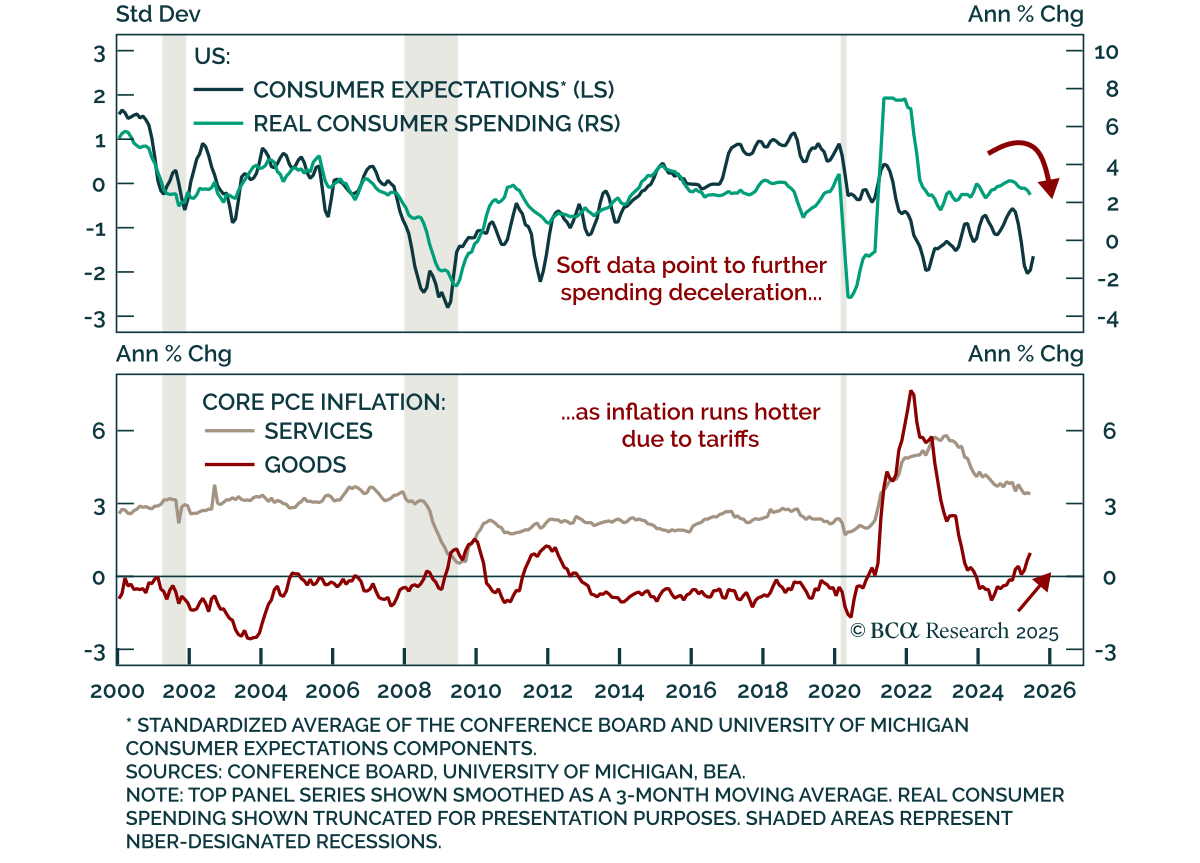

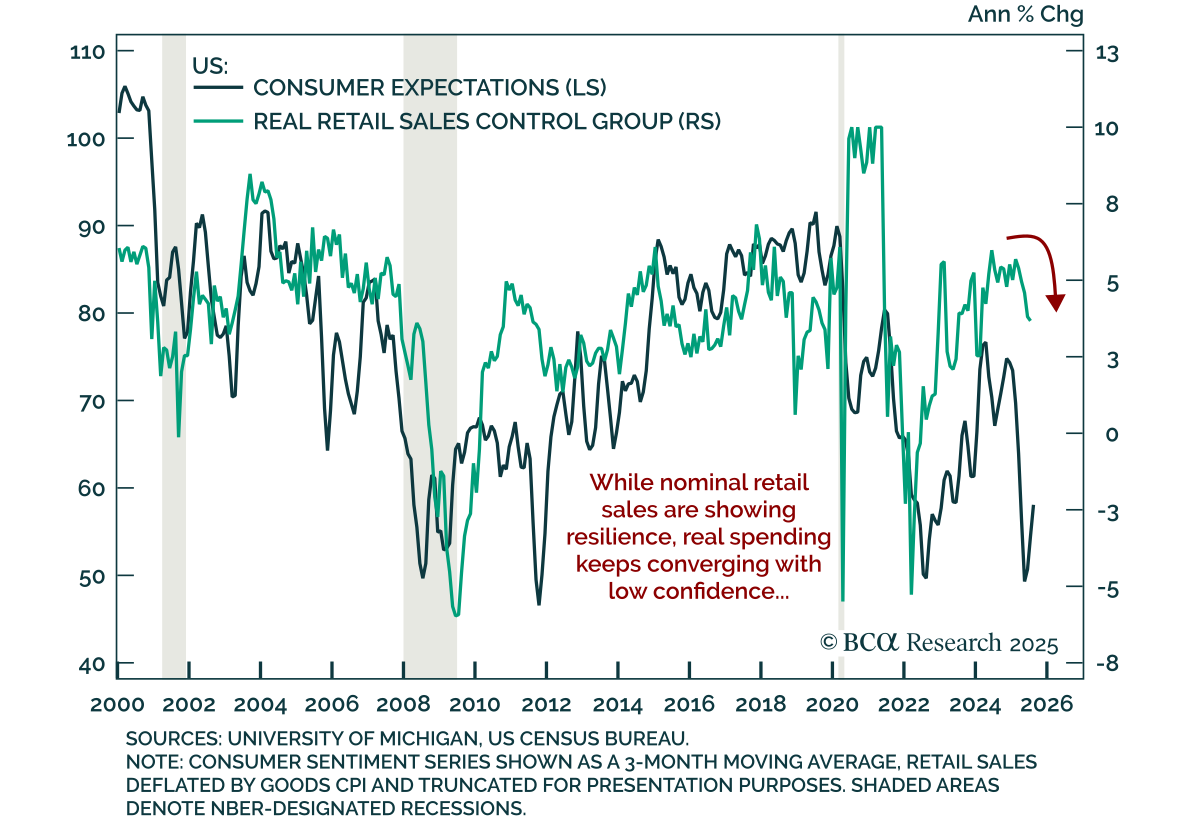

Consumer

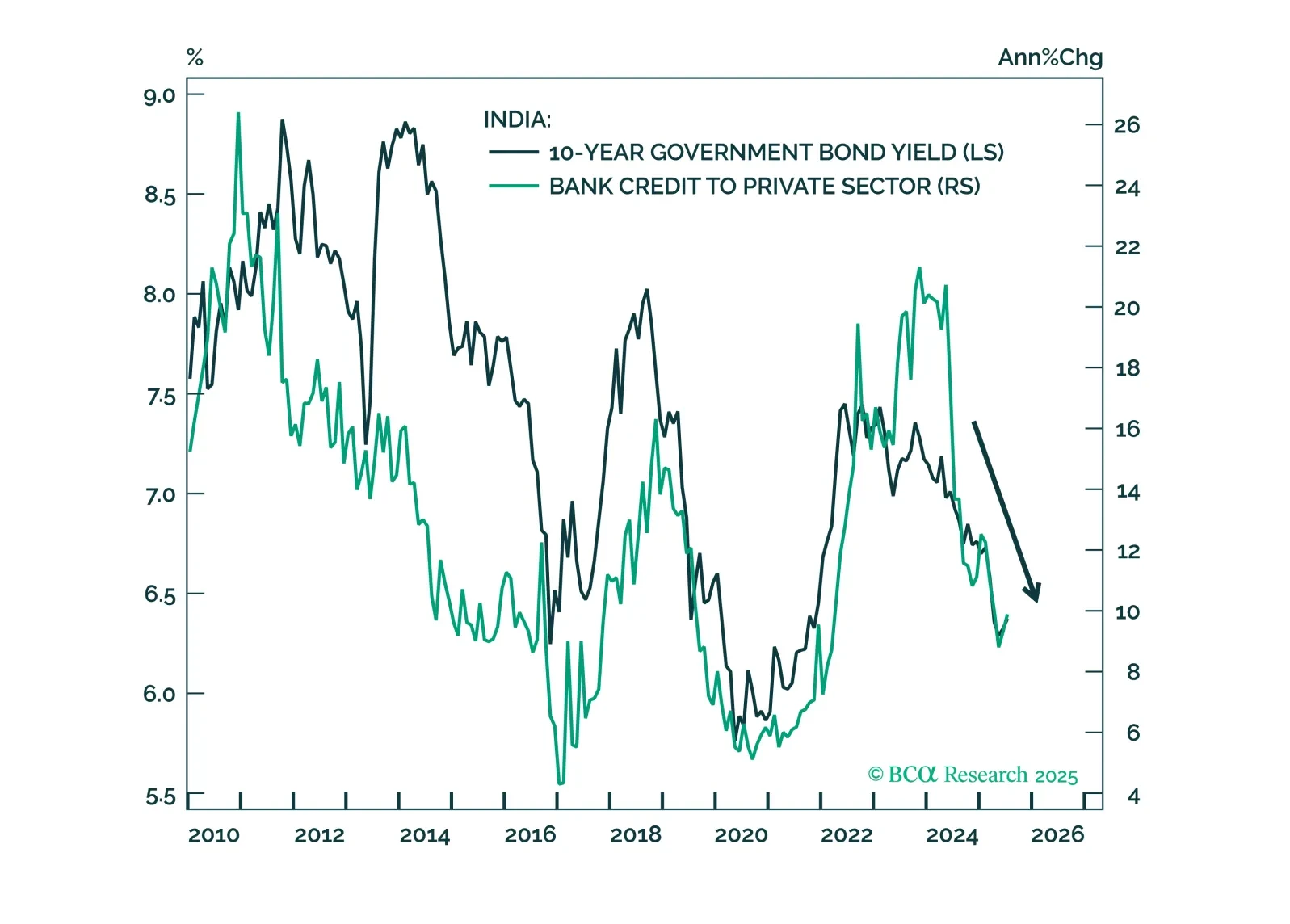

The Indian rupee remains vulnerable to further depreciation amid slowing growth, tight domestic policy, and fragile capital flows. Trade risks and a weakening external balance will likely keep INR underperforming EM Asia peers.

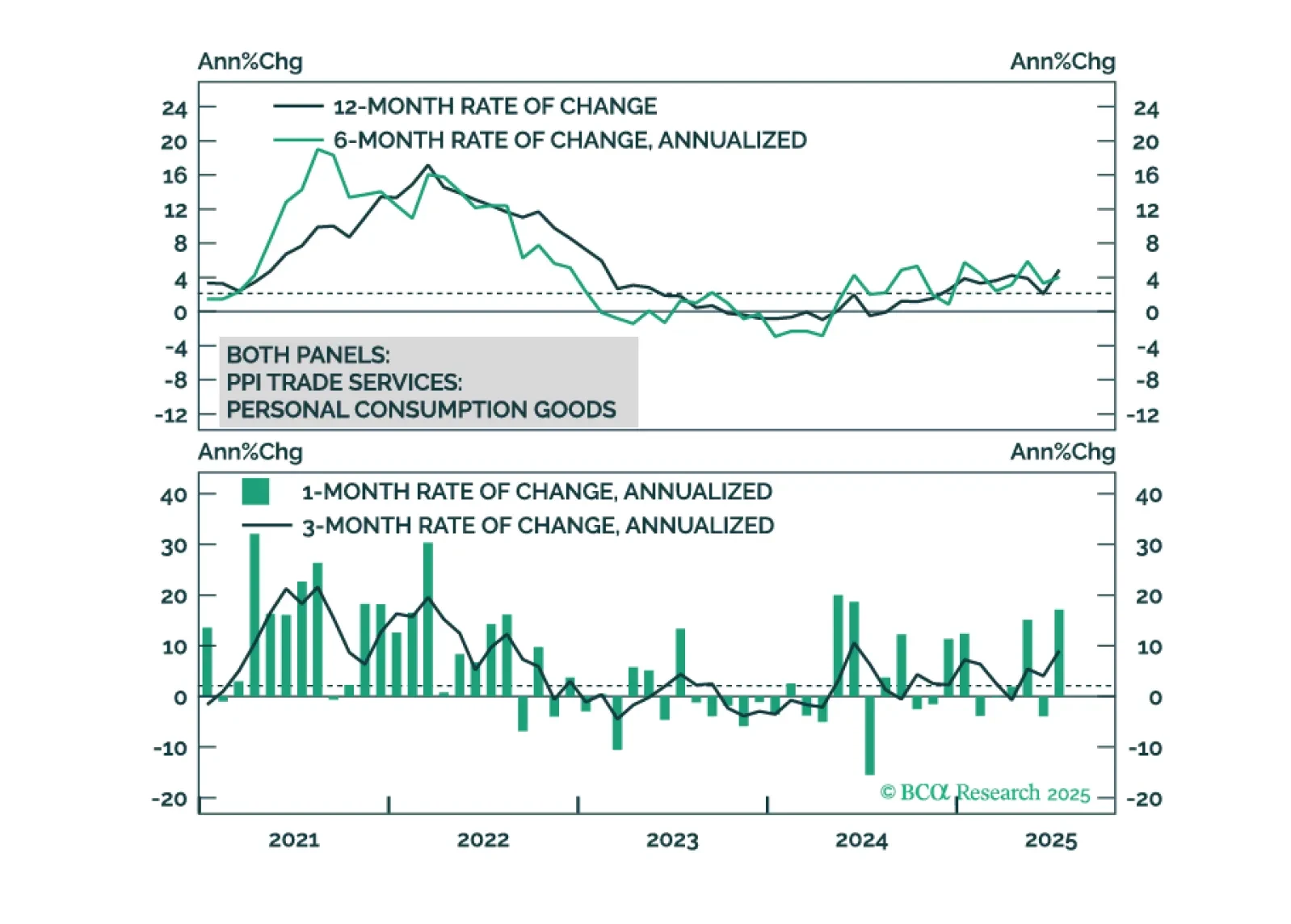

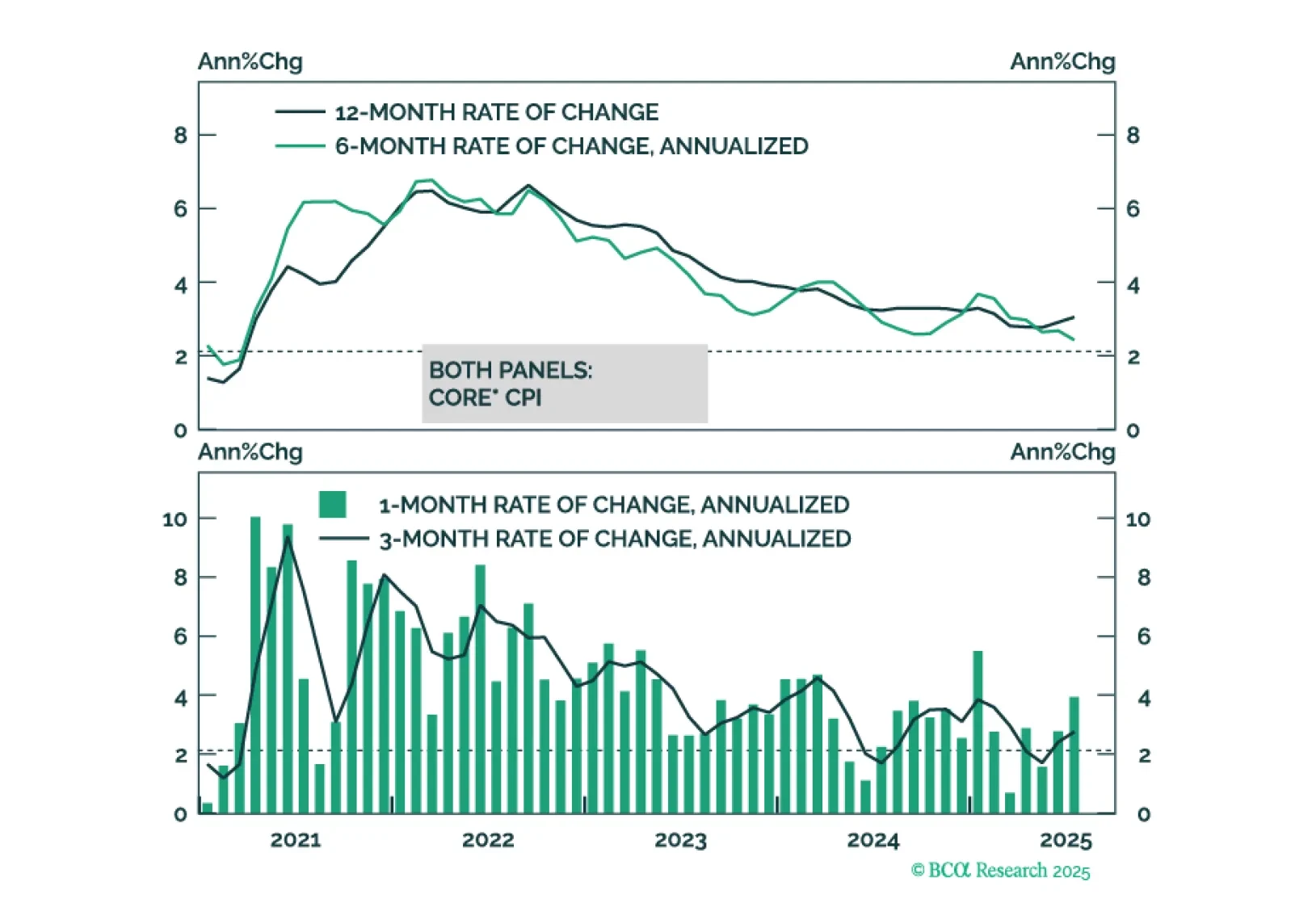

The cost of tariffs is falling on the US consumer, not foreign exporters or US firms.

This morning’s CPI report marginally tips the scales in favor of a September rate cut.

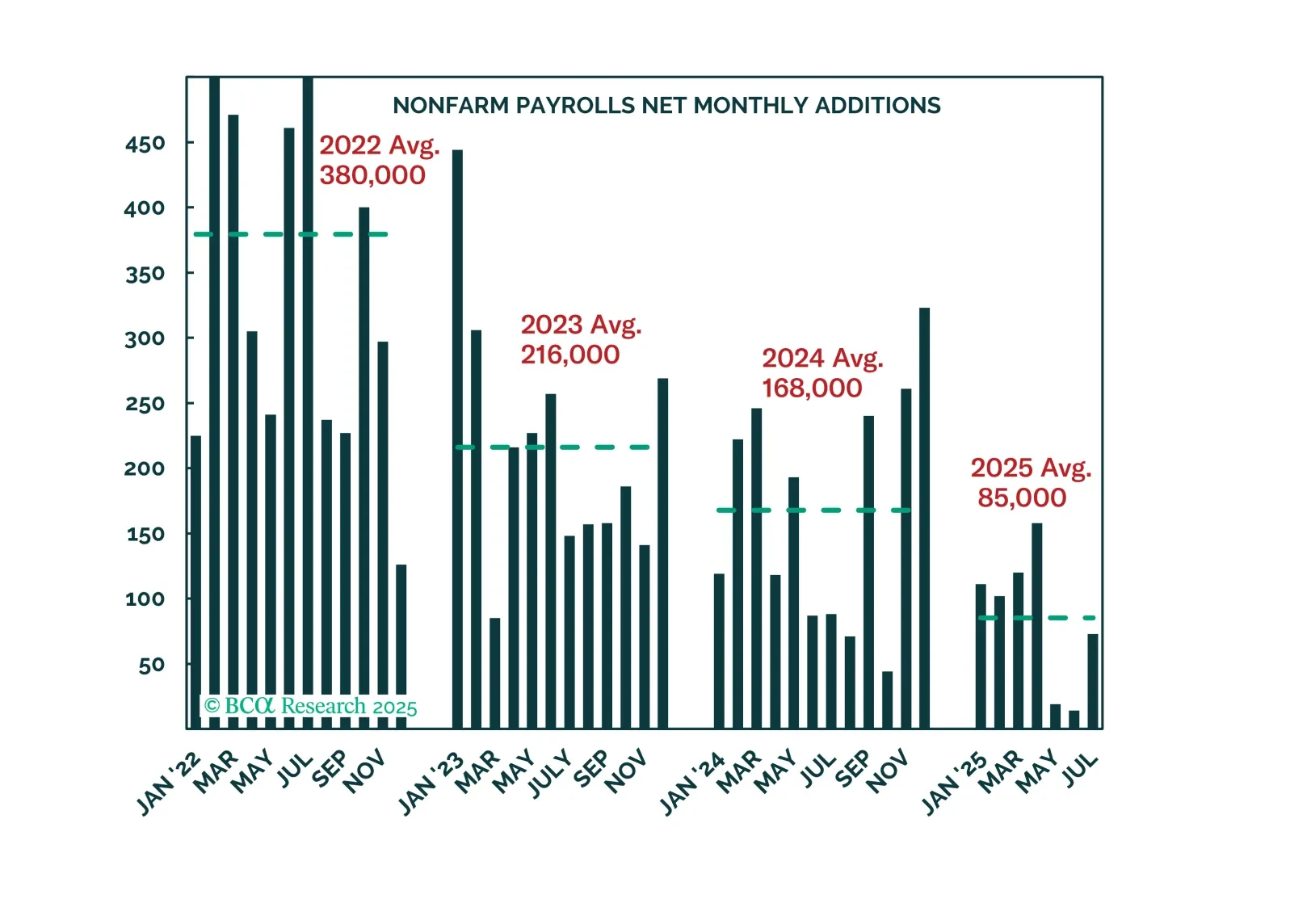

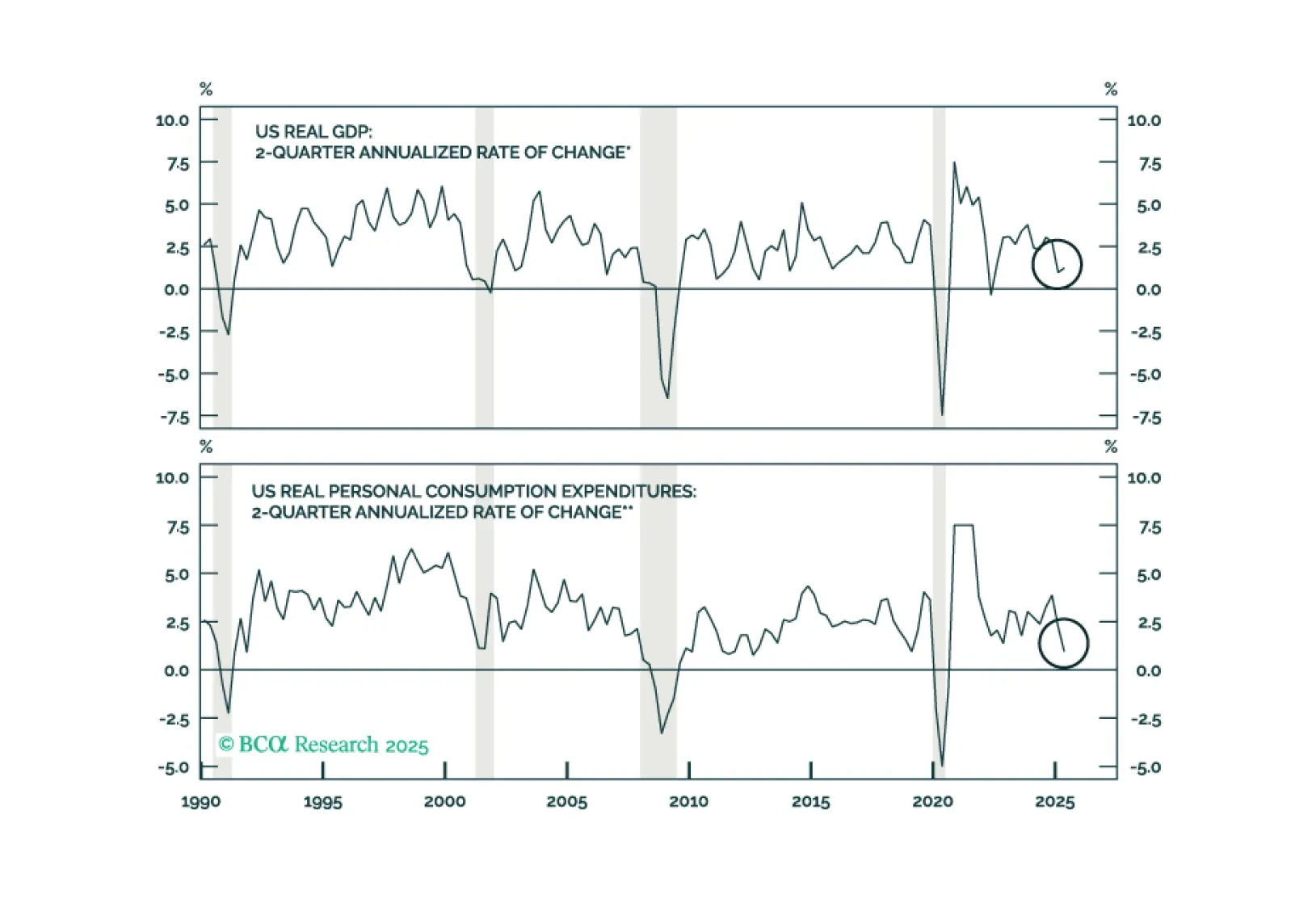

Data received since we began reassessing our bearish stance supported our notion that the economy is not as strong as the investor consensus perceives. But the softness will likely have to intensify in July and August to preserve our defensive recommendations.

We maintain our 12-month US recession probability at 60%. However, until the “whites of the recession’s eyes” are more clearly visible, we would refrain from moving to a fully defensive stance.

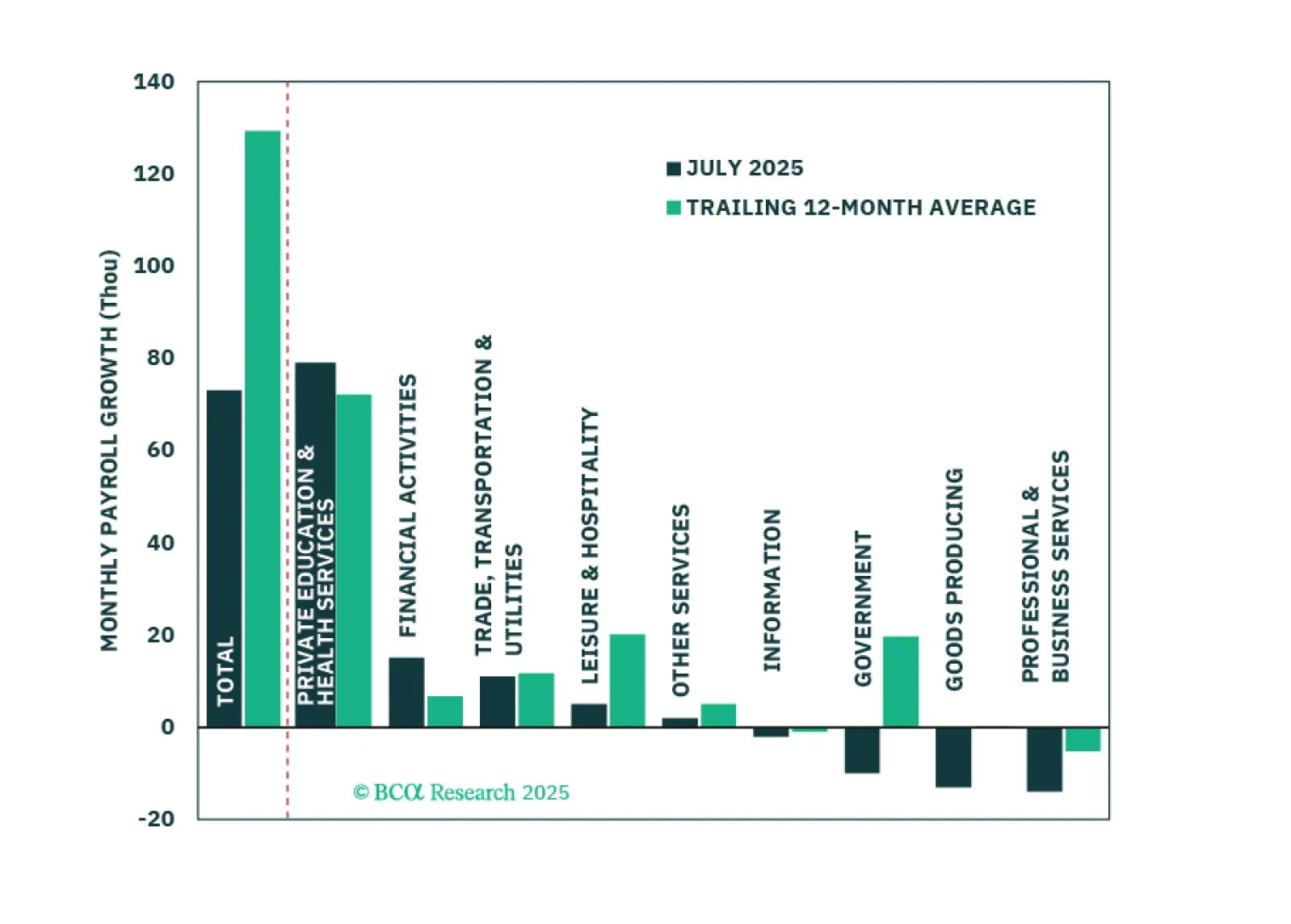

Economic activity and hiring cooled significantly in the first half of the year. The most important question for investors is whether this signals an imminent increase in labor market slack.

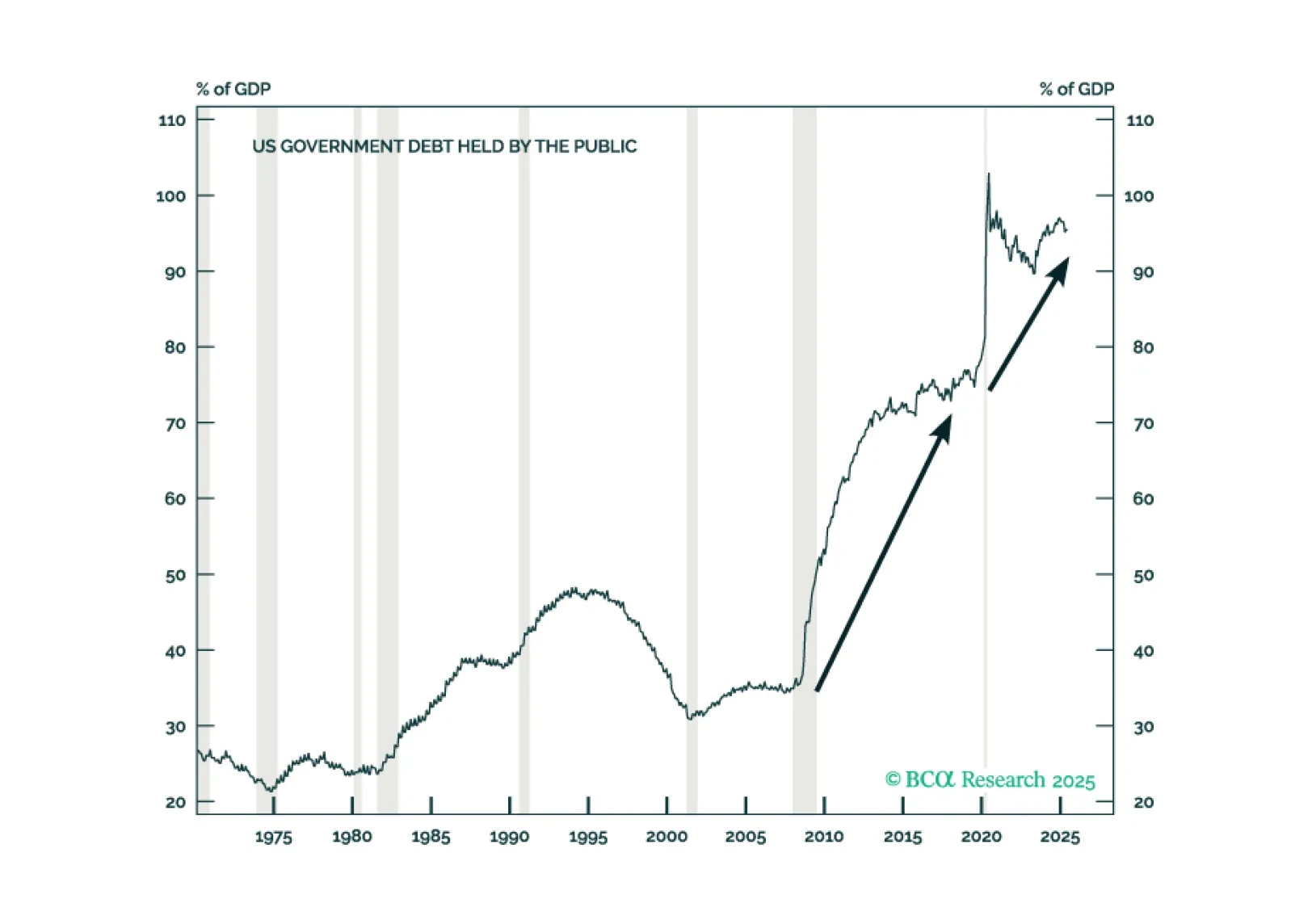

In Section II, Jonathan reviews the US fiscal outlook in the wake of the passage of the OBBBA.

In Section I, Doug weighs the recent reduction in trade uncertainty against the clear signs of labor market and consumer weakness. In Section II, Jonathan reviews the US fiscal outlook in the wake of the passage of the OBBBA.