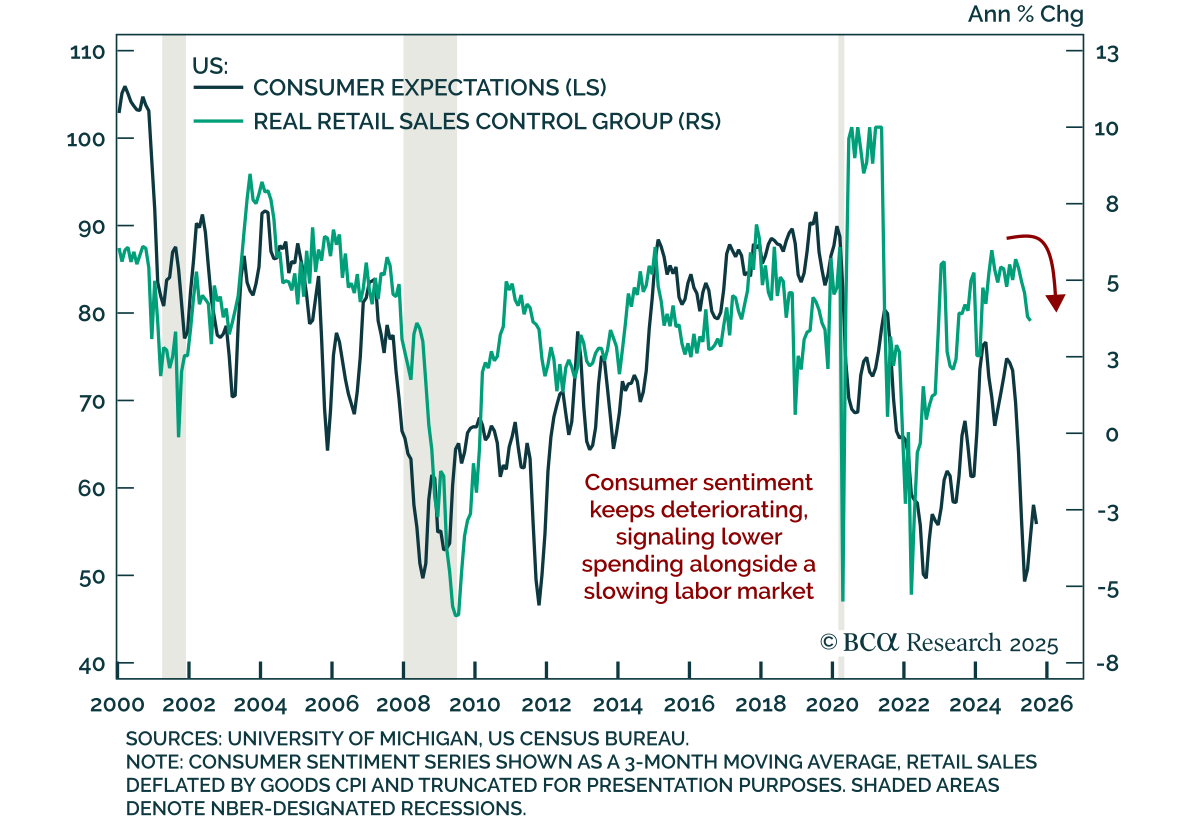

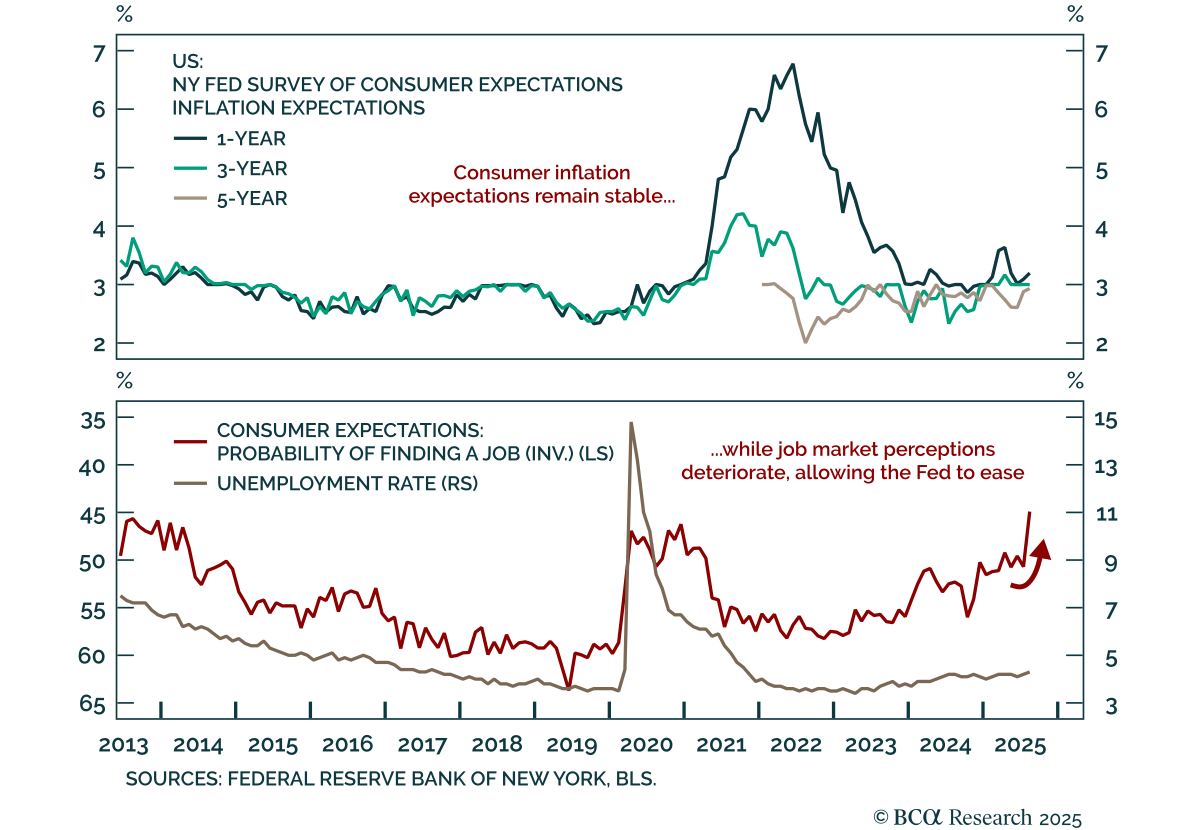

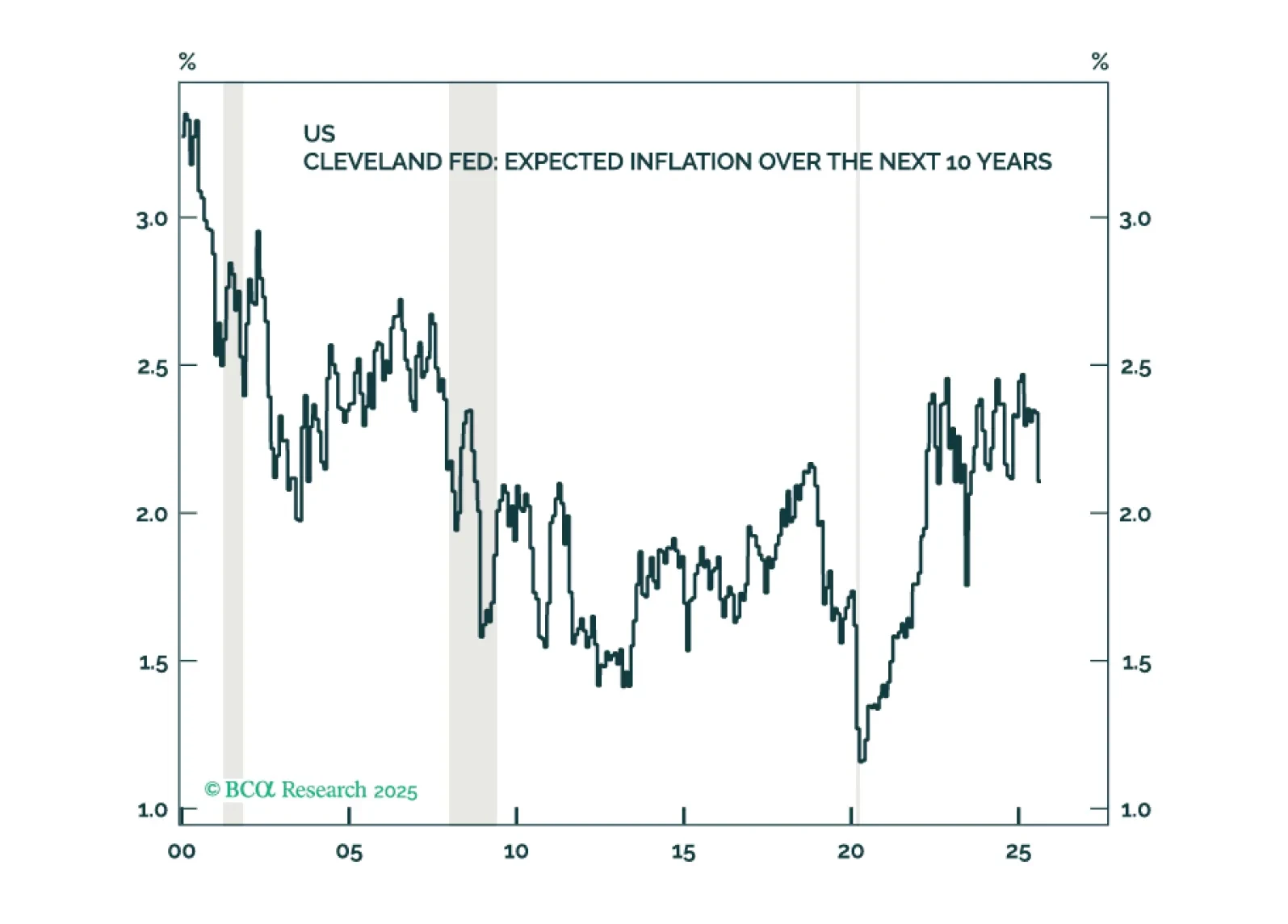

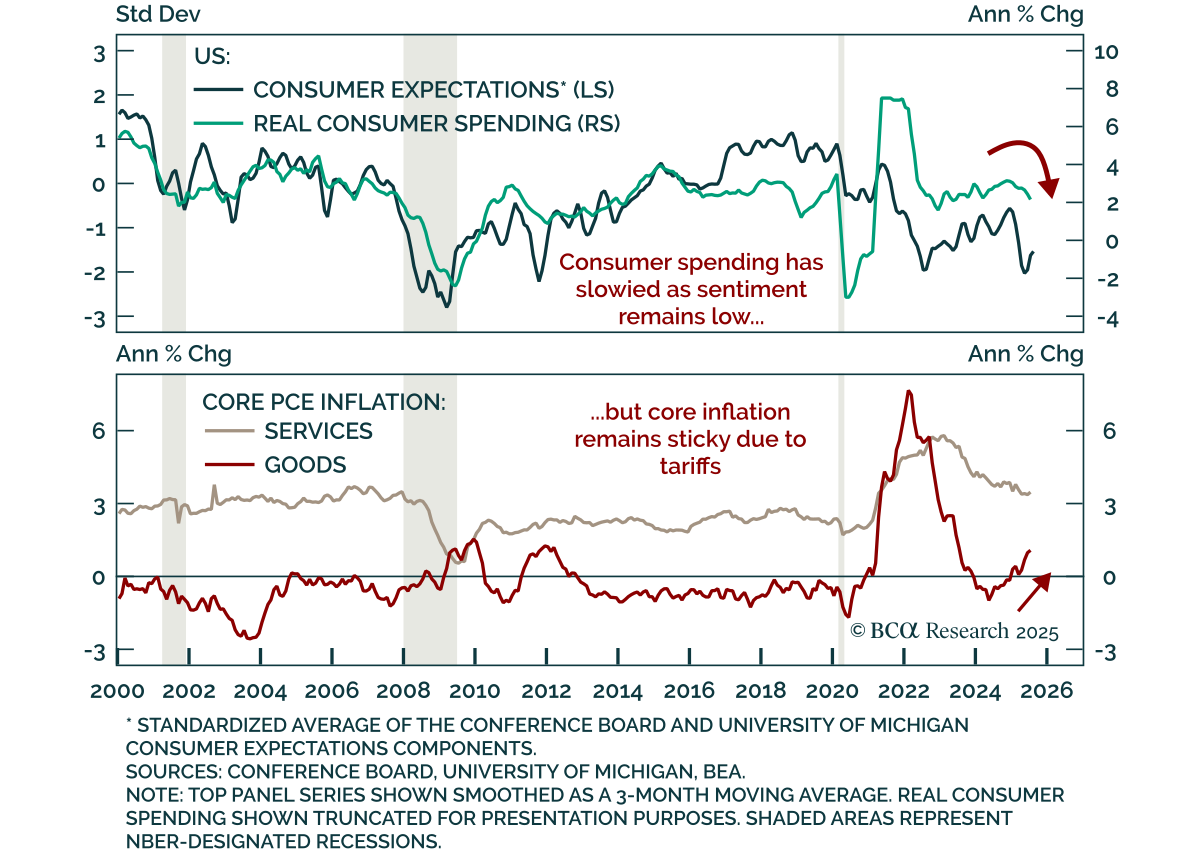

Consumer

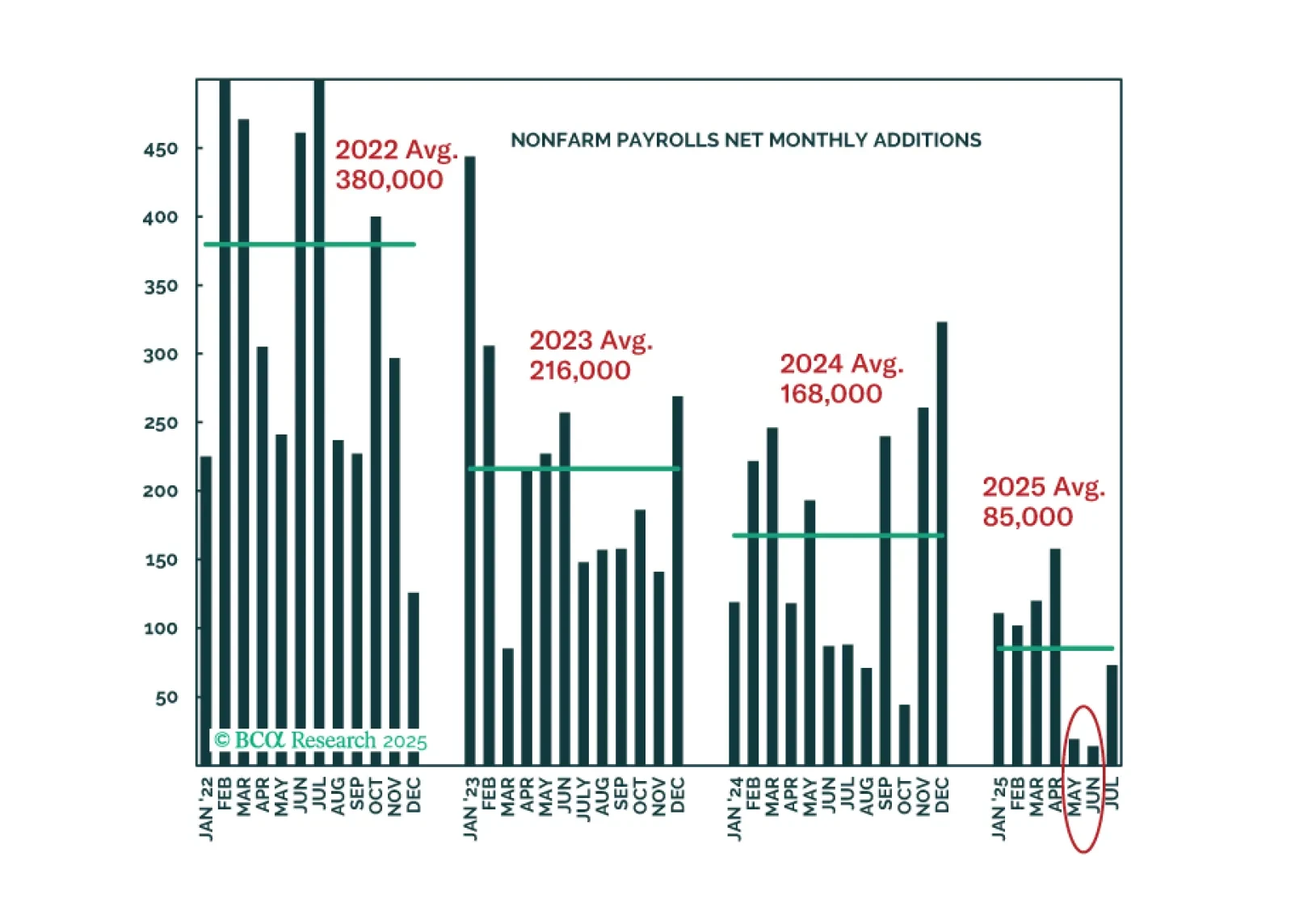

While it is not yet time to bet against risk assets, we push back on the increasingly popular ideas that the wealthiest households and/or AI-related capex can keep the expansion going despite the wobbling labor market.

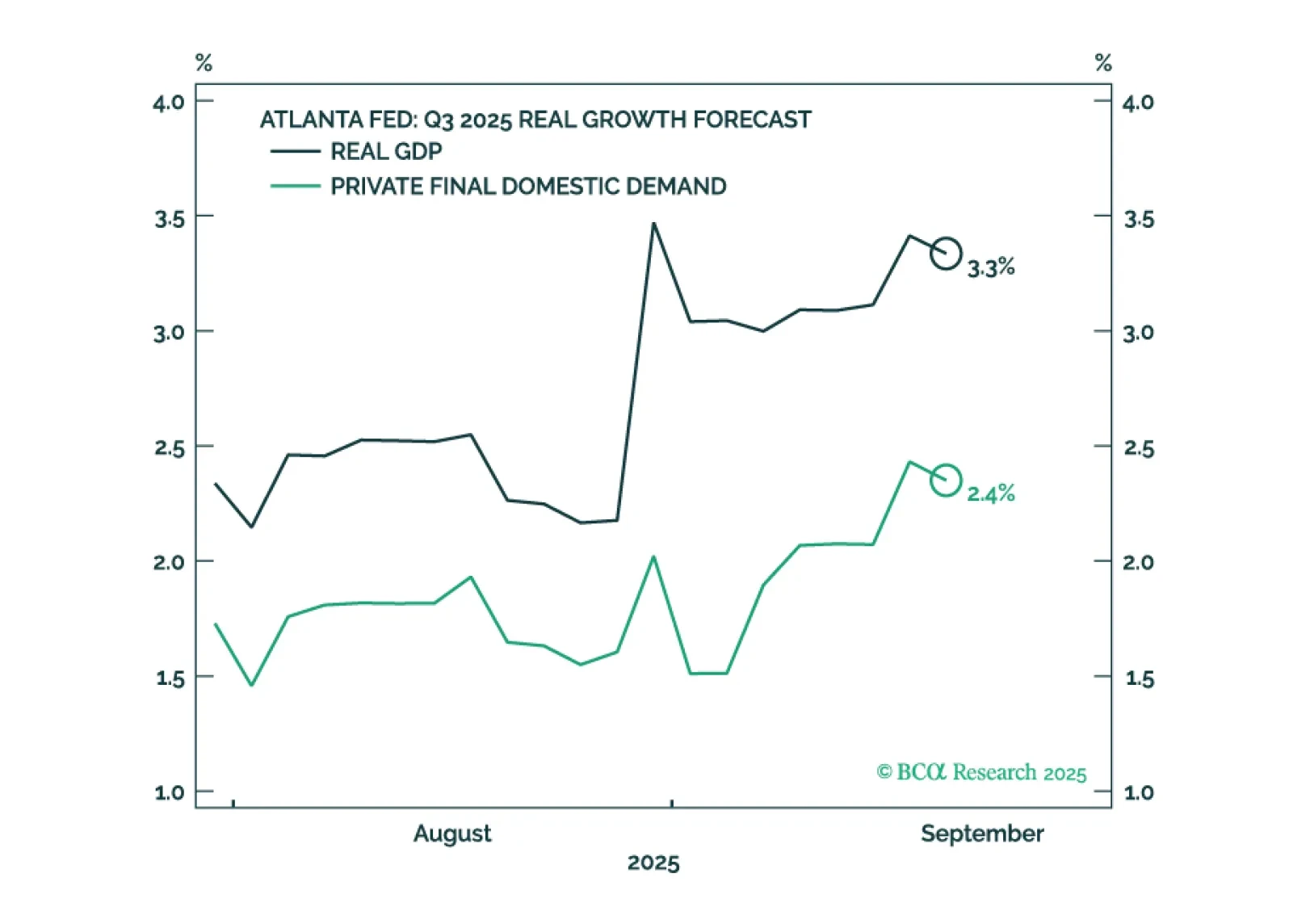

US GDP growth appears to have accelerated even as employment growth has faltered. We will make a final decision in early October when we publish our next Strategy Outlook, but most likely, we will cut our 12-month US recession probability to 40%-to-50% from 60% and turn tactically neutral on stocks, while still retaining a modest equity underweight over a 12-month horizon.

Inflation expectations in the US remain reasonably well anchored and there are few signs of a brewing wage-price spiral. Thus, the near-term risks to growth outweigh the risks of higher inflation. Looking beyond the next year or two, however, we are worried about stagflation.

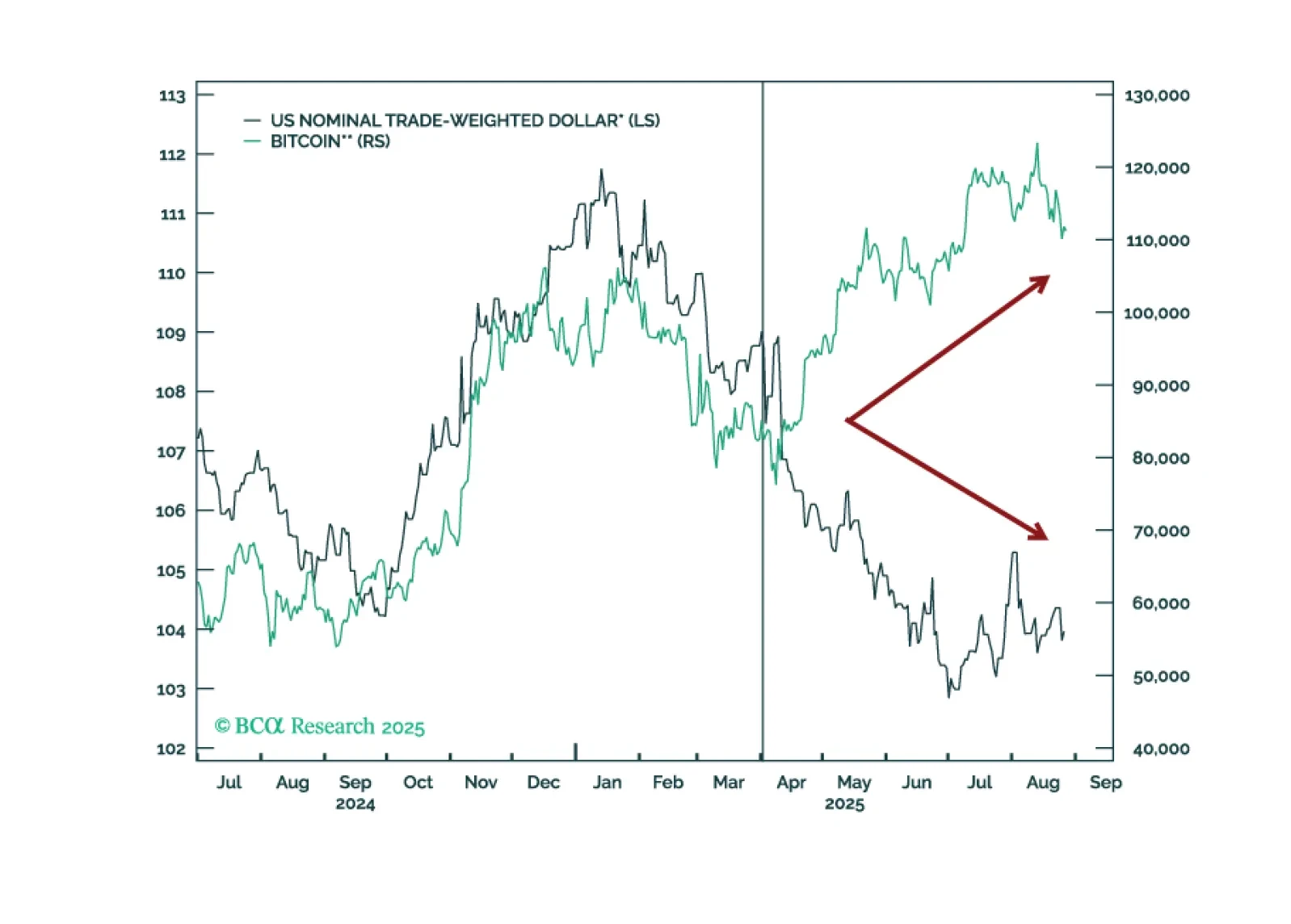

In Section II, Chester reviews the outlook for stablecoins, cryptocurrencies, and central bank digital currencies.

In Section I, Doug notes that a negative stance toward stocks will require a meaningful and imminent deterioration in the US macro data given the ongoing impact of AI optimism on the global equity market. In Section II, Chester reviews the outlook for stablecoins, cryptocurrencies, and central bank digital currencies.