With The "Green Energy" Buildout

Copper Headed Higher On Surge In Steel Prices

Copper Headed Higher On Surge In Steel Prices

Chart 6Renewables Dominate Incremental New Generation

Copper Headed Higher On Surge In Steel Prices

Copper Headed Higher On Surge In Steel Prices

Longer term, as we have written in past research reports, the transition to a low-carbon energy mix favoring distributed renewable electricity generation, more resilient grids and electric vehicles (EVs) will be a major source of demand growth for bulks like iron ore and steel, and base metals, particularly copper (Chart 5).1 Already, renewable generation represents the highest-growth segment of incremental power generation being added to the global grid (Chart 6). Copper Supply Growth Requires Higher Prices Copper supply will have a difficult time accommodating demand in the short term (to end-2022) when, for the most part, the buildout in renewables and EVs will only be getting started. This means that over the medium (to end-2025) and the long terms (2050) significant new supply will have to be developed to meet demand. In the short term, the supply side of refined copper – particularly the semi-refined form of the metal smelters purify into a useable input for manufactured products (condensates) – is running extremely low, as can be seen in the longer-term collapse of Treatment Charges and Refining Charges (TC/RC) at Chinese smelters (Chart 7). At ~ $22/MT last week, these charges were the lowest since the benchmark TC/RC index tracking these charges in China was launched in 2013, according to reuters.com.2 Chart 7Copper TCRCs Fall As Supplies Fall, Pushing Prices Higher

Copper TCRCs Fall As Supplies Fall, Pushing Prices Higher

Copper TCRCs Fall As Supplies Fall, Pushing Prices Higher

The copper supply story also can be seen in Chart 8, which converts annual supply and demand into balances, which will be mediated by the storage market. The International Copper Study Group (ICSG) estimates mine output again registered flat year-on-year growth last year, while refined copper supplies were up a scant 1.5% y/y. Chart 8Physical Deficits Will Draw Copper Stocks...

Physical Deficits Will Draw Copper Stocks...

Physical Deficits Will Draw Copper Stocks...

Consumption was up 2.2%, according to the ICSG's estimates, which expects a physical deficit this year of 456k MT, after adjusting for Chinese bonded warehouse stocks. This will mark the fourth year in a row the copper market has been in a physical deficit, which, since 2017, has averaged 414k MT. The net result of this means inventories will once again be relied on to fill in supply gaps, and global stockpiles, which are down ~25% y/y, and will continue to fall (Chart 9). With mining capex weak and copper ore quality falling, higher prices will be required to incentivize significant new investment in production (Chart 10). However, the lead time on these projects is five years in the best of circumstances, which means miners have to get projects sanctioned with final investment decisions made in the near future (Chart 11). Chart 9...Which After Four Years Of Physical Deficits Are Low

...Which After Four Years Of Physical Deficits Are Low

...Which After Four Years Of Physical Deficits Are Low

Chart 10Higher Copper Prices Required To Reverse Weak Capex, Falling Ore Quality

Higher Copper Prices Required To Reverse Weak Capex, Falling Ore Quality

Higher Copper Prices Required To Reverse Weak Capex, Falling Ore Quality

Chart 11Falling Lead Times To Bring New Mines Online, But Time Is Short

Copper Headed Higher On Surge In Steel Prices

Copper Headed Higher On Surge In Steel Prices

Investment Implications Our focus on copper is driven by the simple fact that it spans all renewable technologies and will be critical for EVs as well, particularly if there is widespread adoption of this technology (Chart 12). We continue to expect copper supply challenges across the short-, medium- and long-term investment horizons. To cover the short term, we recommended going long December 2021 copper on 10 September 2020, and this position is up 39.2%. To cover the longer term, we are long the S&P Global GSCI commodity index and the iShares GSCI Commodity Dynamic Roll Strategy ETF (COMT), recommended 7 December 2017 and 12 March 2021 , respectively, which are down 2.3% and 0.8%. Chart 12Widespread EV Uptake Will Create All New Copper Demand

Copper Headed Higher On Surge In Steel Prices

Copper Headed Higher On Surge In Steel Prices

At tonight's close, we will cover the medium-term opportunity of the copper supply-demand story developed above by getting long the 2022 CME/COMEX copper futures strip and short 2023 CME/COMEX copper futures strip, given our expectation the continued tightening of the market will force inventories to draw, leading to a steeper backwardation in the copper forward curve. The principal risks to our short-, medium- and long-term positions above are a global failure to contain the COVID-19 pandemic, which, we believe is a short-term risk. Second among the risks to these positions is a large release of strategic copper concentrate reserves held by China's State Reserve Bureau (aka, the State Bureau of Minerial Reserves). In the case of the latter risk, the actual holdings of the Bureau are unknown, but are believed to be in the neighborhood of 2mm MT.3 Bottom Line: We remain bullish industrial commodities, particularly copper. Robert P. Ryan Chief Commodity & Energy Strategist rryan@bcaresearch.com Commodities Round-Up Energy: Bullish Texas is expected to add 10 GW of utility-scale solar power by the end of 2022, according to the US EIA. Texas entered the solar market in a big way in 2020, installing 2.5 GW of capacity. The EIA expects The Great State to add ~ 5GW per year in the next two years, which would take total solar capacity to just under 15 GW. Roughly 30% of this new capacity is expected to be built in the Permian Basin, home to the most prolific oil field in the US. By comparison, the leading producer of solar power in the US, California, will add 3.2 GW of new solar capacity, according to the EIA (Chart 13). To end-2022, roughly one-third of total new solar generation in the will be added in Texas, which already is the leading wind-powered generator in the country. Wind availability is highest during the nighttime hours, while solar is most abundant during the mid-day period. Precious Metals: Bullish Palladium prices, trading ~ $2,876/oz on Wednesday, surpassed their previous record of $2,875.50/oz set in February 2020 and are closing in on $3,000/oz, as supply expectations continue to be lowered by Russian metals producer Nornickel, the largest palladium producer in the world (Chart 14). Earlier this week, the company updated earlier guidance and now expects mine output to be down as much as 20% this year in its copper, nickel and palladium operations, due to flooding in its mines. Palladium is used as a catalyst in gasoline-powered automobiles, sales of which are expected to rebound as the world emerges from COVID-19-induced demand destruction and a computer-chip shortage that has limited new automobile supply. In addition, production of platinum-group metals (PGMs) is being hampered by unreliable power supply in South Africa, which has forced the national utility suppling most of the state's power (> 90%) to revert to load-shedding schemes to conserve power. We remain long palladium, after recommending a long position in the metal 23 April 2020; the position is up 35.6%. Chart 13

Copper Headed Higher On Surge In Steel Prices

Copper Headed Higher On Surge In Steel Prices

Chart 14

Palladium Prices

Palladium Prices

Footnotes 1 Please see, e.g., Renewables, China's FYP Underpin Metals Demand, which we published 26 November 2020. It is available at ces.bcaresearch.com. 2 Please see RPT-COLUMN-Copper smelter terms at rock bottom as mine squeeze hits: Andy Home published by reuters.com 14 April 2021. The report notes direct transactions between miners and smelters were reported as low as $10/MT, in a sign of just how tight the physical supply side of the copper market is at present. 3 Please see Column: Supercycle or China cycle? Funds wait for Dr Copper's call, published by reuters.com 20 April 2021. Investment Views and Themes Recommendations Strategic Recommendations Tactical Trades Commodity Prices and Plays Reference Table Trades Closed in 2021 Summary of Closed Trades

Higher Inflation On The Way

Higher Inflation On The Way

COMEX copper peaked at $4.30/lb on February 24, up a remarkable 103% since its late-March 2020 lows. Since then it has traded mostly sideways, but recently perked up and is nearing its February top. Our Commodity & Energy strategists’ most recent…

Highlights There are tentative signs that US growth outperformance is ebbing. The recovery in the manufacturing sector abroad is already taking leadership from the US. This trend will soon rotate to the service sector. As such, long-term investors should begin to accumulate the euro on weakness. The Canadian economy is improving faster than our February assessment. This suggests the CAD could outperform sooner rather than later. Feature Chart I-1The Euro Drives The DXY

Relative Growth, The Euro, And The Loonie

Relative Growth, The Euro, And The Loonie

The US economy has been the growth outperformer this year. As such, yields have been rising faster in the US and the dollar has caught a bid. Since the start of the year, the DXY index has retraced 2.5% of its yearly losses against developed market currencies. Meanwhile, the rally has been a broad-based one with the euro, yen and Swedish krona taking the brunt of the decline (Chart I-1). Our bias is that growth outperformance will rotate from the US to the rest of the world later this year. This should hurt the dollar and benefit procyclical currencies. This week, we look at the euro and loonie, two currencies that should benefit from this shift. EUR/USD And The Manufacturing Cycle The relationship between bond yields and the economy is circular. Long bond yields can be regarded as a key signaling mechanism about the growth prospects of an economy. At the same time, bond yields directly affect financial conditions, especially when they rise too far too fast. From the point of view of short-term currency forecasting, determining the tipping point at which rising yields become restrictive could be extremely beneficial in forecasting relative economic growth. Chart I-2 shows that whenever the relative bond yield between the US and the euro area rises by 1%, near-term relative growth subsequently tips in favor of the latter, with a lag of about 12 months. This is important since the correlation between EUR/USD and relative growth is quite strong in the short term (Chart I-3). As such, while the rise in yields between the US and the euro area can hurt EUR/USD in the short term, it will begin to benefit relative euro/US growth in the longer term. Chart I-2Relative Bond Yields And The Manufacturing Cycle

Relative Bond Yields And The Manufacturing Cycle

Relative Bond Yields And The Manufacturing Cycle

Chart I-3Economic Data Is Surprising To The Upside In The Euro Area

Economic Data Is Surprising To The Upside In The Euro Area

Economic Data Is Surprising To The Upside In The Euro Area

Bond Flows And Other Market Signals Despite the increase in US Treasury yields, we have not seen higher European purchases of US bonds this year (Chart I-4). During the dollar bull market from 2011 to 2020, there was a direct correlation between rising US yields and higher Treasury purchases. One difference this time around is that other safe-haven bond markets like Canada, Australia, New Zealand and even the UK, are sporting attractive yields today. US yields have not risen much against other G10 countries in aggregate. This will continue to dent the extent to which the euro can fall. On the flipside, the upside to the euro could be quite substantial. From a purchasing parity perspective, the euro can rise 15% just to reset its discount relative to the US. PPP adjustments tend to take several years, but if the US continues to pursue inflationary policies, then by definition, the fair value of the euro will also rise (Chart I-5). Chart I-4Europeans Have Not Been Increasing Treasury Holdings

Europeans Have Not Been Increasing Treasury Holdings

Europeans Have Not Been Increasing Treasury Holdings

Chart I-5The Euro Remains Slightly ##br##Undervalued

The Euro Remains Slightly Undervalued

The Euro Remains Slightly Undervalued

Other cyclical factors also suggest that the euro could experience a coiled-spring rebound. Copper prices have surged this year and the traditional relationship with the euro has been offside (Chart I-6). While copper is benefiting from a move away from carbon towards cleaner electricity, the euro can benefit as well. European economies have decades of experience in renewable technology and could begin to see meaningful inflows into these sectors once investment capital is deployed. This makes the Bloomberg forecast of EUR/USD at 1.23 at the end of 2022 too pessimistic (Chart I-7). Chart I-6The Euro Could Have A Coiled-Spring Rebound Soon

The Euro Could Have A Coiled-Spring Rebound Soon

The Euro Could Have A Coiled-Spring Rebound Soon

Chart I-7Sentiment On The Euro Has Been Slightly Reset

Sentiment On The Euro Has Been Slightly Reset

Sentiment On The Euro Has Been Slightly Reset

Finally, we are short EUR/JPY as a tactical hedge with tight stops at 131. We are also lifting our limit-buy on the EUR/USD from 1.15 to 1.16. The Canadian Recovery Is Accelerating Chart I-8The Canadian Business Survey Outlook Was Encouraging

The Canadian Business Survey Outlook Was Encouraging

The Canadian Business Survey Outlook Was Encouraging

The Canadian recovery is taking shape faster than our February assessment, which the latest Business Outlook Survey corroborated. Both investment intentions and future sales growth were quite strong, with the former hitting a multi-decade high (Chart I-8). Notably: Two-thirds of firms see sales exceeding pre-pandemic levels; most firms stated that the second wave is having less or no impact to sales, compared to the first; and capacity constraints remain high in certain industries, but overall inflationary concerns remain relatively subdued. The robustness of the survey took us by surprise, given that a second wave of infections is raging, and most of the country is under lockdown. That said, the strength in investment spending is becoming a key theme in a global context, suggesting Canada could see significant FDI flows in the coming years. Markets have started pricing in a faster pace of rate hikes in Canada (Chart I-9). This has been a rare occurrence over the last decade and, together with our Global Fixed Income Strategy colleagues, we still believe there is less of a chance that Canada leads the hiking cycle. However, this could change if momentum in the economy allows it to surpass US growth. Chart I-9Markets Are Pricing In Faster Hikes In Canada

Markets Are Pricing In Faster Hikes In Canada

Markets Are Pricing In Faster Hikes In Canada

The IMF estimates that Canadian real GDP growth will be 5% this year and 4.7% next year. Growth could be much stronger than these levels, according to the Bloomberg Nanos Confidence Index (Chart I-10). Chart I-10Canadian GDP On The Mend

Canadian GDP On The Mend

Canadian GDP On The Mend

The employment report has improved tremendously since our February assessment (Chart I-11). Looking at the sub-components of the BoC Monitor, the weakness was centered on economic variables. This is changing, as the Canadian unemployment rate is falling faster than the US unemployment rate (Chart I-12). That is a bullish development for the CAD. Chart I-11The Canadian Jobs Recovery Is Robust

The Canadian Jobs Recovery Is Robust

The Canadian Jobs Recovery Is Robust

Chart I-12Canadian Employment Catching Up To The US

Canadian Employment Catching Up To The US

Canadian Employment Catching Up To The US

The Canadian housing market is heating up. Overall, house prices are up 10% with many cities well exceeding these levels (Chart I-13). The path for Canadian housing prices has been as follows: government support and macro prudential measures leading to a convergence in prices between low- and high-priced cities. Specifically, Vancouver (and to a certain extent, Toronto) are seeing softer pricing growth, while other cities recover. However, as prices start to deviate away from nominal incomes in lower-priced cities, the risk of wider macro prudential measures greatly increases. The second point is crucial, since the rise in Canadian home prices has been more pronounced than in other countries, such as Australia or the US. This means that both rising indebtedness and falling affordability are likely to present a key macro risk to the Canadian economy. Residential construction is a non-negligible part of the Canadian economy (Chart I-14). Chart I-13The Canadian Housing Market Has Heated Up

The Canadian Housing Market Has Heated Up

The Canadian Housing Market Has Heated Up

Chart I-14Residential Construction Is Booming

Residential Construction Is Booming

Residential Construction Is Booming

Bottom Line: Recent developments are increasing the odds that the Bank of Canada hikes rates sooner rather than later. This will allow further gains in the CAD. The CAD And Oil Crude oil prices are another hugely important driver for the CAD. In fact, for most of this year, interest rates have not been an important factor as the BoC faded any near-term improvement in the Canadian outlook. The Covid-19 crisis together with slow vaccination progress also hurt the recovery, putting the brakes on an appreciating loonie (Chart I-15). Our commodity strategists predict that Brent crude will hit $75 in 2023. This is higher than the forward markets are discounting. Rising forward prices will be synonymous with a higher CAD. However, Canada sells the Western Canadian Select (WCS) blend, which has historically traded at a significant discount to Brent or WTI (Chart I-16). Rising environmental standards hurt Canada, since WCS has a higher sulphur content. Pipeline capacity also remains a major bottleneck to getting Canadian crude to US refineries. Chart I-15The Loonie Has Lagged

The Loonie Has Lagged

The Loonie Has Lagged

Chart I-16Canadian Oil Prices Could Lag The Recovery

Canadian Oil Prices Could Lag The Recovery

Canadian Oil Prices Could Lag The Recovery

The redeeming feature this time around is that the correlation between the CAD/USD and crude oil prices is rising faster than for other currencies, as the US begins to embark on significant infrastructure projects (Chart I-17). Around 50% of US oil imports come from Canada. The Covid-19 crisis also slowed US oil production relative to Canada, which has helped increase the correlation between oil prices and the currency. Portfolio flows into Canada have been accelerating this year, benefitting oil stocks and the loonie. Chart I-17Sensitivity Of USD/CAD To Oil Has Increased

Sensitivity Of USD/CAD To Oil Has Increased

Sensitivity Of USD/CAD To Oil Has Increased

Investment Conclusions Chart I-18The CAD Is Cheap

The CAD Is Cheap

The CAD Is Cheap

The CAD remains cheap. It is trading at one standard deviation below its long-term mean, on a real effective exchange rate basis (Chart I-18). A return to the mean would generate about 10% upside. Our PPP model is less bullish, suggesting the loonie is cheap by about 5%. This still puts 84-85 cents within striking distance. Should the nascent Canadian recovery morph into a genuine acceleration, the CAD could rally even higher. Chester Ntonifor Foreign Exchange Strategist chestern@bcaresearch.com Currencies U.S. Dollar Chart II-1USD Technicals 1

USD Technicals 1

USD Technicals 1

Chart II-2USD Technicals 2

USD Technicals 2

USD Technicals 2

US economic data has been robust this week: CPI in March rose 2.6% year-on-year and 0.6% month-on-month, both exceeding expectations. PPI in March came in at 4.2% year-on-year and 1% month-on-month, beating expectations. The Empire Manufacturing survey staged a meaningful rebound from 17.4 to 26.3 in April. Retail sales were particularly strong, coming in at 9.8% month-on-month in March. The NAHB housing market index remained strong at 83 in April. The DXY Index fell by 0.5% this week. The drop in bond yields was surprising, given robust data. This is likely a signal that bond short positions are becoming a crowded trade. The DXY index is rolling over in April; a trend that supports its seasonal pattern. Report Links: Arbitrating Between Dollar Bulls And Bears - March 19, 2021 The Dollar Bull Case Will Soon Fade - March 5, 2021 Are Rising Bond Yields Bullish For The Dollar? - February 19, 2021 The Euro Chart II-3EUR Technicals 1

EUR Technicals 1

EUR Technicals 1

Chart II-4EUR Technicals 2

EUR Technicals 2

EUR Technicals 2

Recent data from the euro area have been mildly positive: Retail sales grew by 3% month-on-month in February versus the expected 1.7%. ZEW Economic Sentiment for both Germany and the EU in April came in lower than forecast. Industrial production fell by 1% in February over the prior month. German CPI came in at 0.5% month-on-month, in line with forecasts. The euro rose by 0.5% against the dollar this week, making this a second week of appreciation. The new Covid-19 wave may be a drag on EUR/USD in the near term, but this has also reset sentiment and positioning indicators. Our intermediate-term indicator has rolled over substantially, which is bullish from a contrarian perspective. Report Links: Portfolio And Model Review - February 5, 2021 On Japanese Inflation And The Yen - January 29, 2021 The Dollar Conundrum And Protection - November 6, 2020 JapaneseYen Chart II-5JPY Technicals 1

JPY Technicals 1

JPY Technicals 1

Chart II-6JPY Technicals 2

JPY Technicals 2

JPY Technicals 2

Data out of Japan have been mixed: Machinery orders recorded another month of decline, falling by 8.5% month-on-month in February versus an expected 2.8% increase. However, more positively, machine tool orders grew by 65% year-on-year in March. PPI in February came in at 0.8% month-on-month, better than expectations. The Japanese yen rose by 0.4% against the US dollar this week and remains one of the strongest G10 currencies in April. Our intermediate-term indicator has collapsed and speculators are net short the currency. We remain short EUR/JPY as a portfolio hedge. Report Links: The Dollar Bull Case Will Soon Fade - March 5, 2021 On Japanese Inflation And The Yen - January 29, 2021 The Dollar Conundrum And Protection - November 6, 2020 British Pound Chart II-7GBP Technicals 1

GBP Technicals 1

GBP Technicals 1

Chart II-8GBP Technicals 2

GBP Technicals 2

GBP Technicals 2

Recent data out of the UK have been mildly positive: February GDP rose 0.4% versus the prior month, slightly falling short of the expected 0.6% rise. Both the industrial and manufacturing production and the construction output exceeded expectations in February, growing at 1%, 1.3%, and 1.6% month-on-month. The trade deficit with the EU increased to 16.4B in February. The British pound rose by 0.3% against the US dollar this week, ranking in the middle among G10 currencies and flat against the Euro. We exited our short EUR/GBP trade last week to take profit on UK’s vaccination success and expected catch up phase for other economies. The elevated net speculative positioning on the pound also makes us neutral. Report Links: Portfolio And Model Review - February 5, 2021 The Dollar Conundrum And Protection - November 6, 2020 Revisiting Our High-Conviction Trades - September 11, 2020 Australian Dollar Chart II-9AUD Technicals 1

AUD Technicals 1

AUD Technicals 1

Chart II-10AUD Technicals 2

AUD Technicals 2

AUD Technicals 2

Recent data in Australia were strong: NAB business conditions came in at 25 in March versus 17 in February. The Westpac Consumer Confidence Index for April rose 6.2% month-on-month to 118.8, highest since August 2010. The labor recovery remains on track. 71K new jobs were added in March versus expectations of 35K. The unemployment rate also fell from 5.8% to 5.6%. The Australian dollar remained flat against the US dollar this week. However, the recent robust data, soaring terms of trade, and high bond yields make AUD/USD a suitable recovery trade. That said, given Mexico’s proximity to the US where recent economic data are strong, we are short the AUD/MXN pair. Report Links: The Dollar Bull Case Will Soon Fade - March 5, 2021 Portfolio And Model Review - February 5, 2021 Australia: Regime Change For Bond Yields & The Currency? - January 20, 2021 New Zealand Dollar Chart II-11NZD Technicals 1

NZD Technicals 1

NZD Technicals 1

Chart II-12NZD Technicals 2

NZD Technicals 2

NZD Technicals 2

The was scant data out of New Zealand this week: RBNZ held the official cash rate at 0.25% and its asset purchase program steady against a backdrop of a heated housing market, citing uncertainty over the outlook for growth. The NZIERB Business Confidence came in at -13% for Q1 versus -6% in Q4, a first decline in four quarters. The New Zealand dollar remained flat against the US dollar this week. On the day of the rate announcement, NZD rallied while the OIS curve flattened, which is a perplexing development. We believe the OIS curve had the appropriate response. Near term upside risk for Kiwi is the planned travel bubble with Australia. We are long the AUD/NZD. Report Links: Portfolio And Model Review - February 5, 2021 Currencies And The Value-Versus-Growth Debate - July 10, 2020 Updating Our Balance Of Payments Monitor - November 29, 2019 Canadian Dollar Chart II-13CAD Technicals 1

CAD Technicals 1

CAD Technicals 1

Chart II-14CAD Technicals 2

CAD Technicals 2

CAD Technicals 2

The recent data out of Canada have been strong: The Bank of Canada Business Outlook Survey was robust. The sentiment indicator recorded 2.87 in Q1, up from 1.3 in Q4 and highest since 2018. The March employment report was blockbuster. There were 303K new jobs versus an expectation of 100K. The split between part-time and full-time was healthy, 175K versus 128K. This brought down the unemployment rate to 7.5% in March, beating both forecasts and the February reading of 8.2%. The Canadian dollar rose by 0.3% against the US dollar this week. We spend some time in the front section discussing the Canadian dollar, which could be a little vulnerable in the short term, but could touch 84 cents in the coming 12-months. Report Links: Will The Canadian Recovery Lead Or Lag The Global Cycle? - February 12, 2021 Currencies And The Value-Versus-Growth Debate - July 10, 2020 More On Competitive Devaluations, The CAD And The SEK - May 1, 2020 Swiss Franc Chart II-15CHF Technicals 1

CHF Technicals 1

CHF Technicals 1

Chart II-16CHF Technicals 2

CHF Technicals 2

CHF Technicals 2

There was scant data out of Switzerland this week: The unemployment reading was 3.3% in March, lower than both the forecast and prior month. The Swiss franc was flat against the US dollar this week, remaining a top performer amongst the G10 currencies in April. As we indicated in last week’s report, the Franc may be due for a rebound after its underperformance in the first three months this year. While the CHF may continue its appreciation against the US dollar, we are long EUR/CHF on valuations concern, but are maintaining tight stops at 1.095. Our USD/CHF intermediate-term indicator is also due for a reversal. Report Links: Portfolio And Model Review - February 5, 2021 The Dollar Conundrum And Protection - November 6, 2020 On The DXY Breakout, Euro, And Swiss Franc - February 21, 2020 Norwegian Krone Chart II-17NOK Technicals 1

NOK Technicals 1

NOK Technicals 1

Chart II-18NOK Technicals 2

NOK Technicals 2

NOK Technicals 2

The recent data out of Norway have been mixed: GDP in February fell by 0.5% month-on-month. House prices increased by 3.4% quarter-on-quarter in Q1. March CPI came in at 3.1% year-on-year, versus expectations of a 3.4% increase. CPI disappointment was driven mainly by a 0.6% month-on-month decline in consumer goods prices. The Norwegian krone remained flat against the US dollar this week. Despite the Norges Bank’s expected rate hike this year, the earliest amongst the G10 nations, the NOK may see near term downside risks given the weak inflation data this month and the potential weakening in oil prices due to renewed virus lockdowns globally. Strategically we remain long NOK along with SEK for an eventual decline in the dollar. Report Links: Portfolio And Model Review - February 5, 2021 Revisiting Our High-Conviction Trades - September 11, 2020 A New Paradigm For Petrocurrencies - April 10, 2020 Swedish Krona Chart II-19SEK Technicals 1

SEK Technicals 1

SEK Technicals 1

Chart II-20SEK Technicals 2

SEK Technicals 2

SEK Technicals 2

The recent inflation data out of Sweden have been strong: The CPIF measure, favored by the Riksbank, rose 1.9% year-on-year versus the 1.5% increase in February. The rise was only was 1.4% ex-energy, but most inflation measures have rebounded powerfully from the 2020 lows. The Swedish krona, up by 1.4% against US dollar this week, was a top performing G10 currency both this week and in April. The 5-year and 10-year inflation swaps remain well anchored above the 2% level, suggesting markets are not regarding the increase in Swedish inflation as transitory. This could bring forward rate hike expectations. The higher 2-year real yield in Sweden versus US, due to higher US inflation, will also support the SEK. However, new Covid-19 cases remain a concern. Report Links: Revisiting Our High-Conviction Trades - September 11, 2020 Updating Our Balance Of Payments Monitor - November 29, 2019 Where To Next For The US Dollar? - June 7, 2019 Trades & Forecasts Forecast Summary Core Portfolio Tactical Trades Limit Orders Closed Trades

Highlights Stronger global growth in the wake of continued and expected fiscal and monetary stimulus, and progress against COVID-19 are boosting oil demand assumptions by the major data suppliers for this year. We lifted our 2021 global demand estimate by 640k b/d to 98.25mm b/d, and assume OPEC 2.0 will make the necessary adjustments to keep Brent prices closer to $60/bbl than not, so as not to disrupt a fragile recovery. We are maintaining our 2022 and 2023 Brent forecasts at $65/bbl and $75/bbl. Commodity markets are ignoring the rising odds of armed conflict involving the US, Russia and China and their clients and allies. Russia has massed troops on Ukraine’s border and warned the US not to interfere. China has massed warships off the coast of the Philippines, and continues its incursions in Taiwan’s air-defense zone, keeping US forces on alert. Intentional or accidental engagement would spike oil prices. Two-way price risk abounds. In addition to the risk of armed hostilities, faster distribution of vaccines would accelerate recovery and boost prices above our forecasts. Downside risk of a resurgence in COVID-19-induced lockdowns remains, as rising death and hospitalization rates in Brazil, India and Europe attest (Chart of the Week). Feature Oil-demand estimates – ours included – are reviving in the wake of measurable progress in combating the COVID-19 pandemic in major economies, and an abundance of fiscal and monetary stimulus, particularly out of the US.1 On the back of higher IMF GDP projections, we lifted our 2021 global demand estimate by 640k b/d to 98.25mm b/d in this month’s balances. In our modeling, we assume OPEC 2.0 will make the necessary adjustments to keep Brent prices closer to $60/bbl than not, so as not to disrupt a fragile recovery. In an unusual turn of events, the early stages of the recovery in oil demand will be led by DM markets, which we proxy using OECD oil consumption (Chart 2). Thereafter, EM economies, re-take the growth lead next year and into 2023. Chart of the WeekCOVID-19 Deaths, Hospitalizations Threaten Global Recovery

Upside Oil Price Risks Are Increasing

Upside Oil Price Risks Are Increasing

Chart 2DM Demand Surges This Year

DM Demand Surges This Year

DM Demand Surges This Year

Absorbing OPEC 2.0 Spare Capacity We continue to model OPEC 2.0, the producer coalition led by the Kingdom of Saudi Arabia (KSA) and Russia, as the dominant producer in the market. The growth we are expecting this year will absorb a significant share of OPEC 2.0’s spare capacity, most of which – ~ 6mm b/d of the ~ 8mm b/d – is to be found in KSA (Chart 3). The core producers’ spare capacity allows them to meet recovering demand faster than the US shale producers can mobilize rigs and crews and get new supply into gathering lines and on to main lines. We model the US shale producers as a price-taking cohort, who will produce whatever the market allows them to produce. After falling to 9.22mm b/d in 2020, we expect US production to recover to 9.56mm b/d this year, 10.65mm b/d in 2022, and 11.18mm in 2023 (Chart 4). Lower 48 production growth in the US will be led by the shales, which will account for ~ 80% of total US output each year. Chart 3Core OPEC 2.0 Spare Capacity Will Respond First To Higher Demand

Core OPEC 2.0 Spare Capacity Will Respond First To Higher Demand

Core OPEC 2.0 Spare Capacity Will Respond First To Higher Demand

Chart 4Shale Is The Marginal Barrel In The Price Taking Cohort

Shale Is The Marginal Barrel In The Price Taking Cohort

Shale Is The Marginal Barrel In The Price Taking Cohort

OPEC 2.0’s dominant position on the supply side allows it to capture economic rents before non-coalition producers, which will remain a disincentive to them until the spare capacity is exhausted. Thereafter, the price-taking cohort likely will fund much of its E+P activities out of retained earnings, given their limited ability to attract capital. Equity investors will continue to demand dividends that can be maintained and grown, or return of capital via share buybacks. This will restrain production growth to those firms that are profitable. We expect the OPEC 2.0 coalition’s production discipline will keep supply levels just below demand so that inventories continue to fall, just as they have done during the COVID-19 pandemic, despite the demand destruction it caused (Chart 5). These modeling assumptions lead us to continue to expect supply and demand will continue to move toward balance into 2023 (Table 1). Chart 5Supply-Demand Balances in 2021

Supply-Demand Balances in 2021

Supply-Demand Balances in 2021

Table 1BCA Global Oil Supply - Demand Balances (MMb/d, Base Case Balances)

Upside Oil Price Risks Are Increasing

Upside Oil Price Risks Are Increasing

We continue to expect this balancing to induce persistent physical deficits, which will keep inventories falling into 2023 (Chart 6). As inventories are drawn, OPEC 2.0’s dominant-producer position will allow it to will keep the Brent and WTI forward curves backwardated (Chart 7).2 We are maintaining our 2022 and 2023 Brent forecasts at $65/bbl and $75/bbl (Chart 8). Chart 6OPEC 2.0 Policy Continues To Keep Supply Below Demand...

OPEC 2.0 Policy Continues To Keep Supply Below Demand...

OPEC 2.0 Policy Continues To Keep Supply Below Demand...

Chart 7OECD Inventories Fall to 2023

OECD Inventories Fall to 2023

OECD Inventories Fall to 2023

Chart 8Brent Forecasts Rise As Global Economy Recovers

Brent Forecasts Rise As Global Economy Recovers

Brent Forecasts Rise As Global Economy Recovers

Two-Way Price Risk Abounds Risks to our views abound on the upside and the downside. To the upside, the example of the UK and the US in mobilizing its distribution of vaccines is instructive. Both states got off to a rough start, particularly the US, which did not seem to have a strategy in place as recently as January. After the US kicked its procurement and distribution into high gear its vaccination rates soared and now appear to be on track to deliver a “normal” Fourth of July holiday in the US. The UK has begun its reopening this week. Both states are expected to achieve herd immunity in 3Q21.3 The EU, which mishandled its procurement and distribution likely benefits from lessons learned in the UK and US and achieves herd immunity in 4Q21, according to McKinsey’s research. Any acceleration in this timetable likely would lead to stronger growth and higher oil prices. The next big task for the global community will be making vaccines available to EM economies, particularly those in which the pandemic is accelerating and providing the ideal setting for mutations and the spread of variants that could become difficult to contain. The risk of a resurgence in large-scale COVID-19-induced lockdowns remains, as rising death and hospitalization rates in Brazil, India and Europe attest. Cry Havoc The other big upside risk we see is armed conflict involving the US, Russia, China and their clients and allies. Commodity markets are ignoring these risks at present. Even though they do not rise to the level of war, the odds of kinetic engagement – planes being shot down or ships engaging in battle in the South China Sea – are rising on a daily basis. This is not unexpected, as our colleagues in BCA Research’s Geopolitical Strategy pointed out recently.4 Indeed, our GPS service, led by Matt Gertken, warned the Biden administration would be tested in this manner by Russia and China from the get-go. Russia has massed troops on Ukraine’s border and warned the US not to interfere. China has massed warships off the coast of the Philippines, and continues its incursions in Taiwan’s air-defense zone, keeping US forces on alert. Political dialogue between the US and Russia and the US and China is increasingly vitriolic, with no sign of any leavening in the near future. Intentional or accidental engagement could let slip the dogs of war and spike oil prices briefly. Finally, OPEC 2.0 is going to have to accommodate the “official” return of Iran as a bona fide oil exporter, if, as we expect, it is able to reinstate its nuclear deal – i.e., the Joint Comprehensive Plan of Action (JCPOA) – with Western states, which was abrogated by then-President Donald Trump in 2018. This may prove difficult, given our view that the oil-price collapse of 2014-16 was the result of the Saudis engineering a market-share war to tank prices, in an effort to deny Iran $100+ per-barrel prices that had prevailed between end-2010 and mid-2014. OPEC 2.0, particularly KSA, has not publicly involved itself in the US-Iran negotiations. However, it is worthwhile recalling that following the disastrous market-share war launched in 2014, KSA and the rest of OPEC 2.0 did accommodate Iran’s return to markets post-JCPOA. Robert P. Ryan Chief Commodity & Energy Strategist rryan@bcaresearch.com Ashwin Shyam Research Associate Commodity & Energy Strategy ashwin.shyam@bcaresearch.com Commodities Round-Up Energy: Bullish Brent and WTI prices rallied sharply following the release of the EIA’s Weekly Petroleum Status Report showing a 9.1mm-barrel decline in US crude and product stocks for the week ended 9 April 2021. This was led by a huge draw in commercial crude and distillate inventories (5.9mm barrels and 2.1mm barrels, respectively). These draws came on the back of generally bullish global demand upgrades by the major data services (EIA, IEA and OPEC) over the past week. These assessments were supported by EIA data showing refined-product demand – i.e., “product supplied” – jumped 1.1mm b/d for the week ended 9 April. With vaccine distributions picking up steam, despite setbacks on the Johnson & Johnson jab, the storage draws and improved demand appear to have catalyze the move higher. Continued weakness in the USD also provided a tailwind, as did falling real interest rates in the US. Base Metals: Bullish Nickel prices fell earlier this week, as China’s official Xinhua news agency reported that Chinese Premier, Li Keqiang stressed the need to strengthen raw materials’ market regulation, amidst rising commodities prices, which been pressuring corporate financial performance (Chart 9). This statement came after China’s top economic advisor, Liu He also called for authorities to track commodities prices last week. Nickel prices fell by around $500/ ton earlier this week on this news, and were trading at $16,114.5/MT on the London Metals exchange as of Tuesday’s close. Other base metals were not affected by this news. Precious Metals: Bullish The US dollar and 10-year treasury yields fell after March US inflation data was released earlier this week. US consumer prices rose by the most in nearly nine years. The demand for an inflation hedge, coupled with the falling US dollar and treasury yields, which reduce the opportunity cost of purchasing gold, caused gold prices to rise (Chart 10). This uncertainty, coupled with the increasing inflationary pressures due to the US fiscal stimulus will increase demand for gold. Spot COMEX gold prices were trading at $1,746.20/oz as of Tuesday’s close. Ags/Softs: Neutral The USDA reported ending stocks of corn in the US stood at 1.35 billion bushels, well below market estimates of 1.39 billion and the 1.50 billion-bushel estimate by the Department last month, according to agriculture.com’s tally. Global corn stocks ended at 283.9mm MT vs a market estimate of 284.5mm MT and a Department estimate of 287.6mm MT. Chart 9Base Metals Are Being Bullish

Base Metals Are Being Bullish

Base Metals Are Being Bullish

Chart 10Gold Prices To Rise

Gold Prices To Rise

Gold Prices To Rise

Footnotes 1 Please see US-Russia Pipeline Standoff Could Push LNG Prices Higher, which we published on 8 April 2021 re the IMF’s latest forecast for global growth. Briefly, the Fund raised its growth expectations for this year and next to 6% and 4.4%, respectively, nearly a full percentage-point increase versus its January forecast update for 2021 2 A backwardated forward curve – prompt prices trading in excess of deferred prices – is the market’s way of signaling tightness. It means refiners of crude oil value crude availability right now over availability a year from now. This is exactly the same dynamic that drives an investor to pay $1 today for a dollar bill delivered tomorrow than for that same dollar bill delivered a year from now (that might only fetch 98 cents today, e.g.). 3 Please see When will the COVID-19 pandemic end?, published 26 March 2021 by McKinsey & Co. 4 Please see The Arsenal Of Democracy, a prescient analysis published 2 April 2021 by BCA’s Geopolitical Strategy. The report notes the Biden administration “still faces early stress-tests on China/Taiwan, Russia, Iran, and even North Korea. Game theory helps explain why financial markets cannot ignore the 60% chance of a crisis in the Taiwan Strait. A full-fledged war is still low-probability, but Taiwan remains the world’s preeminent geopolitical risk.” Investment Views and Themes Recommendations Strategic Recommendations Tactical Trades Commodity Prices and Plays Reference Table Trades Closed in 2021 Summary of Closed Trades

Higher Inflation On The Way

Higher Inflation On The Way

Dear Client, Next week I will be hosting a series of Roundtable discussions with BCA’s clients in both Europe and Asia. Our next report published on April 28th will be a recap of my observations from these meetings. Best regards, Jing Sima China Strategist Highlights The sharp uptick in Chinese producer prices should be transitory, unlikely to trigger a policy response. There are two scenarios under which Chinese manufacturers’ profit margins will benefit: either Chinese exporters will raise export prices and pass input costs onto American customers, or the RMB will depreciate versus the US dollar and commodities prices will experience a setback. The second scenario is more likely in the next 3-6 months. After a pandemic-driven boost in 2020, US imports from China will likely moderate in the second half of 2021 and into 2022. President Biden’s grand infrastructure spending plan, even if approved later this year, will not be a game changer for China’s exports or economy. The strength in the USD may intensify in the near term, and Chinese policymakers will be happy to allow the RMB to depreciate mildly. Stay underweight Chinese stocks. Feature Last week’s China’s producer price index (PPI) was more elevated than the market expected. However, it does not warrant a policy response, given that the increase was mostly driven by supply constraints rather than an overheating domestic economy. Chinese manufacturers have had a tough time passing on mounting input prices to customers, which raises the question about how profit margins will be maintained. For exporters, the answer may be a combination of increasing export prices in USD terms and depreciating the RMB. The rate of growth in US demand for Chinese export goods may moderate in the second half of 2021 and into 2022 after a pandemic-driven boost in 2020. China’s economic growth and interest rate differentials with the US will continue to narrow in the rest of this year. We expect the RMB to face headwinds against the USD, at least in the next quarter or two. Meanwhile, global investors should continue to underweight Chinese stocks. The PBoC Will Not React To Supply-Side Price Pressures Chart 1Marchs Strong PPI Does Not Reflect An Overheating Domestic Economy

Marchs Strong PPI Does Not Reflect An Overheating Domestic Economy

Marchs Strong PPI Does Not Reflect An Overheating Domestic Economy

Despite above-expectation readings in China’s PPI, the domestic economy shows no signs of overheating. The upside pressure on producer prices reflects the impact of both the global rally in commodities and base effects (Chart 1). In March, strength in the PPI was also accentuated by seasonality due to a resumption in construction and real estate activity following the Chinese New Year holiday. While base effects and global supply bottlenecks will continue to buoy PPI prints throughout Q2, these effects are likely transitory and would not justify a policy response. At 0.4% year-over-year in March, core CPI remains significantly below the central bank’s 3% target and does not indicate any demand-side pressure. Instead, the inability for Chinese producers to pass on higher input prices to consumers highlights the relatively subdued state of domestic demand (Chart 1, bottom panel). Chart 2Current Macro Policy Works To Cap The Upsides In Both The Price And Quantity Of Money

Current Macro Policy Works To Cap The Upsides In Both The Price And Quantity Of Money

Current Macro Policy Works To Cap The Upsides In Both The Price And Quantity Of Money

At this point there are little signs that rising producer prices are spilling over to consumer prices. We expect Chinese authorities to continue its current policy trajectory, which intends to keep a steady interbank rate while keeping money supply growth at or below the rate of nominal GDP expansion (Chart 2). China’s Deteriorating Terms Of Trade Chinese export prices climbed slightly in USD terms, but not by enough to offset the RMB’s relentless appreciation from the second half of last year, as indicated by falling export prices in RMB terms (Chart 3). A deteriorating terms of trade (ToT), defined as export prices relative to import costs, means that Chinese producers must export a greater number of units to purchase the same number of imports (Chart 4). The declining ToT can be a powerful deflationary force for China’s manufacturing sector. Chart 3Chinese Export Prices Are Rising In USD Terms But Falling In Local Currency Terms

Chinese Export Prices Are Rising In USD Terms But Falling In Local Currency Terms

Chinese Export Prices Are Rising In USD Terms But Falling In Local Currency Terms

Chart 4Terms Of Trade Have Been Falling

Terms Of Trade Have Been Falling

Terms Of Trade Have Been Falling

Chart 5Chinese Output Prices Lead US Consumer Inflation By A Year

Chinese Output Prices Lead US Consumer Inflation By A Year

Chinese Output Prices Lead US Consumer Inflation By A Year

While there are limited choices for China to improve its ToT, manufacturers could raise export prices in USD terms and “recycle” cost-push inflation back to the US. Chinese PPI normally leads US consumer inflation by 12 to 18 months (Chart 5). Hence, it is possible that the US will see import prices from China picking up more momentum by the middle of next year. The RMB’s performance is a key macro driver for manufacturing-related output prices. A depreciation in the RMB can be a meaningful reflationary force for manufacturers. There has been a clear negative correlation between the trade-weighted RMB and Chinese manufacturers' output prices and industrial profits, as shown in Chart 6. In this scenario, the USD will continue to appreciate against the RMB and possibly emerging market currencies, a headwind to global trade (Chart 7). Chart 6A Falling RMB Can Be Reflationary To Chinese Producers

A Falling RMB Can Be Reflationary To Chinese Producers

A Falling RMB Can Be Reflationary To Chinese Producers

Chart 7A Stronger USD Will Be Headwinds For Global Trade

A Stronger USD Will Be Headwinds For Global Trade

A Stronger USD Will Be Headwinds For Global Trade

Maintaining a strong RMB can partly mitigate the pain stemming from escalating commodity import prices. However, in our view it is the least preferred option by policymakers. In previous cycles a rapidly strengthening RMB did not have a major impact on Chinese exporters' competitiveness, mainly because declines in commodities prices effectively offset a rising RMB (Chart 8 and Chart 9). Therefore, Chinese exporters did not need to boost prices in USD terms to maintain their profit margins. Chart 8RMB Appreciations Did Not Hurt Chinas Share In Global Trade

RMB Appreciations Did Not Hurt Chinas Share In Global Trade

RMB Appreciations Did Not Hurt Chinas Share In Global Trade

Chart 9...Because Declines In Commodities Prices Were Able To Offset A Rising RMB

...Because Declines In Commodities Prices Were Able To Offset A Rising RMB

...Because Declines In Commodities Prices Were Able To Offset A Rising RMB

Bottom Line: Chinese exporters can either raise prices and pass the inflation onto American customers, or the PBoC will allow further depreciation in the RMB to maintain Chinese producers’ competitiveness. Appreciating the RMB is the least preferred option. Don’t Count On A US Buying Spree Market participants in China are pricing in large windfalls from the US$1.9 trillion American Rescue Plan and proposed US$2.4 trillion American Jobs Plan.1 A positive export tailwind in Q1 this year boosted China’s economic activity beyond what measures of domestic money and credit would have predicted, as shown in Chart 10. However, given the strongly positive relationship between the export sector and real investment in China, it is concerning that any deceleration in US demand for Chinese export goods would seriously challenge the sanguine view for China’s economy this year (Chart 11). Chart 10Export Strength Appears To Be Propping Up The LKI

Export Strength Appears To Be Propping Up The LKI

Export Strength Appears To Be Propping Up The LKI

Chart 11China's Export Sector Is Highly Investment-Intensive

From Deflation To Inflation … What’s Next?

From Deflation To Inflation … What’s Next?

Moreover, US demand for Chinese export goods is subject to several countervailing forces, at least in the second half of 2021: The USD currently benefits from widening real interest differentials and stronger US growth relative to the rest of the world. For the next quarter or two, persistent strength in the USD and US Treasury yields will be headwinds to global trade and may cause a temporary setback for the global manufacturing sector (Chart 7 on Page 4). Residential and business investment in the US may not regain much vigor despite large stimulus checks. Our colleagues at BCA US Investment Strategy expect US residential investment to match the long-run trend growth, but the increase will be largely offset by below-trend growth in non-residential investment. More working-from-home options will continue to drive demand for single-family homes in the suburbs and beyond. On the other hand, demand will suffer for office space in central business districts and dwellings in urban centers. Brick-and-mortar retail construction is also going to crater. Consumption for goods in the US may also see below-trend growth in the second half of 2021 and into 2022, whereas the service sector will benefit most from the coming recovery in US business and social activities. Table 1 shows that goods spending rose in 2020 despite an overall decline in consumption, because households dramatically shifted their consumption into goods from services. As such, 2020’s pandemic-driven dividend for Chinese exporters is likely to become a drag on tradeable goods exports to the US in 2021 and/or 2022. Table 1US Consumer Spending Gap Is Almost Entirely On The Services Side

From Deflation To Inflation … What’s Next?

From Deflation To Inflation … What’s Next?

It is also important for investors to put the US$2.4 trillion infrastructure spending budget proposed in the American Jobs Plan into prospective. The US lags far behind China in infrastructure spending. In the past 10 years, US public infrastructure investment (federal and state combined) has declined to an average of about $450 billion.2 This compares with China’s US $1.9 trillion yearly spending on infrastructure (Chart 12). China currently consumes seven to eight times more industrial metals than the US (Chart 13). As such, even if the US infrastructure investment plan will be approved later this year, it is unlikely to be a game changer for global commodity prices or Chinese exports. Chart 12Infrastructure Spending, China Vs. The US

From Deflation To Inflation … What’s Next?

From Deflation To Inflation … What’s Next?

Chart 13US Consumption Of Industrial Metals Is Too Small Relative To China

From Deflation To Inflation … What’s Next?

From Deflation To Inflation … What’s Next?

The proposed US$1.2 trillion spending on the US nation’s roads, bridges, green spaces, water, electricity, and universal broadband will be spread over the next eight years. The additional $150 billion per annum to the US public infrastructure investment will only boost the US spending from 24% to about 32% of China’s annual infrastructure investment. Furthermore, the fiscal multiplier effect from the extra public spending on investment from the US private sector and overall economy may not be as positive as the market has priced in, depending on the size of corporate tax hikes in the final bill. Bottom Line: After a pandemic-driven boost in 2020, growth in US imports from China will likely moderate in the second half of 2021 and into 2022. The proposed infrastructure spending plan in the US will benefit Chinese exports, but the magnitude of the windfall may be disappointing. Investment Implications As discussed in a previous report, rising US bond yields will have a muted effect on their Chinese counterparts. Tightened regulations on the real estate industry and a new round of environmental protection laws in China will continue to suppress the domestic credit demand. As a result, interest rate differentials between China and the US will continue to narrow. The strength in the USD has not run its course and the RMB will face slight depreciation pressures in Q2 and possibly into Q3. A declining RMB will provide reflationary benefits to China’s industrial profits, but with about a six-month time lag. In the meantime, we recommend global investors to continue underweighting Chinese stocks (Chart 14A and 14B). Chart 14AContinue Underweighting Chinese Stocks

Continue Underweighting Chinese Stocks

Continue Underweighting Chinese Stocks

Chart 14BContinue Underweighting Chinese Stocks

Continue Underweighting Chinese Stocks

Continue Underweighting Chinese Stocks

Jing Sima China Strategist jings@bcaresearch.com Footnotes 1According to the OECD, recent US stimulus will boost US GDP growth by almost 3 percentage points in the first full year (from 2021Q2 to 2022Q2). The knock-on effect from the stimulus on other economies is projected to be significant, including a half percentage point addition to China’s GDP during the same period. 2The Congressional Budget Office estimated that combined federal, state and local spending on infrastructure was (in 2019 dollars) $441 billion as of 2017. Cyclical Investment Stance Equity Sector Recommendations

Highlights Global Inflation: The case for maintaining a strategic overall allocation to inflation-linked bonds (ILBs) versus nominal government debt in dedicated global fixed income portfolios remains intact. Global growth expectations are accelerating as vaccinations increase, spare capacity is increasingly being absorbed across the developed world and central banks (led by the Federal Reserve) continue to show no inclination to tighten policy anytime soon. Inflation-Linked Bond Allocations: ILB valuations, however, are no longer uniformly cheap across all countries. Real yields are now moving in a less coordinated fashion as markets try to sort out the timing and pace of eventual future central bank tightening. We recommend shifting inflation-linked bond exposure from Canada to Germany, as both markets have similar valuations but the Bank of Canada is likely to turn less dovish well ahead of the ECB. Feature Chart of the WeekMarkets Remain Unconcerned About An Inflation Overshoot

Markets Remain Unconcerned About An Inflation Overshoot

Markets Remain Unconcerned About An Inflation Overshoot

The global reflation trade over the past year has been highly rewarding to investors. Equity and credit markets worldwide have delivered outstanding returns on the back of highly stimulative monetary and fiscal policies implemented to deal with the negative economic effects of COVID-19. The global INflation trade has also paid off for investors in inflation-linked bonds (ILBs), which have outperformed nominal government debt across the developed economies dating back to last spring. The rising trend for global inflation breakevens remains intact, but is approaching some potential resistance points. A GDP-weighted average of 10-year breakeven inflation rates among the major developed economies is just shy of the 2% level that has represented a firm ceiling over the past decade (Chart of the Week). At the same time, the Bloomberg consensus forecast for headline CPI inflation for that same group of countries calls for an increase to only 1.8% by year-end before slowing to 1.7% in 2022. The latest forecasts from the IMF are similar, calling for headline inflation in the advanced economies to reach 1.6% in 2021 and 1.7% in 2022. If those modest forecasts for realized inflation come to fruition, then there is likely not much more upside in inflation breakevens, in aggregate. Country selection within the ILB universe will become more important over the next 6-12 months, as divergences in growth, realized inflation and central bank reactions will lead to a more heterogeneous path for global inflation breakevens. Underlying Inflation Backdrop Still Supports Rising Breakevens On a total return basis, ILBs enjoyed an extended run of success prior to this year. The cumulative total return of the asset class (in local currency terms) between 2012 and 2020 was a whopping 61% in the UK, 25% in Canada, 22% in the US and 21% in the euro area (aggregating the individual countries in the region with inflation-linked bonds). However, the absolute performance of ILBs has been more disperse on a country-by-country basis so far in 2021. ILBs are down year-to-date in Canada (-6.2%), the UK (-5.0%) and the US (-1.4%). On the other hand, euro area ILBs have delivered a positive total return of +0.5% so far in 2021. Real bond yields have climbed off the lows in the US, UK and, most notably, Canada where the overall index yield on the Bloomberg Barclays inflation-linked bond index is now in positive territory for the first time since before the pandemic started (Chart 2). At the same time, real bond yields have been drifting lower in the euro area. These real yield moves are related to shifting perceptions of central bank responses to the global growth upturn. For example, pricing in overnight index swap (OIS) curves have pulled forward the timing and pace of future interest rate increases in the US and Canada – i.e. real policy rates will become less negative - while there has been comparatively little change in euro zone rate expectations. While the absolute returns for ILBs have become less correlated, the relative trade between nominal and inflation-linked government bonds in all countries remains intact. 10-year breakeven inflation rates have been steadily climbing in the US and UK, while depressed Japanese breakevens have crept modestly higher (Chart 3). Even Europe, where inflation has remained subdued for years, has seen a significant shift higher in inflation breakevens. (Chart 4). The turn in breakevens has occurred alongside a major change in investor perceptions of future inflation, with surveys like the ZEW showing an overwhelming majority of financial professionals expecting higher inflation in the US, Europe and the UK. Chart 2A Fading Bull Market In Inflation-Linked Bonds

A Fading Bull Market In Inflation-Linked Bonds

A Fading Bull Market In Inflation-Linked Bonds

Chart 3A Solid Recovery In Inflation Expectations

A Solid Recovery In Inflation Expectations

A Solid Recovery In Inflation Expectations

Chart 4European Inflation Expectations Starting To Normalize

European Inflation Expectations Starting To Normalize

European Inflation Expectations Starting To Normalize

Inflation forecasts have shifted in response to faster global growth expectations on the back of vaccine optimism and aggressive US fiscal stimulus. Yet inflation forecasts remain modest compared to the huge growth figures expected for 2021 and 2022. In its latest World Economic Outlook published last week, the IMF upgraded its global real GDP forecast to 6.0% for 2021 and 4.4% for 2022. This represented an increase of 0.5 and 0.4 percentage points, respectively, from the last set of forecasts published back in January. While growth upgrades occurred across all major developed and emerging economies, the biggest upgrades came in the US and Canada, for both 2021 and 2022. As a result, the IMF projects the output gap in both countries to turn positive over 2022 and 2023, and be nearly closed in core Europe, Australia and Japan (Chart 5). The IMF is not projecting a major inflation surge on the back of those upbeat growth forecasts, though. While headline inflation in the US is expected to climb to 2.3% in 2021 and 2.4% in 2022, the same measure in Canada is only projected to rise to 1.7% and 2.0% over the same two years. European inflation is expected to remain subdued, reaching only 1.4% this year and drifting back to 1.2% in 2022 despite real GDP growth averaging 4.1% over the two-year period. The IMF attributes the benign inflation outcomes, even in the face of booming growth rates and the rapid elimination of output gaps, to the structural disinflationary backdrop for so-called “non-cyclical” inflation (Chart 6). The IMF defines this as the components of inflation indices that are less sensitive to changes in aggregate demand. The IMF estimates show that the contribution from non-cyclical components to overall inflation in the advanced economies had fallen to essentially zero at the end of 2020. Chart 5A Big Expected Narrowing Of Output Gaps

How Much More Juice Is Left In The Global Inflation Breakeven Trade?

How Much More Juice Is Left In The Global Inflation Breakeven Trade?

Chart 6Non-Cyclical Components Still Weighing On Global Inflation

Non-Cyclical Components Still Weighing On Global Inflation

Non-Cyclical Components Still Weighing On Global Inflation

There is considerable upside risk for the more cyclical components of inflation that could result in inflation overshooting the IMF projections (Chart 7). Chart 7Cyclical Backdrop Is Inflationary

Cyclical Backdrop Is Inflationary

Cyclical Backdrop Is Inflationary

For example, in the US, the Prices Paid component of the ISM Manufacturing index remains elevated at post-2008 highs, while the year-over-year change in the Producer Price Index soared to 6% in March. Across the Atlantic, the European Commission business and consumer surveys have shown a big surge in the net balance of respondents expecting higher inflation in manufacturing and retail trade. Previous weakness in the US dollar and surging commodity prices are playing a major role in this rapid pick-up in price pressures seen in many countries. Given the current backdrop of strong global growth expectations, with actual activity accelerating as vaccinations increase and more parts of the global economy reopen, inflation pressures are unlikely to fade in the near term. With realized inflation rates set to spike due to base effect comparisons to the pandemic-fueled collapse one year ago, the upward pressure on global ILB inflation breakevens will persist in the coming months – especially with breakevens still below levels that would prompt central banks to turn less dovish sooner than expected. Bottom Line: The case for maintaining a strategic overall allocation to inflation-linked bonds (ILBs) versus nominal government debt in dedicated global fixed income portfolios remains intact. Global growth expectations are accelerating as vaccinations increase, spare capacity is increasingly being absorbed across the developed world and central banks (led by the Federal Reserve) continue to show no inclination to tighten policy anytime soon. Assessing Value In Developed Market Inflation-Linked Bonds Chart 8USD Outlook Now More Mixed

USD Outlook Now More Mixed

USD Outlook Now More Mixed

Although the current backdrop remains conducive to a continuation of the rising trend in global ILB breakevens, there are factors that could begin to slow the upward momentum. The future path of the US dollar is now a bit less certain (Chart 8). While the DXY index is still down 7.4% compared to a year ago, it is up 2.4% so far in 2021. Shorter-term real interest rate differentials between the US and the other major developed markets remain dollar-bearish. At the same time, longer-term real yield differentials have risen in favor of the US (middle panel). Furthermore, US growth is outperforming other developed economies, typically a dollar-bullish factor (bottom panel). Given the usual negative correlation between the US dollar and commodity prices, a loss of downside dollar momentum could also slow the pace of commodity price appreciation. This represents a risk to additional global ILB outperformance versus government bonds. Our GDP-weighted aggregate of 10-year ILB breakevens for the major developed economies is currently just under 2% - levels more consistent with oil prices over $80/bbl than the current price closer to $60/bbl (Chart 9). Chart 9Breakevens Consistent With Much Higher Oil Prices

Breakevens Consistent With Much Higher Oil Prices

Breakevens Consistent With Much Higher Oil Prices

Given some of these uncertainties over the strength of any future inflationary push from a weaker US dollar and rising commodity prices, a broad overweight allocation to ILBs across the entire developed market universe may no longer generate the same strong returns versus nominal government bonds seen over the past year. With the “easy money” already having been made in the global breakeven widening trade, country allocation within the ILB universe has now become a more important dimension for bond investors to consider. To assess the relative attractiveness of individual ILB markets, we turn to a few valuation tools. Our regression-based valuation models for 10-year ILB breakevens in the US, UK, France, Italy, Germany, Japan, Canada and Australia are all presented in the Appendix on pages 14-17. The two inputs into the model are the annual rate of change of the Brent oil price in local currency terms (as a measure of shorter-term inflation pressure) and a five-year moving average of realized headline CPI inflation (as a longer-term trend that provides a structural “anchor” for breakevens based off actual inflation outcomes). We first presented these models in April 2020, but we have now made a change in response to some of the unprecedented developments witnessed over the past year.1 Despite the strong visual correlation between the level of oil prices and inflation breakevens in most countries, we chose to use the annual growth of oil prices, rather than the level, in our breakeven models. This is because we found it more logical to compare a rate of change concept like inflation (and breakevens) to the rate of change of oil. However, the oil input into our breakeven models could produce nonsensical results during periods of extreme oil volatility that did not generate equivalent swings in breakeven inflation rates. A good example of that occurred in 2016, when the annual rate of change of the Brent oil price briefly surged toward 100%, yet 10-year US TIPS breakevens did not rise above 2% (Chart 10). An even bigger swing in oil prices has occurred over the past year, with oil prices up over +200% compared to the collapse in prices that occurred one year ago. Putting such an extreme move into our US model would have pushed the “fair value” level of the 10-year TIPS breakeven to 4% - an implausible outcome given that the 10-year breakeven has never risen to even as high as 3% in the entire 24-year history of the TIPS market. Chart 10Pass-Through Of Extreme Oil Moves Has Limits

Pass-Through Of Extreme Oil Moves Has Limits

Pass-Through Of Extreme Oil Moves Has Limits

To deal with this problem, we have truncated the rate of change of oil prices in all our breakeven models at levels consistent with past peaks of breakevens. Going back to the US example, we have “capped” the rate of change of the Brent oil price at +40%, as past periods when oil price momentum was greater than 40% did not translate into any additional increase in TIPS breakevens. We then re-estimated the model using this truncated oil price series to generate fair value breakeven levels. Chart 11A Mixed Impact Of USD Moves On Non-US Breakevens

A Mixed Impact Of USD Moves On Non-US Breakevens

A Mixed Impact Of USD Moves On Non-US Breakevens

We did this for all eight of our individual country breakeven models and in all cases, truncating extreme oil moves improved the accuracy of the model. Interestingly, we did not truncate the downside momentum of oil prices, as there was no obvious “cut-off” point where periods of collapsing oil prices did not generate equivalent declines in breakevens. Oil prices remain the most critical short-term variable to determine ILB breakeven valuation. While it is intuitive to think that currency movements should also have a meaningful impact on inflation (both realized and expected), the effect is not consistent across countries. For example, euro area breakevens appear to be positively correlated to the euro, while Japanese breakevens rarely rise without yen weakness (Chart 11). One other factor to consider when evaluating the value of breakevens is the possible existence of an inflation risk premium component during periods of higher uncertainty over future inflation. Such uncertainty could result in increased demand for ILBs from investors driving up the price of ILBs (thus lowering the real yield) relative to nominal yielding bonds, leading to wider breakevens that do not necessarily reflect a true rise in expected inflation. A simple way to measure such an inflation risk premium is to compare market-based breakevens to survey-based measures of inflation forecasts taken from sources like the Philadelphia Fed's Survey of Professional Forecasters and the Bank of Canada’s Survey Of Consumer Expectations. The assumption here is that the survey-based measures represent a more accurate (or, at least, less biased) depiction of underlying inflation expectations in an economy. We present these simple measures of inflation risk premia, comparing 10-year breakevens to survey-based measures of inflation expectations, in Chart 12 and Chart 13. Breakevens had been trading well below survey-based measures of inflation expectations after the negative pandemic growth shock in 2020 in all countries shown. After the steady climb in global breakevens seen over the past year, those gaps have largely disappeared, with breakevens now trading slightly above survey based inflation expectations in the US, UK and Australia. Chart 12No Major Inflation Risk Premia In These Markets

No Major Inflation Risk Premia In These Markets

No Major Inflation Risk Premia In These Markets

Chart 13Canadian & Australian Breakevens In Line With Inflation Surveys

Canadian & Australian Breakevens In Line With Inflation Surveys

Canadian & Australian Breakevens In Line With Inflation Surveys

Chart 14Assessing The Value Of Breakevens

Assessing The Value Of Breakevens

Assessing The Value Of Breakevens