Consumer

Chinese industrial profits growth accelerated in June, rising from 0.7% y/y to 3.6%. Profits expanded at 3.5% in the first half of 2024, compared to 3.4% in the first half of 2023, and suggest that China’s manufacturing sector remains resilient. A slower…

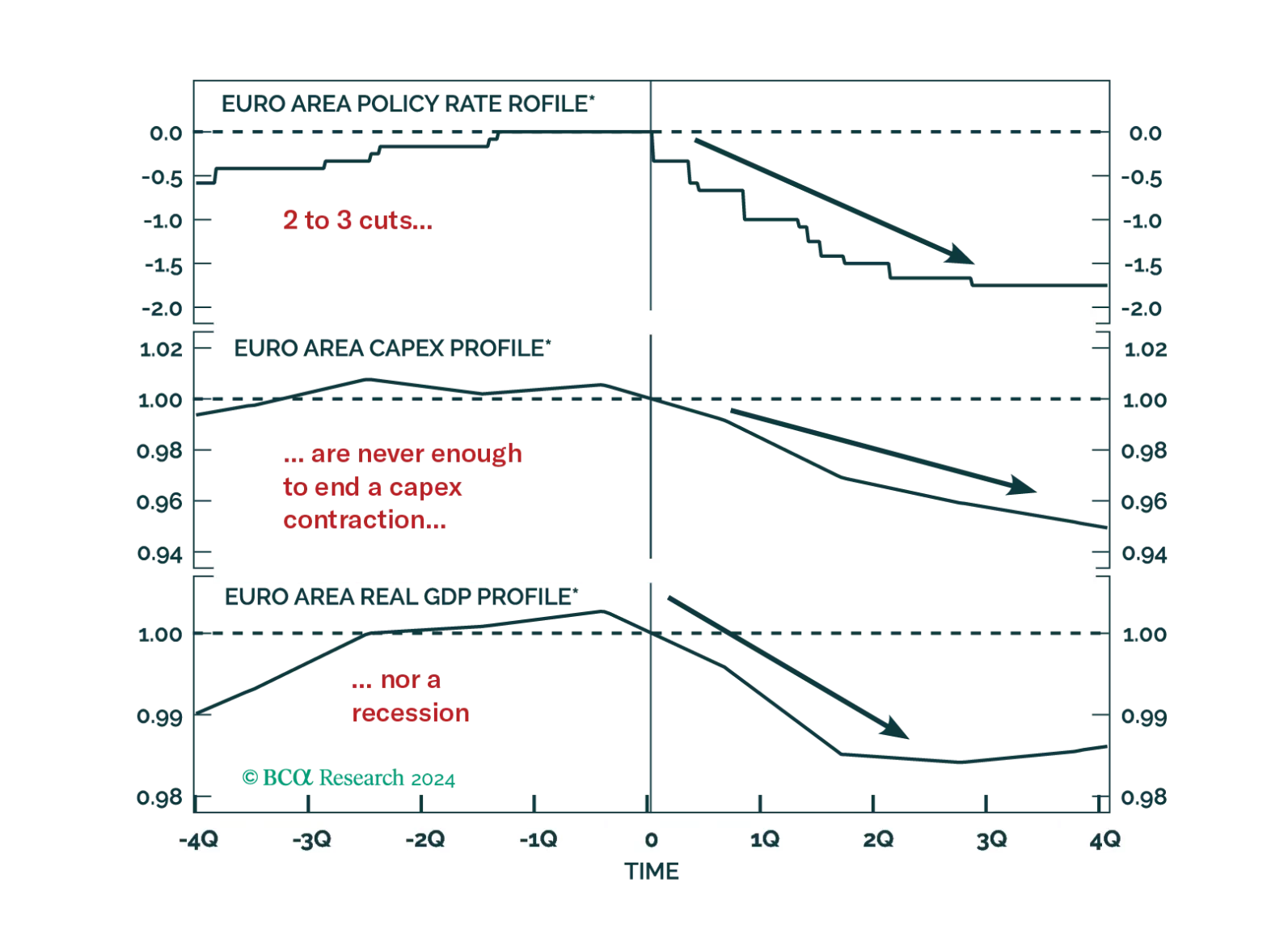

Investors hope that the ECB rate cuts priced into the curve will be sufficient to achieve a soft landing in Europe. History argues against this view, but will this time be different?

Just a few days after unexpectedly lowering three key borrowing rates by 10 basis points (bps), the PBoC cut the 1-year medium-term lending facility rate by 20 bps, from 2.50% to 2.30%. While the earlier cut lowered the interest rate charged by commercial…

The preliminary release of Q2 2024 US GDP surprised to the upside on Thursday. The US economy grew 2.8% on an annualized basis, and 3.1% on a year-over-year basis. The two largest drivers of the acceleration were consumption (mostly in goods) and gross…

The US economy has clearly cooled from its above-trend pace of growth in 2023. The consensus view among BCA Research’s strategists project that this deceleration will eventually culminate in a recession by year-end or early 2025. Our US Investment…

Total consumer credit rose by USD 11.4 billion in May (to USD 5,065 billion outstanding) from a slightly upwardly revised USD 6.5 billion increase in April, surpassing expectations of a smaller increase. Notably, revolving credit (which includes credit cards)…

Don't buy the dip. The equity bull market is over. The US will enter a recession in late 2024 or in early 2025.

BCA Research has been writing extensively on how consumption fueled by excess savings has been propping up the US economy and prevented a recession in 2023. Now, many estimates of pandemic-era excess savings show that they have run out. While consumption is…

The latest iteration of the Fed’s Beige Book, a compilation of qualitative input sourced from business and other organizational contacts in each of its twelve Districts, was released Wednesday afternoon. The Beige Book precedes FOMC meetings by two weeks…

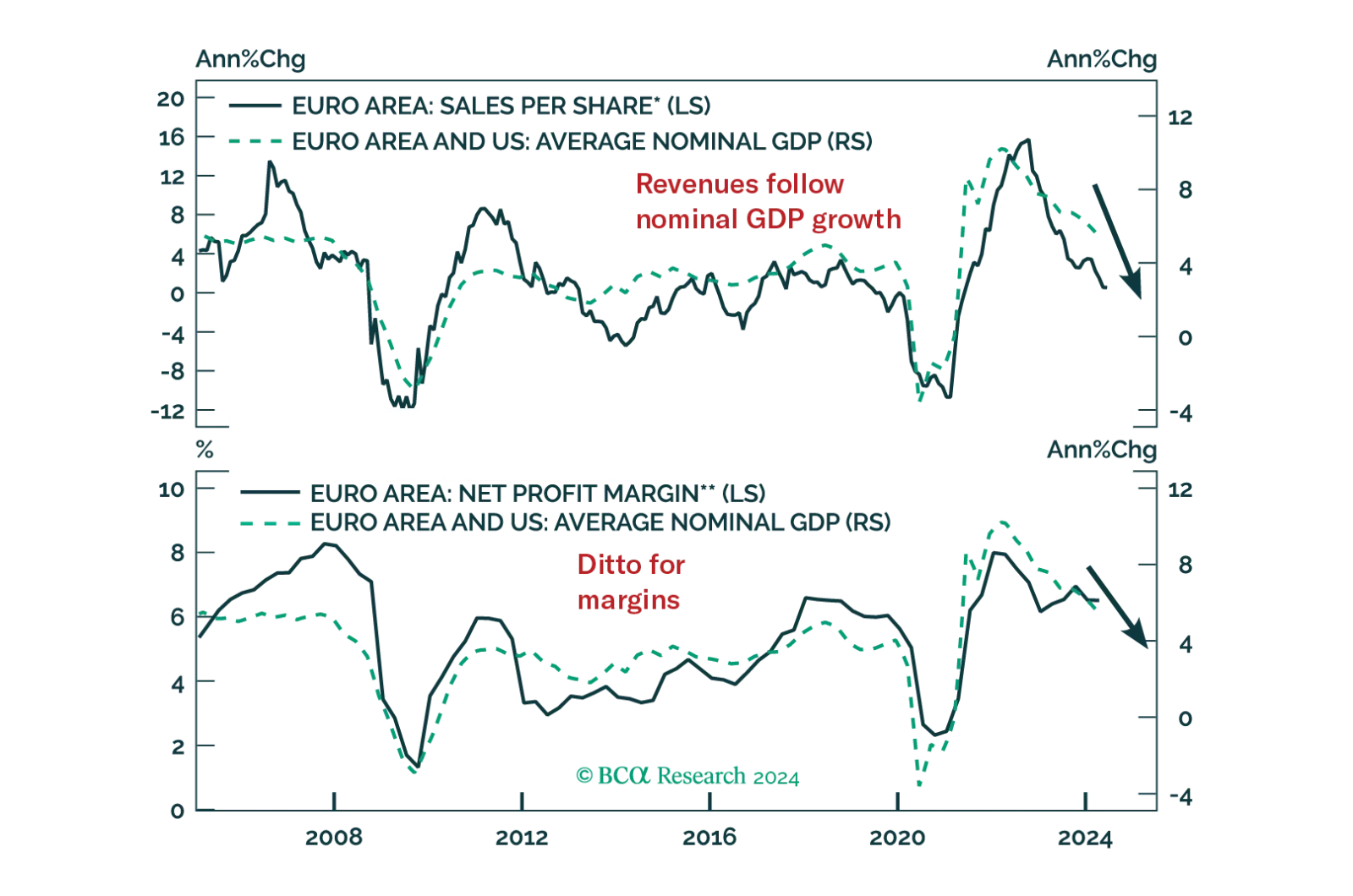

The real threat to European equities is growth, not political risk. How low will Eurozone earnings fall during the coming recession and how much will equities decline in response?