Consumer

Total consumer credit rose by USD 6.4 billion in April (to USD 5,053 billion outstanding), from a USD 1.1 billion decrease in March (a large downward revision to the USD 6.3 billion rise initially reported) and significantly shy of expectations for a USD 10…

The redeployment of pandemic-era excess savings has been a significant driver of US consumption growth and helped the economy avoid a recession last year. Although pandemic-era fiscal support was less generous in China, households nevertheless accumulated CNY…

Consumption accounts for two-thirds of the US economy, and our recession view relies heavily on the deteriorating outlook for US consumers. That said, dissecting US GDP into its components reveals that consumption tends to merely stabilize during…

According to BCA Research’s Global Asset Allocation service, the economy has been in the “Overheating” phase of the cycle for a while, with signs of slowing growth but also stubbornly high inflation. The most likely next phase is “Recession,” though the…

According to BCA Research’s Commodity & Energy Strategy service, the oil demand forecasts from the IEA, EIA, and OPEC are too optimistic. The IEA, EIA, and OPEC all anticipate oil demand growth to slow this year following a robust post-pandemic…

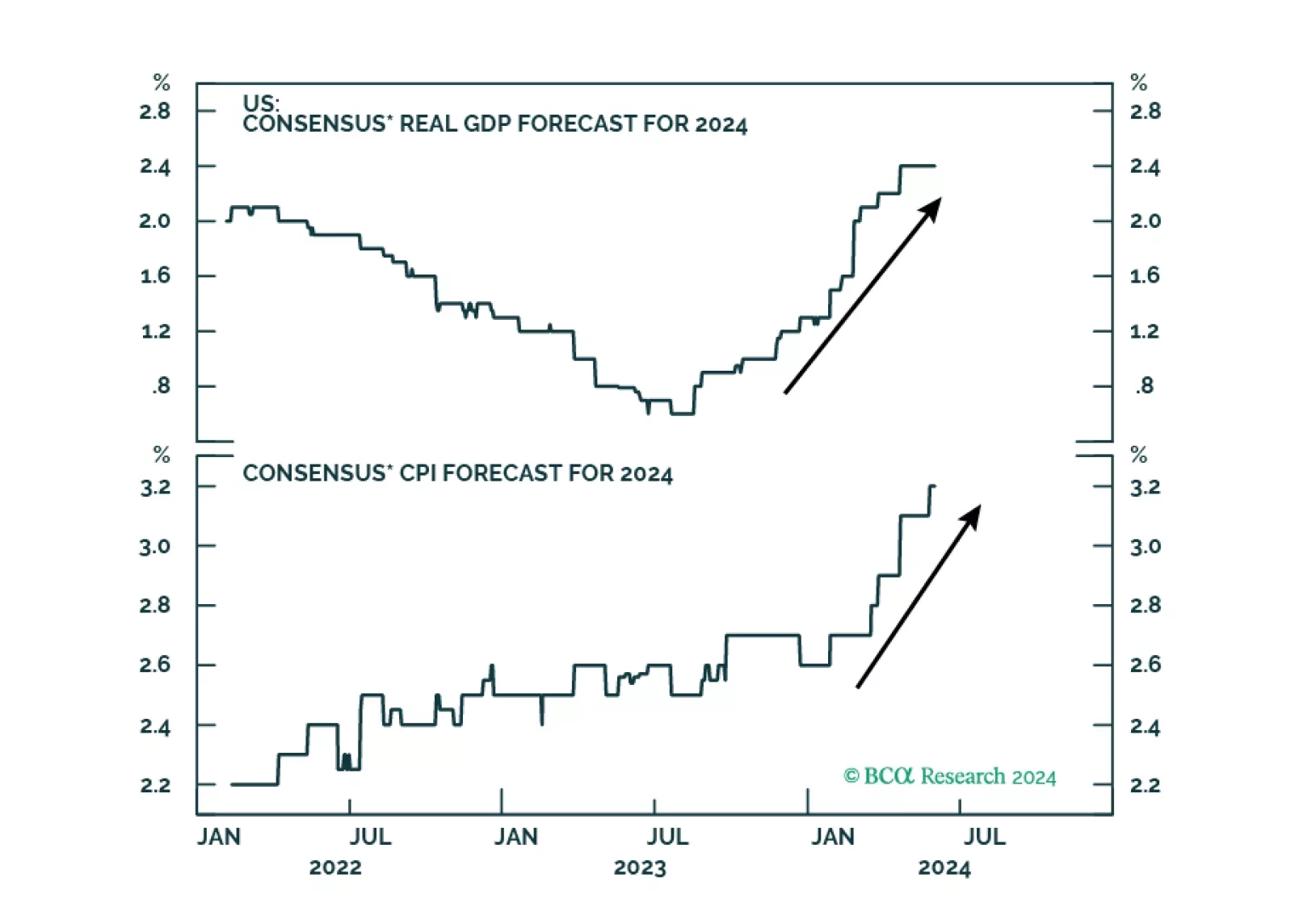

The US economy is in the “Overheating” phase, so stronger growth brings higher inflation. Tight monetary policy means recession is still likely over the next 12 months. Stay defensive.

According to BCA Research’s US Political Strategy service, Trump’s conviction will not be a game changer in the upcoming Presidential election. President Trump was convicted of 34 felony charges by a 12-person jury in a New York state court on May 30 for…

US Q1 GDP was revised lower from 1.6% q/q annualized to 1.3%. Notably, the downward revision to personal consumption was higher than expected, from 2.5% q/q annualized to 2.0%. Investment and government spending were revised higher. Real final sales to…

Chinese PMIs from the National Bureau of Statistics (NBS) disappointed in May. The manufacturing PMI contracted in May (49.5), breaking a two-month expansion streak and disappointing expectations of continued growth. Meanwhile, the services sector PMI…

As in many other countries, China’s cyclical consumption growth is primarily driven by labor market conditions, income, and borrowing. BCA Research’s China Investment Strategy service maintains the view that these three aspects will not meaningfully improve…