Consumer

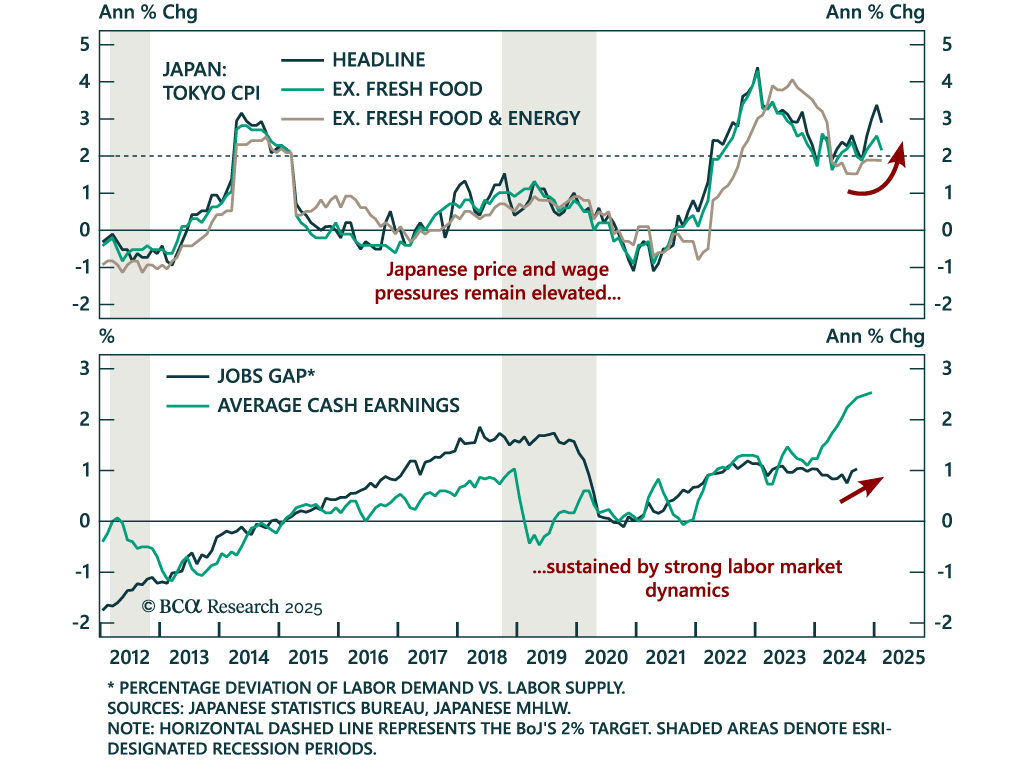

The February Tokyo CPI print came in slightly cooler than expected. Headline inflation moderated to 2.9% y/y from 3.4%, while “core core” was steady at 1.9%. The Tokyo CPI gives an advance reading on national price pressures, and the data suggests…

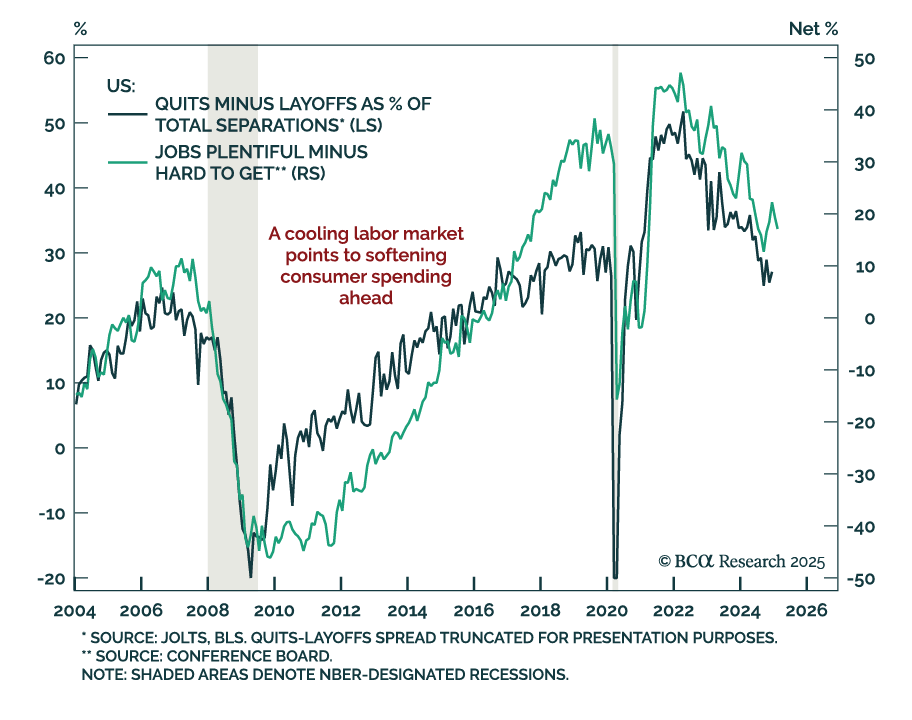

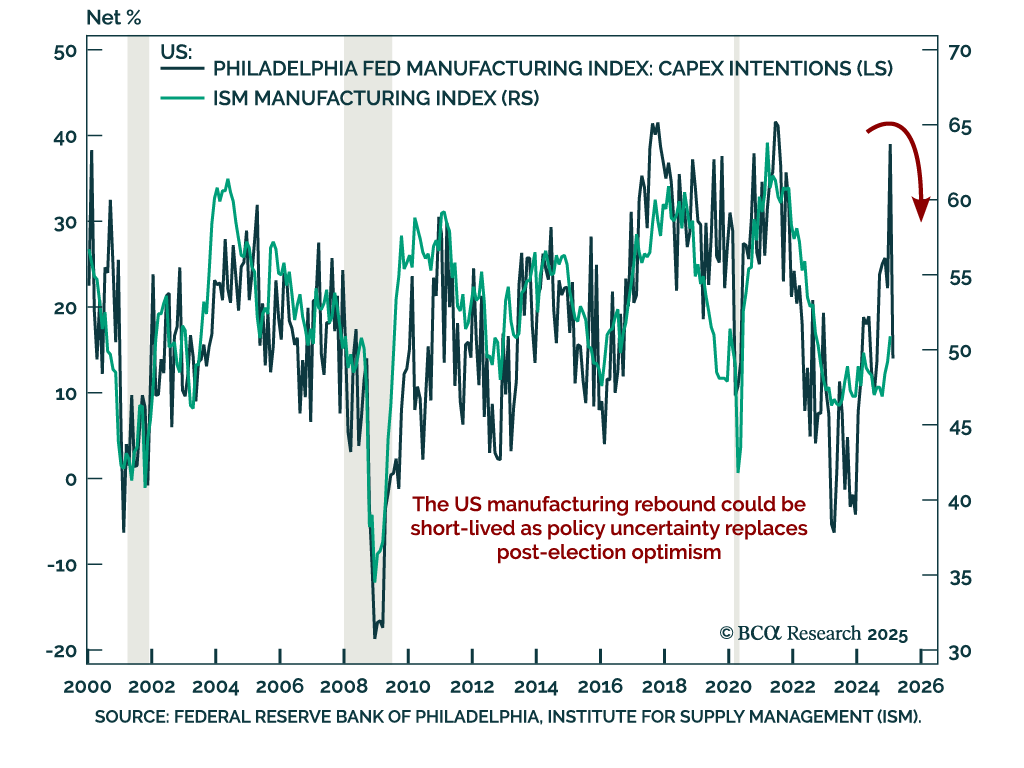

Our Chart Of The Week comes from Juan Correa, from our Global Asset Allocation (GAA) strategy service. Juan highlights weakening US growth observed in the data lately. We have seen a few growth slowdown episodes since 2022. Why is this time…

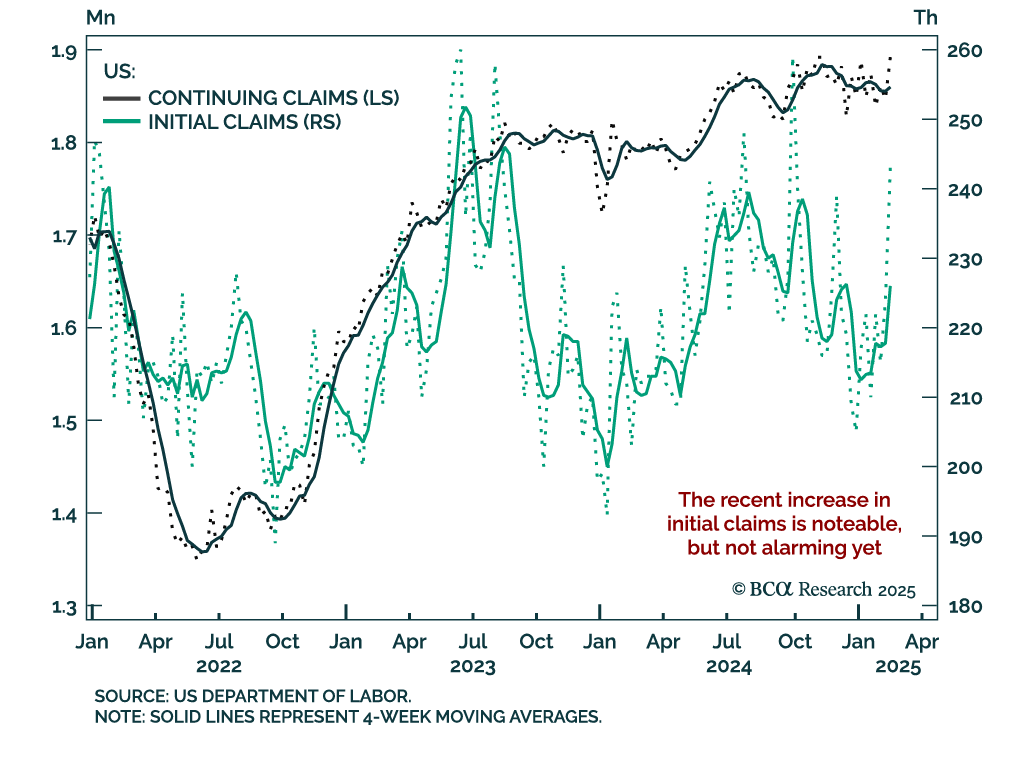

Weekly initial claims ticked up to 242k, near 2024 highs. The data is under the spotlight as the Trump administration implements a reduction of the federal workforce through the DOGE. Initial claims are not alarming yet; they remain near historical lows.…

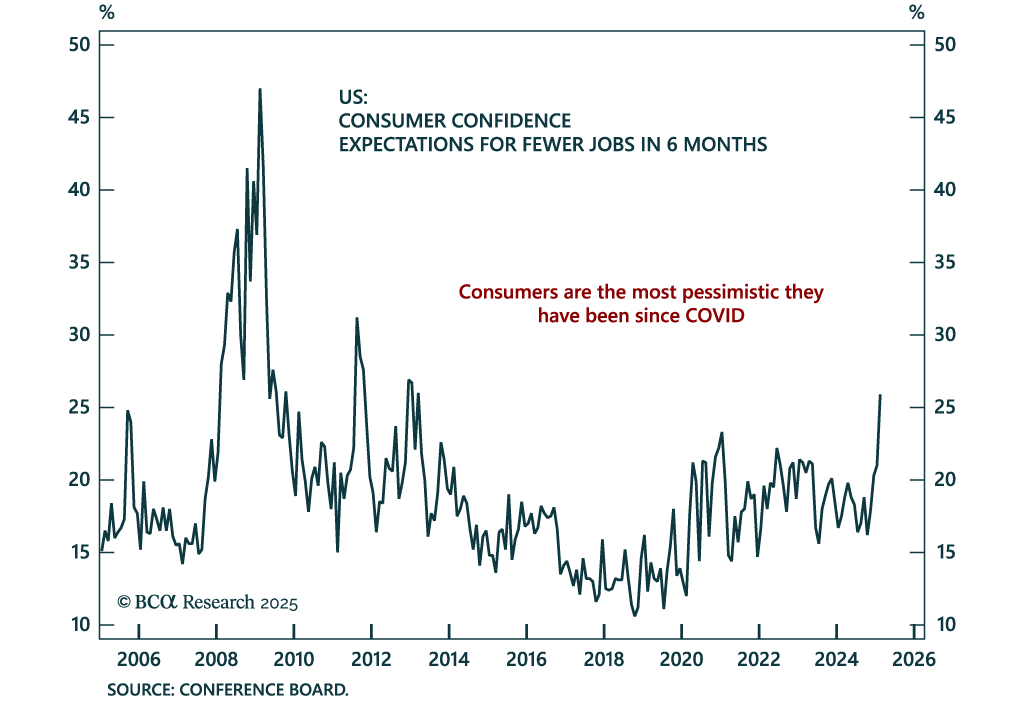

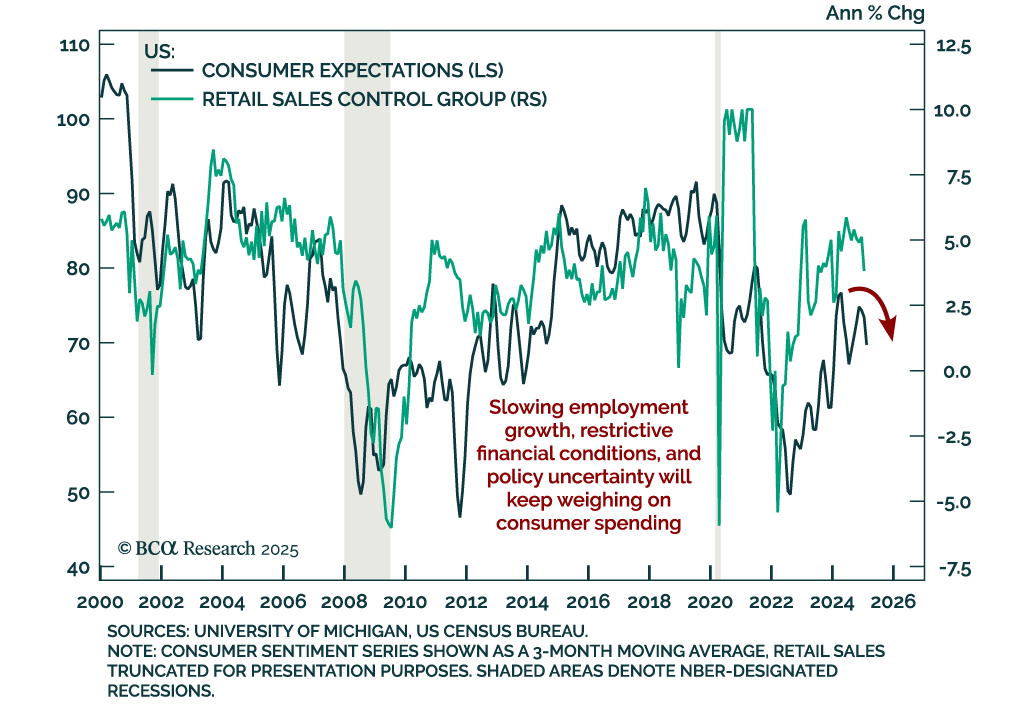

The February Conference Board Consumer Confidence index missed estimates for the third month in a row, falling to 98.3 from 105.3. Consumers’ assessment of both their current situation and their expectations worsened, with the latter falling close to 10…

The February Philadelphia Fed Manufacturing index beat expectations, but retreated to 18.1 from last month’s lofty 44.3 reading. All activity subcomponents pulled back, except for delivery times. The Philly Fed index is volatile even in normal times, and…

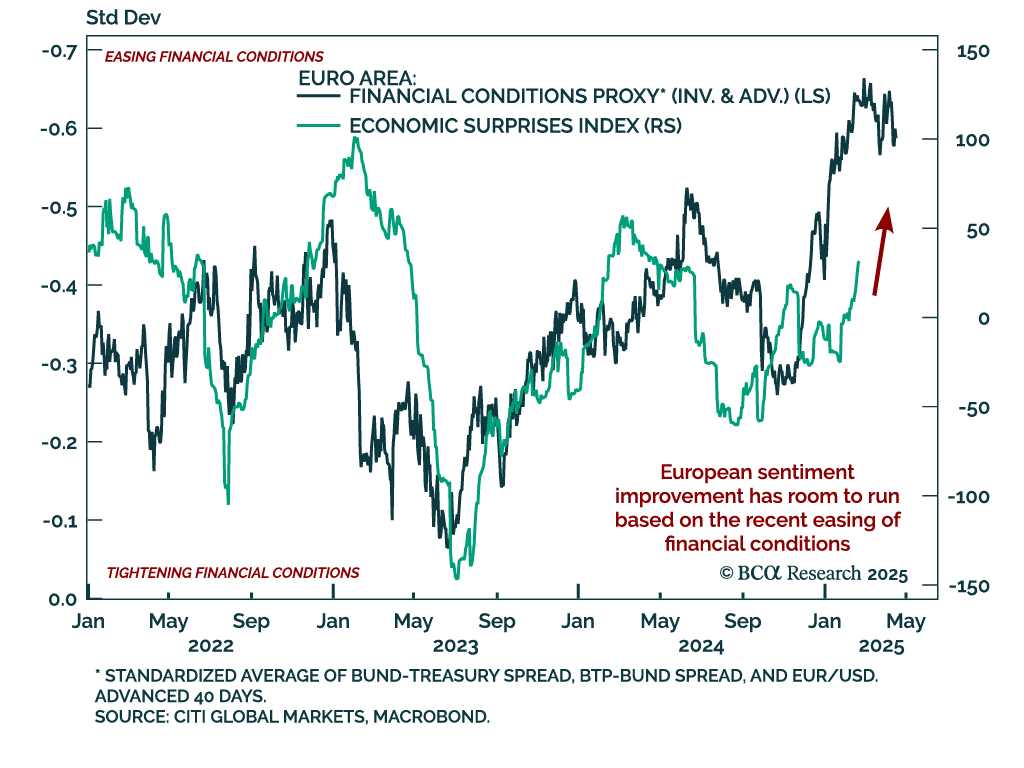

A nascent theme in the latest data is the broad improvement in European sentiment. The February Sentix and ZEW surveys both improved, and flash estimates for European consumer confidence beat estimates, ticking up to -13.6%. Confidence remains low, but…

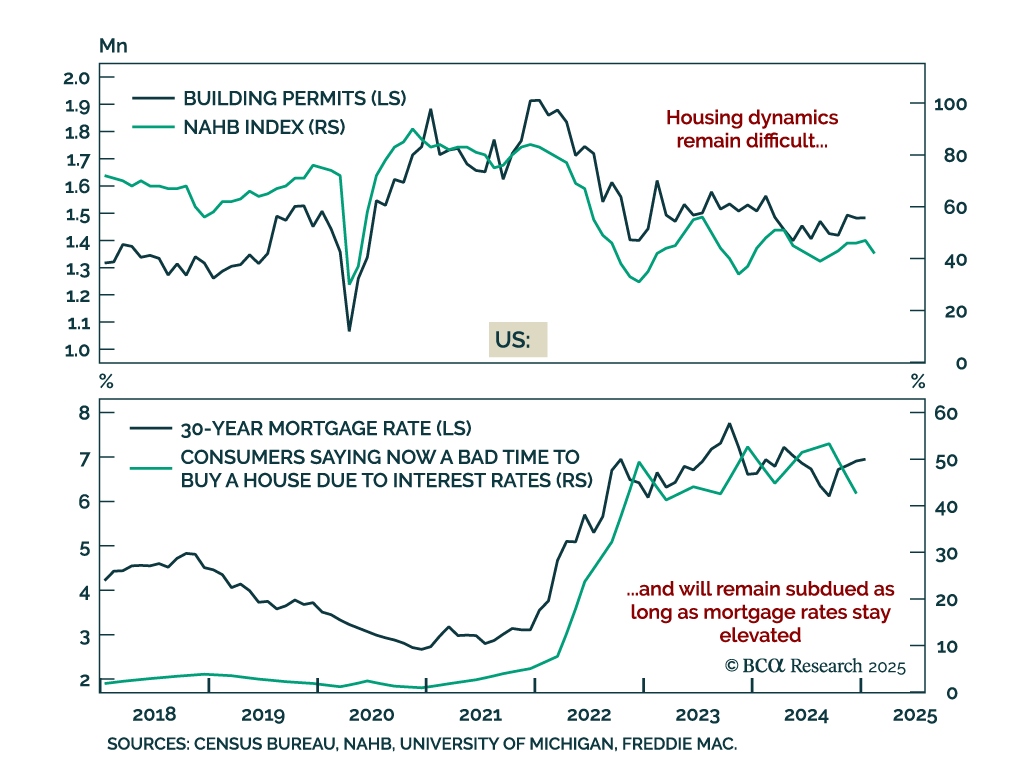

US January housing data disappointed, with housing starts falling 9.8% m/m after expanding 16.1% in December. The February NAHB Housing Market Index also weakened, falling to 42 from 47 in February. Building permits were the one positive surprise, growing…

January US retail sales missed estimates, with the headline number contracting by 0.9% m/m. The decline was broad-based, with spending excluding autos and gas down 0.5%, and the control group also down 0.8%. The retail sales report was impacted by the…

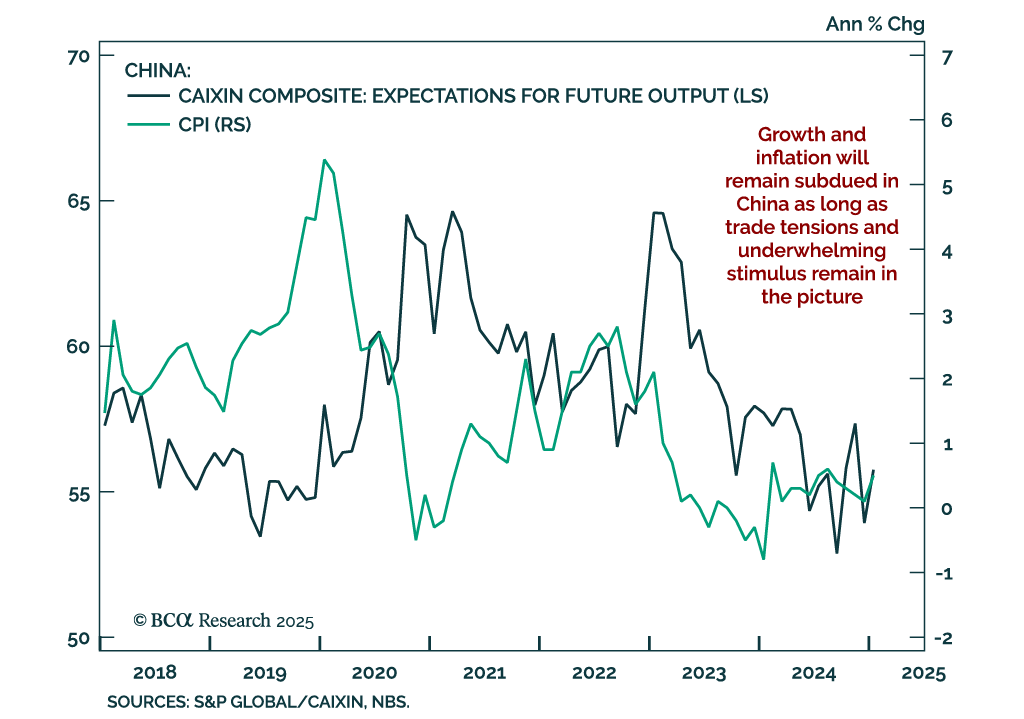

China’s January consumer prices rebounded to 0.5% y/y, and producer price deflation was unchanged at -2.3%. China’s first quarter data tends to be distorted by the Chinese New Year, as its variable dates shift consumption peaks around without a clear pattern.…

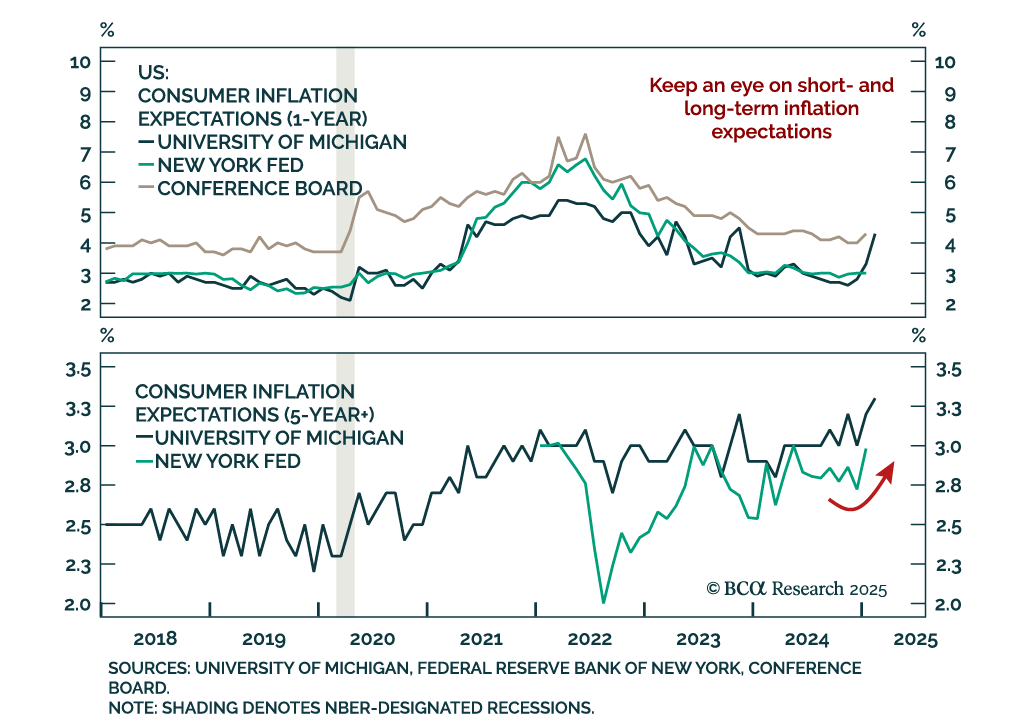

The New York Fed’s Survey of Consumer Expectations’ 1-year and 3-year inflation expectations were unchanged in January. Five-year ahead expectations however increased, as did expectations for staples inflation, while spending expectations…