Consumer

Chinese economic data for the first two months of the year were mixed. On the one hand, industrial production and fixed asset investment growth came in above consensus estimates, accelerating to 7.0% y/y (vs. expectations of 5.2% y/y) and 4.2% y/y (vs.…

Indicators continue to point to resilient US housing market dynamics. The NAHB Housing Market Index increased for the fourth consecutive month to an 8-month high of 51 in March, beating expectations it would remain unchanged at 48. Increases across all three…

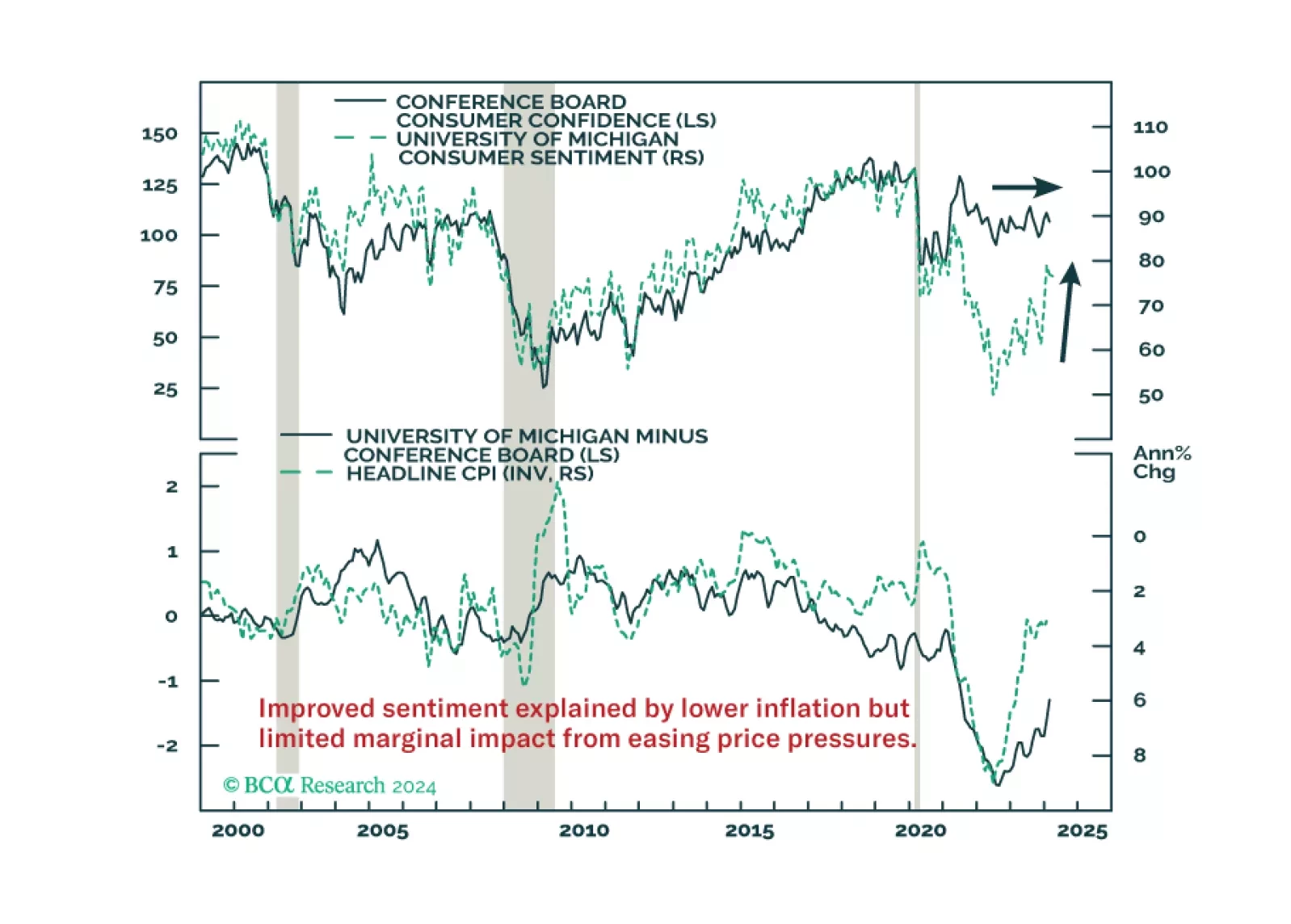

Improved consumer morale will not compensate for the fading tailwinds to consumption. Neither will the wealth effects from higher stocks and home prices.

Chinese private sector credit demand remained weak in February, sending a negative signal about domestic economic conditions. Total social financing growth slowed from a record CNY6.5 trillion in January to CNY1.56 trillion, below consensus forecasts of…

Our US Beige Book monitor – which we use to gauge changes in the language of the Fed’s report – continues to signal lackluster US economic conditions. Historically, the monitor has closely tracked real GDP growth in the US. However, the long standing…

According to BCA Research’s Foreign Exchange Strategy service, Australia’s macroeconomic environment validates a long AUD position, especially at the crosses. The market expects that the RBA will cut interest rates soon, but that is not likely when we look…

The US retail sales report for February delivered a disappointing signal on Thursday. Although retail sales returned to expansion, the 0.6% m/m increase fell below anticipations of a 0.8% m/m rise. In addition, the prior month was revised down to a -1.1% m/m…

The Eurozone Sentix Economic index improved from -12.9 to -10.5 in March, marking a fifth month of improved sentiment amongst investors and economic agents. Notably, the Expectation subindex rose to a 25-month high of -2.3 from -5.5 in February. The Current…

The latest MBA weekly survey shows mortgage applications rose 7.1% in the week ending March 8 on the back of a 4.7% increase in purchases and a 12.2% rise in refinancing, marking the second consecutive weekly increase. Higher mortgage activity comes amid…

There is a general consensus among BCA Research strategists that a US recession is highly likely over the next two years. While last month our Global Investment strategists reduced the probability that a recession will materialize in H1 2024 and raised the…