Corporate Bonds

In this report, we present our performance review of the BCA Research Global Fixed Income Strategy (GFIS) model bond portfolio for the Q2/2023, and the outlook and scenario analysis for the next six months. The portfolio return exactly matched that of the benchmark index during the quarter, as modest gains on government bond allocations in the US, UK and core Europe completely offset losses on spread product underweights. Looking ahead, the portfolio is positioned to capitalize on an expected slowing of global growth over the rest of the year through an overweight stance on government bonds versus spread product and above-benchmark duration tilts in the US and core Europe.

This week we present our Portfolio Allocation Summary for July 2023.

Recession is on track to start around year-end. Stocks usually peak shortly before recession begins. So, position defensively but be prepared for a few more months of the rally.

We build a four-stage business cycle framework based on economic growth and capacity utilization, and then analyze historical returns for most major asset allocation decisions for each stage. Given that we are in the early recession stage (negative growth coupled and an overheated economy), our framework recommends a defensive positioning across all asset classes.

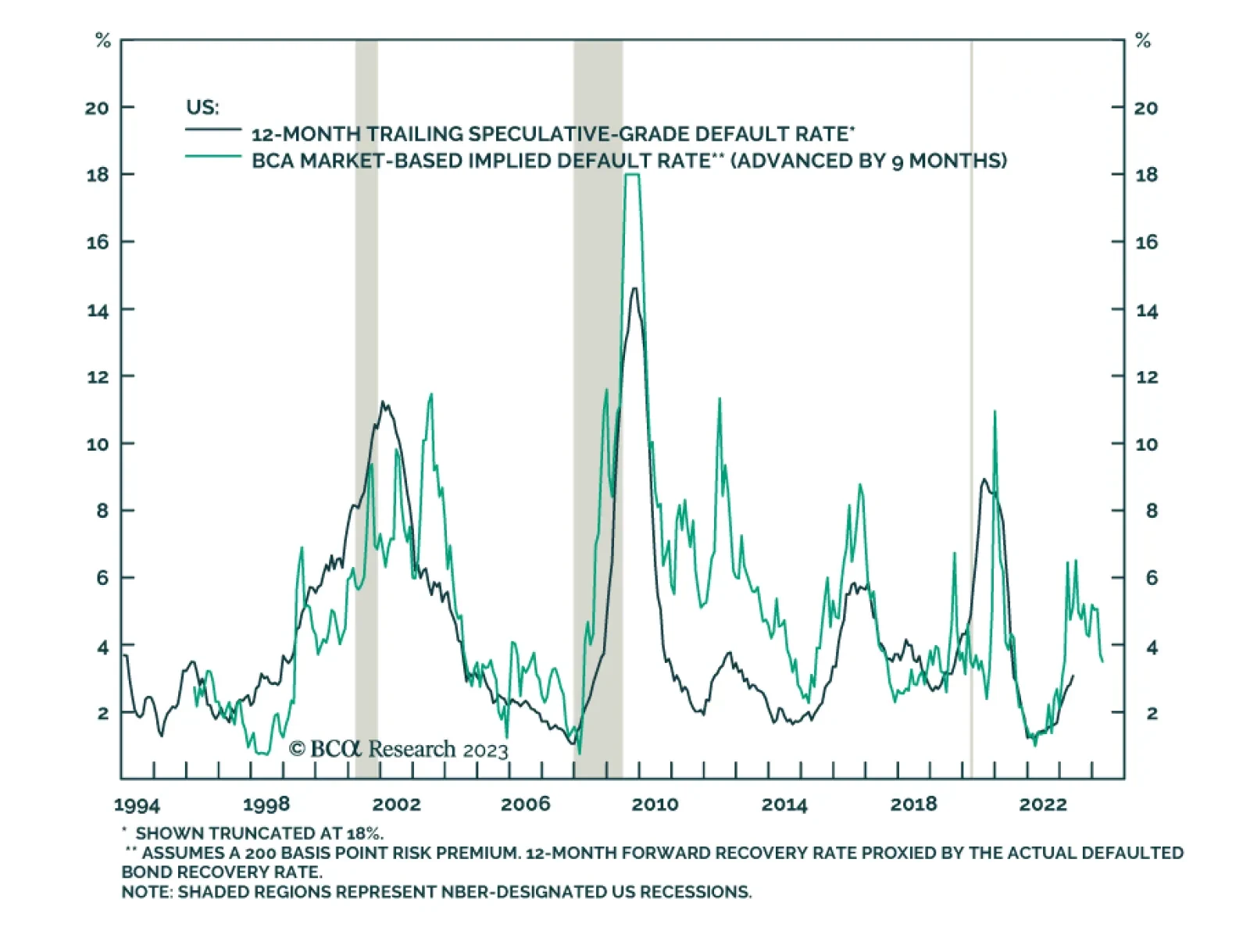

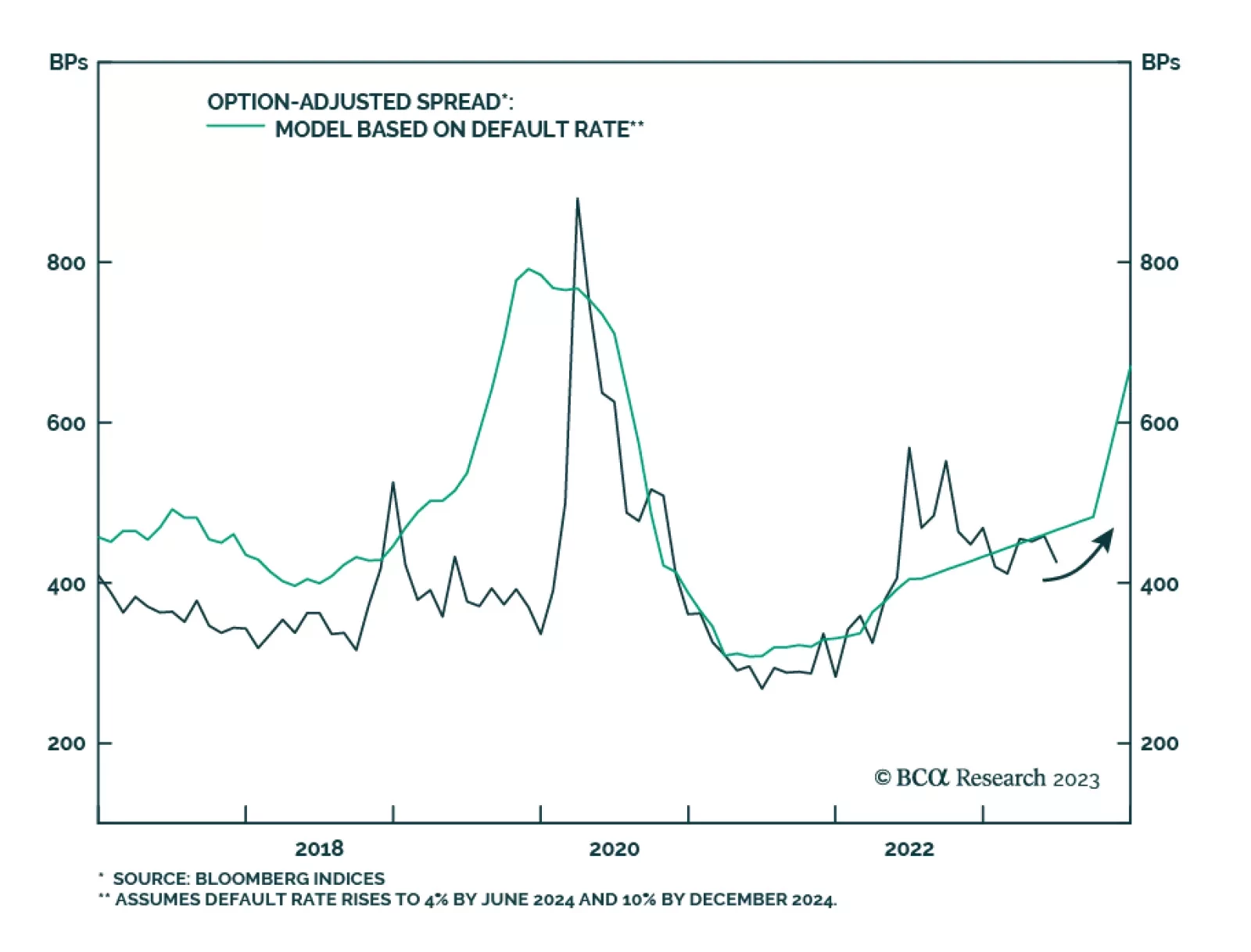

This week’s Special Report updates our US default rate forecast and considers whether corporate bond spreads offer value given the trend in credit fundamentals. We also consider the relative value proposition between investment grade and high-yield credit and between European and US corporate bonds.

This week we present our Portfolio Allocation Summary for June 2023.

Risk assets would perform well over 12 months only if inflation falls to 2% without triggering a recession. That would be unprecedented. We recommend investors stay defensive.

In this US Bond Strategy Insight we discuss the outlook for bank bonds.