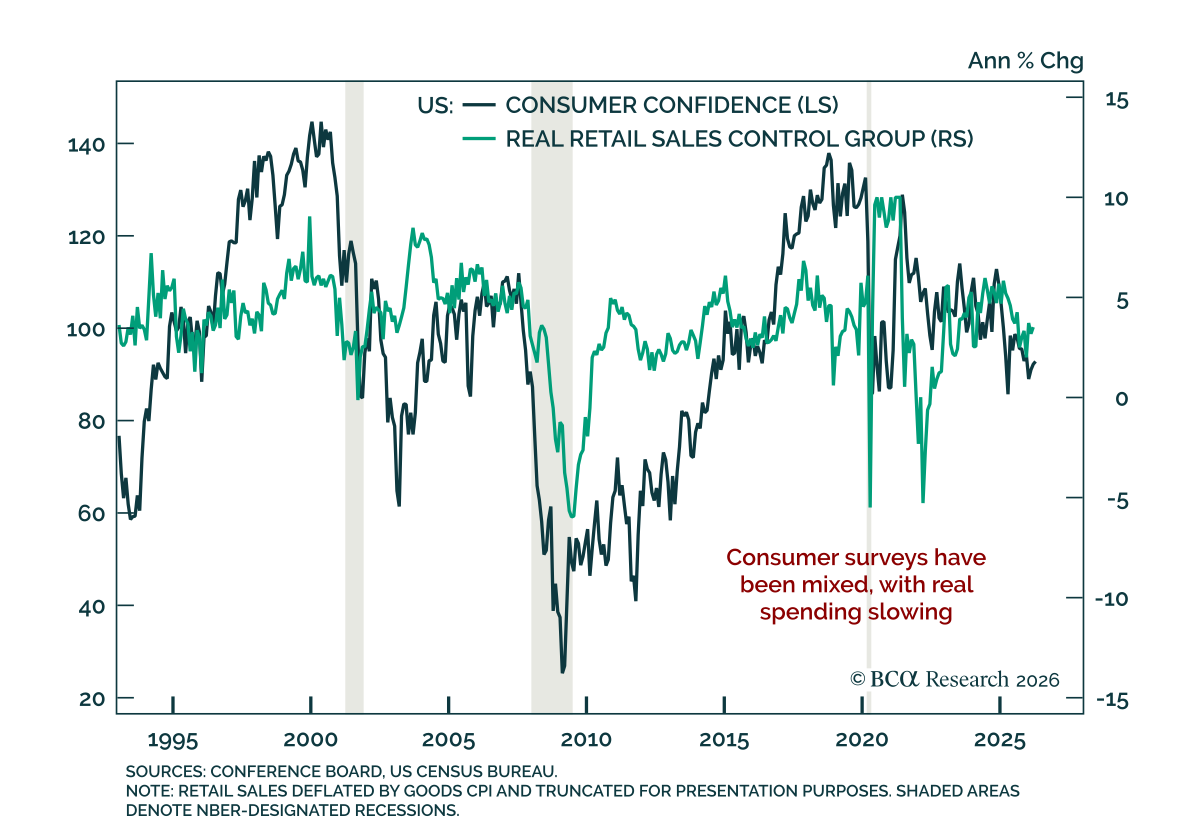

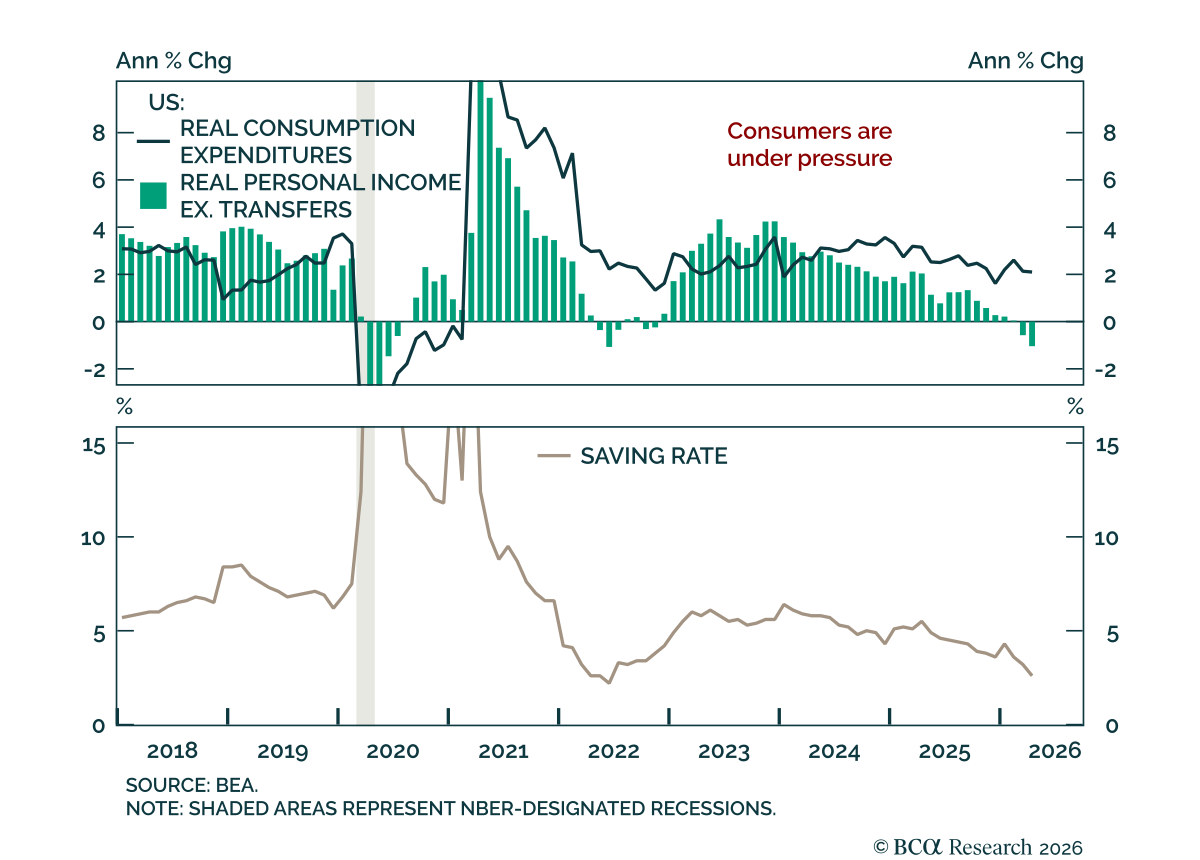

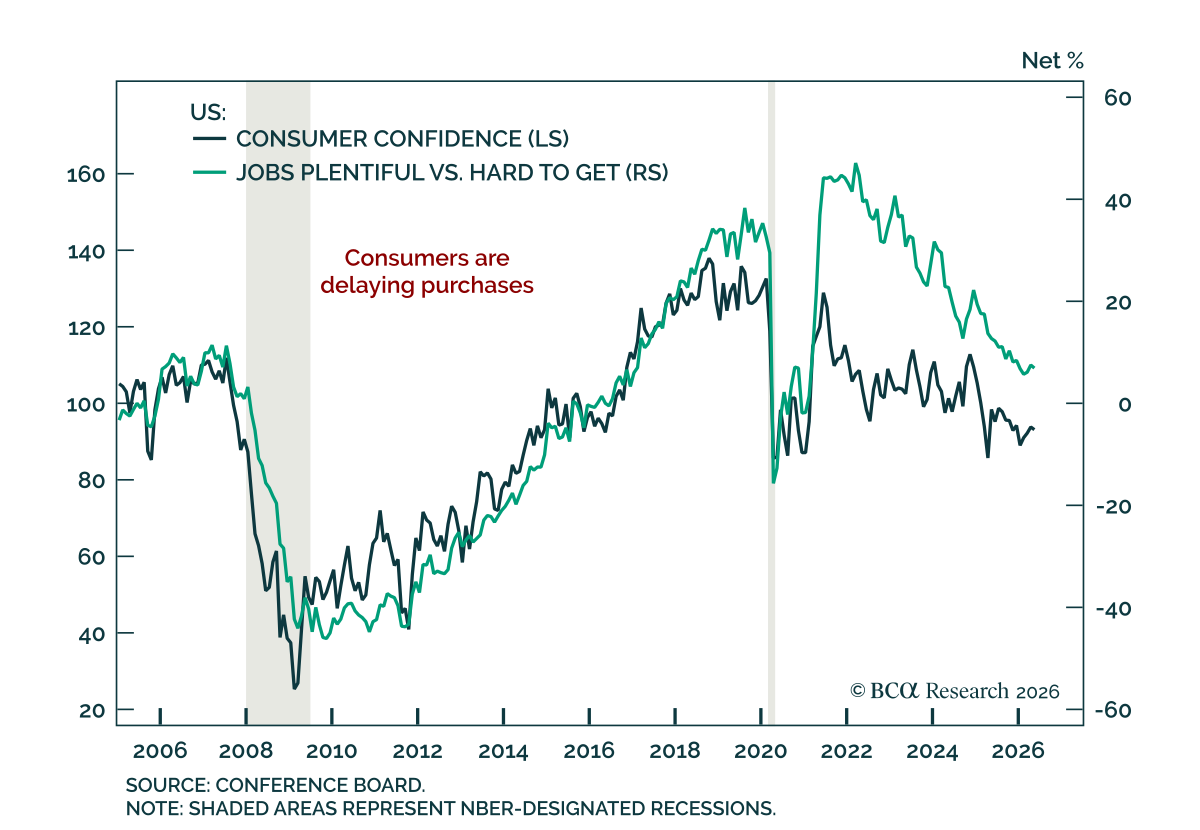

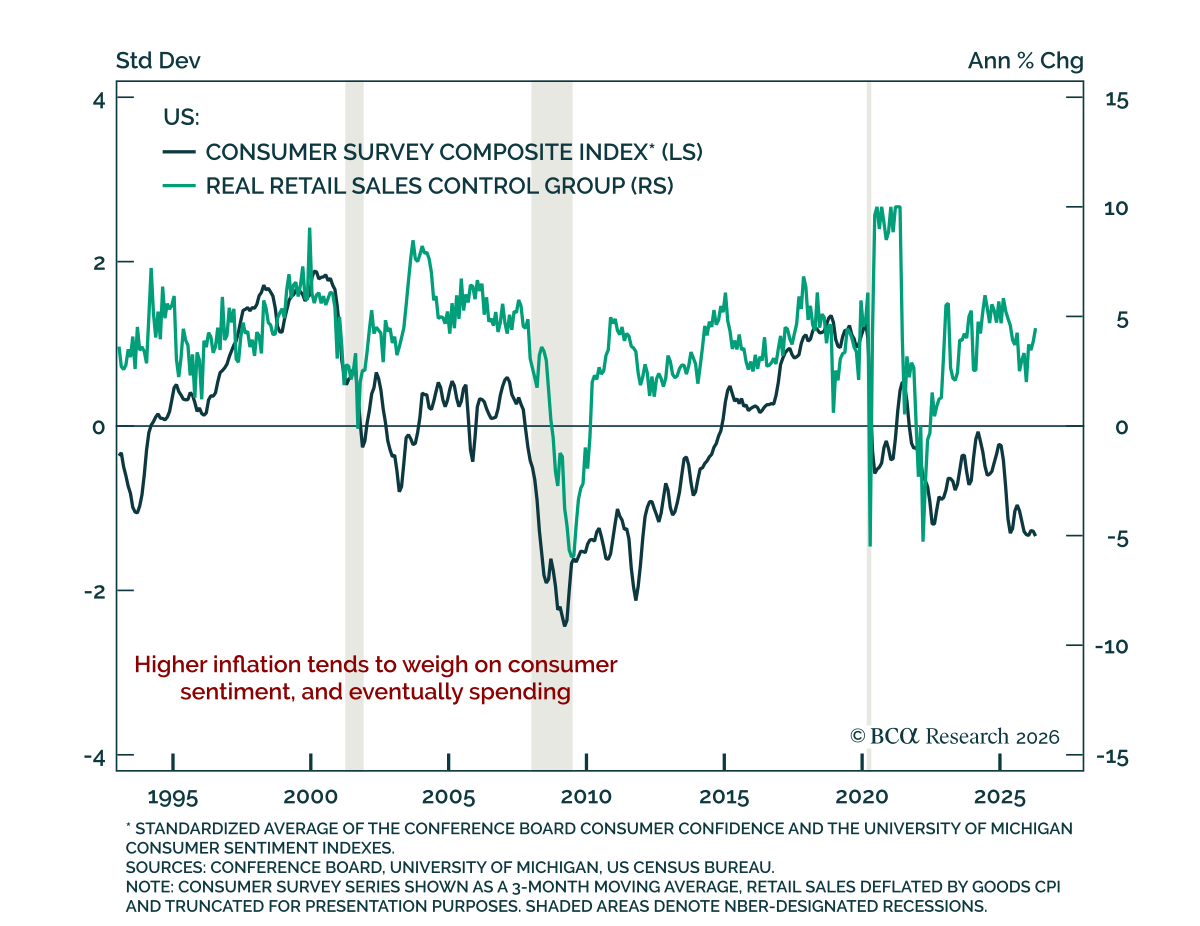

Consumer

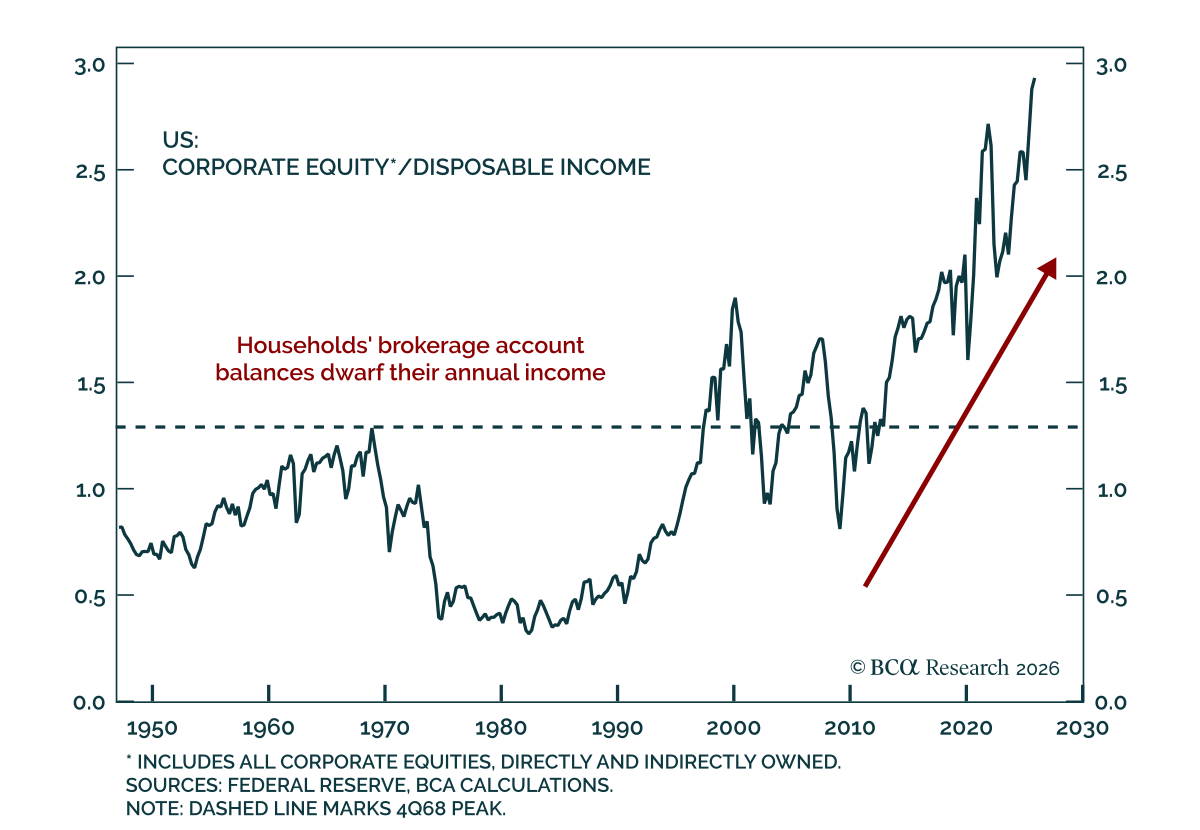

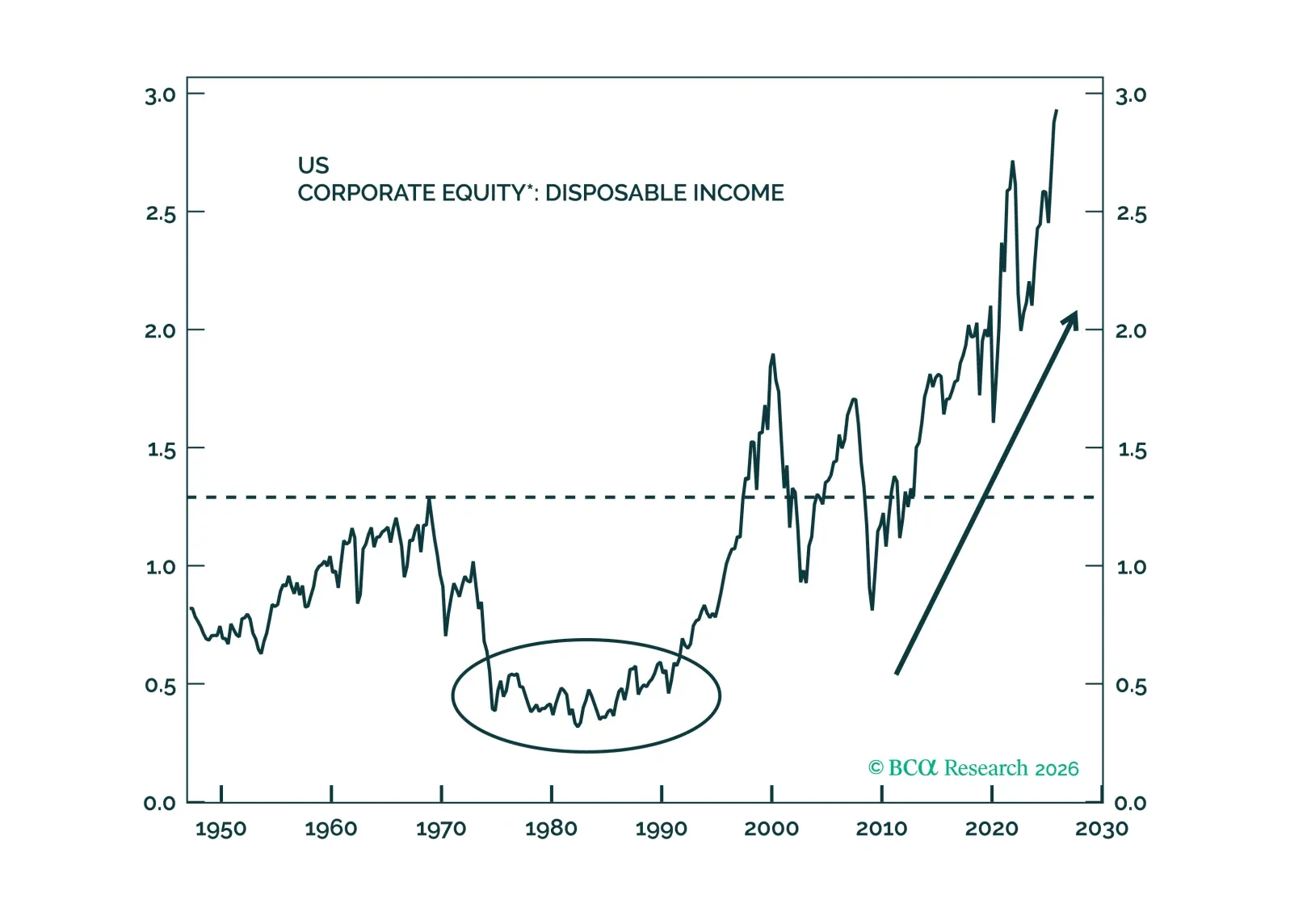

Although the multi-decade surge in the value of households’ equity holdings has made US activity more vulnerable to a stock selloff, the latest income, spending and employment data suggest that consumption growth can carry on at a 2% inflation-adjusted pace.

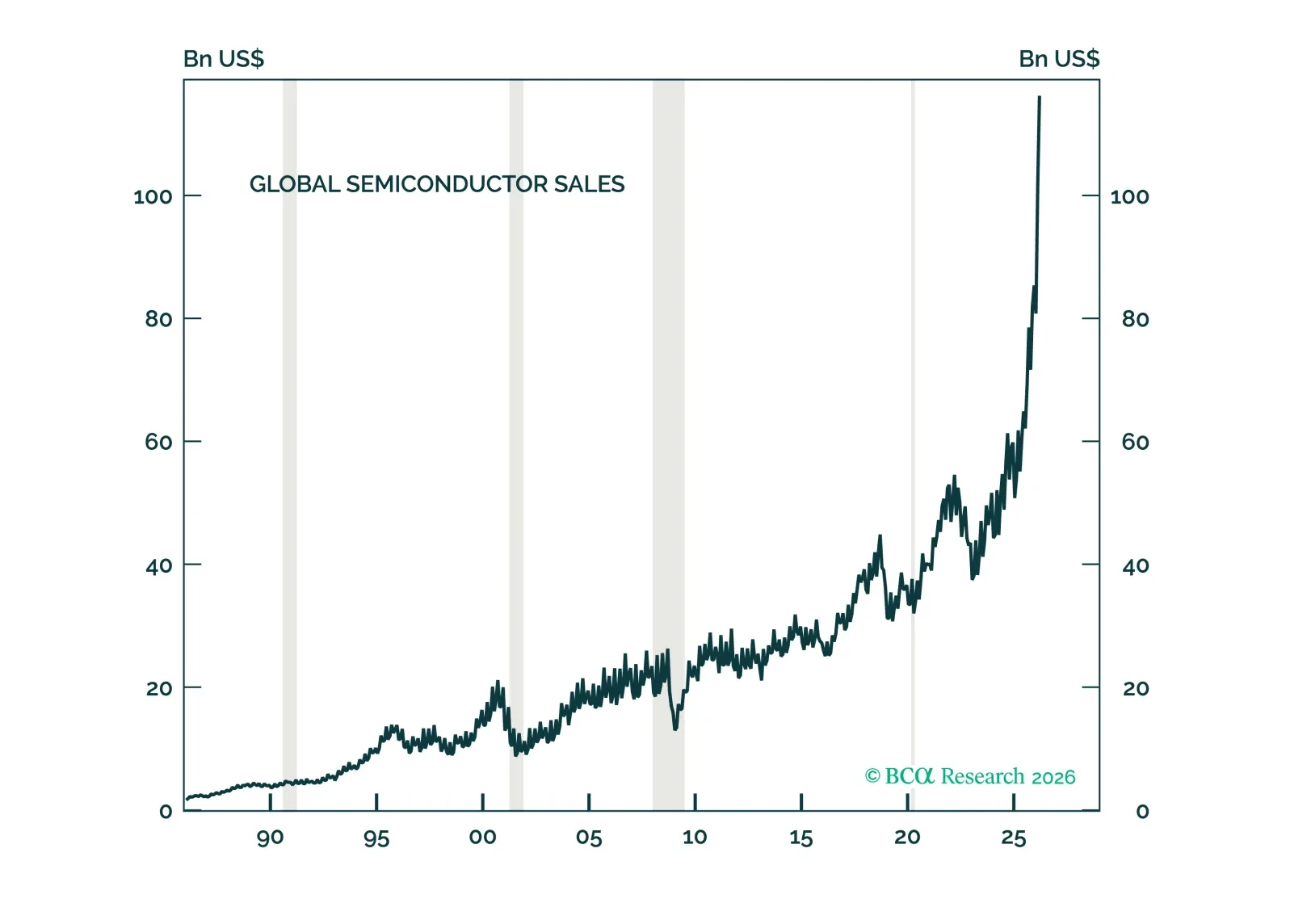

The AI bubble is a different type of bubble. It is primarily an earnings bubble rather than a valuation bubble. Like all bubbles, the AI bubble will burst. For now, however, our AI demand indicators do not suggest that this is imminent.

In Section I, Doug revisits the situation in the Strait of Hormuz and its implications for growth in Europe and the US. In Section II, Jonathan explores whether Kevin Warsh's appointment as Fed Chair signals a return to Greenspan-era, rules-based monetary policy.

The global economy has weathered the oil shock reasonably well so far. However, the risk of a recession will increase meaningfully if the Strait of Hormuz remains closed into June.

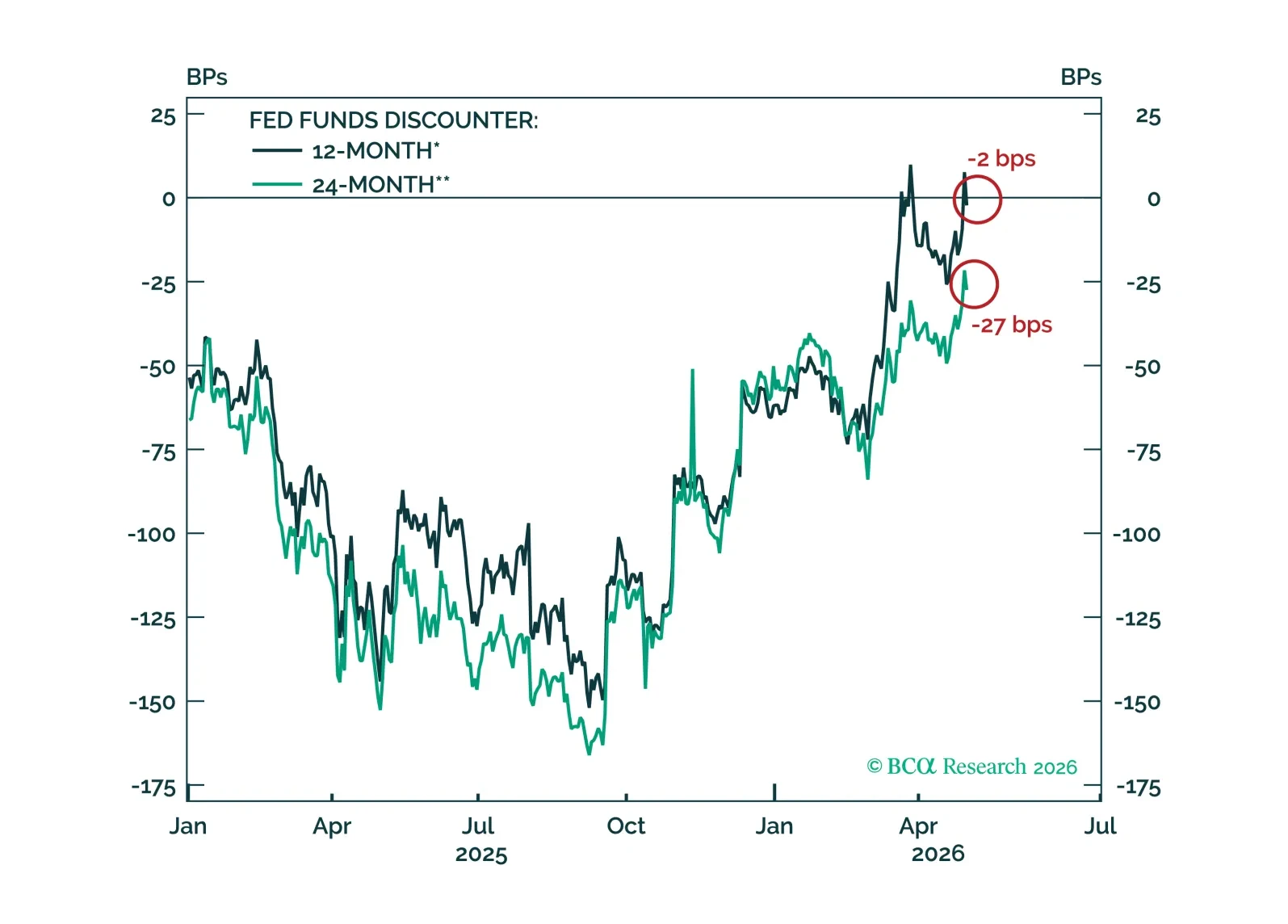

So far, there is no evidence of second-round effects from the oil price shock showing up in the US economy. Fed rate hikes are off the table unless those effects emerge.