Corporate

What do the mixed signals sent by the UK economy mean for the Bank of England, and what are the implications for Gilts and the British pound?

According to BCA Research’s Global Asset Allocation service, there are clear signs that growth is weakening. BCA’s Global Nowcast has been slowing for three months. Behind this slowdown is the fact that the US consumer – the biggest factor keeping growth…

Chinese industrial profits growth accelerated in June, rising from 0.7% y/y to 3.6%. Profits expanded at 3.5% in the first half of 2024, compared to 3.4% in the first half of 2023, and suggest that China’s manufacturing sector remains resilient. A slower…

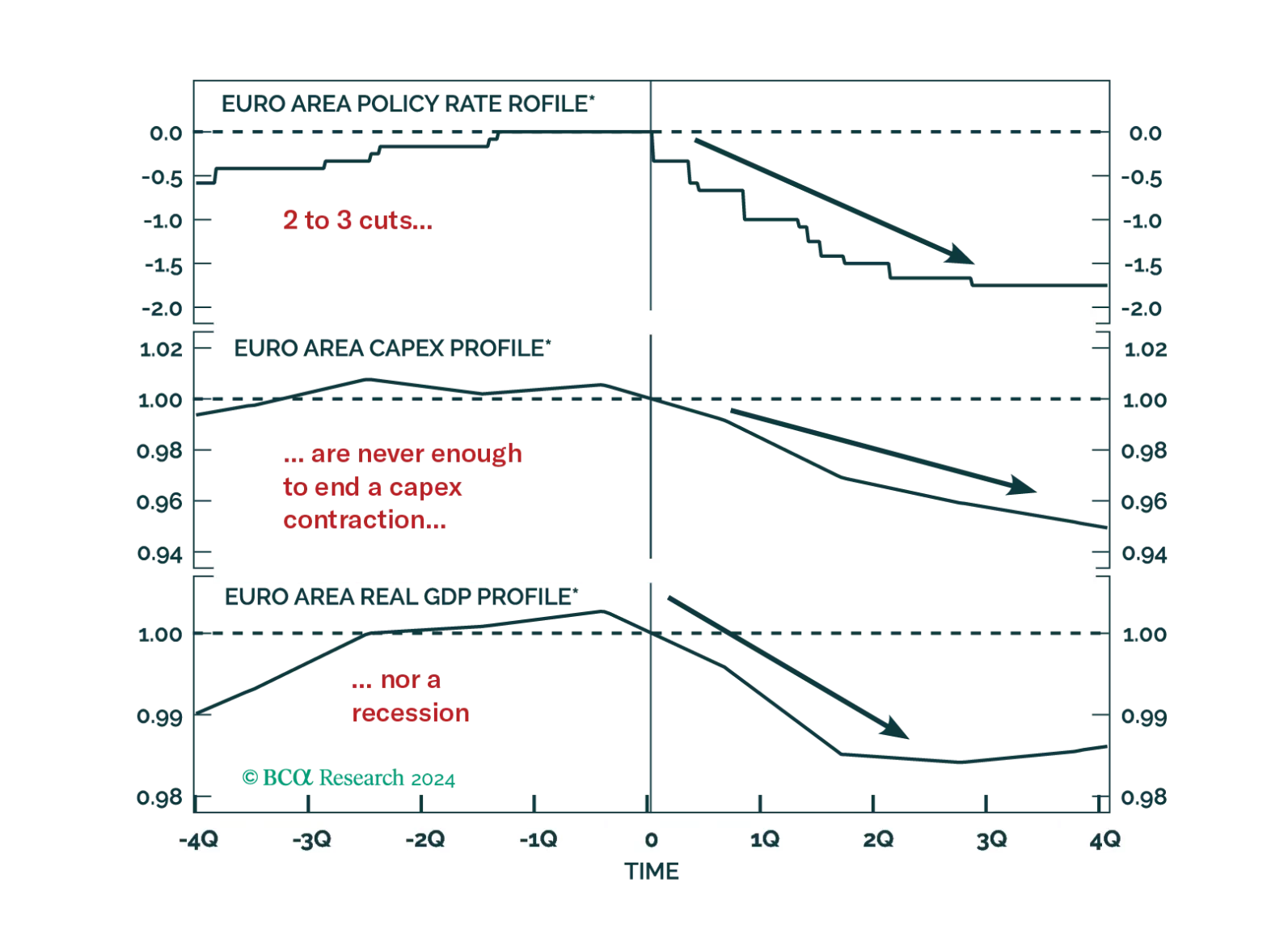

Investors hope that the ECB rate cuts priced into the curve will be sufficient to achieve a soft landing in Europe. History argues against this view, but will this time be different?

Equity investors have been skittish about mid-cap banks ever since Silicon Valley Bank failed in March 2023. The S&P MidCap 400 Regional Banks Index remains 4% below its February 2023 high while the S&P 500 Diversified Banks Index, dominated by the…

Total consumer credit rose by USD 11.4 billion in May (to USD 5,065 billion outstanding) from a slightly upwardly revised USD 6.5 billion increase in April, surpassing expectations of a smaller increase. Notably, revolving credit (which includes credit cards)…

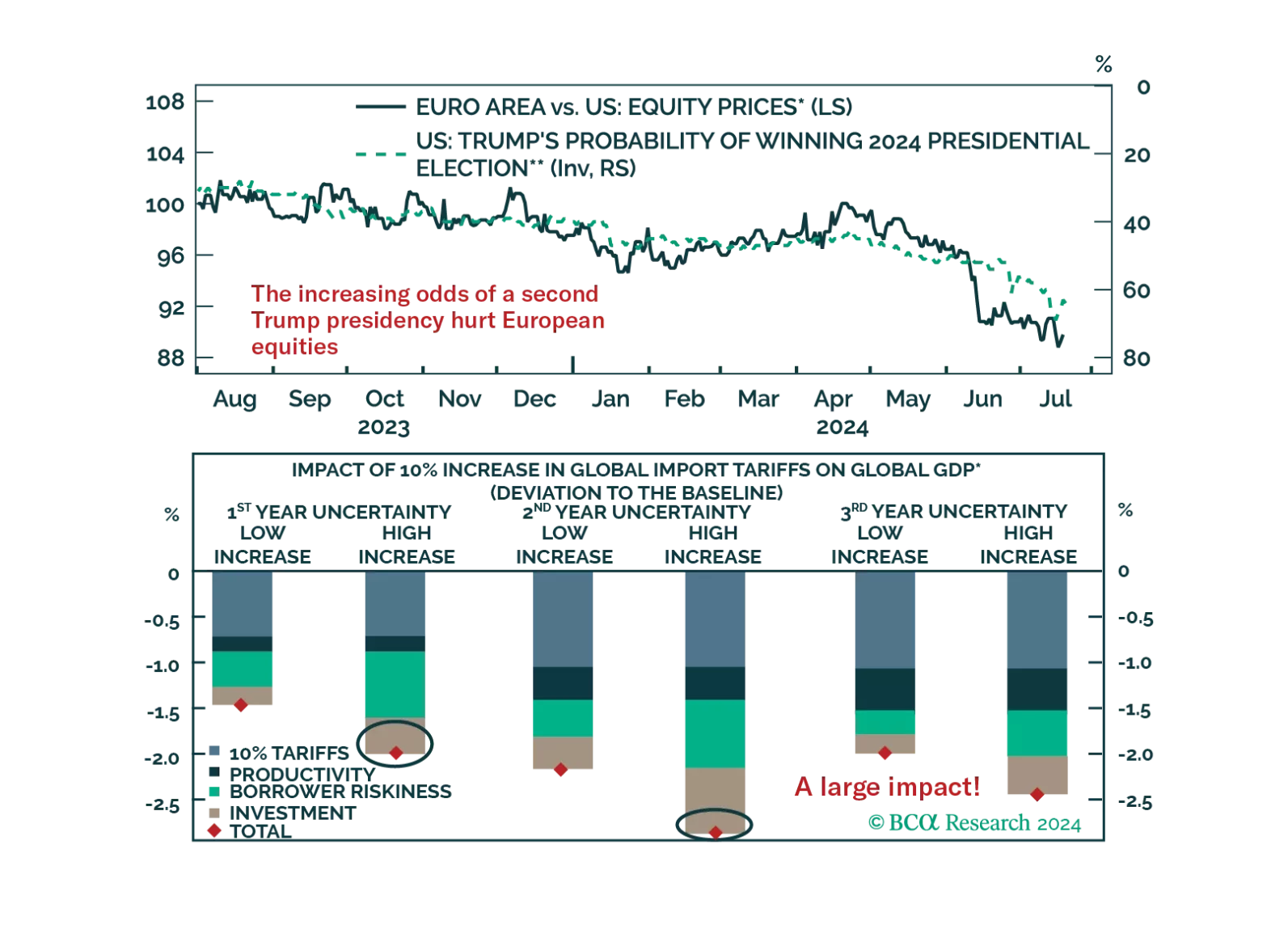

As Trump’s victory odds rise, the underperformance of European equities deepens. How negative would a global trade war be for European assets?

Second quarter earnings season began for US public companies on Friday as JPMorgan (JPM), Citigroup (C) and Wells Fargo (WFC) reported their results before the open. (BAC, the other commercial bank SIFI (systemically important financial institution), reports…

According to BCA Research’s Emerging Markets Strategy service, extremely disappointing corporate profit growth has been the main reason for EM's poor equity performance in absolute terms and massive underperformance relative to the US/DM. EM earnings per…

Our colleagues from the Emerging Markets Strategy team argue that investors should brace for a significant correction in Indian stocks in the coming months. They posit that the pillar of Indian corporations' sustained profit growth — surging revenues — is…