Special Report

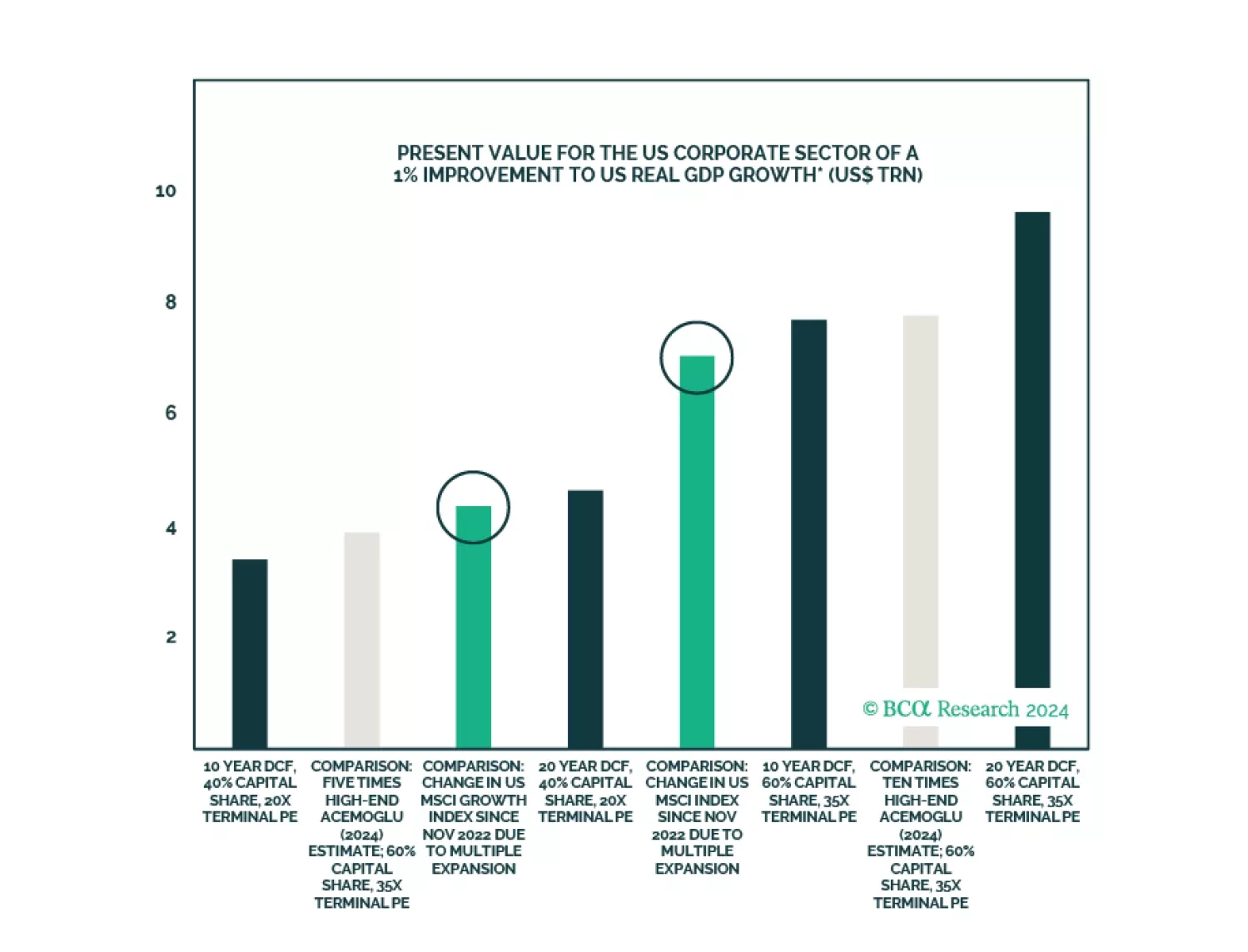

Highlights Investors who are optimistic about the potential for artificial intelligence (AI) to impact economic growth have several bullish private sector estimates to point to. At the same time, other credible estimates point to a minimal impact of AI on economic growth. Bullish estimates of AI’s growth potential rely significantly on expectations that AI models will be able to conduct new tasks, and/or a much higher share of existing tasks that can be profitably performed by AI than existing studies show. The information technology revolution of the 1990s appears to be the most obvious comparable episode to the potential for generative AI. The IT revolution boosted real potential growth by roughly a percentage point for a few years, which we regard as a very high-end estimate for AI’s possible economic impact. We doubt, however, that AI will end up truly boosting economic activity by this magnitude. We model the fair value of a sustained 1% boost to real output for the US equity market using a discounted cash flow (DCF) approach. Using a single-stage DCF model with either a 10- or 20-year time horizon, we find that a 1% improvement in real GDP growth is worth between $3 and $10 trillion for the corporate sector, depending on the margin and multiple assumed. US growth stocks have seen a $4.3 trillion increase in market capitalization since late 2022 from multiple expansion, and the broad market has seen a $7 trillion increase. This suggests that the US equity market is significantly overvalued, unless the deployment of AI technology causes a 10-to-20 year productivity surge in line with what occurred during the IT revolution of the 1990s, with persistently high margins on the revenue generated from the improvement in growth. A “sudden-stop” shift in sentiment about AI is certainly a possible trigger that could pop the bubble in growth stocks, but funding will not be a factor like it was in the late-1990s. A recession remains the most likely trigger for the AI bubble to burst. The bottom line for investors is that the US equity market may continue to rise over the coming few months, potentially strongly, until signs of a recession are unambiguous. But the market’s extremely optimistic expectations about AI’s impact on growth underscore that the US equity market selloff during the next recession is likely to be outsized relative to the impact on employment and GDP growth. Since ChatGPT was released by OpenAI on November 30, 2022, the S&P 500 index has risen close to 38 percent in total return terms (Chart II-1). By contrast, the S&P 500 equal weight index has risen by about 14 percent, which underscores how significantly optimistic expectations about AI have impacted the US equity market. While it is true that earnings have risen over the past year and a half because the economy has continued to expand, close to two thirds of the rise in the overall US equity market since the release of ChatGPT has come from multiple expansion. Chart II-1The "Generative AI Effect" Has Accounted For Over Half Of US Equity Market Returns Over The Past 18 Months In this report, we examine both estimates of AI’s potential to impact economic activity, and what those estimates might mean for the fair value of US stocks. We find that the US equity market is significantly overvalued unless the deployment of AI technology causes a 10-to-20 year productivity surge in line with what occurred during the IT revolution of the 1990s, with persistently high margins on the revenue generated from the improvement in growth. While that is technically a possible outcome, we regard it as the most realistic “best case scenario”, and we doubt that AI will end up truly boosting economic activity by this magnitude. It is possible that the AI bubble will burst before the next US recession, but that would likely depend on a major shift in sentiment about AI, which is extremely difficult to predict. A late-1990s-style “funding shortfall” will not be a catalyst this time around. As such, the US equity market may continue to rise over the coming few months, potentially strongly, until signs of a recession are unambiguous. But once the recession arrives, the extremely optimistic expectations about AI’s impact on growth underscore that the selloff in US stocks will likely be outsized relative to the impact of the recession on employment and GDP growth. Estimating AI’s Potential To Boost Growth: The View Of Others Investors who are optimistic about the potential for artificial intelligence (AI) to impact economic growth have several bullish private sector estimates to point to (Table II-1). For example, Goldman Sachs' baseline is that generative AI will boost aggregate labor productivity growth by 1.5 percentage points per year in the US over a ten-year period.1 The Brookings Institute has published estimates of a potential 1.8% annual improvement in labor productivity over either ten or twenty years.2 And McKinsey has argued that the automation of individual work activities enabled by AI and other technologies could provide the global economy with an annual productivity boost of between 0.5% and 3.4% until 2040, with generative AI contributing 0.1 to 0.6 percentage points of that growth.3 Table II-1Private Sector AI Growth Impact Estimates Are Very Bullish All of these estimates come with a variety of assumptions, but they are not the most optimistic estimates available. Goldman Sachs presents additional possible scenarios which could raise labor productivity growth by anywhere between 2.5 and 3 percentage points per year. On the other hand, a recent paper by Daron Acemoglu presented a much less optimistic view of the potential growth impact of AI.4 Acemoglu is a well-known economist whose research often focuses on the structural drivers of growth, as well as the impact of technological change. His paper concludes that predicted real output gains over the next 10 years from AI advancements are likely to be less than one percent in total over a ten-year period. The gap between Acemoglu’s estimates and those of other major organizations such as Brookings / McKinsey / Goldman Sachs lies, first, in the fact that Acemoglu only considered the potential for AI to impact existing tasks, rather than the growth impact of new tasks. Using Hulten’s theorem, which posits that the macro impact of microeconomic shocks can be estimated by what fraction of tasks are impacted and average task-level cost savings, Acemoglu arrives at his modest AI impact estimates through the following calculations: 20% of US labor tasks are exposed to AI, based on estimates from Eloundou et al. (2023)5 Among exposed tasks, 23% can be profitably performed by AI based on estimates from Svanberg et al (2024)6 Based on average time improvement studies, average labor costs savings from deploying AI are 27%, which are translated into overall cost savings of 14.4% using industry labor shares Applying this approach yields a total factor productivity boost of AI’s impact on existing tasks of no more than 0.66% (cumulative) over 10 years (20% times 23% times 14.4%). Acemoglu argues that even this is likely to be overstated because existing estimates of productivity gains and costs savings have been based on “easy-to-learn” tasks for AI, whereas “harder-to-learn” tasks would entail lower productivity enhancements. Acemoglu arrives at a final upper bound estimate of 0.53% total rise in total factor productivity (5.3 basis points per year), and a 0.9% total rise in real GDP (9 basis points per year). The GDP impact is higher than the TFP improvement because of an assumed improvement in the contribution of capital intensity to labor productivity. Assuming no change in Acemoglu’s average labor cost savings estimates and assuming an unchanged labor share estimate, Table II-2 shows how Acemoglu’s estimates of the impact of AI on annualized total factor productivity can be scaled up. The table highlights that the TFP impact implied by a Hulten’s Theorem approach falls short of the estimates cited by the major organizations noted above, even when we assume that most labor tasks are exposed to AI and that more than half of those tasks can be profitably employed by AI models. As such, investors should recognize that the AI growth potential estimates provided by several organizations appear to rely significantly on expectations that AI models will be able to conduct new tasks, and/or a much higher share of existing tasks that can be profitably performed by AI than existing studies show. Table II-2AI Growth Impact Estimates Based Only On Existing Tasks Are Nowhere Near As Bullish Estimating AI’s Potential To Boost Growth: Our Thoughts If Acemoglu’s estimates are too pessimistic because they don't account for AI creating new tasks, and if estimates from major organizations appear to be too optimistic, what should investors use as a benchmark for AI's economic impact? It is very difficult to determine how AI will boost economic activity if most of the gains are likely to come from new tasks, because it requires envisioning and quantifying the effect of tasks that do not yet exist. In our view, without more evidence of the utility and application of AI programs, the most reasonable approach is to identify a comparable episode of technological progress and measure the impact that it had on growth. Over the past 20-to-30 years, investors have witnessed numerous technological advancements, including the following: The rapid deployment of information and communication technology products and infrastructure in the 1990s The commercialization of the internet The development of smartphones The introduction of social media The advent of cryptocurrencies The impressive use of fracking technology to boost US oil output and, The growth of electric vehicles and alternative energy. Of these examples, the information technology revolution of the 1990s appears to be the most obvious comparable episode to the potential for generative AI. It is true that the acceleration in productivity growth that occurred in the 1990s was smaller than that of the last third of the nineteenth century or the 1930s-to-early-1970s period. Table II-3, however, shows that these periods benefitted from truly general-purpose technologies that occurred alongside a significant improvement in the average lifespan. The impact of that improvement on the effectiveness of human capital may not be fully captured in measures of labor composition. We would need to see much more evidence before believing that artificial intelligence could reproduce those kinds of effects. Table II-3The 1990s Was Not The Largest Productivity Surge In History, But Likely The Most Comparable To AI’s Potential Today What caused the IT-driven surge in productivity in the 1990s? Computers had been around for two decades prior to the 1990s, but significant cost reductions made the widespread deployment of IT equipment affordable. Advancements in office productivity software also significantly increased output per hour of service workers. Measuring exactly what the 1990s IT revolution did to economic growth is subject to a few assumptions. On the one hand, overall labor productivity accelerated from 1.6% on average between 1992 and 1995 to 3.2% on average between 2001 and 2005. Indeed, when looking at Chart II-2, it appears as if the acceleration in productivity lasted for almost a decade. Chart II-2Seemingly A Decade-Long Productivity Surge, But Not Really On the other hand, the period from 2001 to 2005 occurred during a recession and a subsequent period of weak corporate profits and employment growth. Chart II-3 shows that the labor productivity improvement that occurred during that period also happened alongside a significant reduction in hours worked, which is why real GDP growth was meaningfully weaker than it was from 1996 to 2000. Chart II-4 shows that the relationship between productivity growth and hours worked has been negative since the mid-1980s, even after accounting for the fact that this relationship appears to be especially negative during recessions. Chart II-3Strong Productivity In The 2000s Occurred For A Different Reason Than In The 1990s Chart II-4Over The Past Forty Years, Productivity Gains Have Not Fed Fully Through To Growth Given that generative AI has substantial potential to displace labor, productivity gains from this technology may not map directly to real GDP growth if there are negative consequences for the labor market. In our view, this reinforces our perspective that optimistic projections about AI’s potential to boost growth are overstated. All told, an analysis of the 1990s IT revolution shows that it boosted real potential growth by roughly a percentage point for a few years. In the case of AI, we think that a 1% annual growth improvement is somewhat reasonable, but we would characterize it as a very high-end estimate. We acknowledge, however, that its benefits may be longer lasting in such a scenario than what occurred in the 1990s. What Are Stocks Pricing In For AI? To gauge what the equity market is pricing in in terms of expectations for AI to boost economic activity and generate substantial corporate profits, we conduct a discounted cash flow (DCF) valuation exercise to determine the fair value of a sustained 1% boost to real output. We essentially regard this as the most realistic “best-case scenario” and we doubt that AI will end up truly boosting economic activity by this magnitude.7 But, if the rise in the equity market since late 2022 is meaningfully lower than the fair value implied by a 1% growth improvement, that could justify further gains for tech-related stocks. Unfortunately for investors who are optimistic about AI, it turns out that that is not the case. We make several assumptions when modeling the likely cash flows from a 1% growth improvement: We assume that risk-free interest rates are equal to nominal trend growth We assign a 2% equity risk premium to the risk-free rate when calculating the discount rate We assume that the corporate sector's share of the output generated is higher than is currently the case, varying between 40% and 60%. This compares to a 40% capital share of output in 2022, according to the BLS’ total factor productivity database. Strictly speaking, a full discounted cash flow approach that assumes an indefinite 1% annual growth improvement would value this development at between $11 and $16 trillion today. However, it is unrealistic to expect any technological development to boost growth every year in perpetuity. Thus, we conduct this valuation exercise using a different approach: a single-stage discounted cash flow model with either a 10- or 20-year time horizon. We calculate a terminal value at the end of the forecast period, employing a generous trailing P/E ratio of between 20 and 35 times profits. This approach values a 1% improvement in real GDP growth for the corporate sector at between $3 and $10 trillion, depending on the margin and multiple assumed. To determine what the equity market is pricing in regarding AI, we use a similar approach to that shown for Microsoft in last month's report, but applied to the US MSCI Growth Index and the overall US equity index. Our method calculates the change in market capitalization since November 2022 that is not attributable to an improvement in actual fundamentals, which we infer is the market cap increase associated with AI growth expectations. While it is true that expectations of a recession have been dialed back since late-2022, Chart II-5 highlights that there was no rise in our equity risk premium proxy that year. That strongly points to AI growth expectations as explaining most of or all of the subsequent rise in equity multiples given that bond yields have not declined meaningfully since. Chart II-5The Rise In Equity Multiples Since Late-2022 Has Occurred Due To Growth Expectations, Not Reduced Recession Risk Our approach highlights that US growth stocks have seen a $4.3 trillion increase in market capitalization since late 2022 from multiple expansion, and that the broad market has seen a $7 trillion increase. Chart II-6 contextualizes those numbers, by presenting them alongside the range of fair value estimates from our DCF approach. We also include a substantial scaling up of the growth impact estimates provided by Acemoglu, on the order of five and ten times the effect. Chart II-6The US Equity Market Is Pricing In A Substantial And Long-Lasting Boost To Growth From AI The chart vividly illustrates that the US equity market is currently priced roughly in line with the fair value of a 1% sustained improvement to real GDP growth and only slightly lower than what a ten-fold increase in Acemoglu’s existing-task estimates would imply. That may seem reasonable to investors with high hopes that AI will revolutionize the global economy but, from our perspective, it underscores a major source of risk to the US equity market. Chart II-6 may be framed in a different fashion: it suggests that the US equity market is significantly overvalued, unless the deployment of AI technology causes a 10-to-20 year productivity surge in line with what occurred during the IT revolution of the 1990s, with persistently high margins on the revenue generated from the improvement in growth. What Will Stop The Mania? If the US stock market is indeed grossly overvalued because of overly optimistic expectations about AI’s potential to boost economic growth, then it is important for investors to identify triggers that might pop the bubble. A starting point is to ask what popped the equity market bubble in the 1990s. The NASDAQ peaked on March 10, 2000, and rising interest rates were clearly a factor. Chart II-7 shows that the fed funds rate rose from 4.75% in the summer of 1999 to 6.5% in May 2000, a 175 basis point increase on what was already quite an elevated level. Chart II-8 shows, however, that funding was also an important element that had been flagging a warning sign well in advance of the peak in the stock market. The chart shows that the number of IPOs actually peaked in 1996, and fell to less than half their peak level in 1998. IPO activity rebounded in 1999, but the quality clearly diminished: 76% of the IPOs in that year had negative earnings, a metric that rose to 81% in 2000. Chart II-7Tighter Monetary Policy Clearly Played A Role In Bursting The Dotcom Bubble Chart II-8Dried-Up Funding Also Helped Pop The Dotcom Bubble Chart II-9Large Tech Companies Have A Lot Of Room To Continue Investing In AI On March 20, 2000, ten days after the peak in the equity market, Barron’s published a cover story, entitled “Burning Up.”8 The article focused on the fact that many internet companies were rapidly “burning through” their cash balances and would likely be out of money by the end of that year. This suggests that the narrative of “dried-up funding” was an important element in triggering the substantial selloff that followed. Today, while a “sudden-stop” shift in sentiment about AI is certainly a possible trigger that could pop the bubble in growth stocks, we doubt that funding will truly be a factor. NVIDIA’s surge in sales have gone largely to large tech companies, such as Google/Alphabet, Amazon, Microsoft, and Meta, and these firms have ample cash flow and cash holdings that can continue to be spent on AI chips and development (Chart II-9). It is true that the cash holdings of these firms has peaked and are trending lower, but their current level of $330 billion implies that large tech companies could fund another three years of NVIDIA’s most recent quarterly revenue without having to spend out of profits. If large tech firms significantly slow their pace of investment in AI, it is likely to be in response to one of two things: either a recession, or the belief / evidence that the pace of improvement of AI models is significantly slowing and that better quality data is the actual bottleneck rather than more “compute.” The latter has been hinted at in recent new stories in the financial press,9 but there is no sign yet from tech company executives that this is impacting their AI spending decisions. As such, we conclude that, while it is possible that the AI bubble will burst on its own, a recession remains the most likely trigger. Investment Conclusions Based on our analysis, the US equity market appears to be priced as if AI will deliver a late-1990s style productivity boom for 10-to-20 years. While possible, we doubt that this will occur, underscoring that US tech stocks are highly vulnerable to changes in the structural outlook for AI. It is possible that the AI bubble will burst before the next US recession, but that would likely depend on a major shift in sentiment about AI that will be extremely difficult to predict. A late-1990s-style “funding shortfall” will not be a catalyst this time around. A recession is likely to cause a major shock to AI-related stocks. Using Microsoft as a bellwether for the industry, Chart II-10 highlights that Microsoft’s capital expenditures as a share of EBITDA are quite elevated relative to history and are potentially subject to decline in a recession (which would also lower EBITDA itself). Chart II-11 shows that Microsoft’s capital expenditures have contracted in the past when the economy or corporate profits have been weak, suggesting that NVIDIA’s revenue will take a significant hit during a recession. That would be a cyclical effect that would not necessarily affect AI’s potential to impact economic activity over the longer term, but it would likely affect the “invulnerable AI” narrative for a time and would cause significant profit-taking among investors who are heavily overweight tech stocks. Chart II-10CAPEX Rates Are Elevated Relative To Cash Flow Chart II-11During A Recession, Tech Sector CAPEX Will Very Likely Decline The bottom line for investors is that the US equity market may continue to rise over the coming few months, potentially strongly, until signs of a recession are unambiguous. But the extremely optimistic expectations about AI’s impact on growth underscore that the US equity market selloff during the next recession is likely to be outsized relative to the impact on employment and GDP growth. Jonathan LaBerge, CFA Vice President The Bank Credit Analyst Footnotes 1 Elder, Bryce. "Surrender Your Desk Job to the AI Productivity Miracle, Says Goldman Sachs." Financial Times Alphaville, 27 March 2023 2 Baily, Martin Neil, Erik Brynjolfsson, and Anton Korinek. "Machines of Mind: How Generative AI Will Power the Coming Productivity Boom." Brookings Institution, 5 May 2023. 3 Chui, Michael, et al. "The Economic Potential of Generative AI: The Next Productivity Frontier." McKinsey & Company, 14 June 2023. 4 Acemoglu, Daron. "The Simple Macroeconomics of AI." NBER Working Paper 32487, May 2024. 5 Eloundou, Tyna, Sam Manning, Pamela Mishkin, and Daniel Rock, “GPTs are GPTs: An Early Look at the Labor Market Impact Potential of Large Language Models,” Technical Report, arXiv 2023. 6 Svanberg, Maja, Wensu Li, Martin Fleming, Brian Goehring, and Neil Thompson, “Beyond AI Exposure: Which Tasks are Cost-Effective to Automate with Computer Vision?,” 2024. MIT Working Paper. 7 Note to readers: I used ChatGPT to assist with elements of the production of this report. To put it mildly, the experience was not consistent with a 1% sustained boost to real GDP growth! 8 "Burning Up: Warning: Internet Companies Are Running Out of Cash - Fast." Barron's, 20 March 2000. 9 Mims, Christopher. "The AI Revolution Is Already Losing Steam." The Wall Street Journal, 31 May 2024.