Corporate Bonds

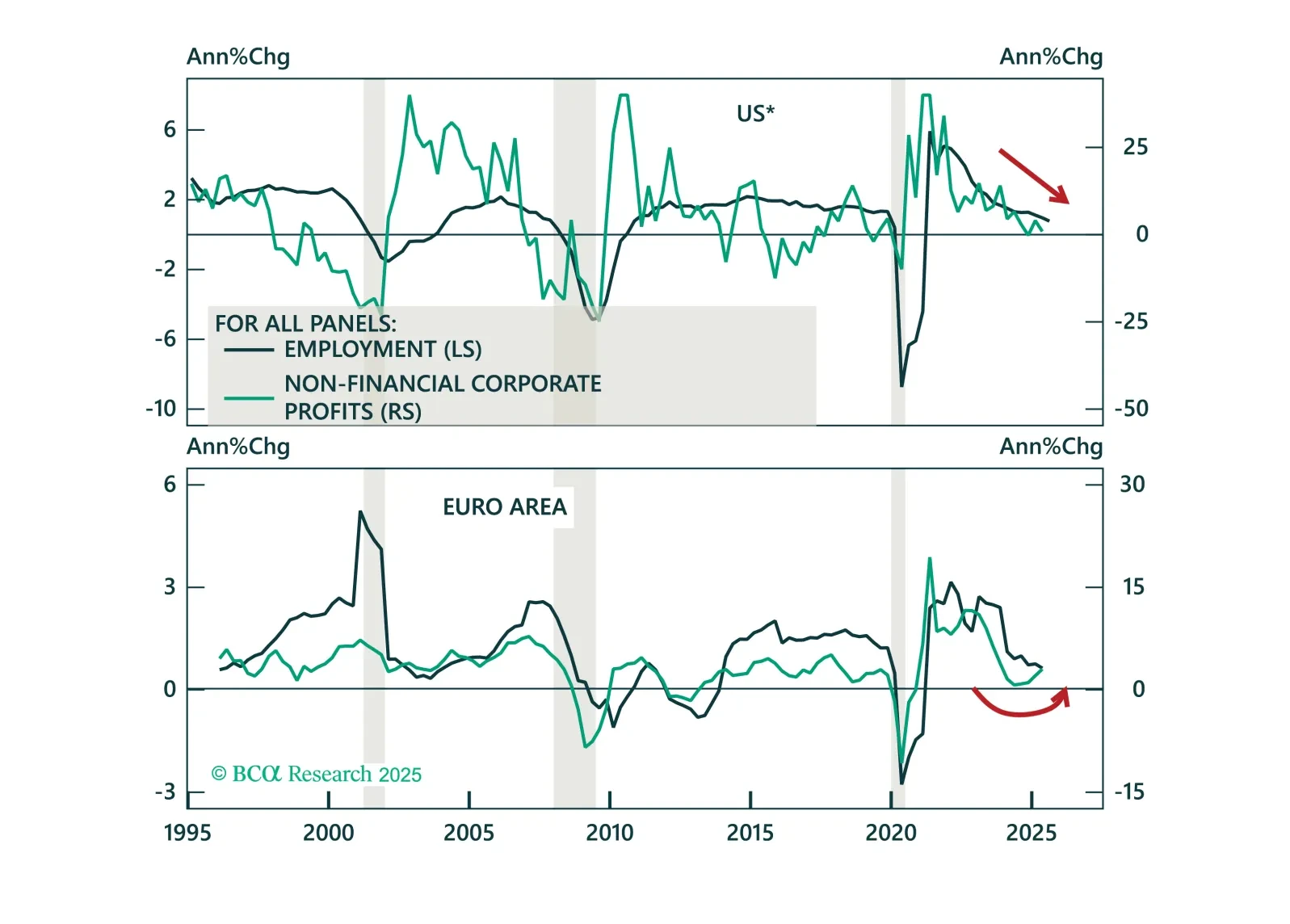

In this Q4 Strategy Outlook, we discuss where we stand on our recession call, the outlook for stocks and bonds in various scenarios, why investors are misunderstanding the impact of AI on corporate profits, whether the US dollar has entered a structural downtrend, our perspective on the yen, gold and other commodities, and much more.

Despite concerns about fiscal sustainability, a rise in term premia, and attacks on central bank independence, monetary policy remains the primary driver of bond markets. In our Q3 Review & Outlook, we update our views and identify opportunities in government bonds, short-term interest rate futures, global yield curves, inflation-linked bonds, and credit.

Our Portfolio Allocation Summary for October 2025.

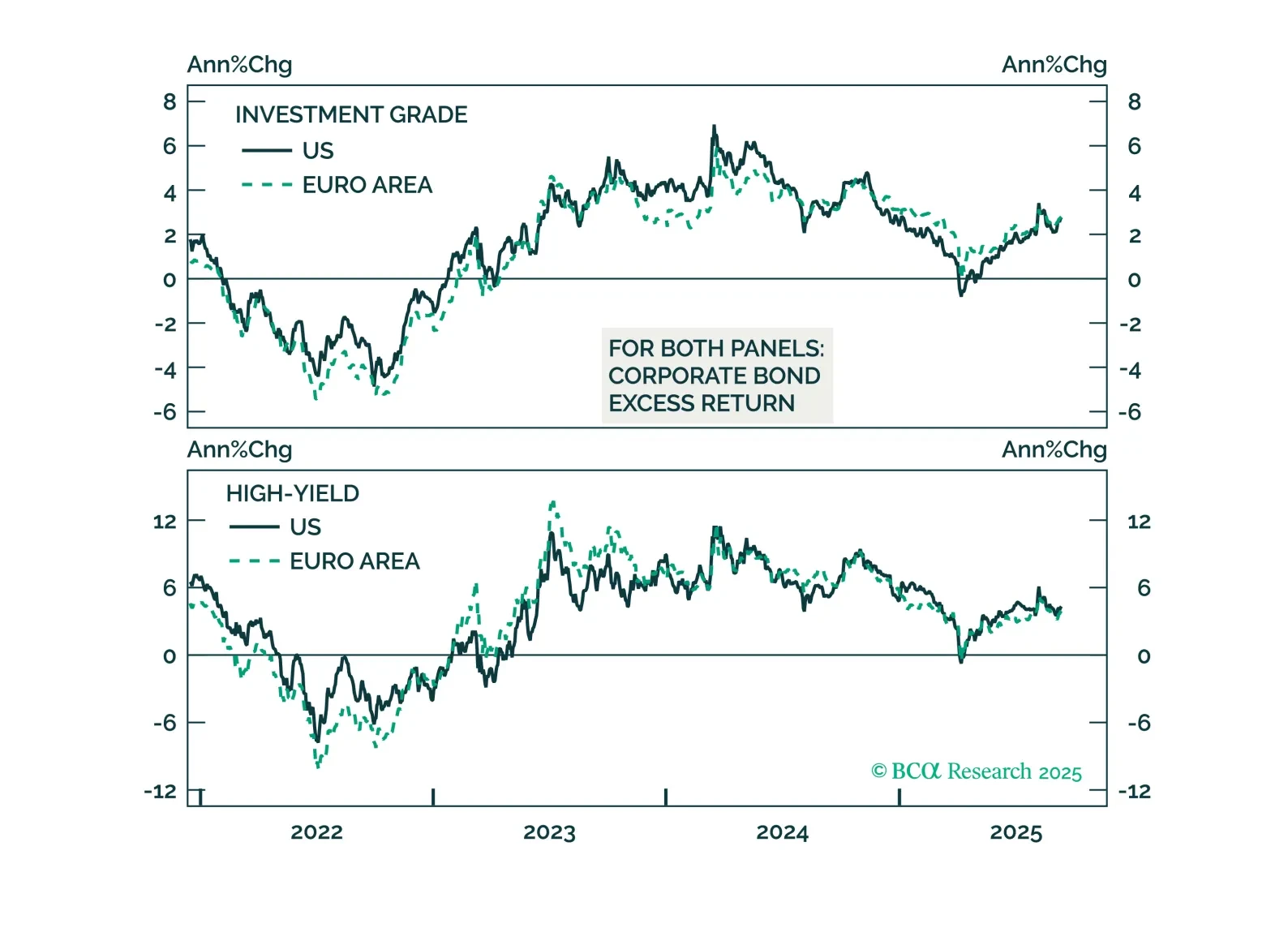

Structural tailwinds help explain tight credit spreads. In Europe, we see room for further tightening. Stay underweight US credit amid cyclical risks, but upgrade Euro Area IG to overweight and HY to neutral.

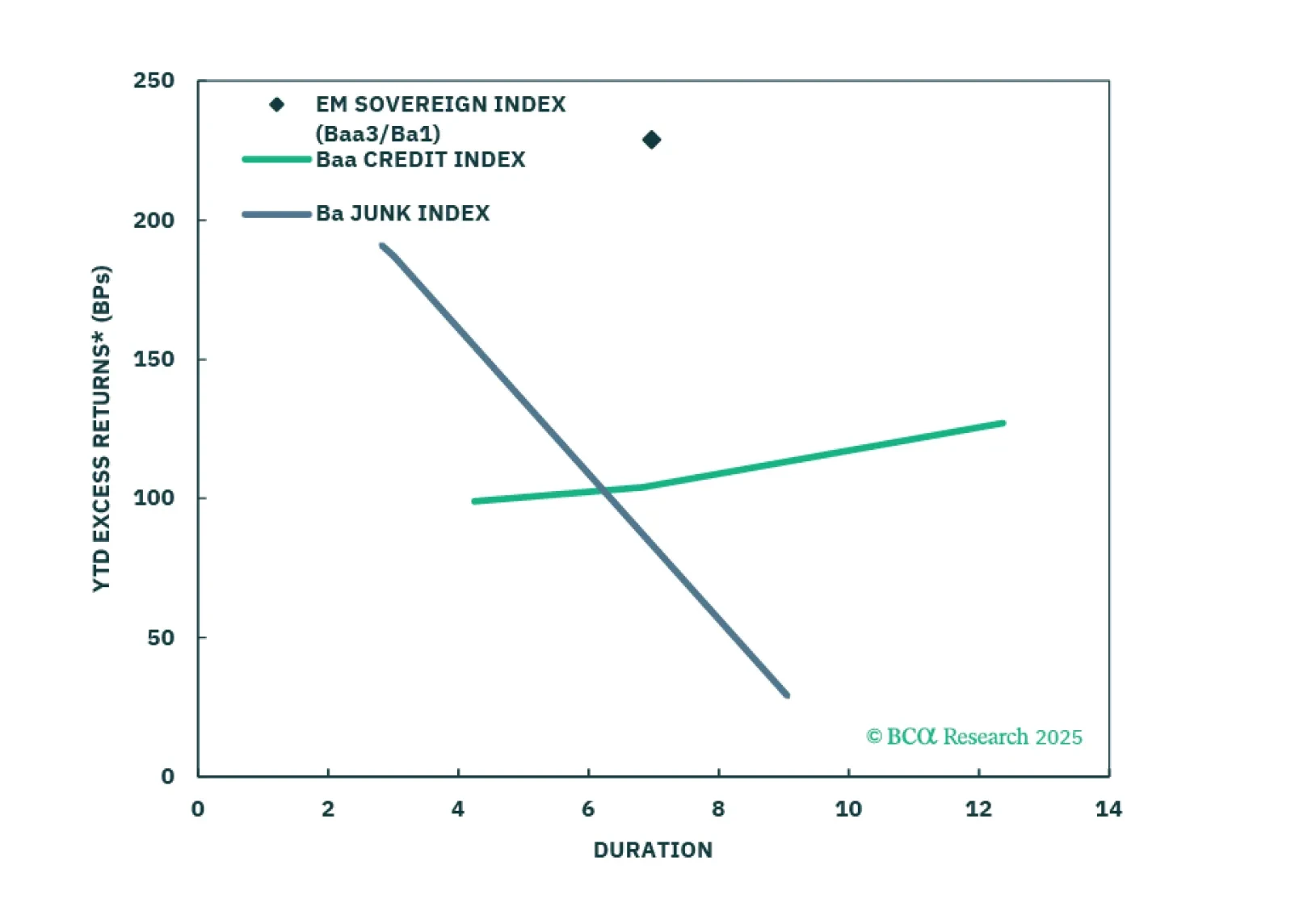

USD-denominated Emerging Market bonds have been outperforming US corporates for the past year. We don’t think the rally is exhausted yet.

Our Portfolio Allocation Summary for September 2025.

Our Portfolio Allocation Summary for August 2025.

Our Portfolio Allocation Summary for July 2025.

Investors should modestly underweight equities in their portfolios and look to turn more aggressively defensive once the whites of the recession’s eyes are visible. We think that will happen within the next few months.