Corporate

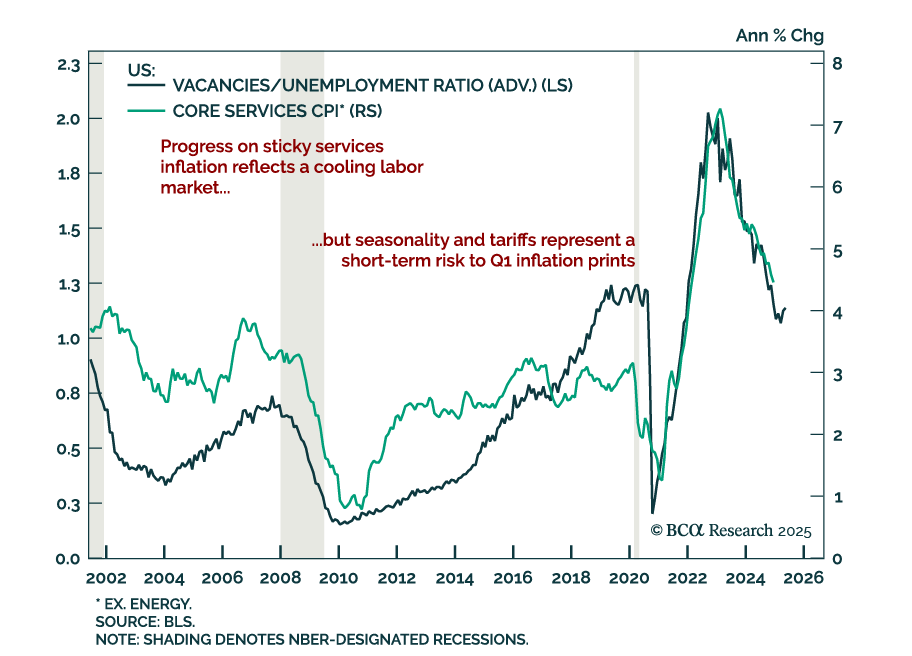

The December US CPI came in better than expected. While headline CPI met estimates of 0.4% m/m (2.9% y/y), core surprised to the downside at 0.2% m/m, decelerating to 3.2% y/y from 3.3%. Moderation in core annual inflation was driven by both goods, which are…

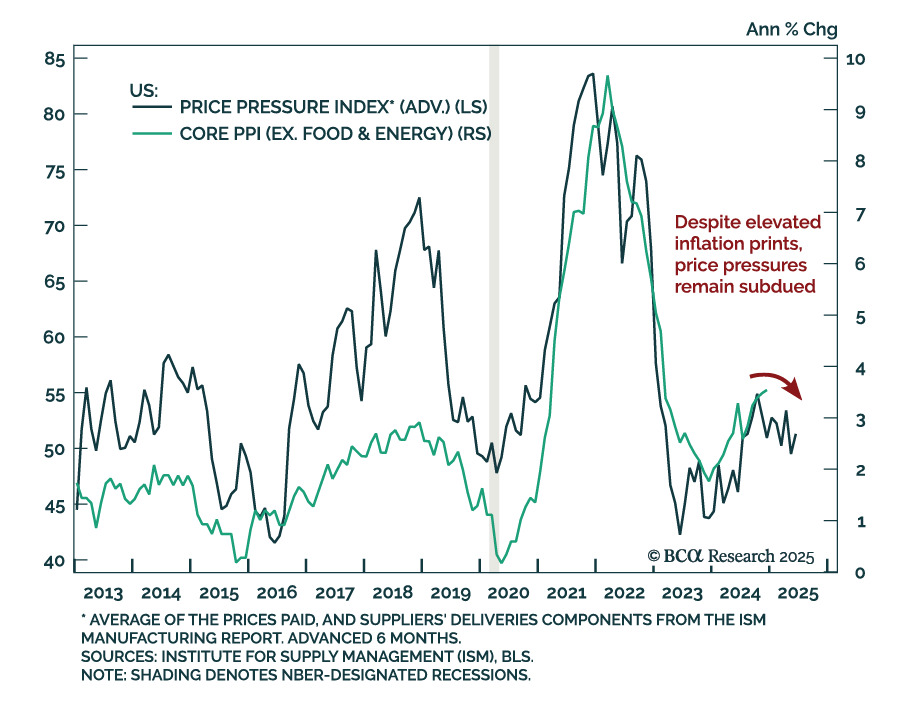

The December US Producer Price Index came in cooler than expected, increasing 0.2% m/m, a deceleration from 0.4% in November. Core PPI, excluding food and energy, was flat after increasing 0.2% a month prior. Inflation is a lagging variable, as…

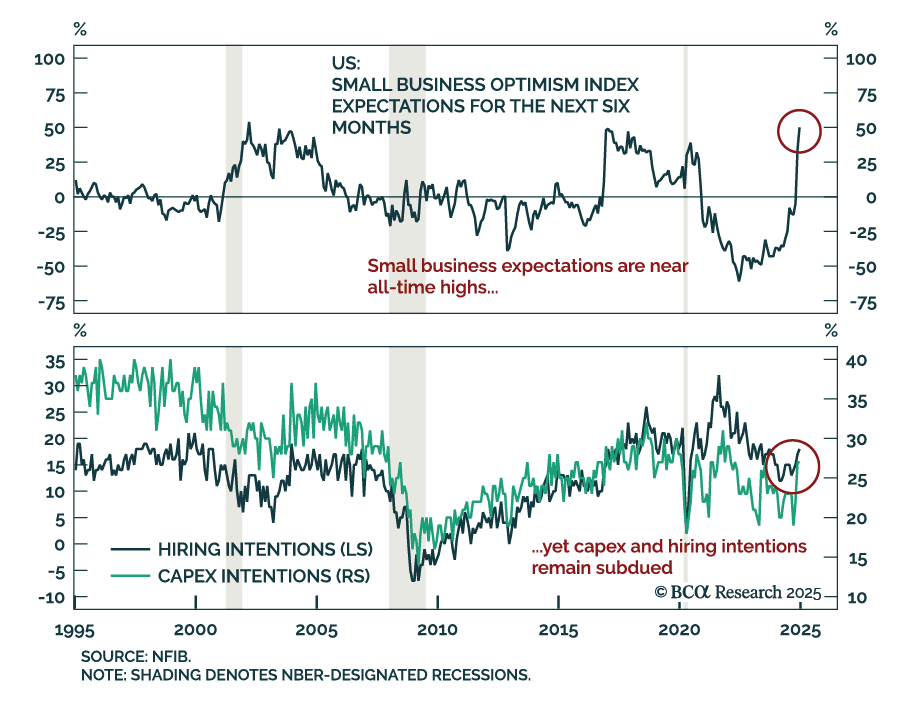

The December NFIB Small Business Optimism Index beat expectations, jumping to 105.1 from 101.7 in November. Most index subcomponents increased, led by measure of expectations, notably for the state of the economy and real sales. After jumping 39 percentage…

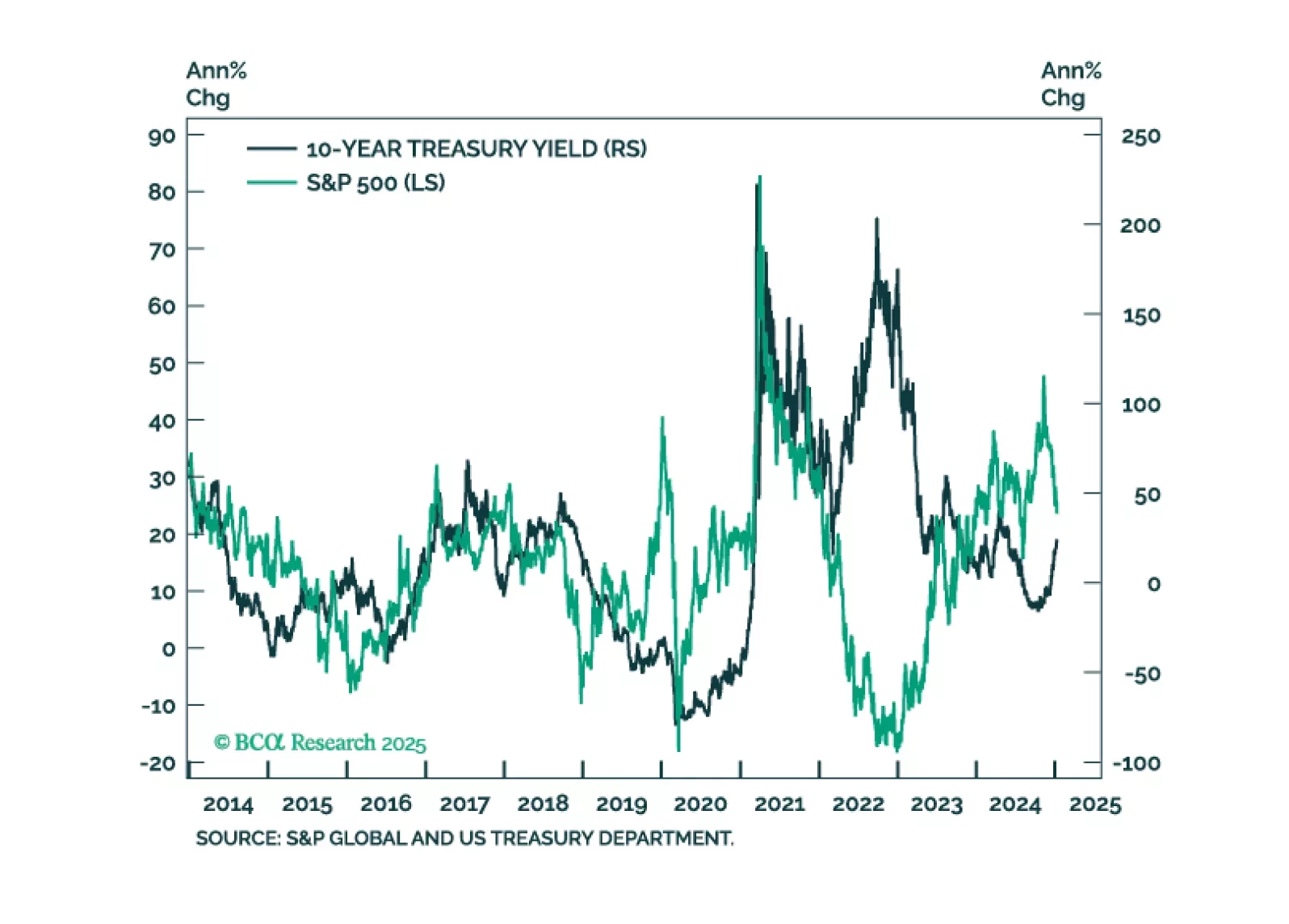

In this first presentation of 2025, we start with an overview of the 2025 outlook webcast polls, and a brief post-mortem of the 2024 market performance. Then, we shift gears and examine what is behind the recent surge in bond yields and its implications for equities. We also review market technicals and positioning and conclude with a list of trades to prepare our portfolio for continued moves in yields.

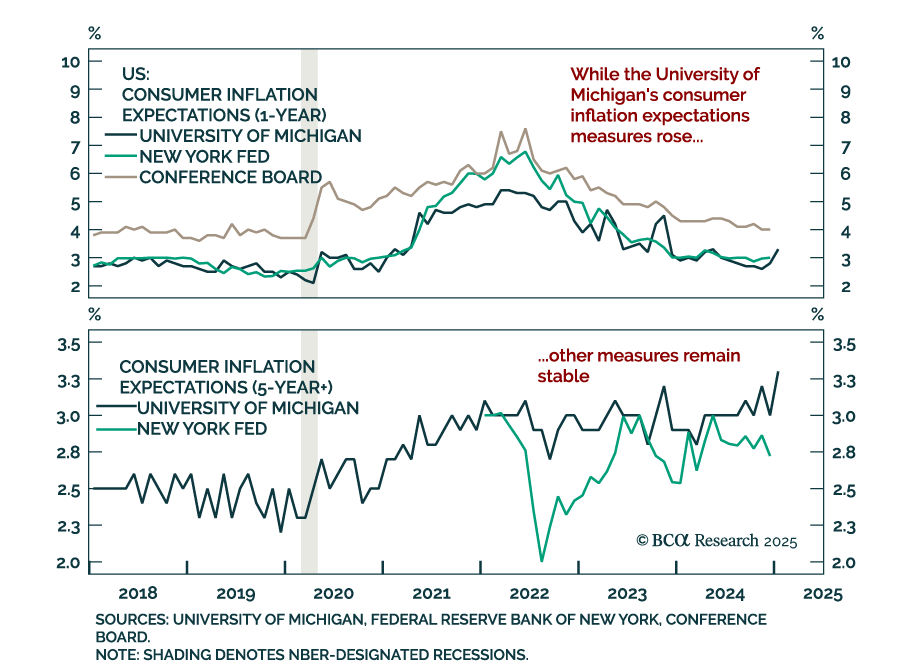

The preliminary January University of Michigan Consumer Sentiment Index missed estimates on Friday, driven by a cooling of consumer expectations. Worryingly, both the 1-year and 5-to-10 year inflation expectations ticked up to 3.3% from 2.8% and 3.0%,…

November factory orders in Germany widely missed estimates, falling by 5.4% m/m, worsening the 1.5% October decline. Excluding major orders, which often distort the overall picture, core new orders fell 1.7% y/y after growing 5.7% in October. The European…

Job openings once again beat expectations in November, increasing to 8.1m from 7.8m in October. However, hires and quits decreased and layoffs increased. The gap between quits and layoffs, a leading indicator of labor market demand, ticked down. The jobs gap,…

The December ISM Services PMI beat estimates, increasing to 54.1 from 52.1 in November. All subcomponents increased except for employment, which nonetheless remains in expansion. The prices paid component was especially strong, increasing to 64.4 from…

The November Canadian CPI was slightly below estimates, declining to 1.9% y/y from 2.0%, below the BoC’s 2% target but within the 1%-to-3% range. The BoC’s favored core measures, median and trim, were flat at 2.6% and 2.7% respectively after revisions. CPI…

European sentiment data was mixed. The December Ifo Business Climate index for Germany missed estimates and was down 1 point to 84.7 from November. The decrease came from its expectations component, which fell to 84.4 from 87.2. Meanwhile, the December ZEW…