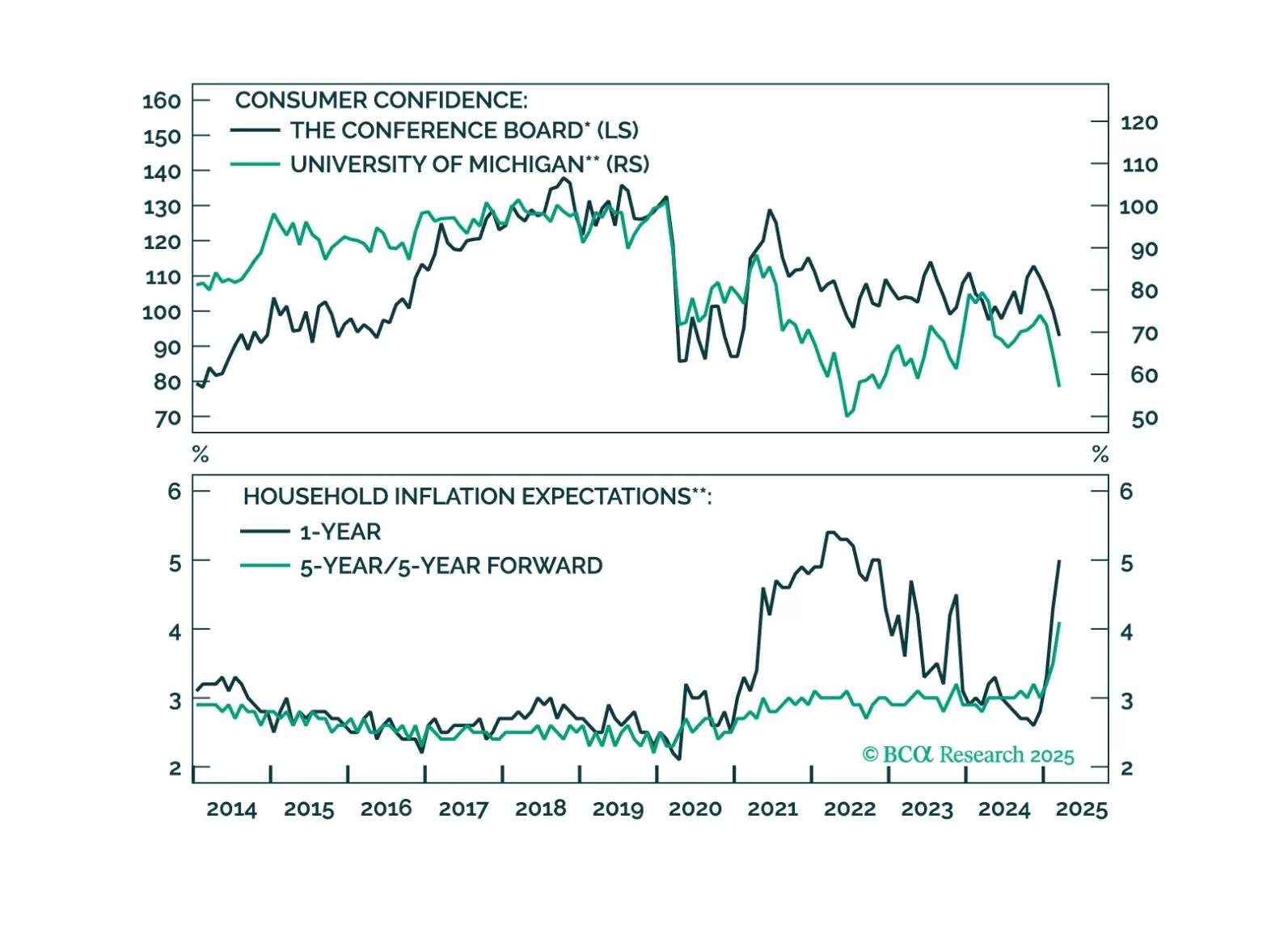

Consumer

We reiterate our defensive global asset allocation, as risk assets face an asymmetric outlook whether growth slows or re-accelerates. The March US jobs report came in stronger than expected, with payrolls rising by 228k. However, the three-month moving…

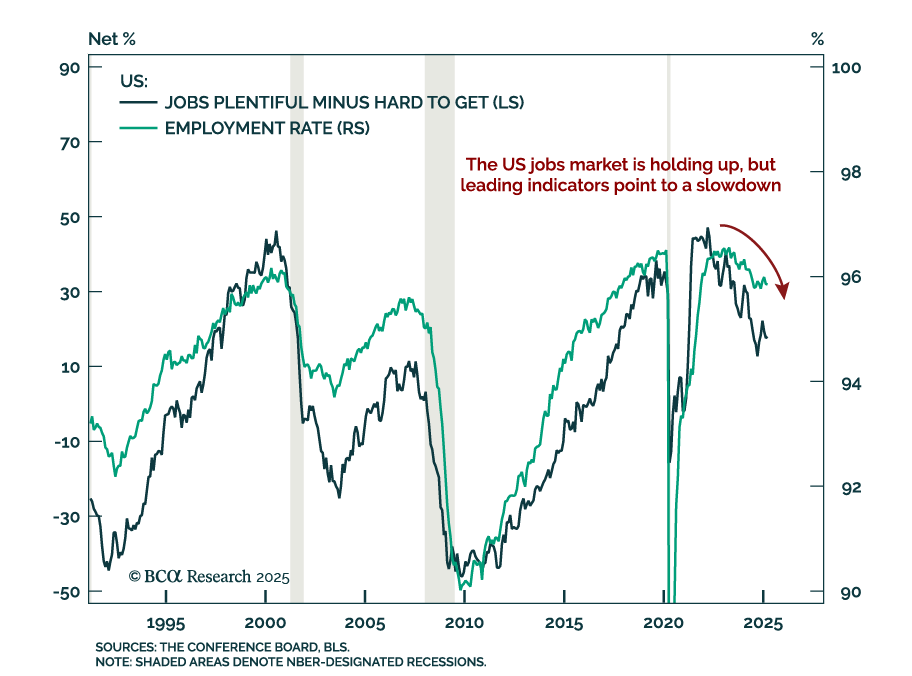

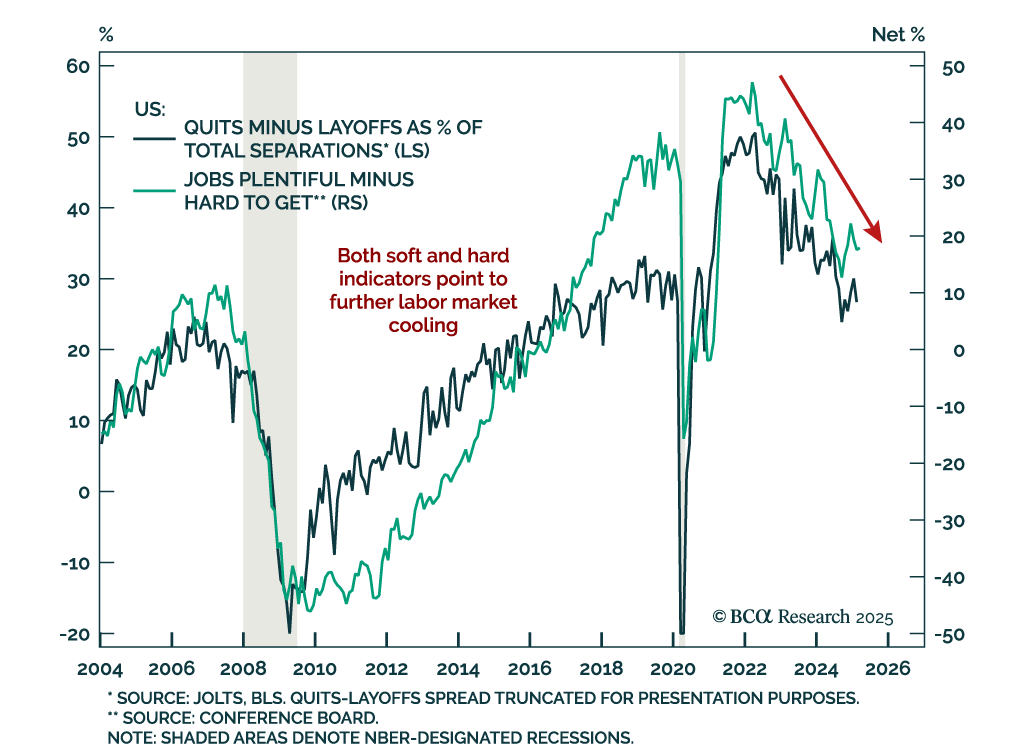

Labor market data continues to cool, reinforcing our overweight in government bonds and above-benchmark duration stance. February job openings fell to 7.6m, below expectations. Declining quits and rising layoffs signal that labor market slack is increasing.…

With economic headwinds building and fiscal dynamics shifting, bond markets are at a turning point. Our latest note outlines why German bund yields are set to decline and why UK gilts are poised to outperform — and how to position accordingly.

February US PCE data adds to the stagflationary tone, reinforcing our overweight duration stance and tactical short in front-end rates. Core PCE inflation rose 0.4% m/m, lifting the year-on-year rate to 2.8%, matching the Fed’s 2025 projection. Headline held…

This morning’s weak consumer spending and strong inflation data reinforce our sense that the US economy is heading toward recession.

In this Second Quarter Strategy Outlook, we explore the major trends that are set to drive financial markets for the rest of 2025 and beyond.

Our US Investment Strategy team recommends investors remain defensively positioned. Stay underweight US equities and overweight Treasuries and cash, on both a tactical and cyclical horizon, as the likelihood of a midyear recession continues to rise. With key…

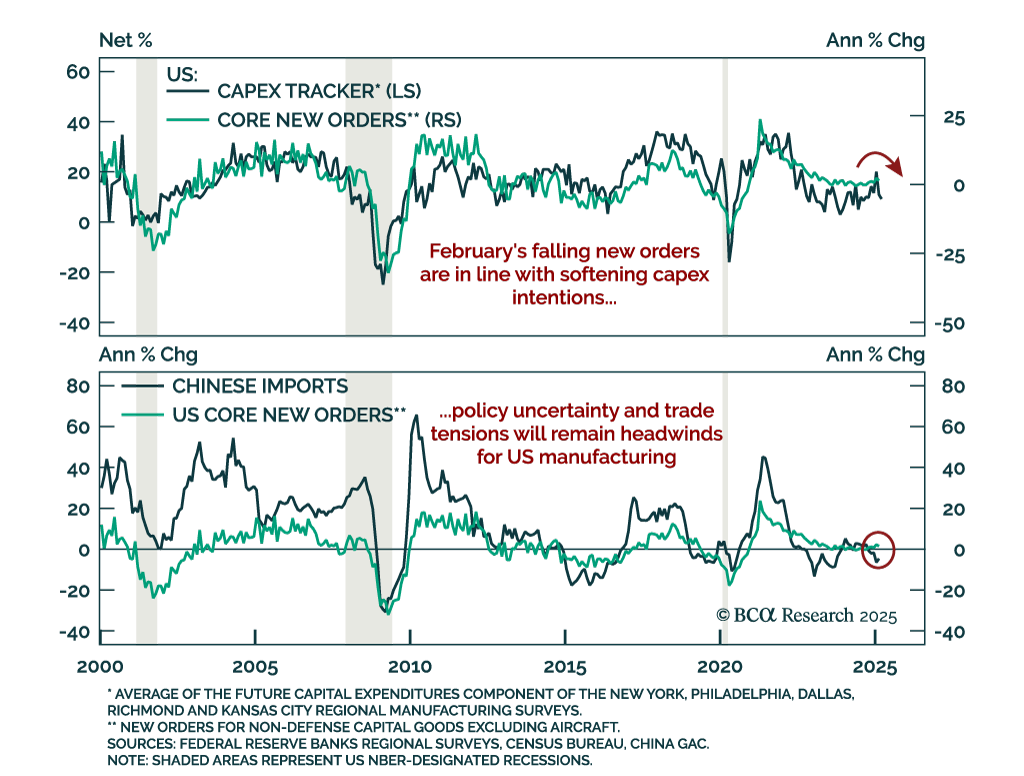

A drop in core capex orders points to slowing business spending and softening global growth. Businesses appear to have front-loaded shipments ahead of potential tariffs while deferring new orders amid policy uncertainty. With hiring and capex plans softening…

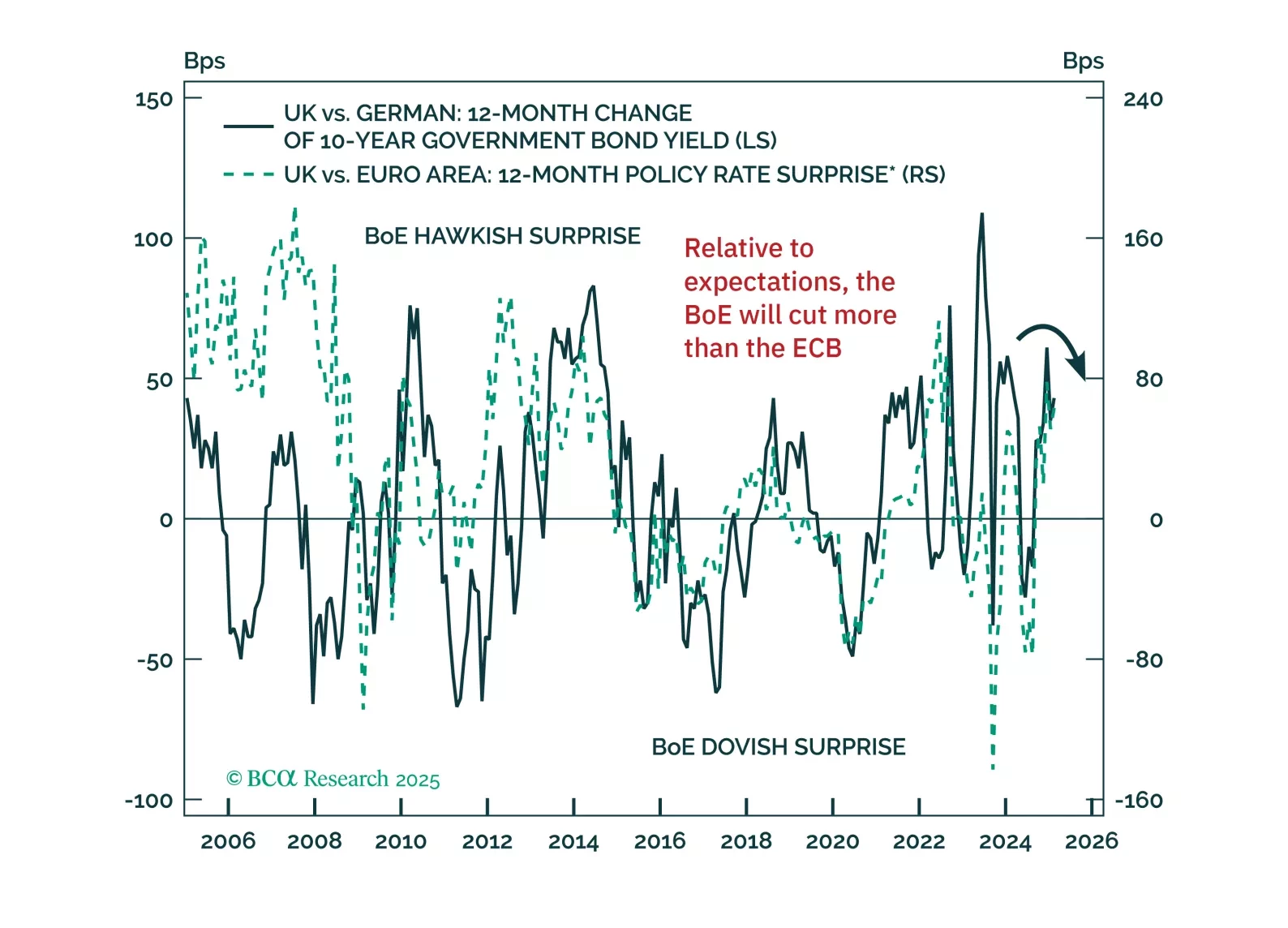

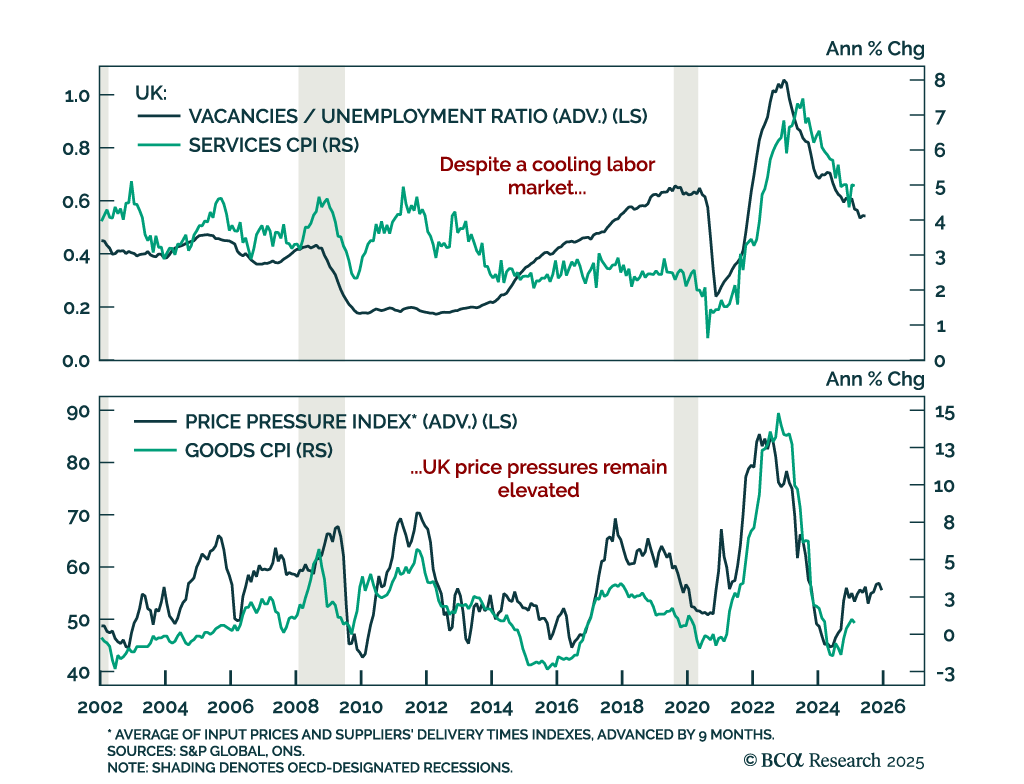

UK inflation came in cooler than expected in February, but lingering price pressures and a still-firm labor market keep the BoE sidelined, for now. Our Global Fixed-Income strategists view the BoE as the most likely DM central bank to surprise on the dovish…

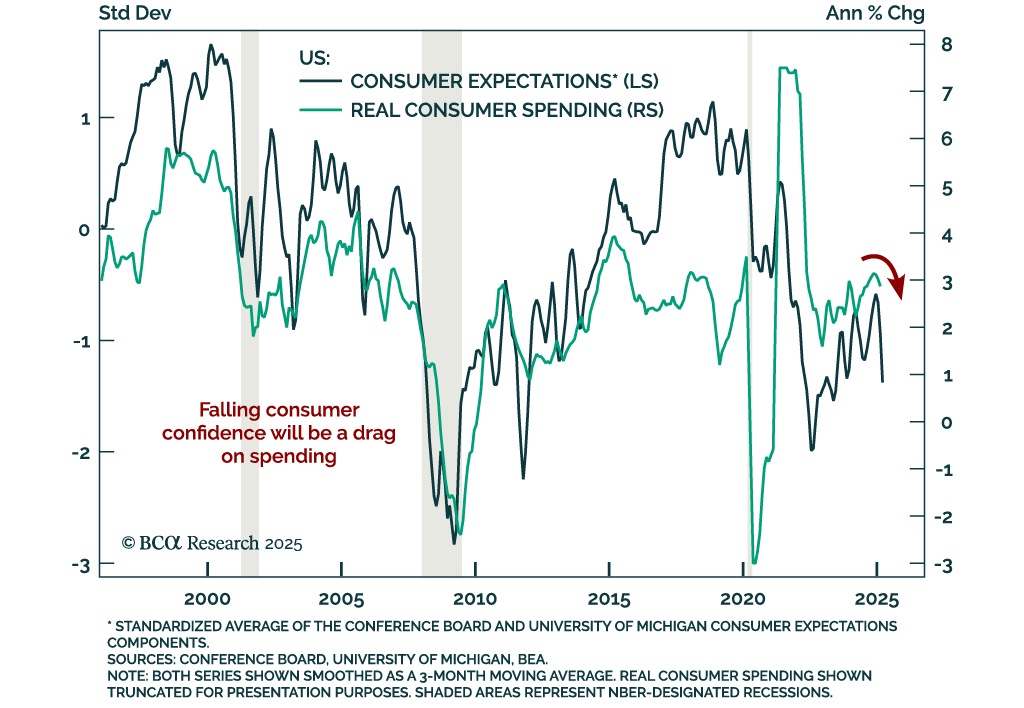

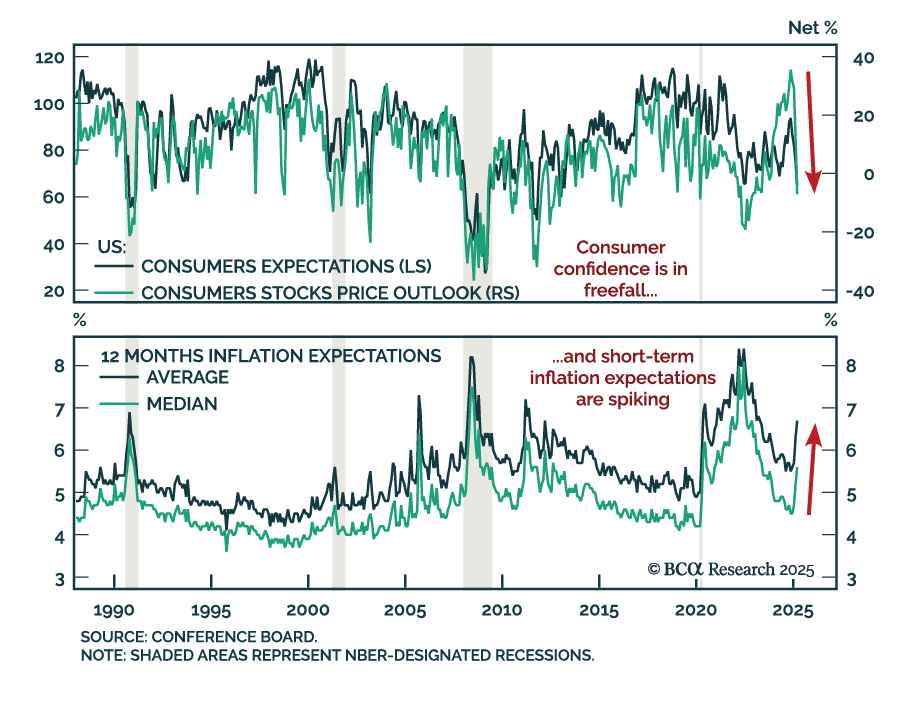

A sharp drop in consumer confidence adds to signs that a consumption slowdown is coming, threatening both US and global growth. Yet rising short-term inflation expectations will keep central banks cautious, weighing on long-term yields even as growth weakens.…