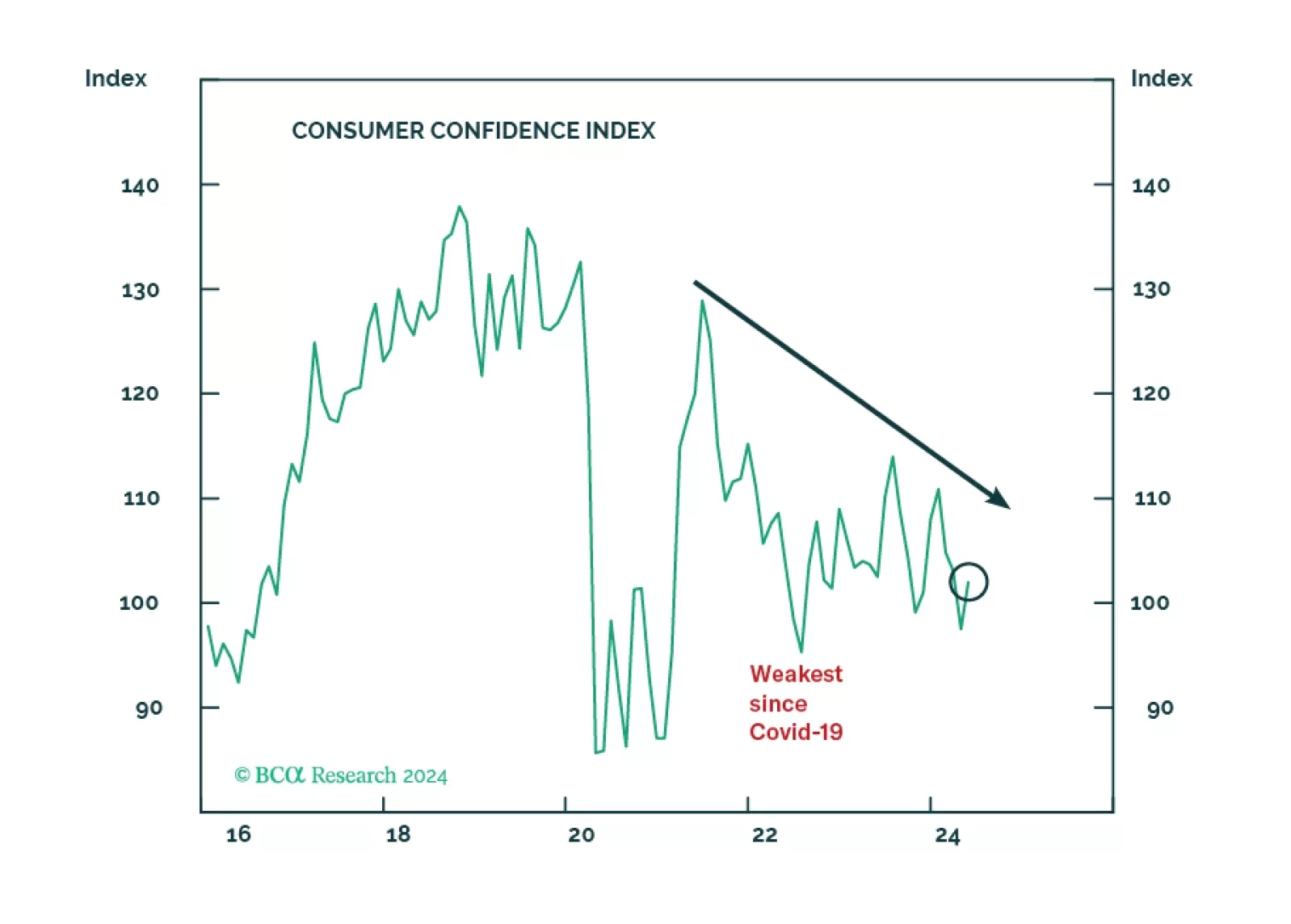

Consumer

In Section I, we argue that global investors have been lulled into a false sense of security concerning the resiliency of the US economy. Tight monetary policy means that something must change for a recession to be avoided, and developed market rates cuts will likely be too modest and come too late to save the day. Nimble investors or those highly sensitive to tracking error should not be underweight stocks over the coming 3-6 months. Over a 6-12 month time horizon, we continue to recommend that investors remain underweight global equities versus US$-hedged long-maturity developed market government bonds. Section II is a guest report written by Martin Barnes, BCA’s former Chief Economist. Martin revisits the idea of the Debt Supercycle and discusses how its true end may emerge in response to a fiscal crisis in the US over the coming few years.

Favor defensive sectors, low-beta assets, and long-duration bonds until the election uncertainty is lifted one way or another over the next five months.

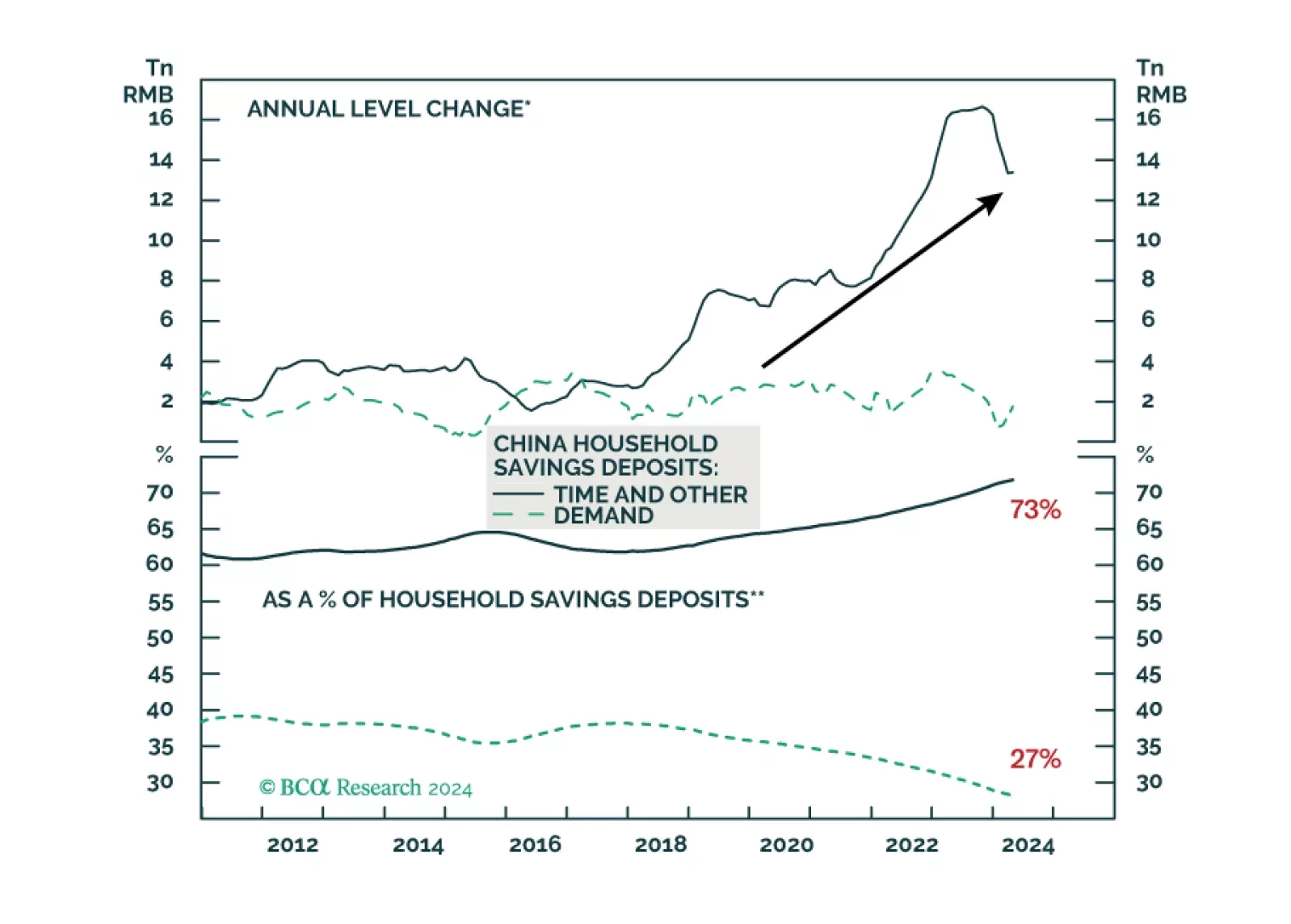

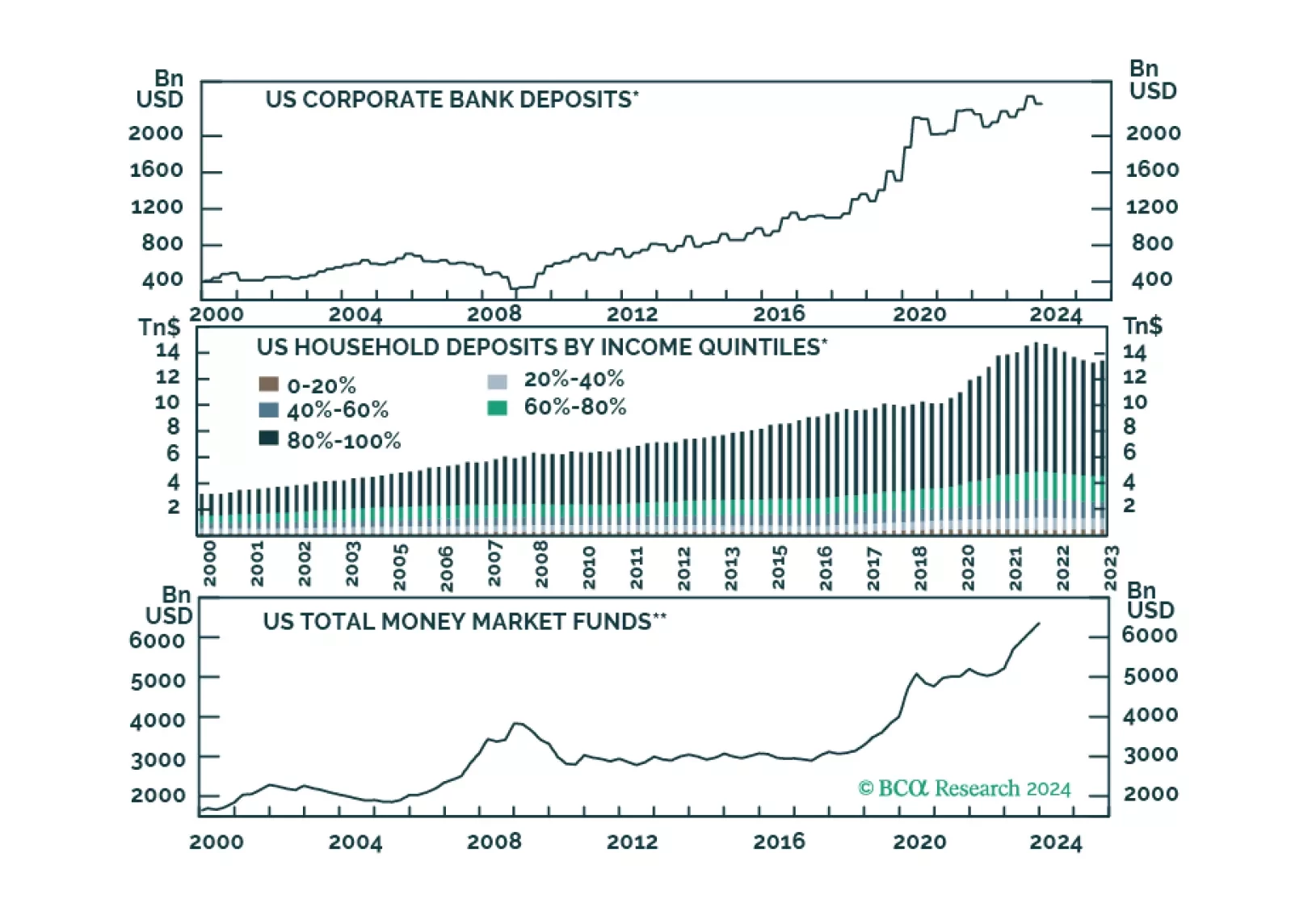

The large buildup in Chinese households’ savings deposits is unlikely to fuel consumption. Poor outlooks on labor market conditions, income, and households’ unwillingness to borrow will hinder consumption through the rest of 2024.

The signs of an approaching recession are starting to emerge. We will turn tactically defensive once they all fall into place.

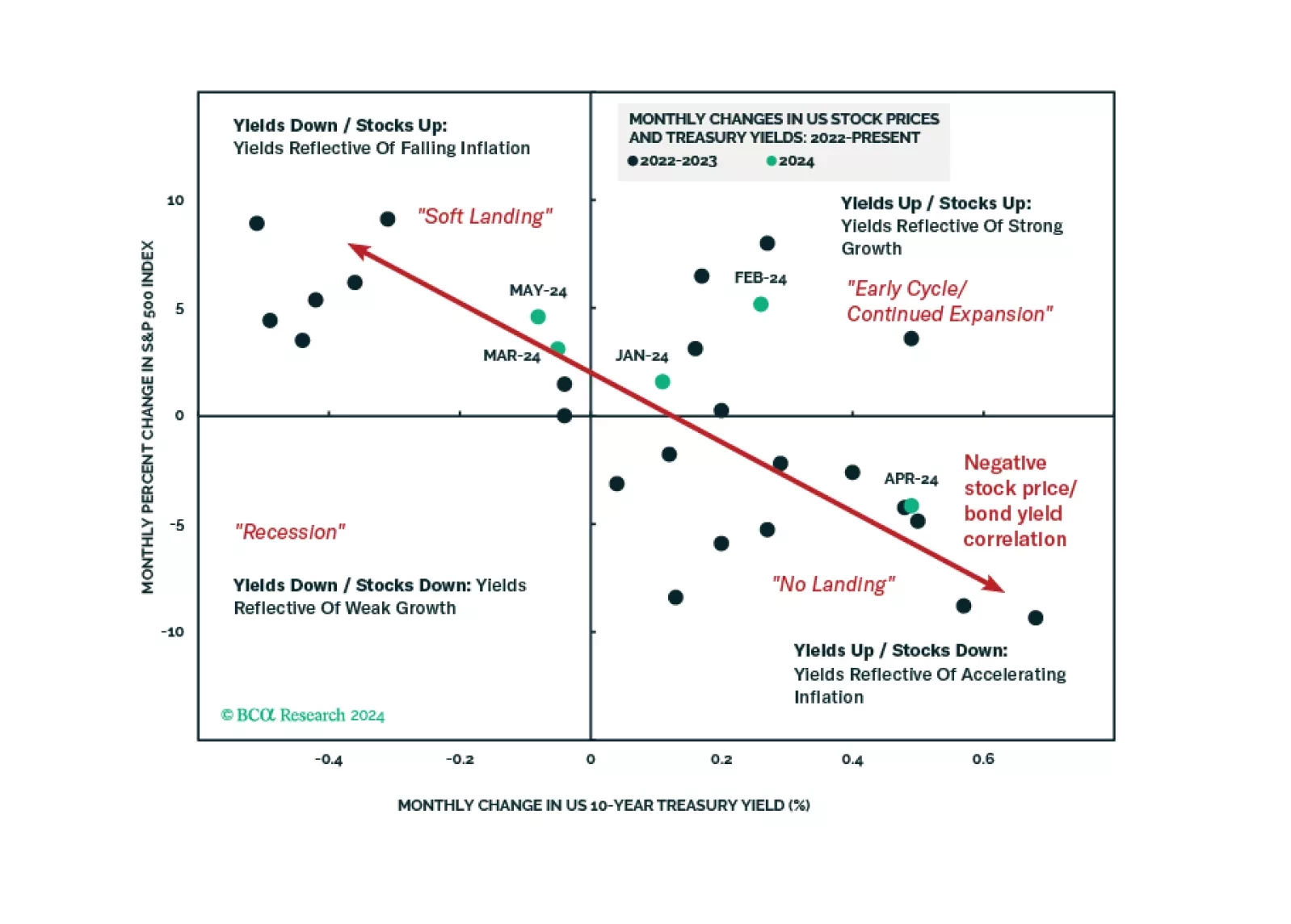

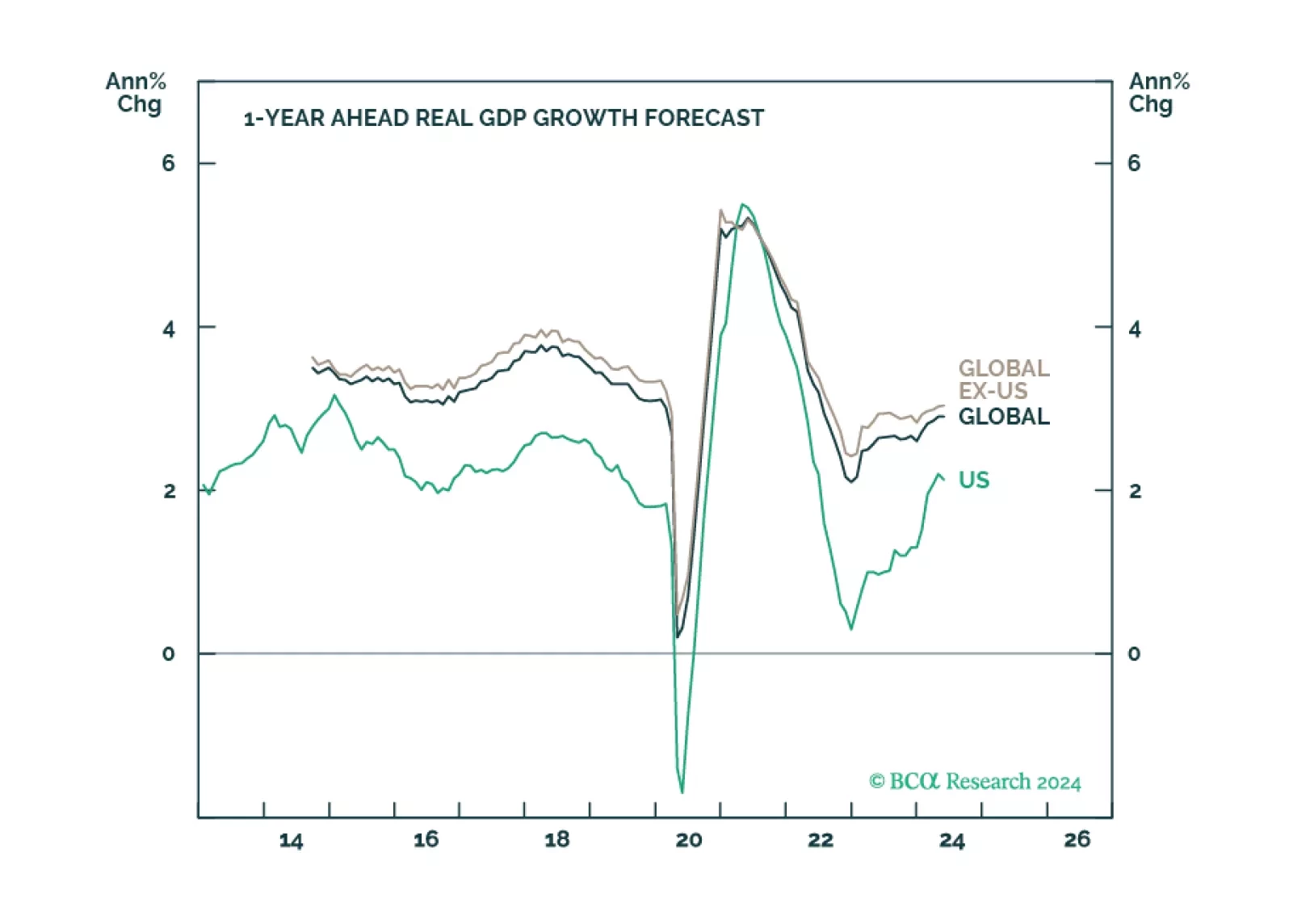

Looking at economic activity, global monetary policy seems restrictive, however, the behavior of financial markets tells a different story. What gives?

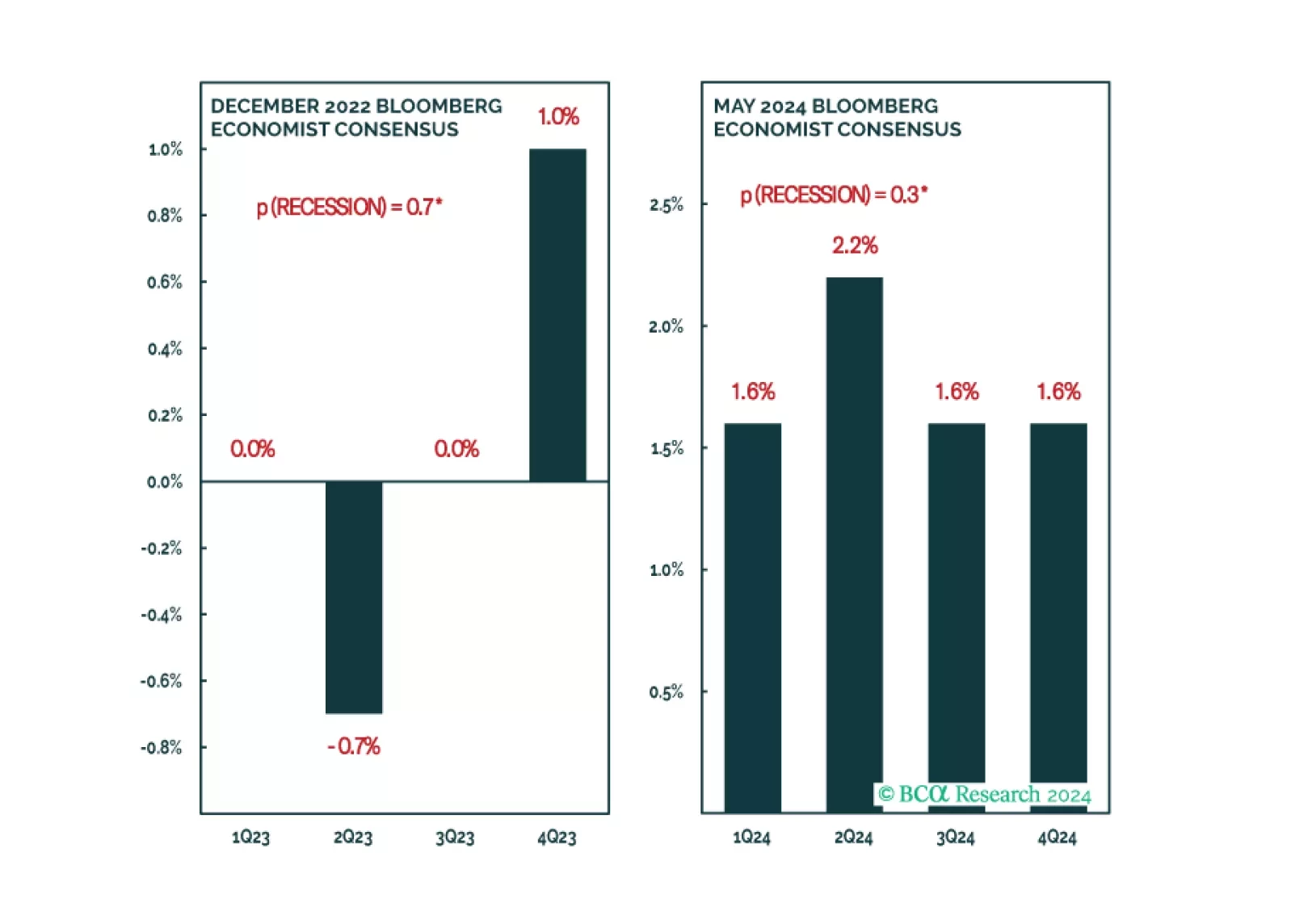

There is a path to a soft landing, but it is a narrow one. We estimate that there is only a 20% chance that the US will avoid a recession before the end of 2025. We are currently neutral on global equities, but expect to downgrade stocks to underweight during the summer.