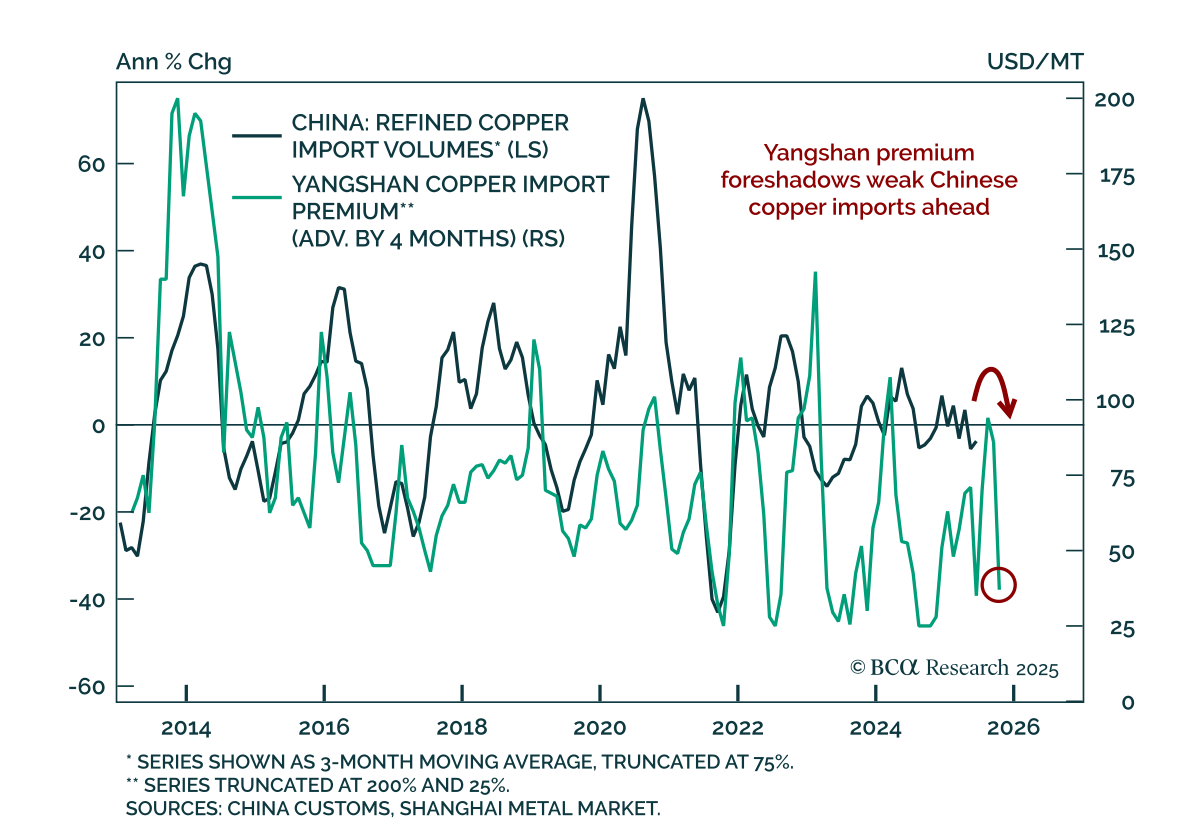

Copper

U.S. copper tariffs will redirect the metal’s trade flows from the US to the rest of the world, replenishing depleted inventories abroad. With global copper demand set to soften in H2, the red metal will likely face downward price pressure outside the US.

Stay long gold / short LME copper, and initiate an outright LME copper short.

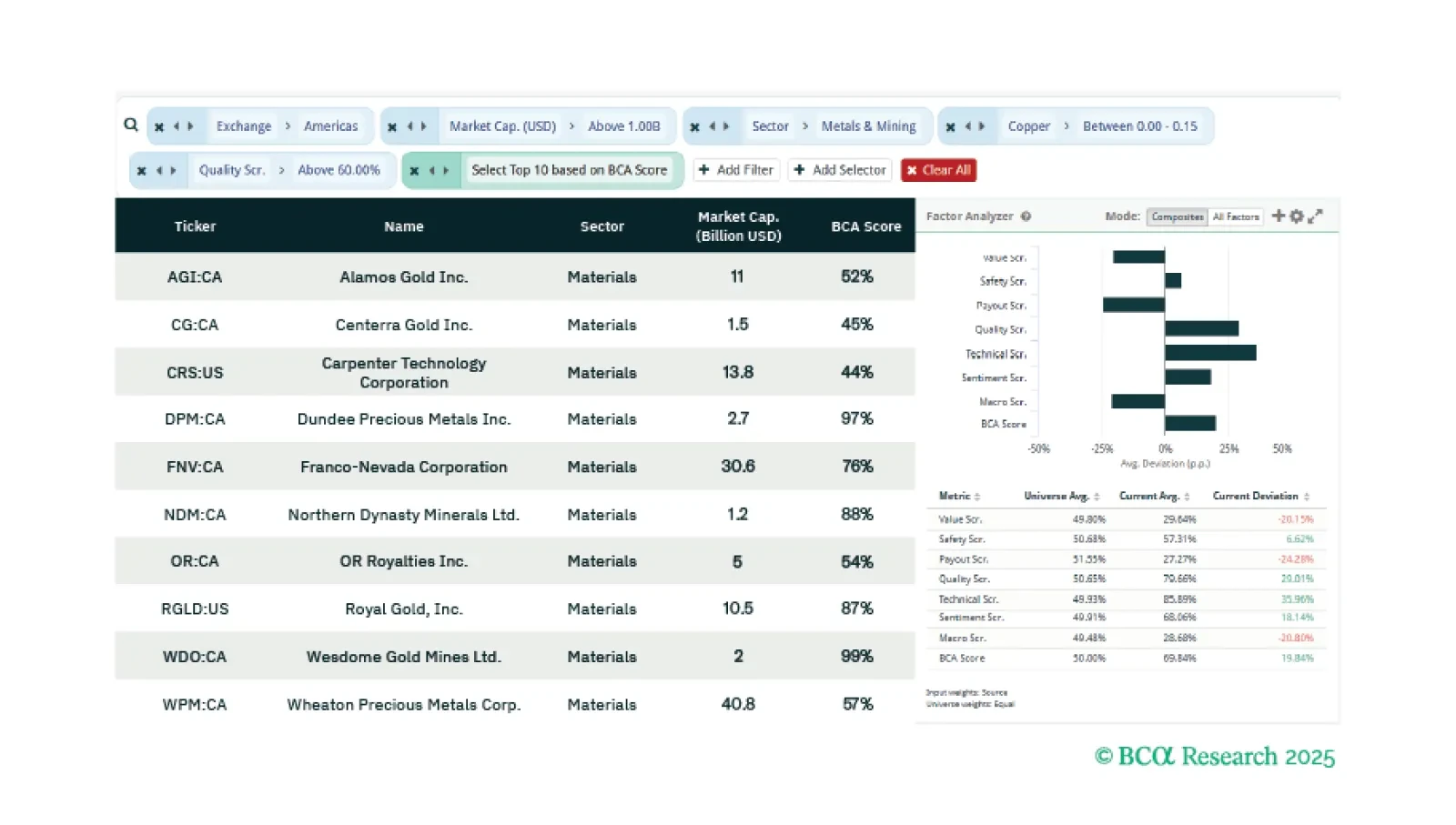

This week our three screeners identify equity plays on copper prices, stocks that are considered “boring” but are solid earners during heightened uncertainty, and stocks which are positively correlated with Bitcoin.

An update on the key themes and views that will shape commodity markets through the remainder of 2025.

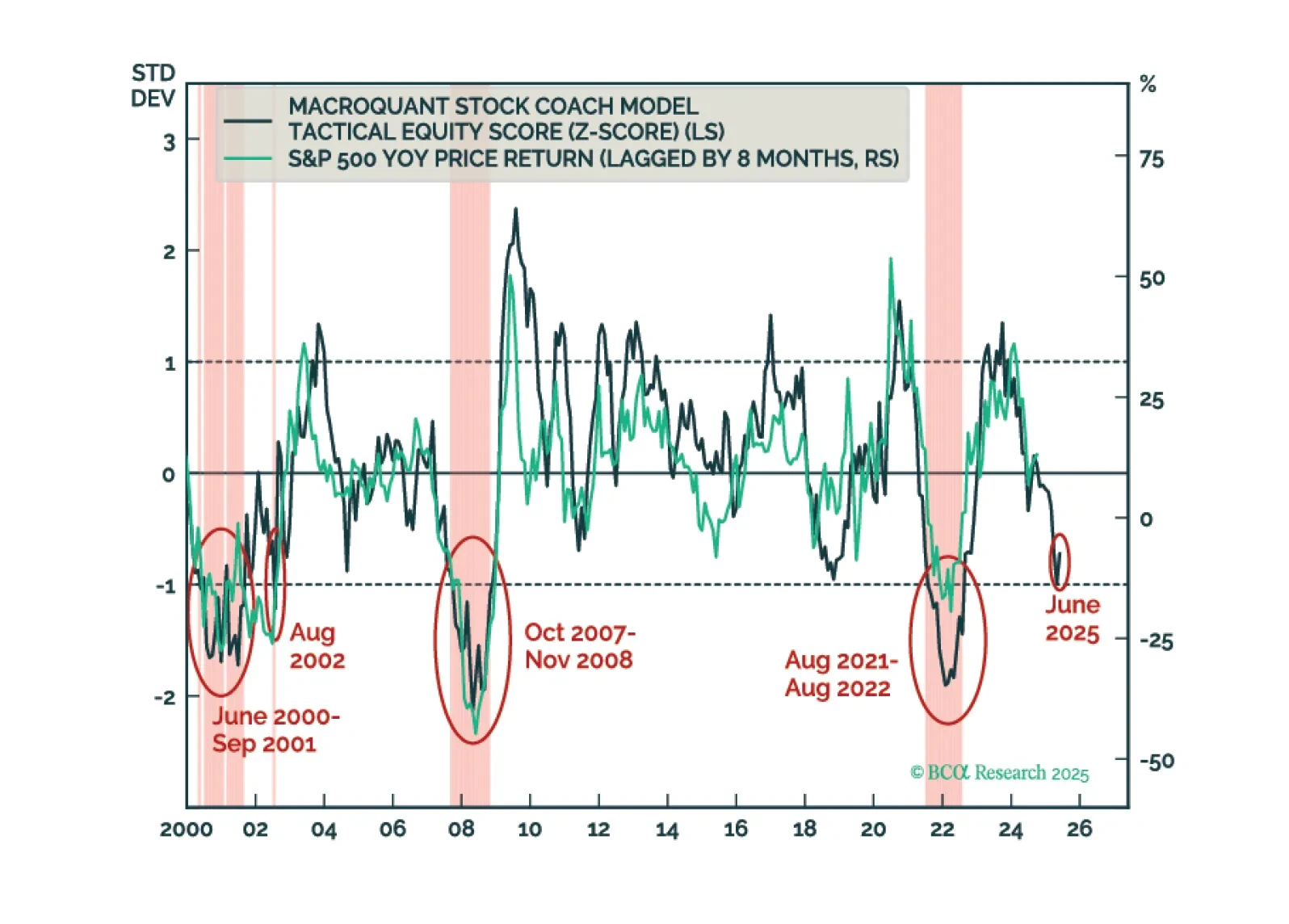

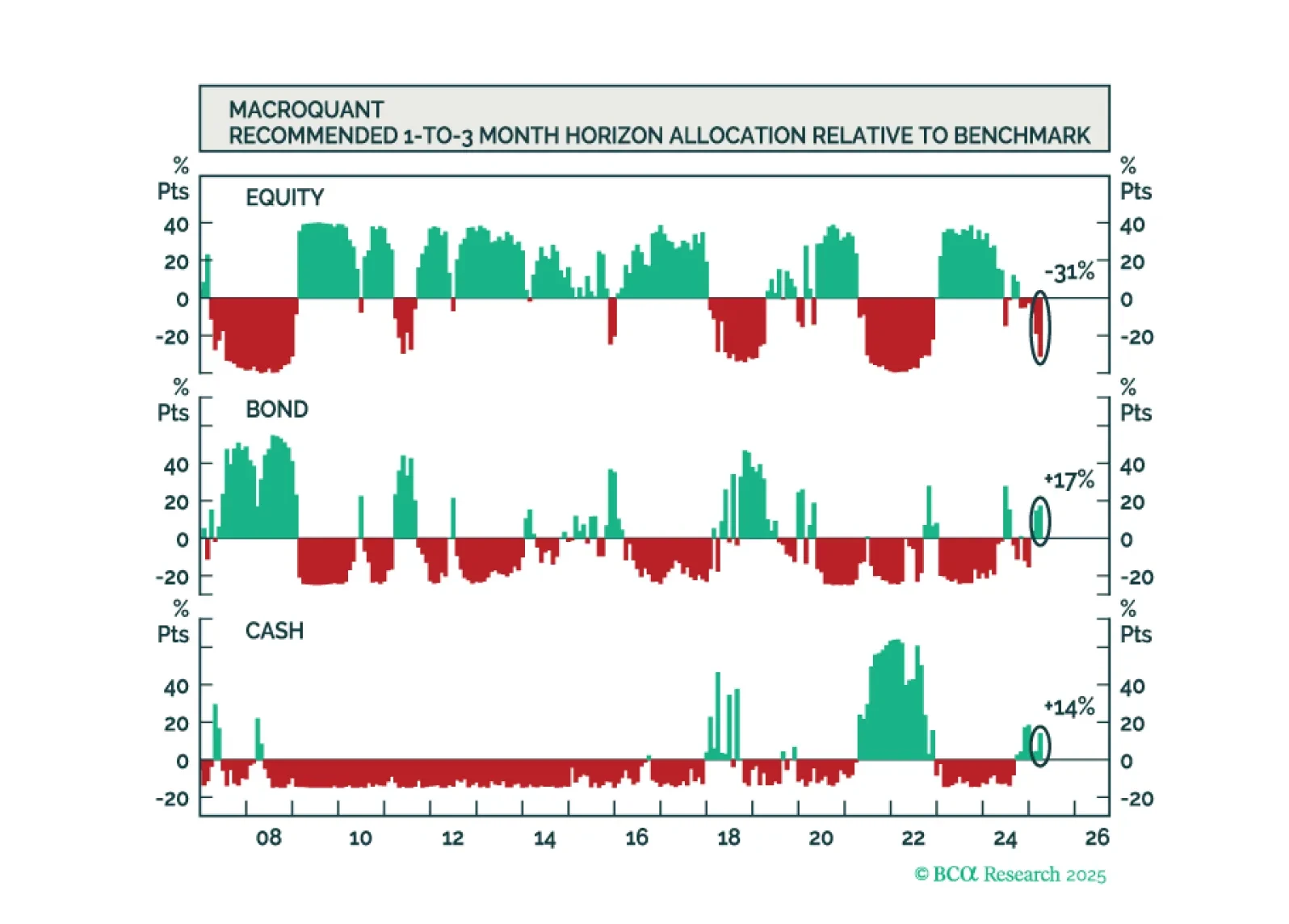

MacroQuant’s US equity z-score is dangerously close to the -1 threshold. Moves below that threshold have reliably coincided with equity bear markets in the past. As such, MacroQuant recommends an underweight on stocks, offset by an overweight on bonds and cash.

Investors should modestly underweight equities in their portfolios and look to turn more aggressively defensive once the whites of the recession’s eyes are visible. We think that will happen within the next few months.

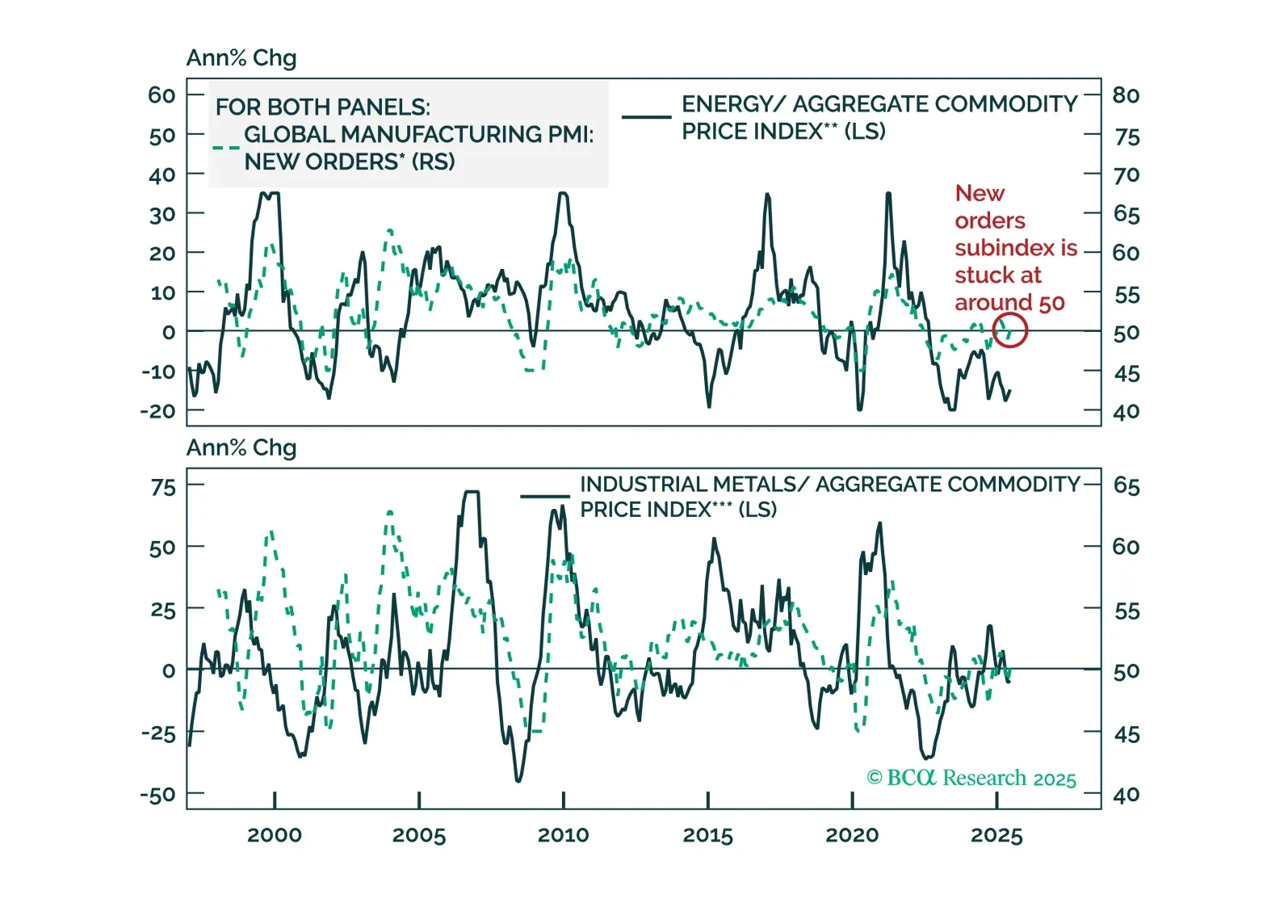

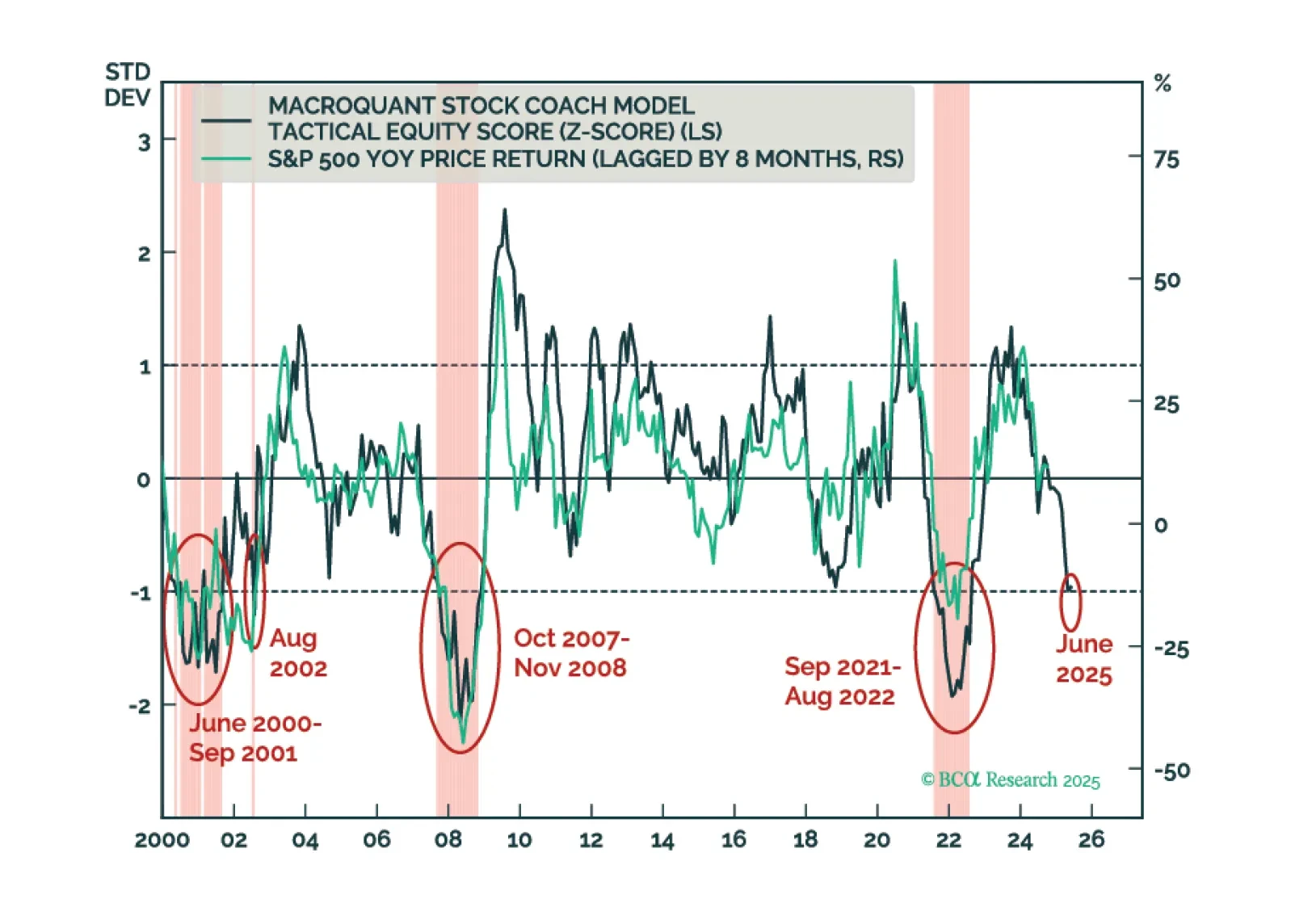

Investors often rely on past relationships to predict future outcomes. This strategy is at risk now that several commodity correlations have broken down. We explore the causes and sustainability of the new commodity relationships.

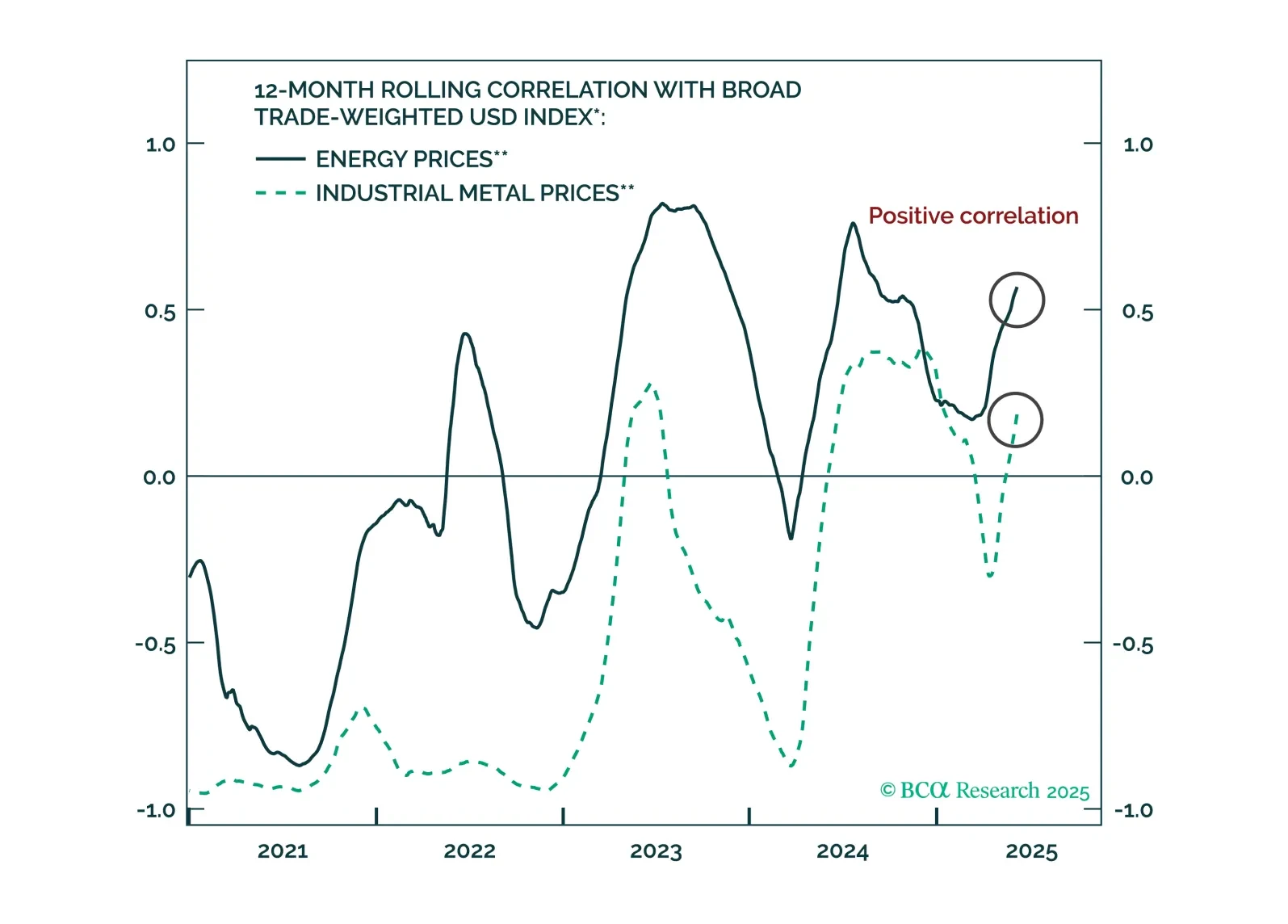

Oil, copper, and gold futures curves have recently experienced abnormal shifts and twists. Brent is no longer fully backwardated, copper curves on the LME and CME have diverged, and gold is in a steep contango.

We examine the drivers and implications of these shifts for prices and curve structure across the three commodities.

MacroQuant sees the risks to US growth as being to the downside and the risks to inflation as being to the upside. Such a stagflationary brew justifies an underweight on stocks.

MacroQuant sees the risks to US growth as being to the downside and the risks to inflation as being to the upside. Such a stagflationary brew justifies an underweight on stocks.