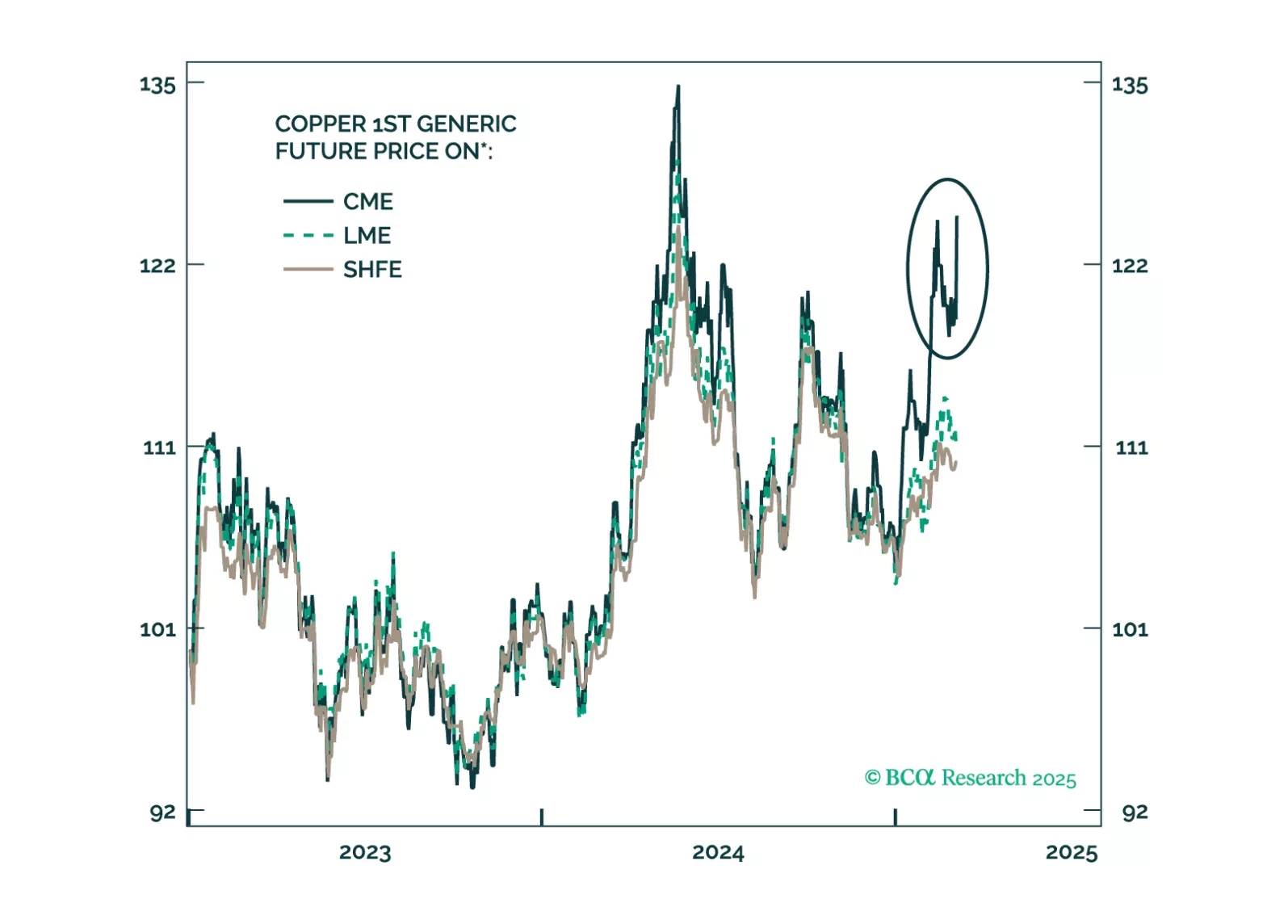

Copper prices in New York shot higher on Wednesday amid concerns that US imports of the red metal will face a 25% tariff. The catalyst for the renewed concern is President Trump’s comments during his Tuesday night speech: “And I have also imposed a 25% tariff on foreign aluminum, copper, lumber and steel, because, if we don’t have, as an example, steel and lots of other things, we don’t have a military, and frankly, we just won’t have a country very long.”These comments follow last week’s Executive Order directing Commerce Secretary Howard Lutnick to conduct a Section 232 investigation into whether copper imports are a threat to national security. The investigation could take months. The Commerce Department has up to 270 days to issue a recommendation after which the president has 90 days to make a decision followed by a 30 day period to implement the decision. However, White House Trade Advisor Peter Navarro has stated that the investigation would be completed in “Trump time,” suggesting that a decision will be made over a much shorter timeframe. Efforts to draw in physical copper to the US ahead of potential tariffs have driven the Comex copper price surge. Case in point, the price in New York has jumped significantly above prices in London and Shanghai, where the copper rebounds have been tame (Chart 1). The implication is that the CME copper price has disconnected from supply-demand fundamentals. If the US imposes tariffs on copper, price signals from the LME and SHFE will temporarily be more pertinent than CME ones. If Trump decides against imposing tariffs, the price of the red metal in New York will face downside pressure. Regarding the likelihood of tariffs on US copper imports, President Trump’s Executive Order raises the odds that tariffs will be imposed. Nevertheless, it is worth highlighting the lack of a strong case for these tariffs. The Section 232 investigation will encompass all forms of copper (mined, concentrates, refined, alloys, scrap, and derivatives). Yet the US is much more import-dependent on refined copper than on mined copper. The US has become increasingly dependent on refined copper imports over the past decade, with net imports now accounting for 45% of US copper consumption (Chart 2). Meanwhile, the US is a net exporter of copper ores and concentrates, with foreign sales accounting for nearly a third of its copper ores and concentrates production (Chart 3).This means that the Trump administration is determined to promote an increase in US refined copper production. Ergo refined copper imports are more likely to face tariffs than copper ores and concentrates.Indeed, the Executive Order highlighted that “the United States has ample copper reserves, yet our smelting and refining capacity lags significantly behind global competitors.”Importantly, the reason why the US is a net exporter of copper ores & concentrates and a net importer of refined copper is because it lacks domestic copper refining capacity. According to estimates by Wood Mackenzie, the US refined copper capacity utilization rate stood at 98% in 2024. Since US refiners are already operating at full capacity, tariffs are unlikely to boost US refined copper production over the near term. In other words, refined copper production cannot easily or quickly be expanded.Moreover, imports from China – which the Executive Order singled out as a global competitor to America’s smelting and refining sector – account for a negligible share of US refined copper purchases. Instead, the US sources most of its refined copper imports from Chile (65%), Canada (17%), Mexico (9%), and Peru (6%). Therefore, these countries' copper exports might be at least temporarily impacted in the event that US tariffs are imposed. It is also worth noting that there is less scope for tariffs to boost US production of refined copper compared to steel and aluminum. That is because there is greater domestic steel and aluminum spare capacity that is available to be utilized. The capacity utilization rates for steel and aluminum are 75% and 55%, respectively. The Section 232 tariffs on steel and aluminum aim to boost capacity utilization to at least 80%. Given that refined copper’s capacity utilization rate (98%) already surpasses 80%, an increase in production capacity would be needed to boost refined copper output. This can only be achieved over a longer-term horizon. Bottom Line: The risk of tariffs on US copper imports – not supply-demand dynamics – is behind the copper rally in New York. In the event that tariffs are not imposed, the Comex copper rally will completely unwind. If US tariffs on copper imports are imposed, CME prices will trade at a substantial premium to LME and SHFE prices.Based on President Trump’s remarks in his Tuesday speech to Congress, it seems that the Trump administration’s objective is a substantial revival and expansion in metals refining capacity. The aim is long-term and relates to national security concerns. This raises the odds that copper tariffs will be imposed. Roukaya IbrahimCommodity Strategistroukayai@bcaresearch.com