Consumer

US durable goods orders surprised to the upside in April, growing 0.7% m/m against expectations they would decline. The March growth rate was nevertheless revised significantly lower, from 2.6% m/m to 0.8% m/m. Core capital goods shipments (an input into…

We do not subscribe to the Goldilocks scenario in which price pressures continue to ease while economic growth remains robust. We expect that softening labor demand will eventually hinder consumption as wage and payrolls growth slows, at the same time that…

Our US Investment strategists have used the savings rate as a proxy for households’ willingness to spend. Its persistent decline suggests that consumers have been spending their pandemic-era excess savings and our colleagues would consider a normalization…

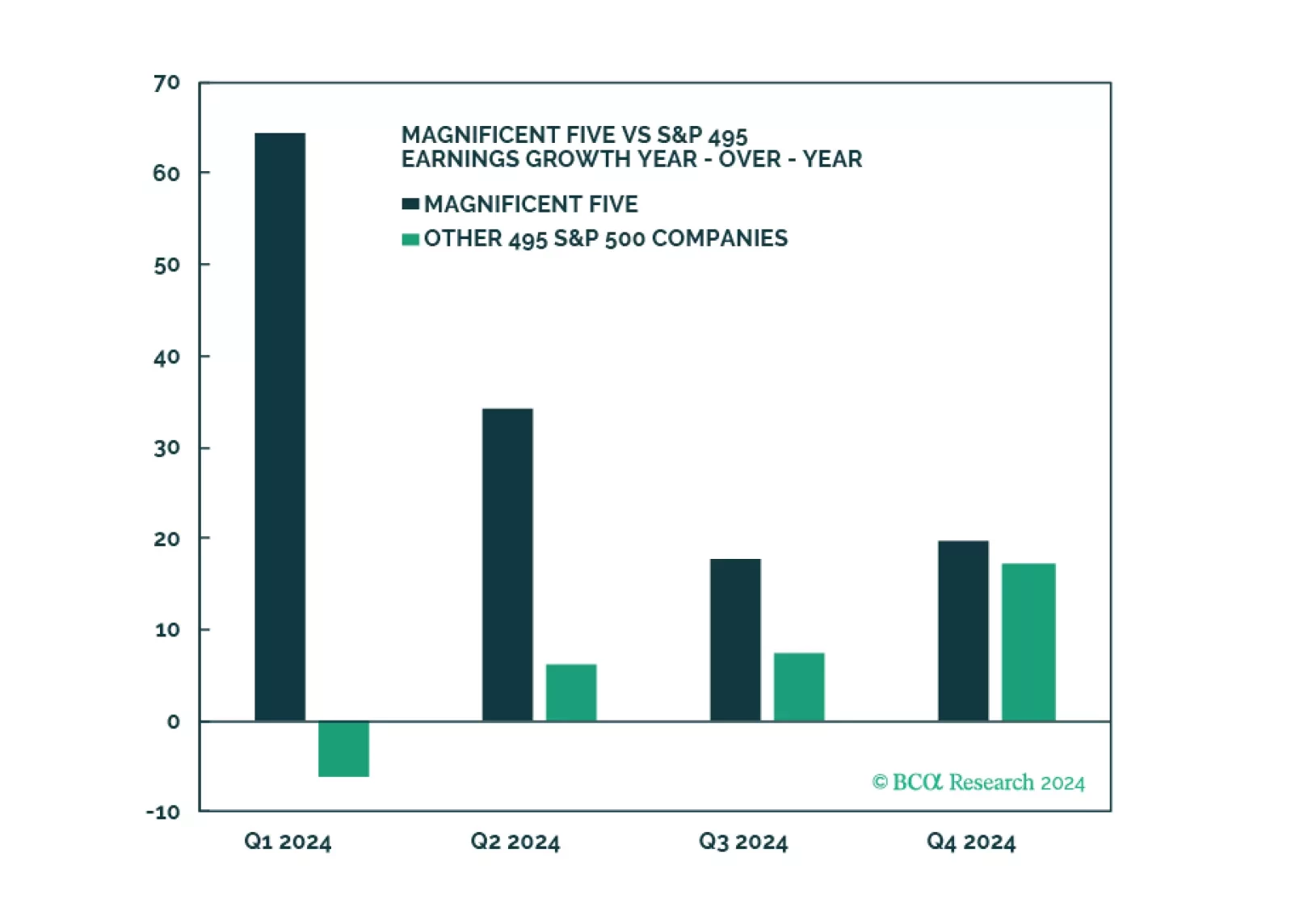

Q1 Earnings and sales growth were strong, but the devil is in the details: Without the Magnificent Five, earnings growth for the index would have been negative. On a positive note, margins have stabilized, and earnings growth is expected to broaden into yearend. Companies are optimistic about the economy. Development of AI applications is in full swing, but few companies are monetizing them yet. Consumer spending is strong but is slowing. We reiterate our underweight of consumer sectors, and overweight of Software and Services as the “don’t fight AI” adage holds.

Several economic releases out of China disappointed in April. Retail sales decelerated from 3.1% y/y to 2.3% y/y and fixed asset investment growth slowed from 4.5% YTD y/y to 4.2% YTD y/y. Both were expected to accelerate. Although industrial production…

An adverse shock is not a recession prerequisite. The empirical record shows that the US economy regularly evolves its way into a contraction with little fanfare. If current cooling trends continue, we project a recession will begin in late 2024/early 2025. …

US retail sales remained unchanged in April, a downside surprise from expectations of 0.4% m/m growth. Notably, the retail sales control group (an input to GDP) declined by 0.3% m/m despite expectations of mild growth and all of the March figures were revised…

Despite historically high interest rates and the fact that variable-rate mortgage issuances dominate the mortgage market landscape, Australian home prices continue to climb at a close to double-digit annual rate. The Core Logic House Price index is now…

On the surface, the Tuesday release of the NFIB Small Business Survey indicated resilience among small businesses. The headline index appreciated to 89.7 from 88.5, upending expectations of a moderation to 88.2. However, the marginal improvement has not…

Emergency pandemic policies elongated the lag between Fed rate hikes and an observable slowdown in the economy. Notably, fiscal transfers and constrained consumption options endowed households with more than $2 trillion of savings they would not otherwise…