Consumer

Our kinked Phillips curve framework predicted the immaculate disinflation of 2023. That same framework is now warning that the global economy is heading towards a recession in the second half of 2024.

Confidence is on the mend in the Euro Area. The rebounding ZEW growth expectations index reveals that investors are becoming more optimistic. The German IFO's business climate index inched higher in October for the first time since April, suggesting that…

After dipping into negative territory between June and early August, the Global Economic Surprise Index has since rebounded, signalling an improvement in economic momentum. Initially, this rebound was isolated to the US. However, the trend has been broadening…

To the extent that Taiwanese export orders act as a bellwether for global trade dynamics, we often monitor the release to gain a sense of the state of the manufacturing cycle. On this front, the October update provided a positive signal. The pace of decline…

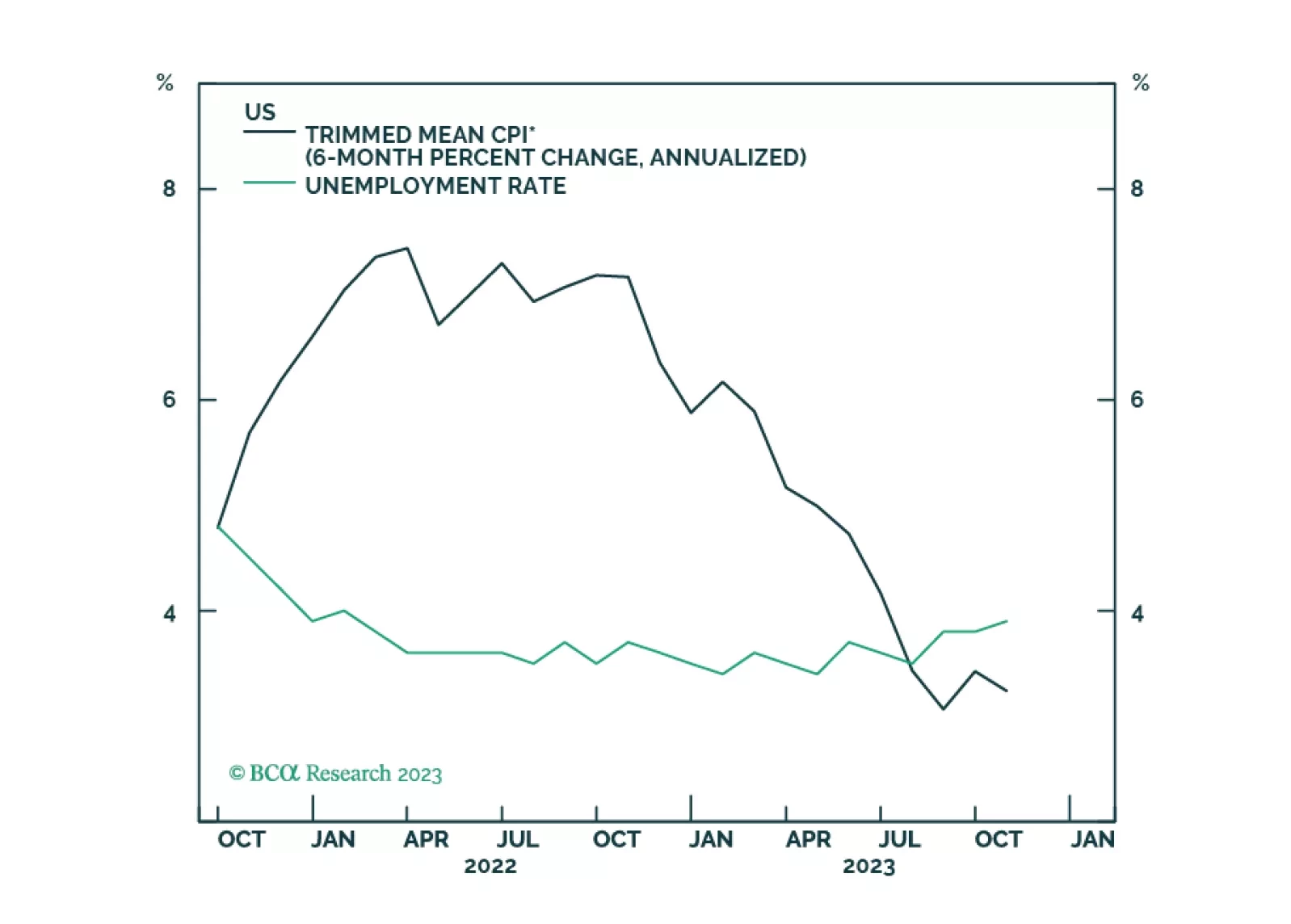

The soft-landing narrative is gaining momentum, pushing equities higher and potentially offering investors a better entry point to position against it. Financial markets appear to have been surprised by the comforting inflation picture painted by the…

According to BCA Research’s European Investment Strategy service, the Magic Eight are the European counterpart to the US’ Magnificent Seven. The dominance of the so-called Magnificent Seven in the US S&P 500 is well-documented. Europe has its own…

Recent data releases have painted a mixed picture of US housing market dynamics. On the one hand, housing starts and building permits unexpectedly increased on a month-on-month basis in October. After falling in 2022, housing starts have somewhat…

Oil prices have relapsed despite the supply cuts and the geopolitical volatility stemming from the Middle East. Odds are that global oil demand is downshifting. The chart above illustrates that there is a tight relationship between crude oil prices and the…

The latest house price data indicate that China's housing market remains weak. The prices of newly built homes across 70 medium and large Chinese cities declined by 0.4% m/m in October – a faster pace of decline than the 0.3% m/m drop registered in September…

The US retail sales release delivered a mixed signal about US consumption. Although the headline figure contracted by 0.1% m/m in October, it was better than expectations of a 0.3% m/m decline. Moreover, the September increase was revised up from 0.7% m/m to…