Corporate

Highlights Please note that analysis on India is published below. Even if the recent upturn in the Chinese credit impulse is sustained, there will likely still be a six- to nine-month lag between the impulse’s trough and the bottom in the mainland’s business cycle. EM corporate earnings cycles typically lag Chinese stimulus efforts by about nine months. Therefore, EM profits will be contracting in the first three quarters of 2019. This will short-circuit the current rebound in EM share prices. EM equity valuations are not cheap enough to shield stocks from profit contraction. Feature China’s credit growth was very strong in January. We contend that even if the upturn in the credit impulse proves to be persistent, there will likely be a six- to nine-month lag between its low point and the bottom in the mainland’s business cycle. Chart I-1 demonstrates that the credit impulse leads both nominal manufacturing output growth and the manufacturing PMI’s import subcomponent by roughly nine months. Chinese imports are the most pertinent variable to gauge China’s economic impact on the rest of the world. Chart I-1China: Credit Impulse Leads Business Cycle By Nine Months

China: Credit Impulse Leads Business Cycle By Nine Months

China: Credit Impulse Leads Business Cycle By Nine Months

In the meantime, will financial markets exposed to Chinese growth look through the valley of the ongoing growth deceleration and continue to rally? Or will they experience a major relapse in the coming months? In our opinion, corporate profits will be the key to broader financial market performance. So long as corporate profits do not shrink, investors will likely look beyond weak macro data, and any weakness in stocks will be minor. However, if corporate profits contract in the next nine months, then share prices will plummet anew. EM Profits Are Heading Into Contraction Chart I-2 illustrates that China’s credit impulse leads both EM and Chinese corporate earnings per share (EPS) by at least nine months and that it currently foreshadows EPS contraction in the first three quarters of 2019. Even if the recent upturn in the credit impulse is sustained, EM and Chinese EPS growth will likely bottom only in August – while they are in negative territory. Chart I-2EM EPS Is Beginning To Contract

EM EPS Is Beginning To Contract

EM EPS Is Beginning To Contract

EM corporate earnings growth has already dropped to zero and will turn negative in 2019. Chart I-3A reveals that EPS in U.S. dollar terms are already contracting in six out of 10 sectors – industrials, consumer staples, consumer discretionary, telecom, utilities and health care. Chart I-3AEM EPS By Sector

EM EPS By Sector

EM EPS By Sector

Chart I-3BEM EPS By Sector

EM EPS By Sector

EM EPS By Sector

EPS growth has not yet turned negative for financials, technology, energy and materials (Chart I-3B). Notably, corporate earnings within these four sectors collectively account for 70% of EM total corporate earnings, as shown in Table I-1.

Chart I-

Over the course of 2019, these sectors’ EPS are also set to shrink: Technology (accounts for 20% of MSCI EM corporate earnings): NAND semiconductor prices have been plunging for some time, and DRAM prices are also beginning to drop (Chart I-4). This reflects broad-based weakness in global trade – global auto sales are shrinking for the first time since the 2008 global financial crisis, global semiconductor sales are relapsing and global mobile phones shipments are falling (Chart I-5). Chart I-4Semiconductor Prices Are Falling

Semiconductor Prices Are Falling

Semiconductor Prices Are Falling

Chart I-5Broad-Based Weakness In Global Trade

Broad-Based Weakness In Global Trade

Broad-Based Weakness In Global Trade

Semiconductors accounted for 77% of Samsung’s operating profits in the first three quarters of 2018, suggesting the potential drop in DRAM prices will be devastating for its profits. Next week we will publish a Special Report on Korea and discuss the outlook for both semiconductors and Korean profits in more detail. In addition, the ongoing contraction in Taiwanese exports of electronics parts confirms downside risks to EM tech earnings (please refer to top panel of Chart I-3B). In brief, the ongoing decline in semiconductor prices will bring about EPS contraction in the EM technology sector. Financials/Banks (financials make up 31% of EM corporate earnings): Banks’ profits often correlate with fluctuations in economic activity, because the latter drive non-performing loan (NPL) cycles (Chart I-6). NPL cycles outside Brazil, Russia and India – where the banking systems have already gone through substantial NPL recognition and provisioning – will deteriorate, and push banks to increase their provisions. The latter will be a major drag on EM banks’ profits. Chart I-6EM Banks EPS And Economic Activity

EM Banks EPS And Economic Activity

EM Banks EPS And Economic Activity

Regarding Chinese banks in particular, if the credit revival in January is sustained, it would strongly suggest that the government is resorting to its old, credit-driven growth playbook. Following 10 years of an enormous credit frenzy and a 20-year capital spending boom, it is currently difficult to find many financially viable projects. Hence, a renewed credit binge will once again be associated with further capital misallocation and more NPLs. Many of these projects will fail to generate sufficient cash flow to service debt. NPLs will thus rise considerably and the need to raise capital will dilute the banks’ existing shareholders. Of course, this will happen with a time lag. Chart I-7 shows that the gap between Chinese banks’ EPS and non-diluted profits has once again widened, and that EPS are beginning to contract. Chart I-7Chinese Banks: Earnings Dilution

Chinese Banks: Earnings Dilution

Chinese Banks: Earnings Dilution

Chinese banks could issue perpetual bonds – discussed in great detail in last week’s report – to recapitalize themselves. Nevertheless, this will be negative for existing shareholders. In a nutshell, despite low multiples, share prices of Chinese banks will drop because more credit expansion amid the lingering credit bubble is negative for existing shareholders. The basis is that it will ultimately lead to their dilution. Chinese banks make up 4.5% of the MSCI’s EM equity market cap and 10% of aggregate EM profits. Hence, their EPS contraction will have a non-trivial impact on overall EM EPS. Resource sectors (energy and materials together make 20% of EM corporate earnings): The ongoing slowdown in China will exert renewed selling pressure in commodities markets. As shown in Chart I-9 on page 8, base metals prices lag the turning points in the Chinese credit impulse by several months and are still at risk of renewed price decline. Hence, profits of firms in the materials sector are at risk. Energy companies’ trailing EPS growth is still positive because the late-2018 carnage in oil prices has not yet filtered through to corporate earnings announcements (Chart I-3B on page 3). More importantly, the recent oil price rebound can be attributed to both Saudi Arabia’s output cuts as well as stronger demand – in the form of a surge in Chinese imports of oil and petroleum products. Chart I-8 illustrates that growth rates of China’s intake of oil and related products approached zero when crude prices were rising but has dramatically accelerated following their plunge. This is consistent with China’s pattern of buying commodities on dips. The point is that the upside in oil prices will be capped by China, which will likely moderate its oil purchases going forward, as crude prices have recently rallied. Chart I-8China And Oil

bca.ems_wr_2019_02_21_s1_c8

bca.ems_wr_2019_02_21_s1_c8

Bottom Line: EM profit cycles lag Chinese’s stimulus by about nine months. EM profits will be contracting in the first three quarters of 2019. This will short-circuit the current rebound in EM share prices. China’s Credit Cycles And Financial Markets What has been the relationship between China’s credit cycle and related financial markets over the past 10 years? The time lag between turning points in China’s credit impulse and relevant financial markets can be anywhere from zero to 18 months. Chart I-9 illustrates historical time lags between the Chinese credit impulse on the one hand and EM share prices, base metals prices and the global manufacturing PMI on the other. The time lag has not been consistent over time. Chart I-9Chinese Credit Impulse And Financial Markets: Understanding Time Lags

Chinese Credit Impulse And Financial Markets: Understanding Time Lags

Chinese Credit Impulse And Financial Markets: Understanding Time Lags

In late 2015-early 2016, the rebound in China’s credit impulse led financial markets by six months. At the recent market peak in January 2018, the credit impulse led financial markets and the global manufacturing PMI by about 18 months. In the meantime, in the 2012-13 mini cycle, EM share prices and commodities markets did not rally much, despite the meaningful upturn in China’s credit impulse. Finally, at the 2010-2011 peak, the credit impulse led EM stocks and base metals prices by 12 months. In short, the credit impulse led those financial markets by a few months to as much as a year and a half. Further, not only do time lags to the stimulus vary, but the impact on both economic activity and financial markets varies as well. This is because both economic activity and financial markets are driven by human psychology and behavior; iterations in stimulus, economic activity and financial markets are chaotic and complex in nature and do not follow well-defined patterns. Given the poor state of sentiment among Chinese consumers, business managers and entrepreneurs, more stimulus and more time may be required to turn the mainland’s business cycle this time around. Besides, unlike in previous episodes, there has not been any stimulus for the property market and no tax reductions on auto sales. Finally, although China and the U.S. may strike a deal on trade, it is unlikely to be a comprehensive agreement that is sustainable in the long run. This would be consistent with our Geopolitical Strategy team’s view that China and the U.S. are in a long-term and broad geopolitical confrontation – not a trade war. The trade war and tariffs are just one dimension of this. Hence, Chinese consumers and businesses, as well as the global business community may well look through this potential deal and not significantly alter their cautious behavior, at least for some time. In other words, the genie of geopolitical confrontation is out of the bottle, and the presidents of the U.S. and China are unlikely to succeed in putting it back. Bottom Line: Turning points in China’s credit impulse generally lead financial markets exposed to Chinese growth by several months. Given that the improvement in the credit impulse is both very recent and modest, odds are that China-related plays including EM risk assets will go through a major selloff before putting in a durable bottom.1 EM Equity Valuations In terms of the ability of EM stocks to withstand profit contraction, would cheap valuations not shield share prices from a considerable drop? We do not think EM equities are cheap; their valuations are neutral. Hence, there is no real valuation cushion in EM stocks to help them endure a period of negative EPS growth. We have written frequently about valuations and will touch on the topic only briefly here. Market cap-based multiples indeed appear very low. However, some segments of the EM universe such as Chinese banks and state-owned companies in Russia, Brazil, China and India have had low multiples for years. In other words, they are a value trap and their multiples are low for a reason. We elaborated above why Chinese banks are chronically “cheap”. For many other companies, low multiples are due to structural issues such as the lack of focus on profitability and shareholder value, or the high cyclicality of profits. Many of these stocks have large market caps, which pull down the EM index’s aggregate multiple. To remove market-cap bias, we have calculated 20% trimmed-mean multiples by ranking 50 MSCI EM industry groups (sub-sectors) and cutting off the top and bottom 10%. Then, we calculate the equal-weighted average of the remaining 80% of the sub-sectors. We did this calculation for the following five ratios: trailing P/E, forward P/E, price-to-cash earnings, price-to-book value and price-to-dividend. Then, we combined them into a composite valuation indicator (Chart I-10, top panel). This indicator shows that EM equity valuations are neutral. Chart I-10EM Equity Valuations In Absolute Terms

bca.ems_wr_2019_02_21_s1_c10

bca.ems_wr_2019_02_21_s1_c10

In addition, we calculated the median and equal-weighted composite valuation indicators (Chart I-10, middle and bottom panels). They also remove market cap bias and tell the same message: EM stocks are trading close to their fair value. EM equities are also close to their historical average relative to developed markets (DM). Chart I-11 illustrates relative EM versus DM valuation indicators based on 20%-trimmed mean, median and equal-weighted metrics. Chart I-11EM Equity Valuations Versus DM

bca.ems_wr_2019_02_21_s1_c11

bca.ems_wr_2019_02_21_s1_c11

In sum, EM valuations are not cheap neither in absolute terms, nor relative to DM. According to both measures, valuations are neutral. Hence, valuations will not prevent share prices from falling as profits begin to contract. This is why we continue to recommend a defensive strategy for absolute-return investors, and we continue to underweight EM versus DM within a global equity portfolio. Arthur Budaghyan, Senior Vice President Emerging Markets Strategy arthurb@bcaresearch.com India: Beware Of Rural Growth Lapse Indian share prices are weak and are underperforming the emerging markets benchmark in U.S. dollar terms (Chart II-1, top panel). Small cap stocks are in a full-fledged bear market (Chart II-1, bottom panel). Chart II-1Indian Stocks Are Weak

Indian Stocks Are Weak

Indian Stocks Are Weak

The latest earnings season turned out to be disappointing. Many companies missed their earnings estimates. Chart II-2 shows that net profit margins of listed non-financial companies have turned down and overall EPS growth is weakening. Chart II-2Indian Corporate Profits Are Sluggish

Indian Corporate Profits Are Sluggish

Indian Corporate Profits Are Sluggish

Disappointing corporate earnings are confirmed by macro data as well. Chart II-3A shows that manufacturing production is decelerating and intermediate goods production is contracting. Further, sales of two-wheelers, three-wheelers, passenger and commercial vehicles, as well as tractors, are either slowing or contracting (Chart II-3B). Chart II-3ACyclical Spending Is Decelerating

Cyclical Spending Is Decelerating

Cyclical Spending Is Decelerating

Chart II-3BCyclical Spending Is Decelerating

Cyclical Spending Is Decelerating

Cyclical Spending Is Decelerating

This weakness emanates from rural areas. The basis is that food prices have been falling since the summer of 2018 – and are deflating for the first time since the early 2000s. This is hurting rural incomes. Several indicators confirm considerable weakness in rural income growth and the latter’s underperformance versus urban income and spending: The top panel of Chart II-4 illustrates that our proxy for spending in rural areas relative to urban areas has deteriorated massively along with the decline in Indian food prices. Chart II-4Rural Spending Is Weaker Than Urban One

Rural Spending Is Weaker Than Urban One

Rural Spending Is Weaker Than Urban One

This measure is calculated as revenue growth of four rural-exposed listed companies minus the revenue growth of four urban-exposed listed companies. In both cases, the companies largely operate in the consumer goods space. Credit growth in rural areas has lagged that of urban areas, explaining the underperformance of rural spending (Chart II-4, bottom panel). Corroborating this, stock prices of these urban-exposed companies have outperformed their rural peers substantially (Chart II-5). Chart II-5Urban-Exposed Stocks Have Outperformed Rural Ones

Urban-Exposed Stocks Have Outperformed Rural Ones

Urban-Exposed Stocks Have Outperformed Rural Ones

Such a slump in rural income is posing a challenge to Modi’s re-election in May. His government – which lost three key state elections in late 2018 – is aware of these ominous trends and is acting boldly to revive income growth in rural areas. The government announced an expansionary budget that appeases rural voters. In particular, the budget aims to strengthen farmers’ support schemes, cut taxes for low- and middle-income earners and introduce a pension scheme for social security coverage of unorganized labor. However, there is a significant risk that the authorities’ fiscal and monetary stimulus are too late to lift growth before May’s elections. According to the past relationship between fiscal spending and India’s business cycle, higher government expenditure growth will only begin to have an effect on the economy in the second half of this year – i.e. after the elections are held (Chart II-6). Hence, the BJP could lose its majority, meaning it would either rule in a minority government or be forced to turn over power to the Congress Party and its allies. Chart II-6Government Expenditures To Lift Growth In H2 2019

Government Expenditures To Lift Growth In H2 2019

Government Expenditures To Lift Growth In H2 2019

Beyond the elections, food prices might be approaching their lows. Well-below average rain will likely result in weak agricultural production and, hence, higher food prices in the second half of 2019 (Chart II-7). Chart II-7Below Trend Monsoon = Food Prices Will Likely Rise

Below Trend Monsoon = Food Prices Will Likely Rise

Below Trend Monsoon = Food Prices Will Likely Rise

Therefore, in the second half of 2019, both fiscal easing and higher food prices will revive rural incomes and spending. In the meantime, monetary easing and credit growth acceleration will support demand in urban areas. Overall, Indian financial markets will likely remain in a risk zone until the elections as economic growth and corporate profits will continue to disappoint. If the opposition Congress Party’s alliance wins the election, Indian stocks and the currency will initially sell off. After this point, Indian assets could offer a buying opportunity because growth will likely revive in the second half of 2019. Bottom Line: For now, we continue to recommend an underweight position in Indian equities relative to the EM equity benchmark. Weakening growth, the very low interest rate differential versus U.S. rates and political uncertainty ahead of the general elections, pose risks of renewed rupee depreciation. A weaker rupee will continue to benefit India’s export-oriented software companies. Therefore, we also reiterate our long Indian software / short EM stocks recommendation. Finally, fixed-income investors should stay with the yield curve steepening trade. The central bank could further cut rates in the near term. However, long-term bond yields will not fall substantially and will likely start drifting higher sooner than later. The widening fiscal deficit, expectations of growth revival in the second half of 2019, and eventually higher food prices and inflation expectations, will all lead to a continuous steepening in the local yield curve. Ayman Kawtharani, Associate Editor ayman@bcaresearch.com Footnotes 1 This is the view of BCA’s Emerging Markets Strategy team and it is different from BCA’s house view on China-related assets and the global business cycle. The primary source of the difference is the outlook for China’s growth. Equity Recommendations Fixed-Income, Credit And Currency Recommendations

Highlights Spread Product Valuation: Corporate bond spreads don’t look especially cheap relative to average historical levels. But they are far too elevated for the current phase of the economic cycle. Valuations in other spread products are not nearly as attractive. Investors should remain overweight corporate bonds (both investment grade and junk) within U.S. fixed income portfolios. Corporate Defaults: Slowing corporate profit growth during the next 12 months will cause corporate leverage to flatten-off and will lead to a slightly higher default rate than most baseline forecasts suggest. Junk spreads currently offer adequate compensation for the extra default risk, but that cushion will evaporate quickly if spreads tighten during the next few months. Mexican Sovereign Bonds: Mexico’s USD-denominated sovereign debt is attractively priced relative to similarly-rated U.S. corporate credit. U.S. fixed income investors should take the opportunity to add USD-denominated Mexican bonds to their portfolios. Feature Corporate bonds have been on fire since the start of the year. High-yield excess returns have already made back all of their lost ground from 2018, and investment grade credits are on their way (Chart 1). With the Fed’s rate hike cycle on hold and some signs of credit easing in China, the near-term backdrop is amenable to further spread compression. Especially from current elevated levels. Chart 1Corporate Bonds Having A Good Run In 2019

Corporate Bonds Having A Good Run In 2019

Corporate Bonds Having A Good Run In 2019

On the flipside, some indicators of corporate default risk are starting to deteriorate and we can easily envision a more difficult environment for corporate spreads in the second half of this year. Especially if the Fed re-starts rate hikes, as we expect.1 In this week’s report we illustrate the extent of undervaluation in corporate spreads, and also detail our concerns related to budding default risk. We conclude that investors should maintain an overweight allocation to corporate bonds (both investment grade and high-yield) for now, but be prepared to trim exposure once spreads reach more reasonable levels. Finally, we identify an opportunity in USD-denominated Mexican sovereign bonds. Too Cheap For Phase 2 In our Special Report from mid-December that laid out our key themes for 2019, we described how we split the economic cycle into different phases based on the slope of the yield curve (Chart 2).2 We define the three phases of the cycle as follows: Chart 2Expect To Stay In Phase 2 For Most (If Not All) Of 2019

Expect To Stay In Phase 2 For Most (If Not All) Of 2019

Expect To Stay In Phase 2 For Most (If Not All) Of 2019

Phase 1: From the end of the prior recession until the 3-year / 10-year Treasury slope flattens to below 50 bps Phase 2: When the 3/10 slope is between 0 bps and 50 bps Phase 3: From when the 3/10 slope inverts until the start of the next recession Dividing the cycle this way reveals a reliable pattern in corporate bond excess returns versus Treasuries. Excess returns tend to be highest in Phase 1. They tend to be quite low but still positive in Phase 2, and they tend not to turn negative until Phase 3. We argued in December that we are currently in Phase 2 and that we will probably stay there for most, if not all, of 2019. The main reason that excess returns are lower in Phase 2 than in Phase 1 is that corporate bond spreads are much tighter in Phase 2. Most of the cyclical spread compression occurs in Phase 1, in the immediate aftermath of the recession. With that in mind, consider the data presented in Chart 3. The chart shows 12-month breakeven spreads for each corporate bond credit tier as a percentile rank relative to history.3 For example, a percentile rank of 50% means that the breakeven spread has been tighter than its current level half of the time throughout history. Chart 3 also divides the historical data into two samples, showing how breakeven spreads rank relative to the entire history of available data, and also how they rank relative to other Phase 2 periods only.

Chart 3

When the full historical sample is considered, only the B-rated and Caa-rated credit tiers have breakeven spreads above their historical medians. However, when we focus exclusively on Phase 2 environments we see that spreads for every credit tier other than Aaa look extremely cheap. Essentially, Chart 3 shows that today’s spread levels are more consistent with periods when the economy is either just exiting or entering a recession. Absent that sort of macro environment, there would appear to be an obvious buying opportunity in corporate bonds. Interestingly, other spread products don’t look nearly as cheap as corporate bonds. Chart 4 shows the same data as Chart 3 but for all non-corporate U.S. spread products with available data prior to 2000. It shows that Agency MBS and Consumer ABS spreads are close to median Phase 2 levels. USD-denominated Sovereign debt looks somewhat cheap. Meanwhile, Domestic Agencies and Supranationals both look expensive. What’s clear is that right now corporate credit offers the most attractive opportunity in U.S. fixed income.

Chart 4

Bottom Line: Corporate bond spreads don’t look especially cheap relative to average historical levels. But they are far too elevated for the current phase of the economic cycle. Valuations in other spread products are not nearly as attractive. Investors should remain overweight corporate bonds (both investment grade and junk) within U.S. fixed income portfolios. Default Cycle At A Turning Point? Another valuation tool in our arsenal is the High-Yield default-adjusted spread. This is the excess spread available in the high-yield index after accounting for expected 12-month default losses. It can also be thought of as the 12-month return earned by the High-Yield index in excess of a position in duration-matched Treasuries, assuming that default losses match expectations and that there are no capital gains (losses) from spread tightening (widening). Expected default losses are calculated using the Moody’s baseline default rate forecast and our own forecast of the recovery rate. Combining the Moody’s baseline default rate forecast of 2.4% and our recovery rate forecast of 45% gives expected 12-month default losses of 1.3%. Those expected default losses are then subtracted from the average High-Yield index option-adjusted spread to get a default-adjusted spread of 274 bps. This is slightly above the historical average of 250 bps (Chart 5). In other words, junk investors are currently being compensated at slightly above average levels to bear default risk. Chart 5A Look At The Default-Adjusted Spread

A Look At The Default-Adjusted Spread

A Look At The Default-Adjusted Spread

Another way to conceptualize the default-adjusted spread is to ask what default rate would have to prevail over the next 12 months for junk investors to earn average historical excess compensation. This spread-implied default rate is denoted by the ‘X’ in the second panel of Chart 5. It is currently 2.8%, slightly above Moody’s baseline expectation. Is The Baseline Default Rate Forecast Reasonable? If we view the Moody’s 2.4% default rate forecast as reasonable, then we should conclude that junk bonds are attractively valued. However, some macro indicators suggest that 2.4% might be too optimistic. Chart 6 shows a model of the 12-month trailing speculative grade default rate based on gross leverage, which we define as total debt over pre-tax profits, and C&I lending standards. Chart 6A Simple Model Of The 12-Month Trailing Speculative Grade Default Rate

A Simple Model Of The 12-Month Trailing Speculative Grade Default Rate

A Simple Model Of The 12-Month Trailing Speculative Grade Default Rate

Gross leverage has improved during the past few quarters as profit growth has outpaced corporate debt growth (Chart 6, panel 2). This has acted to push down the fair value reading from our default rate model. On the other hand, commercial & industrial (C&I) lending standards tightened in the fourth quarter of last year (Chart 6, bottom panel). A net tightening in C&I lending standards is consistent with a higher default rate. Overall, the fair value reading from our default rate model is currently 3.5%, above the current 12-month trailing default rate of 2.6%. For the purposes of valuation, where the default rate will be 12 months from now is more important than where it is currently. To get a sense of where the fair value from our model is headed we need forecasts for corporate profit and debt growth. Profit growth will almost certainly moderate from its current lofty levels (Chart 7). Pressures on revenues and expenses both point in that direction. Total business sales and the ISM Manufacturing PMI have both fallen sharply from their recent highs (Chart 7, panel 2), suggesting lower corporate revenue growth going forward. Meanwhile, wages continue to accelerate (Chart 7, bottom panel). Chart 7Forecasting Profit Growth

Forecasting Profit Growth

Forecasting Profit Growth

Using a model based on nominal GDP growth, wage growth, industrial production and the trade-weighted dollar, if we forecast that nominal GDP growth slows to the same rate as wage growth over the next 12 months, then the model predicts that profit growth will fall into the mid-single digits (Chart 7, top panel). This would be more or less consistent with the recent growth rate in corporate debt, meaning that gross leverage would flatten-off and the fair value reading from our default rate model would stabilize near 3.5%. In summary, if profit growth moderates in line with our expectations during the next 12 months, then it is likely that the corporate default rate will be somewhat higher than the current Moody’s forecast of 2.4%, possibly as high as 3.5%. But even a 3.5% default rate would still translate to a default-adjusted junk spread of 211 bps. Positive compensation for default risk, though less than average historical levels. In that case we would still expect solid positive excess returns from junk bonds. However, it will be important to monitor our default-adjusted spread during the next few months. If junk spreads tighten in the near-term, as we anticipate, then the excess compensation for default risk will evaporate quickly. Bottom Line: Slowing corporate profit growth during the next 12 months will cause corporate leverage to flatten-off and will lead to a slightly higher default rate than most baseline forecasts suggest. Junk spreads currently offer adequate compensation for the extra default risk, but that cushion will evaporate quickly if spreads tighten during the next few months. Buy Mexican Bonds While most spread products have benefited from the Fed’s pause, delivering excellent year-to-date returns. We notice that the spreads on Mexico’s USD-denominated sovereign debt have not tightened alongside other comparable credits (Chart 8). This presents an attractive opportunity. Chart 8Mexican Bonds: An Attractive Opportunity

Mexican Bonds: An Attractive Opportunity

Mexican Bonds: An Attractive Opportunity

When we compare 12-month breakeven spreads between the USD-denominated sovereign debt of different emerging market countries versus the spreads on equivalently-rated U.S. corporate bonds, we see that Mexico has now joined Argentina, Saudi Arabia, Qatar, UAE and Poland as the only countries that offer attractive compensation relative to the U.S. corporate sector (Chart 9).

Chart 9

Why has this happened? Our Emerging Markets Strategy service postulates that many investors fear that the new political regime will bring fiscal profligacy, but in fact, the AMLO administration is proving to be less populist and more pragmatic than expected.4 The 2019 budget, for example, targets a primary surplus of 1% of GDP, and envisages a decline in nominal expenditures in 29 out of 56 categories. This commitment to sound fiscal policy should benefit Mexican sovereign bond spreads. More fundamentally, our Emerging Markets strategists note that the Mexican peso is very cheap as measured by the real effective exchange rate based on unit labor costs. This is not surprising given that the peso has been relatively flat versus the dollar during the past two years, despite interest rates being much higher in Mexico than in the U.S. The Mexican 10-year real yield is currently 4.1%, well above real GDP growth which was 2.6% during the past four quarters (Chart 10). Contrast that with the U.S., where the 10-year real yield is a meagre 0.8% versus real GDP growth of 3% during the past four quarters. In other words, interest rate differentials favor a stronger peso, which is positive for USD-denominated sovereign spreads. Chart 10Good Time To Add USD-Denominated Mexican Bonds To A Portfolio

Good Time To Add USD-Denominated Mexican Bonds To A Portfolio

Good Time To Add USD-Denominated Mexican Bonds To A Portfolio

Though the Mexican/U.S. interest rate differential remains wide, it is likely to compress going forward. Elevated Mexican interest rates relative to growth signal that monetary policy is restrictive. A fact that is already evident in decelerating Mexican money supply (Chart 10, bottom panel). Meanwhile, low U.S. real yields relative to GDP suggest that further Fed tightening is necessary before U.S. rates are similarly restrictive. Bottom Line: Mexico’s USD-denominated sovereign debt is attractively priced relative to similarly-rated U.S. corporate credit. U.S. fixed income investors should take the opportunity to add USD-denominated Mexican bonds to their portfolios. Ryan Swift, Vice President U.S. Bond Strategy rswift@bcaresearch.com Footnotes 1 Please see U.S. Bond Strategy Weekly Report, “Caught Offside”, dated February 12, 2019, available at usbs.bcaresearch.com 2 Please see U.S. Bond Strategy Special Report, “2019 Key Views: Implications For U.S. Fixed Income”, dated December 11, 2018, available at usbs.bcaresearch.com 3 The 12-month breakeven spread is the spread widening required over the next 12 months for the corporate bond to break even with a duration-matched position in Treasury securities. We use the breakeven spread instead of the average index spread because it takes into account the changing duration of the bond indexes. 4 Please see Emerging Markets Strategy Weekly Report, “Dissecting China’s Stimulus”, dated January 17, 2019, available at ems.bcaresearch.com Fixed Income Sector Performance Recommended Portfolio Specification

Highlights The current trajectory in global share prices resembles what took place in 2000 and early 2001. The early 2001 rebound in global and EM stocks lasted several weeks only, despite ongoing easing by the Federal Reserve. Corporate profits – not the Fed – was the key driver in 2001 and remains the principal driver of global and EM stocks today. EM corporate profits are set to contract this year due to China’s continuing slowdown and weakening global trade. This suggests the current EM rally is unsustainable; continue underweighting EM. In Chile, bet on lower swap rates. Continue shorting the peso but overweight the local bourse within an EM equity portfolio. Feature The dovish shift by the U.S. Federal Reserve in the past month has boosted EM risk assets and currencies. Yet, we find that in the medium and long term there is a very low correlation between Fed policy and U.S. interest rates, on the one hand, and EM financial markets on the other. Instead, EM risk assets and currencies correlate with EM/China business cycles and global trade (Chart I-1). We have not detected any improvement in China/EM growth, nor in global trade (Chart I-1). What’s more, we expect Chinese growth and world trade to continue to weaken in the coming six months. Therefore, the EM rebound and outperformance will be reversed sooner than later. Chart I-1Global Growth Indicators Do No Confirm EM Rally

Global Growth Indicators Do No Confirm EM Rally

Global Growth Indicators Do No Confirm EM Rally

Please note this is the view of BCA’s Emerging Markets Strategy team. BCA’s house view is presently positive on global risk assets and global growth. The basis for this difference between our current position and that of the majority of our colleagues is the outlook for China’s growth. A Replay Of 2016 Or 2001? Most investors are betting that 2019 will be a replay of 2016, when the Fed’s dovish turn and China’s stimulus propelled the EM and global equity rallies. It is enticing to compare the current episode in financial markets to the one that occurred only three years ago. To be sure, there are a lot of similarities: the global trade slowdown driven by China/EM, selloffs in global equity and credit markets, a dovish shift in the Fed’s stance and policy stimulus in China are all reminiscent of early 2016. Not surprisingly, this has created a stampede into EM. According to the most recent Bank of America Merrill Lynch survey, as of mid-January some 29% of investors were overweight EM stocks compared to 1% overweight in the U.S., 11% underweight in the euro area and 1% underweight in Japan. By now, the overweight in EM equities is most likely even higher, given the stampede into EM assets that has occurred over the past several weeks. This stands in contrast to the 33% underweight in EM equities in January 2016. It is apparent that the majority of investors are indeed extrapolating 2016 into 2019. We hold a different view and believe China’s slowdown will be more protracted than in 2015-’16, and that EM corporate earnings are set to contract (please refer to Chart I-5 on page 6). A key distinction between China’s current policy efforts and what was implemented in 2015-‘16 is the absence of stimulus for real estate. The odds are that China’s property market will continue to languish, weighing on household and business sentiment as well as spending. Further, the efficiency of monetary transmission mechanisms could be lower today than it was in 2016 due to the regulatory tightening on both banks and non-banks. The fiscal multiplier could also be lower due to the fragile sentiment among consumers and businesses. We discussed these issues in detail in our January 17, 2019 report. Remarkably, it appears that global share prices are tracking the pattern of 1998-2001 – their trajectories are identical in terms of both magnitude and duration (Chart I-2). Chart I-2Global Stocks Are Tracking Pattern Of 1998-2001 In Magnitude And Duration

Global Stocks Are Tracking Pattern Of 1998-2001 In Magnitude And Duration

Global Stocks Are Tracking Pattern Of 1998-2001 In Magnitude And Duration

That said, there are substantial differences between today and 2001 in respect to the economic backdrops in the U.S. and China. Our focal point is to demonstrate that the Fed easing is not sufficient to prop up share prices if it does not lead to a recovery in corporate earnings. We conclude that the latest rebound in EM risk assets is probably late because neither the Fed’s pause nor China’s stimulus will revive EM corporate profits in the next nine months. In terms of market action, one can draw a number of parallels between the trajectory in global share prices today and in 2000-’01. Following an exponential rally in 1999, the global equity index peaked in January 2000 (Chart I-3). The equity selloff accelerated in the last quarter of 2000, with stocks plunging in December of that year. Chart I-3Is Rebound In Global And EM Stocks Late?

Is Rebound In Global And EM Stocks Late?

Is Rebound In Global And EM Stocks Late?

Oversold conditions in global share prices and the Fed’s intra-meeting 50-basis-point rate cut on January 3, 2001, generated a 7% and 15% rebound in global and EM stocks, respectively. The bounce lasted from late December 2000 until early February 2001. The current trajectory in global share prices – the rollover in late January 2018, the top formation lasting several months followed by a dramatic plunge, the bottom in late December, 2018 and the subsequent rebound – closely resemble the path global share prices took in 2000 and early 2001 (Chart I-3, top panel). The same holds true for EM share prices (Chart I-3, bottom panel). Critically, the Fed continued to cut interest rates in 2001 and 2002, yet the bear market in global equities, including EM, persisted until March 2003 (Chart I-4A and I-4B, top panels). The culprit was shrinking corporate profits (Chart I-4A and Chart I-4B, bottom panels). Chart I-4AFed Easing Did Not Help Global Stocks In 2001

Fed Easing Did Not Help Global Stocks In 2001

Fed Easing Did Not Help Global Stocks In 2001

Chart I-4BFed Easing Did Not Help EM Stocks In 2001

Fed Easing Did Not Help EM Stocks In 2001

Fed Easing Did Not Help EM Stocks In 2001

Odds are that EM earnings are set to contract this year as discussed below and shown in Chart I-5. As a result, this view bolsters our conviction that EM equities are likely to roll over soon and plunge anew in absolute terms, and certainly underperform U.S. stocks. Bottom Line: There are many economic differences between today and 2001. Our main point is that the Fed easing-inspired rally in global equities in early 2001 lasted several weeks only and was followed by a new cycle low. The key factor was not Fed policy but corporate profits. Provided our view that corporate earnings in EM and global cyclical sectors will contract this year, the rally in these segments is not sustainable regardless of Fed policy. What Drives EM: Chinese Or U.S. Growth? Predicting the outlook for China and global trade correctly is key to getting the EM call right. First, China’s credit and fiscal spending impulse leads EPS growth of companies included in the EM MSCI equity index by nine months, and it currently points to continued deceleration and contraction in EM EPS in the months ahead (Chart I-5, top panel). The average of new and backlog orders within China’s manufacturing PMI also portends a negative outlook for EM corporate earnings (Chart I-5, bottom panel). Chart I-5EM Profits Are Heading Into Contraction

EM Profits Are Heading Into Contraction

EM Profits Are Heading Into Contraction

The primary linkage between China’s credit and fiscal spending impulse and EM profits is as follows: China impacts EM and the rest of the world via its imports. This explains why EM share prices correlate with Chinese PMI imports (Chart I-6). Chart I-6Chinese Imports And EM Equities

Chinese Imports And EM Equities

Chinese Imports And EM Equities

Second, China’s imports are to a large extent driven by capital spending, especially construction. Some 85% of mainland imports are composed of various commodities, industrial goods and materials, and autos. Consumer goods make up only about 15% of imports. Major capital expenditures in general and construction, in particular, cannot be undertaken without financing. This is why the country’s credit and fiscal spending impulse leads its imports cycles (Chart I-7). This impulse is presently foreshadowing a deepening slump in mainland imports and by extension its suppliers’ revenues and profits. Chart I-7Chinese Imports Are Heading South

bca.ems_wr_2019_02_07_s1_c7

bca.ems_wr_2019_02_07_s1_c7

Third, as EM shipments to China dwindle, not only will EM corporate revenues and profits disappoint but EM currencies will also depreciate. The latter bodes ill for EM U.S. dollar and local currency bonds. The basis is that exchange rate depreciation makes U.S. dollar debt more expensive to service, and also pushes up local bond yields in high-yielding EM fixed-income markets. Fourth, The majority of developing economies sell more to China than to the U.S. Remarkably, global trade and global manufacturing decelerated in 2018, even though U.S. goods imports were booming (Chart I-8). Crucially, the more recent strength in the U.S.’s intake of goods was in part due to frontloading of shipments to the U.S. before the import tariffs went into effect on January 1, 2019. Chart I-8U.S. Imports Are Very Robust

U.S. Imports Are Very Robust

U.S. Imports Are Very Robust

Yet despite robust U.S. demand, aggregate exports of Korea, Taiwan, and Japan have done poorly and their manufacturing have slumped (Chart I-9A and Chart I-9B). Chart I-9AAsian Exports: Flirting With Contraction

Asian Exports: Flirting With Contraction

Asian Exports: Flirting With Contraction

Chart I-9BAsian Manufacturing: Flirting With Contraction

Asian Manufacturing: Flirting With Contraction

Asian Manufacturing: Flirting With Contraction

This highlights the increased significance of Chinese demand and the diminished importance of U.S. domestic demand in world trade. In particular, at $6 trillion, EM aggregate goods and services imports, including Chinese imports (but excluding China’s imports for processing and re-exporting), is greater than the combined imports of the U.S. and EU, which currently stand at $4.7 trillion ($2.5 trillion plus $2.2 trillion, respectively). Finally, the media and many investors have exaggerated the impact of U.S. tariffs on the Chinese economy. We are not implying that the tariffs are not relevant at all, or that they have not damaged sentiment among mainland businesses and households. They have. The point is that China’s exports to the U.S. constitute 3.8% of Chinese GDP only (Chart I-10). This compares to Chinese capital spending amounting to 42% of GDP and total annual credit origination and fiscal spending of 26% of GDP. Chart I-10China's Exports To U.S. Are Small (3.8% of GDP)

China's Exports To U.S. Are Small (3.8% of GDP)

China's Exports To U.S. Are Small (3.8% of GDP)

Overall, China’s growth slowdown in 2018 was not due to its plunging shipments to the U.S. – actually, the latter were rising strongly till December due to frontloading – but due to weakness in credit origination, primarily among non-banks (shadow banking). Bottom Line: The Chinese business cycle – not the U.S.’s – is the key driver of EM share prices and currencies and more important than the Fed. EM And The Fed On the surface, it seems that EM is tracking Fed policy. To us, however, this is akin to“not seeing the forest for the trees”. Investors need to stand back and examine the medium- and long-term relationships between U.S. interest rates, DM central banks’ balance sheets, and EM financial markets. In this broader context, the following becomes apparent: There is no stable correlation between EM share prices, EM currencies and EM sovereign credit, on the one hand, and U.S. 10-year bond yields, on the other (Chart I-11). Chart I-11EM And U.S. Bond Yields: No Stable Correlation

EM And U.S. Bond Yields: No Stable Correlation

EM And U.S. Bond Yields: No Stable Correlation

Historically, the correlation between EM share prices and the Fed funds rate has been mixed, albeit more positive than negative (Chart I-12). On this 40-year chart, we shaded the periods when EM stocks did well during periods of a rising fed funds rate. These time spans are 1983-1984, 1988-1989, 1999-2000, 2003-2007 and 2017. Chart I-12EM Stocks And Fed Funds Rate: A Historical Perspective

EM Stocks And Fed Funds Rate: A Historical Perspective

EM Stocks And Fed Funds Rate: A Historical Perspective

The only two episodes when EMs crashed amid rising U.S. interest rates were the 1982 Latin America debt crisis and the 1994 Mexican peso crisis. Yet, it is essential to emphasize that these crises occurred because of poor EM fundamentals: elevated foreign currency debt levels, negative terms-of-trade shocks, large current account deficits and pegged exchange rates. Dire EM fundamentals also prevailed before the Asian/EM crises of 1997-1998. However, these late-1990s crises occurred without much in the way of Fed tightening or rising U.S. bond yields. Remarkably, there is also no correlation between the size and the rate of change of DM central banks’ balance sheets, on the one hand, and EM risk assets and currencies on the other. In particular, Chart I-13 validates that the annual growth rate of G4 central banks’ balance sheets does not correlate with either EM share prices or EM local currency bonds’ total returns in U.S. dollars. Chart I-13Pace Of QEs And EM: No Correlation

Pace Of QEs And EM: No Correlation

Pace Of QEs And EM: No Correlation

Finally, there is a low correlation between U.S. real interest rates and the real broad trade-weighted dollar (Chart I-14). Notably, Chart I-15 illustrates that the greenback often acts as a countercyclical currency, appreciating when global growth is slowing and depreciating when the global business cycle accelerating. Please note that the dollar is shown inverted on this chart. Chart I-14The U.S. Dollar And U.S. Real Rates

The U.S. Dollar And U.S. Real Rates

The U.S. Dollar And U.S. Real Rates

Chart I-15The U.S. Dollar Is Countercyclical

The U.S. Dollar Is Countercyclical

The U.S. Dollar Is Countercyclical

Bottom Line: Many analysts and investors assign more significance to the Fed policy’s impact on EM risk assets than historical evidence warrants. Unless Fed policy easing coincides with EM growth recovery, the Fed’s positive impact on EM will prove to be fleeting. Investment Considerations Widespread bullish bias on EM among investors currently and a continuous slew of poor growth data in China and global trade give us the conviction to argue that the current EM rally is not sustainable. Even if the S&P 500 drifts higher, EM stocks and credit will underperform their U.S. counterparts (Chart I-16). Chart I-16Stay Short EM / Long S&P 500

Stay Short EM / Long S&P 500

Stay Short EM / Long S&P 500

The EM equity index is sitting at a major technical resistance, and a decisive break above this level will challenge our view (Chart I-17, top panel). The same holds true for many EM currencies and copper (Chart I-17, bottom panel). However, for now, we are maintaining our negative bias. Chart I-17EM Equities And Copper Are Facing Resistance

EM Equities And Copper Are Facing Resistance

EM Equities And Copper Are Facing Resistance

Within the EM equity universe, our overweights are Brazil, Mexico, Chile, Russia, central Europe, Korea, and Thailand. Our underweights are Indonesia, India, Philippines, South Africa, and Peru. We continue to recommend shorting the following EM currency basket versus the U.S. dollar: ZAR, IDR, MYR, CLP, and KRW. The full list of our recommended positions across EM equities, local rates, credit, and currencies is available on pages 17-18. Arthur Budaghyan, Senior Vice President Emerging Markets Strategy arthurb@bcaresearch.com Chile: Favor Bonds Over Stocks Local currency bonds will outperform equities in Chile over the next six to nine months (Chart II-1). Chart II-1Chile: Favor Bonds Over Stocks

Chile: Favor Bonds Over Stocks

Chile: Favor Bonds Over Stocks

The central bank is raising interest rates to cap inflation. However, we believe this is misguided because China’s ongoing deceleration along with lower copper prices, will slow growth in Chile over the course of this year. In addition, the current domestic inflation dynamics are less worrisome than the central bank contends. There is ongoing debate in the policy circles of Santiago over whether the recent large net immigration wave, particularly from Venezuela, is inflationary or disinflationary. On the one hand, net immigration expands the supply of labor and puts downward pressure on wages, and hence is disinflationary (Chart II-2). On the other hand, net immigration bolsters demand, and thereby inflation. Chart II-2Chile: Labor Force Is Expanding At 2%

Chile: Labor Force Is Expanding At 2%

Chile: Labor Force Is Expanding At 2%

The central bank has acknowledged both effects but has cited that the latter will overwhelm the former. We disagree with this assessment and believe that current immigration in Chile will be more disinflationary. There are a number of factors that make us believe so: Both nominal and real wage growth are cooling off rapidly (Chart II-3). This corroborates the thesis that the expanding supply of labor is capping wage increases. Chart II-3Chile: Wage Growth Is Decelerating

Chile: Wage Growth Is Decelerating

Chile: Wage Growth Is Decelerating

Central banks in any country need to be concerned with rising unit labor costs and service sector inflation. Energy and food prices are beyond a central bank’s control. Monetary policy should not respond to fluctuations in these prices unless there are second-round effects on wages and other prices. There is presently no genuine inflationary pressures in Chile. The average of Chile’s core and trimmed mean inflation rates stands at 2.5%, and service sector inflation is at 3.7% (Chart II-4). This is within the central bank’s inflation target range of 3% +/-1%. Chart II-4Chile: Inflation Is Within Target Range

Chile: Inflation Is Within Target Range

Chile: Inflation Is Within Target Range

Finally, Chile’s exports are set to shrink due to the ongoing deceleration in China and lower copper prices (Chart II-5). With exports accounting for 30% of GDP, a negative external shock will slow domestic demand too. This will be disinflationary. Chart II-5Chilean Exports Are About To Contract

Chilean Exports Are About To Contract

Chilean Exports Are About To Contract

The fixed-income market in Chile is pricing in rate hikes (Chart II-6). We continue to recommend receiving 3-year swap rates. Even if the central bank continues to tighten, long-term interest rates will decline, anticipating rate cuts down the road. Chart II-6Chile: Receive 3-Year Swap Rates

Chile: Receive 3-Year Swap Rates

Chile: Receive 3-Year Swap Rates

Chilean share prices, in absolute terms, are at risk from the EM and commodities selloff. However, we recommend dedicated EM equity portfolios overweight Chile. The economy is fundamentally and structurally solid, and local equity markets are supported by large local investment pools. Importantly, unlike many other commodity producers, currency depreciation in Chile does not stop the central bank from cutting interest rates. Banco Central de Chile does not target the exchange rate and will cut rates to mitigate the adverse external shock. This will ensure that business cycle fluctuations in Chile will be milder than in other developing economies where central banks tighten to defend their currencies. This is positive for Chilean stocks versus other EM bourses. Finally, the peso is at risk of depreciation from lower copper prices. Bottom Line: Local investors should favor domestic bonds over stocks. Fixed-income traders should bet on lower three-year swap rates. Dedicated EM investors should overweight Chilean equities. Currency traders should maintain a short CLP / long USD trade. Footnotes Equity Recommendations Fixed-Income, Credit And Currency Recommendations

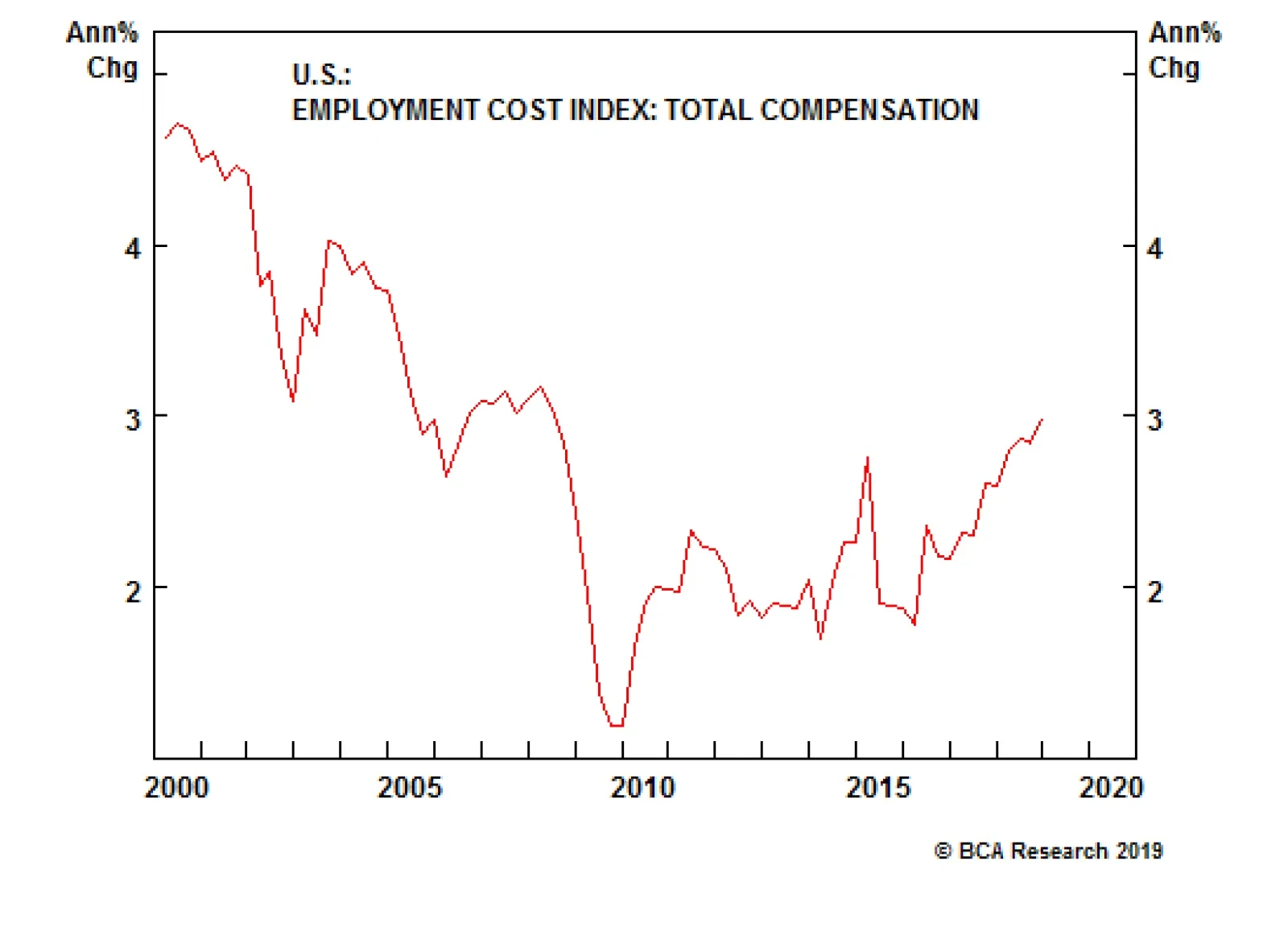

Compensation costs should not hurt margins if they grow at or below the sum of the rate of price-level and productivity gains. If inflation grows at the Fed’s 2% target, and productivity maintains its rough 1.25% growth pace, compensation growth of 3.25%…

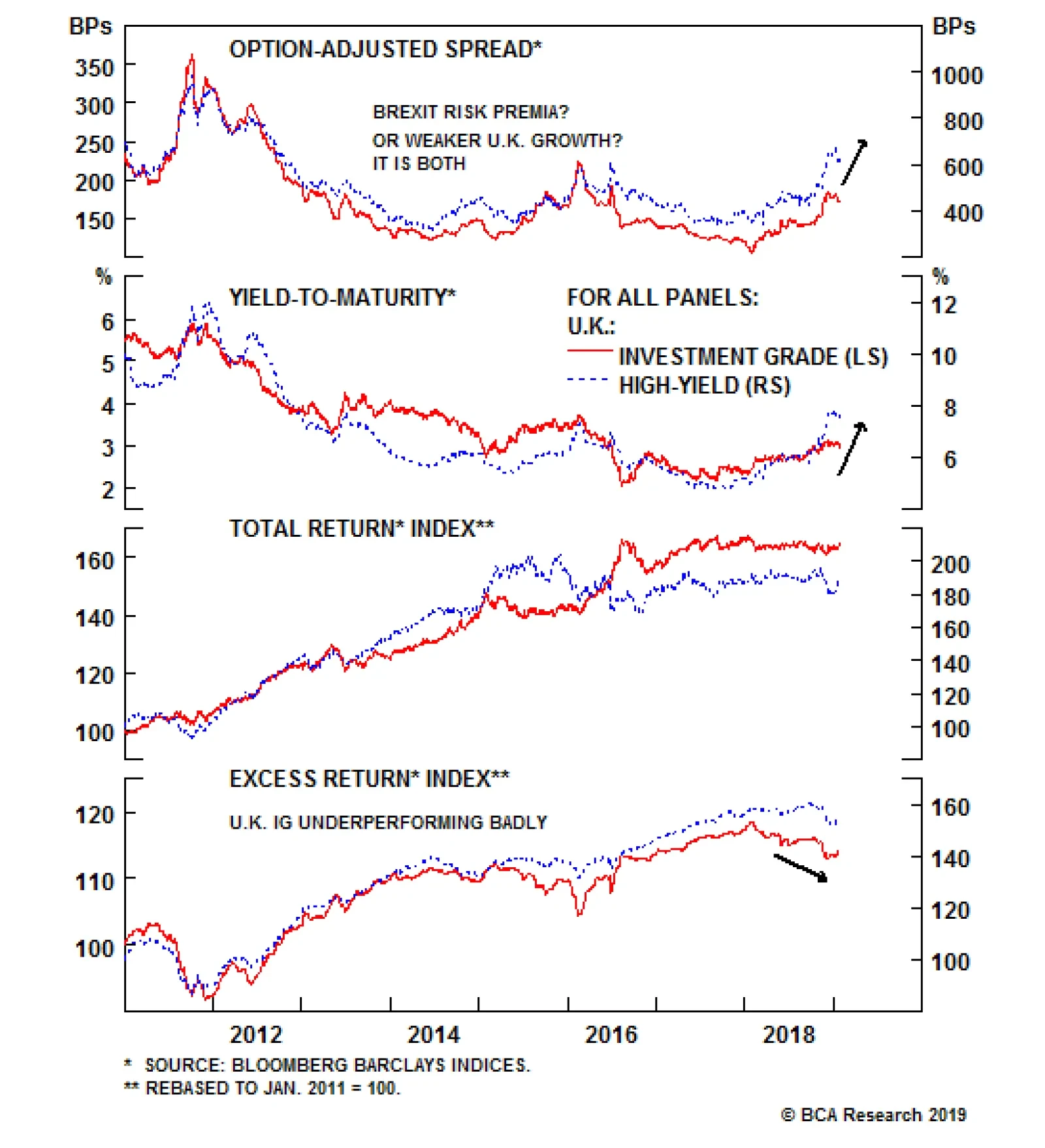

All the components of the U.K. CHM have contributed to this worsening trend. Even short-term liquidity, which had been in a powerful uptrend for almost a decade, has started to roll over. The cause for this deterioration can be reduced to one cause:…

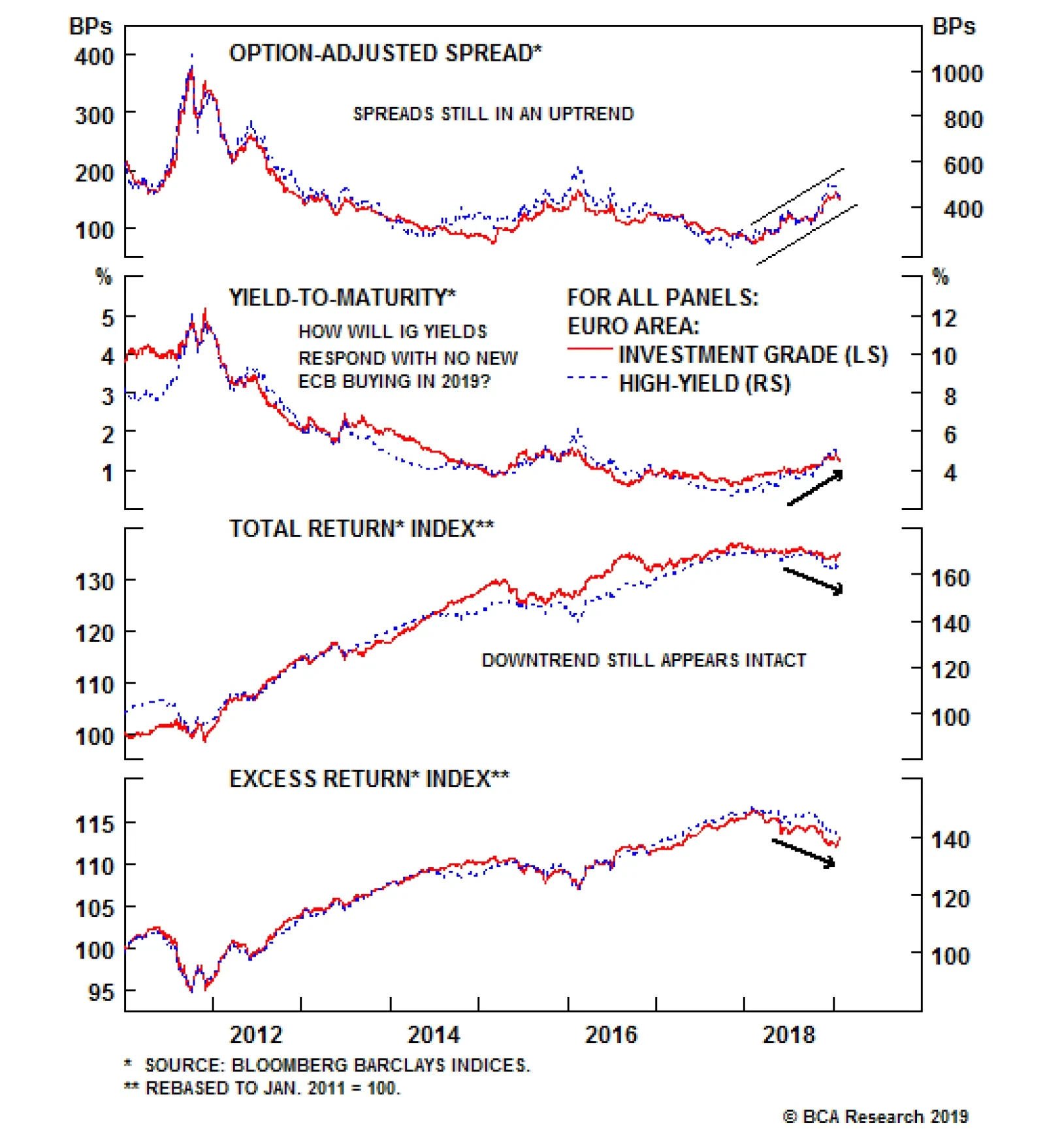

For IG, the gap between domestic and foreign issuers continues to widen, with the former worsening at the margin. For domestic issuers, interest and debt coverage has improved but operating margins and return on capital remain low while leverage is inching…

Highlights We recently upgraded our recommended investment stance on global corporate bonds to overweight on a tactical (3 to 6 months) basis.1 Feature That change was mostly based on our view that global financial conditions had tightened enough in late 2018 – both through lower equity prices and wider corporate credit spreads – to force central banks (most notably, the Fed) to shift to a less hawkish policy bias. Our opinion that global growth expectations had grown too pessimistic, particularly in the U.S., also played a role in the upgrade (Chart 1). Chart 1Global Corporates: Too Much Bad News Now Discounted

Global Corporates: Too Much Bad News Now Discounted

Global Corporates: Too Much Bad News Now Discounted

One other supporting factor for the upgrade to corporates: the prior bout of spread widening was not justified by a significant worsening of the underlying financial health of companies. With that in mind, this week we are presenting our latest update of the BCA Corporate Health Monitor (CHM) Chartbook. The CHMs are composite indicators of balance sheet and income statement ratios (using both top-down and bottom-up data) that are designed to assess the financial well-being of the overall non-financial corporate sectors in the major developed economies. A brief overview of the methodology is presented in Appendix 1 on Pages 15-16. The broad conclusion from the latest readings on our CHMs is that global credit quality has been enjoying a cyclical improvement, but with divergences starting to open up among individual regions. The U.S. has delivered the biggest improvement in corporate health, thanks largely to the boost to profitability from the Trump corporate tax cuts. Euro area corporates still appear to be in decent health, but are now exposed to the sharp slowing of European growth and the end of the ECB’s buying of corporates through its Asset Purchase Program. Meanwhile, corporate health in the U.K. and Japan is showing some strain from weaker growth in both countries. Given those regional divergences, we continue to prefer U.S. corporates over non-U.S. equivalents, even within that tactical overweight recommendation on global corporate exposure. Beyond that tactical timeframe, however, there are growing risks for corporate bond performance. Our base case scenario is that resilient U.S. growth and inflation will prompt the Fed to restart the rate hike cycle later in the year, creating a more challenging backdrop for corporates from U.S. growth uncertainty and rising volatility. Yet if the U.S. (and global) economy surprises to the downside, that is even worse for corporate bond returns given how the only real improvements in our global CHMs have come from cyclical variables like profit margins and interest coverage. U.S. Corporate Health Monitors: Strong Profits “Trump” High Leverage Our top-down CHM for the U.S. has ever so slightly flipped into the “improving health” zone, after flashing “deteriorating health” since mid-2014 (Chart 2). The resilience of the U.S. economy, combined with the positive impact on U.S. profitability from the Trump corporate cuts, has put U.S. companies in a cyclically healthier position, even with relatively high leverage. Chart 2Top-Down U.S. CHM: Supported By Cyclically Strong Profits

Top-Down U.S. CHM: Supported By Cyclically Strong Profits

Top-Down U.S. CHM: Supported By Cyclically Strong Profits

There are clear uptrends in the ratios that go into the top-down CHM that are directly related to corporate profits – return on capital, profit margins, interest coverage and debt coverage. From a fundamental perspective, the top-down U.S. CHM suggests that the U.S. credit cycle is being extended by the stubborn endurance of the U.S. business cycle. In other words, there are no immediate domestic pressures on U.S. corporate finances that should require significantly wider credit spreads to compensate for rising downgrade/default risk. The bottom-up versions of the U.S. CHMs for IG corporates (Chart 3) and HY companies (Chart 4) have also shown meaningful cyclical progress, with the HY indicator now firmly in “improving health” territory. This confirms that the signal from our top-down CHM is being reflected in both higher rated and lower quality companies. Yet the longer-term issues related to high leverage and low interest/debt coverage are not going away, suggesting that potential problems are being stored up for the next U.S. economic downturn. Chart 3Bottom-Up U.S. IG CHM: Steady, But Have Margins Peaked?

Bottom-Up U.S. IG CHM: Steady, But Have Margins Peaked?

Bottom-Up U.S. IG CHM: Steady, But Have Margins Peaked?

Chart 4Bottom-Up U.S. High-Yield CHM: Only A Cyclical Improvement

Bottom-Up U.S. High-Yield CHM: Only A Cyclical Improvement

Bottom-Up U.S. High-Yield CHM: Only A Cyclical Improvement

Interest coverage remains the key ratio to watch in both the IG and HY bottom-up U.S. CHMs. For IG, the fact that interest coverage has fallen in recent years, despite high profit margins and historically low corporate borrowing rates, is worrisome. This indicates that the stock of U.S. corporate debt is now so large that the interest expense required to service that debt is eating up a greater share of corporate revenues, even at a time when profit growth is still quite strong. This will raise downgrade risk if corporate borrowing rates were to increase significantly or if U.S. earnings growth slows sharply – likely from rising labor costs eroding high profit margins. For HY, interest coverage remains depressed by historical standards, with the liquidity ratio down to levels last seen prior to the 2009 recession. This suggests that U.S. HY companies are at risk of a severe default cycle when the current U.S. economic expansion ends, with fewer liquid assets available to meet current liabilities. Given these more medium-term fundamental concerns, we do not plan on overstaying our current tactical overweight stance on U.S. IG and HY corporates versus both U.S. Treasuries and non-U.S. corporates (Chart 5). We anticipate cutting our recommended exposure once the Fed begins signaling a need to restart the rate hikes, likely around mid-year. For those with an investment horizon beyond the next six months, the more prudent decision may be to sell into the corporate bond outperformance that we are expecting. The medium-term outlook for U.S. corporates is far more challenging given the advanced age of the U.S. monetary, business and credit cycles. Chart 5U.S. Corporates: Stay Tactically Overweight IG & HY

U.S. Corporates: Stay Tactically Overweight IG & HY

U.S. Corporates: Stay Tactically Overweight IG & HY

Euro Corporate Health Monitors: Stable, But Slowing Growth Is A Problem The CHMs remain a core part of our suite of bond market indicators, reliably proving their usefulness in helping evaluate the fundamental risks in owning corporate bonds. That does not, however, mean that there is no room for improvement in the CHM methodology from time to time. This is the case for our top-down CHM for the euro area, which has been behaving in a manner inconsistent with our bottom-up CHMs for the region – which are based on actual reported financial data from publicly traded companies – for some time. This is not the case in the U.S., where our bottom-up and top-down CHMs continue to move broadly in lockstep. Thus, we are taking our top-down euro area CHM “into the garage” for repairs. We will revisit all aspects of the methodology, from calculations to data sources, to try and improve the signal from the top-down euro area CHM. We plan on introducing a new and (hopefully) improved indicator sometime in the next few months. The message from our bottom-up CHMs for euro area IG and HY is still generally positive for overall European corporate health. Yet there are noticeable divergences within the sub-components of those individual CHMs that paint a more worrisome picture. For IG, the gap between domestic and foreign issuers in the euro area corporate bond market continues to widen, with the former worsening on the margin (Chart 6). While interest/debt coverage has improved for domestic issuers, operating margins and return on capital remain low and leverage has been inching higher. These trends have not been matched by foreign issuers. Perhaps most ominously, the short-term liquidity ratio has fallen quite sharply for domestic IG issuers in the euro area. Chart 6Bottom-Up Euro Area IG CHMs: Stable, But Watch Liquidity Ratios

Bottom-Up Euro Area IG CHMs: Stable, But Watch Liquidity Ratios

Bottom-Up Euro Area IG CHMs: Stable, But Watch Liquidity Ratios

For HY, the signal from the bottom-up CHM is more consistently positive between domestic and foreign issuers (Chart 7). Leverage has declined and operating margins have improved for both sets of issuers, but interest/debt coverage and liquidity are worse for domestic issuers. Chart 7Bottom-Up Euro Area High-Yield CHMs: Cyclically Healthier

Bottom-Up Euro Area High-Yield CHMs: Cyclically Healthier

Bottom-Up Euro Area High-Yield CHMs: Cyclically Healthier

Within the euro area, our bottom-up IG CHMs for Core and Periphery countries show that both remain in the “improving health” zone (Chart 8). Yet the CHM for the Core now sits on the edge of the “deteriorating health” zone, led by higher leverage, lower debt coverage and a sharply falling liquidity ratio. Notably, there is no gap between the profitability metrics of the Core and Peripheral companies used in our bottom-up CHMs. Chart 8Bottom-Up Euro Area IG CHMs: Trending In Wrong Direction

Bottom-Up Euro Area IG CHMs: Trending In Wrong Direction

Bottom-Up Euro Area IG CHMs: Trending In Wrong Direction

Peripheral European issuers continue to have much higher leverage and much lower interest coverage, the latter suggesting that Core issuers have benefitted more from the ECB’s super-easy monetary policies that have lowered borrowing costs (negative short-term interest rates, liquidity programs designed to prompt low-cost bank lending, and asset purchase programs that include buying of corporate bonds). Despite the lack of a major negative signal from the CHMs, we are concerned that the combination of slowing euro area economic growth and the end of ECB corporate bond buying will negatively impact the performance of euro area corporates (Chart 9). We are only maintaining a neutral allocation to euro area corporates, even within our current overweight stance on overall global corporates. In addition, we are sticking with our preference to favor U.S. corporates – both IG and HY – over euro area equivalents for two important reasons: stronger U.S. growth and better U.S. corporate health. Chart 9Euro Area Corporates: Stay Tactically Neutral IG & HY

Euro Area Corporates: Stay Tactically Neutral IG & HY

Euro Area Corporates: Stay Tactically Neutral IG & HY

Euro area corporates have not enjoyed the same rally that U.S. corporates have seen so far in 2019, and for good reasons. In Chart 10, we show an overall bottom-up CHM for the U.S. and euro area, combining both IG and HY are combined into a single measure for each region.2 The obvious visible trend is that U.S. corporate health has been steadily improving, while it is starting to worsen in the euro area. The gap between those two CHMs is strongly correlated to the difference in credit spreads between European and U.S. issuers (middle panel), suggesting that relative corporate health is favoring U.S. names. At the same time, the relatively stronger U.S. economy continues to support U.S. corporate performance versus euro area equivalents (bottom panel). Chart 10Relative Bottom-Up CHMs: Continue To Favor U.S. Over Europe

Relative Bottom-Up CHMs: Continue To Favor U.S. Over Europe

Relative Bottom-Up CHMs: Continue To Favor U.S. Over Europe

U.K. Corporate Health Monitor: A Brexit-Fueled Deterioration Our top-down U.K. CHM indicates that U.K. companies remain in the “improving health” zone, but just barely as the indicator has been drifting towards “deteriorating health” over the past two years. All the components of the U.K. CHM have contributed to this worsening trend (Chart 11). Even short-term liquidity, which has been in a powerful uptrend for almost a decade, has started to roll over. Chart 11U.K. Top-Down CHM: Cyclical Hit From Brexit Worries

U.K. Top-Down CHM: Cyclical Hit From Brexit Worries

U.K. Top-Down CHM: Cyclical Hit From Brexit Worries

The cause for this deterioration can be reduced to six letters: B-R-E-X-I-T. Two years of political uncertainty over the details of the U.K.’s future relationship with the European Union have eroded confidence among U.K. businesses and consumers. The result is slowing economic growth and diminished corporate profitability that has hit all earnings-related ratios in the U.K. CHM. Perhaps most disturbingly for U.K. credit performance, even the interest coverage ratio has rolled over – at a historically low level – despite the Bank of England keeping U.K. interest rates at deeply depressed levels. The toxic combination of political uncertainty and weaker economic growth has resulted in a substantial widening of U.K. credit spreads. The spread on U.K. HY corporates has widened by 293bps since September 2017 and now sits at the widest level since September 2012. U.K. IG has not seen the same degree of spread widening, but has underperformed even more on an excess return basis versus duration-matched U.K. Gilts (Chart 12). Chart 12U.K. Corporates: Brexit Uncertainty = Stay Underweight

U.K. Corporates: Brexit Uncertainty = Stay Underweight

U.K. Corporates: Brexit Uncertainty = Stay Underweight

We are currently recommending an underweight stance on U.K. corporates, even as we have become more tactically positive on overall global corporate exposure. While credit spreads have widened to levels that appear to offer value, U.K. economic momentum is fading steadily and leading economic indicators are pointing to even slower growth in 2019. With Conservative Prime Minster Theresa May now in a dramatically weakened position after losing the recent vote on her Brexit deal with the EU, there are no immediate options that will solve the Brexit uncertainty in a way that will provide a lasting boost to U.K. business confidence. In fact, the only realistic options – postponing Brexit, fresh U.K. elections, even a second Brexit referendum – all involve a period of even more uncertainty that will weigh on the performance of U.K. corporate debt. Japan Corporate Health Monitor: A Negative Signal Our bottom-up Japan CHM3 has consistently stayed in the “Improving health” zone since 2010; however, the most recent data shows that the health of Japanese corporates has started to deteriorate as the last data point from Q3/2018 is just above the zero line (Chart 13). The overall Japanese economy has generally performed well (by Japanese standards) over the past few years, boosted by “Abenomics” economic stimulus combined with the extraordinarily easy monetary policies of the Bank of Japan. Yet the slowing of global growth momentum seen in 2018 has weighed on the performance of the Japanese corporate sector, which is still heavily geared to exports and global growth. Chart 13Japan Bottom-Up CHM: Cyclical Deterioration

Japan Bottom-Up CHM: Cyclical Deterioration

Japan Bottom-Up CHM: Cyclical Deterioration

Looking at the components of the CHM, there was a modest deterioration of all the ratios last year, except for profit margins which have been virtually unchanged since 2015. On an absolute basis, the CHM components do not suggest any major problems with Japanese credit quality. Japanese companies are not highly levered and liquidity remains near the highest level seen since at least the mid-2000s. Interest coverage is still high on a historical basis and is much higher than the ratios seen in the other major developed markets. Yet at the same time, return on capital and profit margins remain very low compared to those same other major economies. Japanese companies remain cash-rich with low debt levels – a sharp contrast to the other countries show in this report. There are many potential cyclical risks for Japanese corporates in 2019: even weaker demand for Japanese exports, the drag on Japanese capital spending from firms worried about slowing global growth and the spillover effects from the U.S.-China trade war, even a possible hike in the consumption tax that the Abe government is still considering for October of this year. Yet these all would prevent any adjustment of the interest rate policy of the Bank of Japan, which remains the biggest factor to consider when looking at the investment prospects of Japanese corporate bonds. Japanese corporate spreads did not widen much compared to other countries’ corporate spreads in the 2018 selloff, due to their relative illiquidity and the extreme low level of interest rates in Japan. As the central bank is under no pressure to move off its current hyper-easy monetary policy settings, government bond yields and corporate spreads will remain low, even if the Japanese economy continues to slow. Therefore, for those investors who have access to the relatively small Japanese corporate debt market, we continue to recommend an overweight stance on Japanese corporates vs Japanese government bonds (Chart 14). Chart 14Japan Corporates: Stay Overweight Vs JGBs

Japan Corporates: Stay Overweight Vs JGBs

Japan Corporates: Stay Overweight Vs JGBs

Canada Corporate Health Monitor: Now Even Healthier Both our top-down and bottom-up Canadian CHMs indicate an improving trend in Canadian corporate health (Chart 15). Steady above-trend economic growth, combined with some increases in realized inflation, have helped boost the profitability and interest/debt coverage ratios. Yet not all the news is good - leverage is high and rising, while the absolute levels of return on capital and debt/interest coverage are low. This may be building up risks for the next Canadian economic downturn but, for now, Canadian companies look in decent shape. Chart 15Canada CHMs: Supported By Solid Growth

Canada CHMs: Supported By Solid Growth

Canada CHMs: Supported By Solid Growth

With so much of Canada’s economy (and its financial markets) geared to the performance of the energy sector, the recent recovery in global oil prices is a significant boost for the overall Canadian corporate market. Our commodity strategists see additional upside in oil prices over the next 6-9 months, which will further underpin the health of Canadian oil companies. Canadian corporates were not immune to the period of global spread widening seen at end of 2018, but the magnitude of the move was modest (Chart 16). This is a function of the still-low interest rate environment in Canada, where the Bank of Canada has not yet lifted policy rates to its own estimate of neutral (2.5-3.5%). Easy monetary conditions and relatively low Canadian interest rates will continue to make Canadian corporates relatively attractive, in an environment of decent growth and firm corporate health. Chart 16Canadian Corporates: Stay Overweight Vs Canadian Govt. Debt

Canadian Corporates: Stay Overweight Vs Canadian Govt. Debt

Canadian Corporates: Stay Overweight Vs Canadian Govt. Debt

We continue recommending an overweight position in Canadian corporate debt relative to Canadian government bonds on a tactical basis. Spreads have been in a very stable range since the 2009 recession, ranging between 100-200bps even during periods when our CHMs were indicating worsening corporate health. To break out of that range to the upside, we would need to see a sharp deterioration of Canadian economic growth or several more rate hikes from the Bank of Canada – neither outcome is likely over at least the next six months. Yet given how closely the Bank of Canada has been tracking the Fed’s current tightening cycle, we anticipate downgrading Canadian corporates at the same time do the same for U.S. corporates, likely around mid-2019. Robert Robis, CFA, Senior Vice President Global Fixed Income Strategy rrobis@bcaresearch.com Ray Park, CFA, Research Analyst ray@bcaresearch.com Appendix 1: An Overview Of The BCA Corporate Health Monitors The BCA Corporate Health Monitor (CHM) is a composite indicator designed to assess the underlying financial strength of the corporate sector for a country. The Monitor is an average of six financial ratios inspired by those used by credit rating agencies to evaluate individual companies. However, we calculate our ratios using top-down (national accounts) data for profits, interest expense, debt levels, etc. The idea is to treat the entire corporate sector as if it were one big company, and then look at the credit metrics that would be used to assign a credit rating to it. Importantly, only data for the non-financial corporate sector is used in the CHM, as the measures that would be used to measure the underlying health of banks and other financial firms are different than those for the typical company. The six ratios used in the CHM are shown in Table 1 below. To construct the CHM, the individual ratios are standardized, added together, and then shown as a deviation from the medium-term trend. That last part is important, as it introduces more cyclicality into the CHM and allows it to better capture major turning points in corporate well-being. Largely because of this construction, the CHM has a very good track record at heralding trend changes in corporate credit spreads (both for Investment Grade and High-Yield) over many cycles. Table 1Definitions Of Ratios That Go Into The CHMs

BCA Corporate Health Monitor Chartbook: Still OK … For Now

BCA Corporate Health Monitor Chartbook: Still OK … For Now

Top-down CHMs are now available for the U.S., euro area, the U.K. and Canada. The CHM methodology was extended in 2016 to look at corporate health by industry and by credit quality.4 The financial data of a broad set of individual U.S. and euro area companies was used to construct individual “bottom-up” CHMs using the same procedure as the more familiar top-down CHM. Some of the ratios differ from those used in the top-down CHM (see Table 1), largely due to definitional differences in data presented in national income accounts versus those from actual individual company financial statements. The bottom-up CHMs analyze the health of individual sectors, and can be aggregated up into broad CHMs for Investment Grade and High-Yield groupings to compare with credit spreads. In 2018, we introduced bottom-up CHMs for Japan and Canada. With the country expansion of our CHM universe, we now have coverage for 92% of the Bloomberg Barclays Global Aggregate Corporate Bond Index (Appendix Chart 1).

Image

Appendix 2: U.S. Bottom-Up CHMs For Selected Sectors

APPENDIX 2: ENERGY SECTOR

APPENDIX 2: ENERGY SECTOR

APPENDIX 2: MATERIALS SECTOR

APPENDIX 2: MATERIALS SECTOR

APPENDIX 2: COMMUNICATIONS SECTOR

APPENDIX 2: COMMUNICATIONS SECTOR

APPENDIX 2: CONSUMER DISCRETIONARY SECTOR

APPENDIX 2: CONSUMER DISCRETIONARY SECTOR

APPENDIX 2: CONSUMER STAPLES SECTOR

APPENDIX 2: CONSUMER STAPLES SECTOR

APPENDIX 2: HEALTH CARE SECTOR