Corporate Bonds

Highlights Chart 1How Long Until Full Employment?

How Long Until Full Employment?

How Long Until Full Employment?

It’s official. The vaccination roll-out is successfully suppressing the spread of COVID-19 throughout the United States and the associated economic re-opening is leading to a surge in activity. Not only did March’s ISM Manufacturing PMI come in at 64.7, its highest reading since 1983, but the economy also added 916 thousand jobs during the month. Interestingly, the 10-year Treasury yield was relatively stable last week despite the eye-catching economic data. This is likely because the Treasury curve already discounted a significant rebound in economic activity and last week’s data merely confirmed the market’s expectations. At present, the Treasury curve is priced for Fed liftoff in September 2022 and a total of five rate hikes by the end of 2023. By our calculations, the Fed will be ready to lift rates by the end of 2022 if monthly employment growth averages at least 410k between now and then (Chart 1). If payroll growth can somehow stay above 701k per month, then the Fed will hit its “maximum employment” target by the end of this year. While a lot of good news is already priced in the Treasury curve, the greatest near-term risk is that the data continue to beat expectations. Maintain below-benchmark portfolio duration. Feature Table 1Recommended Portfolio Specification

It’s A Boom!

It’s A Boom!

Table 2Fixed Income Sector Performance

It’s A Boom!

It’s A Boom!

Investment Grade: Neutral Chart 2Investment Grade Market Overview

Investment Grade Market Overview

Investment Grade Market Overview

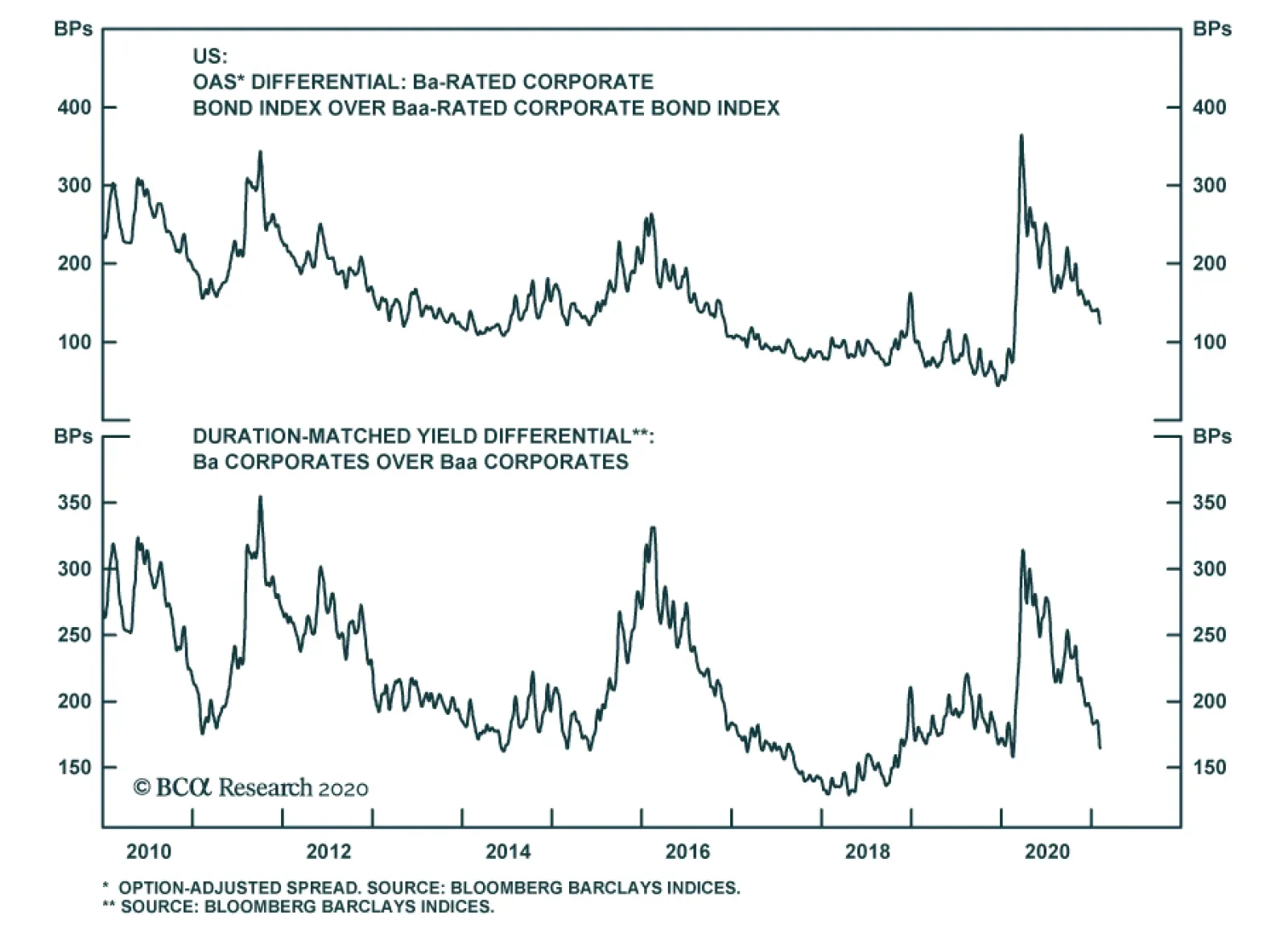

Investment grade corporate bonds outperformed the duration-equivalent Treasury index by 29 basis points in March, bringing year-to-date excess returns up to +98 bps. The combination of above-trend economic growth and accommodative monetary policy supports positive excess returns for spread product versus Treasuries. Though Treasury yields have risen, this does not yet pose a risk for credit spreads. The 5-year/5-year forward TIPS breakeven inflation rate remains below the Fed’s target range of 2.3% to 2.5%. We won’t be concerned about restrictive monetary policy pushing spreads wider until inflation expectations are well-anchored around the Fed’s target. Despite the positive macro back-drop, investment grade corporate valuations are extremely tight. The investment grade corporate index’s 12-month breakeven spread is down to its 2nd percentile (Chart 2). This means that the breakeven spread has only been tighter 2% of the time since 1995. The same measure shows that Baa-rated bonds have also only been more expensive 2% of the time (panel 3). We don’t anticipate material underperformance versus Treasuries, but we see better value outside of the investment grade corporate space.1 Specifically, we advise investors to favor tax-exempt municipal bonds over investment grade corporates with the same credit rating and duration. We also prefer USD-denominated Emerging Market Sovereign bonds over investment grade corporates with the same credit rating and duration. Finally, the supportive macro environment means we are comfortable adding credit risk to a portfolio. With that in mind, we encourage investors to pick up the additional spread offered by high-yield corporates. Table 3ACorporate Sector Relative Valuation And Recommended Allocation*

It’s A Boom!

It’s A Boom!

Table 3BCorporate Sector Risk Vs. Reward*

It’s A Boom!

It’s A Boom!

High-Yield: Overweight Chart 3High-Yield Market Overview

High-Yield Market Overview

High-Yield Market Overview

High-Yield outperformed the duration-equivalent Treasury index by 83 basis points in March, bringing year-to-date excess returns up to +263 bps. In last week’s report we looked at the default expectations that are currently priced into the junk index and considered whether they are likely to be met.2 If we demand an excess spread of 100 bps and assume a 40% recovery rate on defaulted debt, then the High-Yield index embeds an expected default rate of 3.4% (Chart 3). Using a model of the speculative grade default rate that is based on gross corporate leverage (aka pre-tax profits over debt) and C&I lending standards, we can estimate a likely default rate for the next 12 months using assumptions for profit and debt growth. The median FOMC forecast of 6.5% real GDP growth in 2021 is consistent with 31% corporate profit growth. We also assume that last year’s debt binge will be followed by relatively weak corporate debt growth in 2021. According to our model, 30% profit growth and 2% debt growth is consistent with a default rate of 3.4% for the next 12 months, exactly matching what is priced into junk spreads. Given that the Fed’s 6.5% real GDP growth forecast looks conservative given the large amount of fiscal stimulus coming down the pike, and the fact that the combination of strong economic growth and accommodative monetary policy could easily cause valuations to overshoot in the near-term, we are inclined to maintain an overweight allocation to High-Yield bonds. MBS: Underweight Chart 4MBS Market Overview

MBS Market Overview

MBS Market Overview

Mortgage-Backed Securities outperformed the duration-equivalent Treasury index by 17 basis points in March, bringing year-to-date excess returns up to +15 bps. The nominal spread between conventional 30-year MBS and equivalent-duration Treasuries tightened 12 bps in March. This spread remains wide compared to levels seen during the past few years, but it is still tight compared to the recent pace of mortgage refinancings (Chart 4). The MBS option-adjusted spread (OAS) currently sits at 19 bps. This is considerably below the 52 bps offered by Aa-rated corporate bonds, the 38 bps offered by Agency CMBS and the 27 bps offered by Aaa-rated consumer ABS. All in all, the value in MBS is not appealing compared to other similarly risky sectors. The plummeting primary mortgage spread was a key reason for the elevated refi activity seen during the past year. However, the spread has now recovered back to more typical levels (bottom panel). The implication is that further increases in Treasury yields will likely be matched by higher mortgage rates, meaning that mortgage refinancings have probably peaked. The coming drop in refi activity will be positive for MBS returns, but we aren’t yet ready to turn bullish on the sector. First, as mentioned above, value is poor compared to other similarly risky sectors. Second, the gap between the nominal MBS spread and the MBA Refinance Index remains wide (panel 2) and we could still see spreads adjust higher. Government-Related: Neutral Chart 5Government-Related Market Overview

Government-Related Market Overview

Government-Related Market Overview

The Government-Related index outperformed the duration-equivalent Treasury index by 45 basis points in March, bringing year-to-date excess returns up to +66 bps (Chart 5). Sovereign debt outperformed duration-equivalent Treasuries by 157 bps in March, bringing year-to-date excess returns up to +40 bps. Foreign Agencies outperformed the Treasury benchmark by 8 bps on the month, bringing year-to-date excess returns up to +33 bps. Local Authority bonds outperformed by 81 bps in March, bringing year-to-date excess returns up to +286 bps. Domestic Agency bonds underperformed by 2 bps, dragging year-to-date excess returns down to +14 bps. Supranationals outperformed by 7 bps, bringing year-to-date excess returns up to +13 bps. We recently took a detailed look at valuation for USD-denominated Emerging Market (EM) Sovereigns.3 We found that, on an equivalent-duration basis, EM Sovereigns offer a spread advantage over investment grade US corporates. Attractive countries include: Qatar, UAE, Mexico, Russia and Colombia We prefer US corporates over EM Sovereigns in the high-yield space. Ba-rated high-yield US corporates offer a spread advantage over Ba-rated EM Sovereigns and the lower EM credit tiers are dominated by distressed credits like Turkey and Argentina. Municipal Bonds: Overweight Chart 6Municipal Market Overview

Municipal Market Overview

Municipal Market Overview

Municipal bonds outperformed the duration-equivalent Treasury index by 187 basis points in March, bringing year-to-date excess returns up to +291 bps (before adjusting for the tax advantage). Municipal bond spreads have tightened dramatically during the past few months and Aaa-rated Munis now look expensive compared to Treasuries, with the exception of the short-end of the curve (Chart 6). That said, if we match the duration and credit rating between the Bloomberg Barclays Municipal bond indexes and the US Credit index, we find that both General Obligation (GO) and Revenue Munis appear attractive compared to US investment grade Credit, with the possible exception of some short-maturity GO bonds. Revenue Munis offer a before-tax yield pick-up relative to US Credit for maturities above 12 years (bottom panel). Revenue bonds in the 8-12 year maturity bucket offer an after-tax yield pick-up versus Credit for investors with an effective tax rate above 13% (panel 3). Revenue bonds in the 6-8 year maturity bucket offer an after-tax yield pick-up versus Credit for investors with an effective tax rate above 24%. GO Munis with 17+ years to maturity offer an after-tax yield pick-up relative to Credit for investors with an effective tax rate above 1%. This breakeven effective tax rate rises to 6% for the 12-17 year maturity bucket, 23% for the 8-12 year maturity bucket (panel 3) and 32% for the 6-8 year maturity bucket. All in all, municipal bond value has deteriorated markedly in recent months and we downgraded our recommended allocation from “maximum overweight” to “overweight” in January. However, investors should still prefer municipal bonds over investment grade corporate bonds with the same credit rating and duration. Treasury Curve: Buy 5-Year Bullet Versus 2/10 Barbell Chart 7Treasury Yield Curve Overview

Treasury Yield Curve Overview

Treasury Yield Curve Overview

Treasury yields moved up dramatically in March, with the curve steepening out to the 10-year maturity point and flattening thereafter. The 2/10 Treasury slope steepened 28 bps to end the month at 158 bps. The 5/30 slope steepened 7 bps to end the month at 149 bps (Chart 7). As we showed in a recent report, the Treasury curve continues to trade directionally with yields out to the 10-year maturity point.4 Beyond 10 years, the curve has transitioned into a bear flattening/bull steepening regime where higher yields coincide with a flatter curve and vice-versa (bottom panel). For now, we are content to stick with our recommended steepener: long the 5-year bullet and short a duration-matched 2/10 barbell. However, we will eventually be close enough to an expected Fed liftoff date that the 5/10 slope will follow the 10/30 slope and transition into a bear-flattening/bull-steepening regime. When that happens, it will make more sense to either position for a steepener at the front-end of the curve (long 3-year bullet / short 2/5 barbell) or a flattener at the long-end of the curve (long 5/30 barbell / short 10-year bullet). We don’t yet see sufficient evidence of 5/10 bear-flattening to shift out of our current recommended position and into these new ones, and so we stay the course for now. TIPS: Overweight Chart 8TIPS Market Overview

TIPS Market Overview

TIPS Market Overview

TIPS outperformed the duration-equivalent nominal Treasury index by 155 basis points in March, bringing year-to-date excess returns up to +341 bps. The 10-year TIPS breakeven inflation rate rose 22 bps on the month and it currently sits at 2.38%. The 5-year/5-year forward TIPS breakeven inflation rate rose 30 bps in March and it currently sits at 2.15%. Despite last month’s sharp move higher, the 5-year/5-year forward breakeven rate is still below the Fed’s target range of 2.3% to 2.5% (Chart 8). This means that the rising cost of inflation protection is not yet a concern for the Fed, and in fact, the Fed would like to encourage it to rise further still. Our recommended positions in inflation curve flatteners and real curve steepeners continued to perform well last month. The 5/10 TIPS breakeven inflation slope was relatively stable, but the 2/10 CPI swap slope flattened 8 bps (panel 4). The 2/10 real yield curve steepened 31 bps in March to reach 169 bps (bottom panel). An inverted inflation curve has been an unusual occurrence during the past few years, but we think it will be the normal state of affairs going forward. The Fed’s new strategy involves allowing inflation to rise above 2% so that it can attack its inflation target from above rather than from below. This new monetary environment is much more consistent with an inverted inflation curve than an upward sloping one, and we would resist the temptation to put on an inflation curve steepener. ABS: Overweight Chart 9ABS Market Overview

ABS Market Overview

ABS Market Overview

Asset-Backed Securities underperformed the duration-equivalent Treasury index by 4 basis points in March, dragging year-to-date excess returns down to +16 bps. Aaa-rated ABS underperformed by 5 bps on the month, dragging year-to-date excess returns down to +8 bps. Non-Aaa ABS underperformed by 2 bps, dragging year-to-date excess returns down to +56 bps. The stimulus from last year’s CARES act led to a significant increase in household savings when individual checks were mailed last April. This excess savings has still not been spent and now another round of checks is poised to push the savings rate higher again (Chart 9). The large stock of household savings means that the collateral quality of consumer ABS is very high, with many households using their windfall to pay down debt (bottom panel). Investors should remain overweight consumer ABS and take advantage of strong collateral performance by moving down in credit quality. The Treasury department’s decision to let the Term Asset-Backed Loan Facility (TALF) expire at the end of 2020 does not alter our recommendation. Spreads are already well below the borrowing cost that was offered by TALF, and these tight spread levels are justified by strong household balance sheets. Non-Agency CMBS: Neutral Chart 10CMBS Market Overview

CMBS Market Overview

CMBS Market Overview

Non-Agency Commercial Mortgage-Backed Securities underperformed the duration-equivalent Treasury index by 10 basis points in March, dragging year-to-date excess returns down to +77 bps. Aaa Non-Agency CMBS underperformed Treasuries by 23 bps in March, dragging year-to-date excess returns down to +14 bps. Meanwhile, non-Aaa Non-Agency CMBS outperformed by 30 bps, bringing year-to-date excess returns up to +293 bps (Chart 10). We continue to recommend an overweight allocation to Aaa-rated Non-Agency CMBS and an underweight allocation to non-Aaa CMBS. Even with the expiry of TALF, Aaa CMBS spreads are already well below the cost of borrowing through TALF and thus won’t be negatively impacted. Meanwhile, the structurally challenging environment for commercial real estate could lead to problems for lower-rated CMBS (panels 3 & 4). Agency CMBS: Overweight Agency CMBS outperformed the duration-equivalent Treasury index by 10 basis points in March, bringing year-to-date excess returns up to +49 bps. The average index option-adjusted spread tightened 5 bps on the month and it currently sits at 38 bps (bottom panel). Though Agency CMBS spreads have completely recovered back to their pre-COVID lows, they still look attractive compared to other similarly risky spread products. Stay overweight. Appendix A: Butterfly Strategy Valuations The following tables present the current read-outs from our butterfly spread models. We use these models to identify opportunities to take duration-neutral positions across the Treasury curve. The following two Special Reports explain the models in more detail: US Bond Strategy Special Report, “Bullets, Barbells And Butterflies”, dated July 25, 2017, available at usbs.bcaresearch.com US Bond Strategy Special Report, “More Bullets, Barbells And Butterflies”, dated May 15, 2018, available at usbs.bcaresearch.com Table 4 shows the raw residuals from each model. A positive value indicates that the bullet is cheap relative to the duration-matched barbell. A negative value indicates that the barbell is cheap relative to the bullet. Table 4Butterfly Strategy Valuation: Raw Residuals In Basis Points (As Of March 31ST, 2021)

It’s A Boom!

It’s A Boom!

Table 5 scales the raw residuals in Table 4 by their historical means and standard deviations. This facilitates comparison between the different butterfly spreads. Table 5Butterfly Strategy Valuation: Standardized Residuals (As Of March 31ST, 2021)

It’s A Boom!

It’s A Boom!

Table 6 flips the models on their heads. It shows the change in the slope between the two barbell maturities that must be realized during the next six months to make returns between the bullet and barbell equal. For example, a reading of 43 bps in the 5 over 2/10 cell means that we would only expect the 5-year to outperform the 2/10 if the 2/10 slope steepens by more than 43 bps during the next six months. Otherwise, we would expect the 2/10 barbell to outperform the 5-year bullet. Table 6Discounted Slope Change During Next 6 Months (BPs)

It’s A Boom!

It’s A Boom!

Appendix B: Excess Return Bond Map The Excess Return Bond Map is used to assess the relative risk/reward trade-off between different sectors of the US bond market. It is a purely computational exercise and does not impose any macroeconomic view. The Map’s vertical axis shows 12-month expected excess returns. These are proxied by each sector’s option-adjusted spread. Sectors plotting further toward the top of the Map have higher expected returns and vice-versa. Our novel risk measure called the “Risk Of Losing 100 bps” is shown on the Map’s horizontal axis. To calculate it, we first compute the spread widening required on a 12-month horizon for each sector to lose 100 bps or more relative to a duration-matched position in Treasury securities. Then, we divide that amount of spread widening by each sector’s historical spread volatility. The end result is the number of standard deviations of 12-month spread widening required for each sector to lose 100 bps or more versus a position in Treasuries. Lower risk sectors plot further to the right of the Map, and higher risk sectors plot further to the left. Chart 11Excess Return Bond Map (As Of March 31st, 2021)

It’s A Boom!

It’s A Boom!

Footnotes 1 For a look at alternatives to investment grade corporates please see US Bond Strategy Weekly Report, “Searching For Value In Spread Product”, dated January 26, 2021, available at usbs.bcaresearch.com 2 Please see US Bond Strategy Weekly Report, “That Uneasy Feeling”, dated March 30, 2021, available at usbs.bcaresearch.com 3 Please see US Bond Strategy Weekly Report, “Searching For Value In Spread Product”, dated January 26, 2021, available at usbs.bcaresearch.com 4 Please see US Bond Strategy Weekly Report, “The Fed Looks Backward While Markets Look Forward”, dated March 23, 2021, available at usbs.bcaresearch.com Ryan Swift US Bond Strategist rswift@bcaresearch.com Fixed Income Sector Performance

The BCA Research Global Asset Allocation (GAA) Forum will take place online on May 18th. We have put together a great lineup of speakers to discuss issues of importance to CIOs and asset allocators. These include the latest thinking on portfolio construction, factor investing, alternatives, and ESG. Our keynote speaker will be Keith Ambachtsheer, founder of KPA Advisory and author of many books on investment management including "The Future of Pension Management: Integrating Design, Governance and Investing" (2016). His presentation will be followed by a panel discussion of top CIOs including Maxime Aucoin of CDPQ, James Davis of OPTrust, and Catherine Ulozas of the Drexel University Endowment. The event is complimentary for all GAA subscribers, who can see a full agenda and register here. Others can sign up here. We hope you can join us on May 18th for what should be a stimulating and informative day of ideas and discussion. Highlights Recommended Allocation

Quarterly Portfolio Outlook: What Higher Rates Mean For Asset Allocation

Quarterly Portfolio Outlook: What Higher Rates Mean For Asset Allocation

Global growth will rebound later this year, fueled by an end of lockdowns and generous fiscal stimulus. Despite that, central banks will not move towards tightening until 2023 at the earliest. This remains a very positive environment for risk assets like equities, though the upside is inevitably limited given stretched valuations. We continue to recommend a risk-on position, with overweights in equities and higher-risk corporate bonds. It is unlikely that long-term rates will rise much further over the coming months. But there is a risk that they could, and so we become more wary on interest-sensitive assets. Accordingly, we cut our overweight on the IT sector to neutral, and go overweight Financials. We continue to prefer cyclical sectors, and stay overweight Industrials and Energy. Chinese growth is slowing and so we cut our recommendation on Chinese equities to underweight. Some Emerging Markets will suffer from tighter US financial conditions, so we would be selective in our positions in both EM equity and debt. We stay firmly underweight government bonds, and recommend an underweight on duration, and favor linkers. Within alternatives, we raise Private Equity to overweight. The return to normality will give PE funds a wider range of opportunities, and allow them to pick up distressed assets at attractive valuations. Overview What Higher Rates Mean For Asset Allocation The past few months have seen a sharp rise in long-term interest rates everywhere (Chart 1). These have reflected better growth prospects, but also a greater appreciation of the risk of inflation over the next few years (Chart 2). Our main message in this Quarterly Portfolio Outlook is that we do not expect long-term rates to rise much further over the coming months, but that there is a risk that they could. This would be unlikely to undermine the positive case for risk assets overall, but it would affect asset allocation towards interest-rate sensitive assets such as growth stocks and Emerging Markets, and could have an impact on the US dollar. Chart 1Rates Are Rising Everywhere

Rates Are Rising Everywhere

Rates Are Rising Everywhere

Chart 2...Because Of Both Growth And Inflation Expectations

Quarterly Portfolio Outlook: What Higher Rates Mean For Asset Allocation

Quarterly Portfolio Outlook: What Higher Rates Mean For Asset Allocation

We accordingly keep our recommendation for an overweight on equities and riskier corporate credit on the 12-month investment horizon, but are tweaking some of our other allocation recommendations. The macro environment for the rest of the year continues to look favorable. Pent-up consumer demand will be released once lockdowns end. In the US, this should be mid-July by when, at the current rate, the US will have vaccinated enough people to achieve herd immunity (Chart 3). Excess household savings in the major developed economies have reached almost $3 trillion (Chart 4). At least a part of that will be spent when consumers can go out for entertainment and travel again. Chart 3US On Track To Hit Herd Immunity By July

US On Track To Hit Herd Immunity By July

US On Track To Hit Herd Immunity By July

Chart 4Global Excess Savings Total Trillion

Global Excess Savings Total $3 Trillion

Global Excess Savings Total $3 Trillion

Fiscal stimulus remains generous, especially in the US after the passing of the $1.9 trillion package in March (with another $2 trillion dedicated towards infrastructure spending likely to be approved within the next six months). The OECD estimates that the recent US stimulus alone will boost US GDP growth by almost 3 percentage points in the first full year and have a significant knock-on effect on other economies (Chart 5). Central banks, too, remain wary of the uneven and fragile nature of the recovery and so will not move towards tightening in the next 12 months. The Fed is not signalling a rate hike before 2024 – and it is likely to be the first major central bank to raise rates. In this environment, it is not surprising that long-term rates have risen. We showed in March’s Monthly Portfolio Update that, since 1990, equities have almost always performed strongly when rates are rising. This is likely to continue unless there is either (1) an inflation scare, or (2) the Fed turns more hawkish than the market believes is appropriate. Inflation could spike temporarily over the coming months, which might spook markets (see What Our Clients Are Asking on page 9 for more discussion of this). But sustained inflation is improbable until the labor market recovers to a level where significant wage increases come through (Chart 6). This is unlikely before 2023 at the earliest. Chart 5US Fiscal Stimulus Will Help Everyone

Quarterly Portfolio Outlook: What Higher Rates Mean For Asset Allocation

Quarterly Portfolio Outlook: What Higher Rates Mean For Asset Allocation

Chart 6Labor Market Still Well Away From Full Employment

Labor Market Still Well Away From Full Employment

Labor Market Still Well Away From Full Employment

BCA Research’s fixed-income strategists do not see the US 10-year Treasury yield rising much above 1.8% this year.1 Inflation expectations should settle down around the current level (shown in Chart 2, panel 2) which is consistent with the Fed achieving its 2% PCE inflation target on average over the cycle. Treasury yields are largely driven by whether the Fed turns out to be more or less hawkish than the market expects (Chart 7). The market is already pricing in the first Fed rate hike in Q3 2022 (Chart 8). We think it unlikely that the market will start to price in an earlier hike than that. Chart 7The Fed Unlikely To Hike Ahead Of What Market Expects...

The Fed Unlikely To Hike Ahead Of What Market Expects...

The Fed Unlikely To Hike Ahead Of What Market Expects...

Chart 8...Since This Is As Early As Q3 2022

...Since This Is As Early As Q3 2021

...Since This Is As Early As Q3 2021

How much would a further rise in rates hurt the economy and stock market? Rates are still well below a level that would trigger problems. First, long-term rates are considerably below trend nominal GDP growth, which is around 3.5% (Chart 9). Second, short-term real rates are well below r* – hard though that is to measure at the moment given the volatility of the economy in the past 12 months (Chart 10). Finally, one of the best indicators of economic pressure is a decline in cyclical sectors (consumer spending on durables, corporate capex, and residential investment) as a percentage of GDP (Chart 11). This is because these are the most interest-rate sensitive parts of the economy. But, at the moment, consumers are so cashed up they do not need to borrow to spend. The same is true of corporates, which raised huge amounts of cash last year. The only potential problem is real estate, buoyed last year by low rates which are now reversing (Chart 12). But mortgage rates are still very low and this is not a big enough sector to derail the broader economy. Chart 9Long-Term Rates Well Below Damaging Levels...

Long-Term Rates Well Below Damaging Levels...

Long-Term Rates Well Below Damaging Levels...

Chart 10...Such As The R-Star

Fed Still Below Neutral ...Such As The R-Star

Fed Still Below Neutral ...Such As The R-Star

Chart 11Interest-Rate Sensitive Sectors Are Robust...

Interest-Rate Sensitive Sectors Are Robust...

Interest-Rate Sensitive Sectors Are Robust...

Chart 12...With The Possible Exception Of Housing

...With The Possible Exception Of Housing

...With The Possible Exception Of Housing

Chart 13Debt Levels Are High In Emerging Markets...

Debt Levels Are High In Emerging Markets...

Debt Levels Are High In Emerging Markets...

Chart 14...Which Makes Them Vulnerable To Tightening Financial Conditions

...Which Makes Them Vulnerable To Tightening Financial Conditions

...Which Makes Them Vulnerable To Tightening Financial Conditions

This sanguine view may not apply to Emerging Markets, however. Given the amount of foreign-currency debt they have built up in the past decade (Chart 13), they are very sensitive to US financial conditions, particularly a rise in rates and an appreciation of the US dollar (Chart 14). Accordingly, we have become more cautious on the outlook for both EM equity and debt over the next 6-12 months. Garry Evans, Senior Vice President Chief Global Asset Allocation Strategist garry@bcaresearch.com What Our Clients Are Asking What will happen to inflation? How can we tell if it is trending up? Chart 15Watch The Trimmed Mean Inflation Measure

Watch The Trimmed Mean Inflation Measure

Watch The Trimmed Mean Inflation Measure

How much inflation rises will be a key driver of asset performance over the next 12-18 months. Too much inflation will push up long-term rates and undermine the case for risk assets. But the picture is likely to be complicated. US inflation will rise sharply in year-on-year terms in March and April because of the base effect (comparison with the worst period of the pandemic in 2020), pricier gasoline, rising import prices due to the weaker dollar, and supply-chain bottlenecks that are pushing up manufacturing costs. Core PCE inflation could get close to 2.5% year-on-year (Chart 15, panel 1). In the second half, too, an end to lockdowns could push up service-sector inflation – which has unsurprisingly been weak in the past nine months – as consumers rush out to restaurants and on vacation (panel 3). The Fed has signalled that it will view these as temporary effects. But they may spook the market for a while. Next year, however, it would be surprising to see strong underlying inflation unless employment makes a miraculous recovery. Payrolls would have to increase by 420,000 a month to get back to “maximum employment” by end-2022.2 Absent that, wage growth is likely to stay muted. Conventional inflation gauges may not be very useful at indicating underlying inflation pressures, in a world where consumers switch their spending depending on what is currently allowed under pandemic regulations. The Dallas Fed’s Trimmed Mean Inflation indicator (which excludes the 31% of the 178 items in the consumer basket with the highest price rises each month, and the 24% with the lowest) may be the best true measure. Research shows that historically it has been closer to trend headline PCE inflation in the long run than the core inflation measure, and predicts future inflation better (panel 4). Currently it is at 1.6% year-on-year and trending down. Investors should focus on this measure to see whether rising inflation is becoming a risk. How can investors best protect against rising inflation? In May 2019 we released a report describing how to best to hedge against inflation.3 In that report, we analyzed every period of rising inflation dating back to the 1970s. Our conclusions were the following: The level of inflation will determine how rising inflation affects assets. When inflation goes from 1% to 2%, the macro environment is entirely different from when it goes from 5% to 6%. Thus, inflation hedging should not be thought of as a static exercise but a dynamic one (Table 1). Table 1Winners During Different Inflationary Regimes

Quarterly Portfolio Outlook: What Higher Rates Mean For Asset Allocation

Quarterly Portfolio Outlook: What Higher Rates Mean For Asset Allocation

As long as the annual inflation rate is below about 3%, equities tend to be the best performing asset during high inflation periods, surpassing even commodities. This is because monetary policy tends to stay accommodative and cost pressures remain benign for most companies. However, as inflation passes this threshold, things start to change. Central banks start to become restrictive as they seek to curb inflation. This rise in policy rates starts to choke off the bull market. Meanwhile cost pressures become more significant and, as a result, equities begin to suffer. It is at this time when commodities – particularly oil and industrial metals – and US TIPS become a much better asset to hold. Finally, if the central bank fails to quash inflation, inflation expectations become unanchored, creating a toxic cocktail of rising prices and poor growth. During such periods, the best strategy is to hold the most defensive securities in each asset class, such as Health Care or Utilities within the equity market, or gold within commodities. Can the shift to renewables drive a new commodities supercycle? Chart 16The Shift To Renewables Is Likely To Be A Tailwind For Metal Prices...

The Shift To Renewables Is Likely To Be A Tailwind For Metal Prices...

The Shift To Renewables Is Likely To Be A Tailwind For Metal Prices...

The rise in commodity prices in H2 2020 has made investors ask whether we are on the verge of a new commodities “supercycle” (Chart 16). Our Commodity & Energy strategists argue that the fundamental drivers of each commodities segment differ. Here we focus on industrial metals – particularly those pertaining to renewable energy and transport electrification. Prices of metals used in electric vehicles (EVs) have risen by an average 53% since July 2020, reflecting strong demand that is outstripping supply (Chart 16). In the short-term, metals markets are likely to be in deficit, especially as demand recovers after the pandemic. Modelling longer-term demand is tricky since it relies on assumptions for the emergence of new technologies, metals’ efficiency, recycling rates, and the share of renewables. A study by the Institute for Sustainable Futures showed that, in the most positive scenarios, demand for some metals will exceed available resources and reserves (Table 2).4 The most pessimistic scenarios – which, for example, assume no major electrification of the transport system – show demand at approximately half of available resources. It is likely that demand will lay somewhere between those scenarios. Table 2...As Future Demand Exceeds Supply

Quarterly Portfolio Outlook: What Higher Rates Mean For Asset Allocation

Quarterly Portfolio Outlook: What Higher Rates Mean For Asset Allocation

Supply is concentrated in a handful of countries: For example, the DR Congo is responsible for more than 65% of cobalt production and 50% of the world’s reserves;5 Australia supplies almost 50% of the world’s lithium and has 22% of its reserves.6 Production bottlenecks could therefore put significant upside pressures on prices. Factoring in supply/demand dynamics, as well as an assessment of future technological advancements, we conclude that industrial metals might be posed for a bull market over the upcoming years. How can we add alpha in the bond bear market? Chart 17Government Bond Yield Sensitivities To USTs

Government Bond Yield Sensitivities To USTs

Government Bond Yield Sensitivities To USTs

For a portfolio benchmarked to the global Treasury index, one way to add alpha is through country allocation. BCA’s Fixed Income Strategy recommends overweighting low yield-beta countries (Germany, France, and Japan) and underweighting high yield-beta countries (Canada, Australia, and the UK).7 The yield beta is defined as the sensitivity of a country’s yield change to changes in the US 10-year Treasury yield, as shown in Chart 17. BCA’s view is that the Fed will be the first major central bank to lift interest rate, therefore investors' underweights should be concentrated in the US Treasury index. It’s worth noting, however, that yield beta is influenced by many factors, and can change over time. When applying this approach, it’s important to pay attention to key factors in each country, especially those that are critical to central bank policy decisions (Table 3). Table 3A Watch List For Bond Investors

Quarterly Portfolio Outlook: What Higher Rates Mean For Asset Allocation

Quarterly Portfolio Outlook: What Higher Rates Mean For Asset Allocation

Global Economy Chart 18US Growth Already Looks Strong...

US Growth Already Looks Strong...

US Growth Already Looks Strong...

Overview: Growth continues to recover from the pandemic, although the pace varies. Manufacturing has rebounded strongly, as consumers spend their fiscal handouts on computer and household equipment, but services remain very weak, especially in Europe and Japan. Successful vaccination programs and the end of lockdowns in many countries should lead to strong growth in H2, as consumers spend their accumulated savings and companies increase capex to meet this demand. Perhaps the biggest risk to growth is premature tightening in China, but the authorities there are very aware of this risk and so it is unlikely to drag much on global growth. US: Although the big upside surprises to economic growth are over (Chart 18, panel 1), the US continues to expand more strongly than other major economies, due to its relatively limited lockdowns and large fiscal stimulus (which last year and this combined reached 25% of GDP, with another $2 trillion package in the works). Fed NowCasts suggest that Q1 GDP will come in at around 5-6% quarter-on-quarter annualized, with the OECD’s full-year GDP growth forecast as high as 6.5%. Nonetheless, there is still some way to go: Consumer expenditure and capex remain weak by historical standards, and new jobless claims in March still averaged 727,000 a week. Euro Area: More stringent pandemic regulations and slow vaccine rollout mean that the European service sector has been slow to recover. The services PMI in March was still only 48.4, though manufacturing has rebounded strongly to 64.2 (Chart 19, panel 1). Fiscal stimulus is also much smaller than in the US, with the EUR750 billion approved in December to be spent mostly on infrastructure over a period of years. Growth should rebound in H2 if lockdowns end and the vaccination program accelerates. But the OECD forecasts full-year GDP growth of only 3.9%. Chart 19...But Chinese Growth Has Probably Peaked

...But Chinese Growth Has Probably Peaked

...But Chinese Growth Has Probably Peaked

Japan has seen the weakest rebound among the major economies, slightly puzzlingly so given its heavy weight in manufacturing and large exposure to the Chinese economy. Industrial production still shrank 3% year-on-year in February (Chart 19, panel 2), exports were down 4.5% YoY in February, and the manufacturing PMI is barely above 50. The main culprit remains domestic consumption, with confidence very weak and wages still declining, leading to a 2.4% YoY decline in retail sales in January. The OECD full-year GDP growth forecast is just 2.4%. Emerging Markets: The Chinese authorities have been moderately tightening policy for six months and this is starting to impact growth. Both the manufacturing and services PMIs have peaked, though they remain above 50 (panel 3). The policy tightening is likely to be only moderate and so growth this year should not slow drastically. Nonetheless, there remains the risk of a policy mistake. Elsewhere, many EM central banks are struggling with the dilemma of whether to cut rates to boost growth, or raise rates to defend a weakening currency. Real policy rates range from over 2% in Indonesia to below -2% in Brazil and the Philippines. This will add to volatility in the EM universe. Interest Rates: Policy rates in developed economies will not rise any time soon. The Fed is signalling no rise until 2024 (although the futures are now pricing in the first hike in Q3 2022). Other major central banks are likely to wait even longer. A crucial question is whether long-term rates will rise further, after the jump in the US 10-year Treasury yield to a high of 1.73%, from 0.92% at the start of the year. We see only limited upside in yields over the next nine months, as underlying inflation pressures should remain weak and central banks will remain highly reluctant to bring forward the pace of monetary policy normalization. Global Equities Chart 20Has The Equity Market Priced In All The Earnings Growth?

Has The Equity Market Priced In All The Earnings Growth?

Has The Equity Market Priced In All The Earnings Growth?

The global equities index eked out a 4% gain in Q1 2021, completely driven by a rebound in the profit outlook, since the forward PE multiple slightly contracted by 4%. Forward EPS has now recovered to the pre-pandemic level, while both the index level and PE multiple are 52% and 43% higher than at the end of March 2020 (Chart 20). While BCA’s global earnings model points to nearly 20% earnings growth over the next 12 months and analysts are still revising up earnings forecasts, the key question in our mind is whether the equity market has priced in all the earnings growth. Equity valuations are still not cheap by historical standards despite the small contraction in PEs in Q1. In addition, the VIX index has come down to 19.6, right at its historical average since January 1990, and profit margins in both EM and DM have come under pressure. As an asset class, however, stocks are still attractively valued compared to bonds (panel 5). Given our long-held approach of taking risk where risk will most likely be rewarded, we remain overweight equities versus bonds at the asset-class level, but we are taking some risk off the table in our country and sector allocations by downgrading China to underweight (from overweight) and upgrading the UK to overweight (from neutral), and by taking profits in our Tech overweight and upgrading Financials to overweight (see next two pages). To sum up, we are overweight the US and UK, underweight Japan, the euro area, and China, while neutral on Canada, Australia, and non-China EM. Sector-wise, we are overweight Industrials, Financials, Energy, and Health Care; underweight Consumer Staples, Utilities, and Real Estate; and neutral on Tech, Consumer Discretionary, Communication Services, and Materials. Country Allocation: Downgrade China To Underweight From Overweight Chart 21China Is Risking Overtightening

China Is Risking Overtightening

China Is Risking Overtightening

We started to separate the overall EM into China and Other EM in the January Monthly Portfolio Update this year. We initiated China with an Overweight and “Other EM” with a Neutral weighting in the global equity portfolio. The key rationale was that Chinese growth would remain strong in H1 2021 due to its earlier stimulus, while some EM countries would benefit from Chinese growth but others were still suffering from structural issues. In Q1, China underperformed the global benchmark by 4.5%, while the other EM markets underperformed slightly. China’s National People’s Congress (NPC) indicated that Chinese policymakers will gradually pull back policy support this year. BCA’s China Investment Strategists think that fiscal thrust will be neutral in 2021 while credit expansion will be at a lower rate compared to 2020. The Chinese economy should remain strong in H1 but will slow to a benign and managed growth rate afterwards. Therefore, the risk of policy overtightening is not trivial and could threaten China’s economic growth and corporate profit outlook. The outperformance of Chinese stocks since the end of 2019 has been largely driven by multiple expansion (Chart 21, panel 1), but the slowdown in the credit impulse implies that the recent underperformance of Chinese equities has not run its course because multiple contraction will likely have to catch up and will therefore put more downward pressure on price (panels 2 and 3). We remain neutral on the non-China EM countries, implying an underweight for the overall EM universe. We use the proceeds to fund an upgrade of the UK to Overweight from Neutral because the UK index is comprised largely of globally exposed companies and because we have upgraded GBP to overweight (see page 21). Sector Allocation: Upgrade Financials To Overweight By Downgrading Tech To Neutral Chart 22Financials And Tech: Trading Places

Financials And Tech: Trading Places

Financials And Tech: Trading Places

One year ago, we upgraded Tech to overweight and downgraded Financials to neutral given our views on the impact of the pandemic and interest rates.8 This position has netted out an alpha of 1123 basis points in one year. BCA Research’s House View now calls for somewhat higher global interest rates and steeper yield curves (especially in the US) over the next 9-12 months. Accordingly, we are downgrading Tech to neutral and upgrading Financials to overweight. Financials have outperformed the broad market by about 20% since September 2020 after global yields bottomed in July 2020. We do not expect yields to rise significantly from the current level, nor do we expect Tech earnings growth to slow significantly (Chart 22, panel 5). So why do we make such shift between Financials and Tech? There are three key reasons: First, the Tech sector is a long-duration asset with high sensitivity to changes in the discount rate. In contrast, Financials’ earnings benefit from steepening yield curves. If history is any guide, we should see more aggressive analyst earnings revisions going forward in favor of Financials (Chart 22, panel 3). Second, the performance of Financials relative to Tech has been on a long-term structural downtrend since the Global Financial Crisis. A countertrend rebound to the neutral zone from the currently very oversold level would imply further upside (Chart 22, panel 1). Last, Financials are trading at an extremely large discount to the Tech sector (Chart 22, panel 2). In an environment where overall equity valuations are stretched by historical standards, it is prudent to rotate into an extremely cheap sector from an extremely expensive sector. Government Bonds Chart 23Policy Mix Is Bond-Bearish

Policy Mix Is Bond-Bearish

Policy Mix Is Bond-Bearish

Maintain Below-Benchmark Duration. Global bond yields have climbed sharply in Q1, supported by strong economic growth, mostly smooth rollout of vaccination and the Biden Administration’s very stimulative fiscal package of USD1.9 trillion. The US stimulus package changes the trajectory of the 2021 US fiscal impulse from a $0.8 trillion contraction to a $0.3 trillion expansion, according to estimates from the US Committee for a Responsible Federal Budget. Going forward, the path of least resistance for global yields is still up, though the upside will be limited given the resolve of central banks to maintain accommodative monetary policies (Chart 23). Chart 24Stay Long TIPS

Stay Long TIPS

Stay Long TIPS

Still Favor Linkers Vs. Nominal Bonds. Our overweight position in inflation-linked bonds relative to nominal bonds has panned out well so far this year, as has our positioning for a flattening inflation-protection curve. Even though inflation expectations have run up quickly, the 5 year-5 year forward inflation breakeven rate is still below 2.3-2.5%, the range that is consistent with core PCE reaching the Fed’s 2% target in a sustainable fashion (Chart 24). The US TIPS 5/10-year curve is inverted already, but our fixed income strategists are still reluctant to exit the curve-flattening position for two key reasons: 1) The Fed has indicated that it will tolerate core PCE overshooting the 2% target because it will try to hit the target from above rather than from below; and 2) the short end of the inflation expectation curve is more sensitive to actual inflation than the long end. There are signs (core producer prices, prices paid in the ISM manufacturing survey, and NFIB reported prices are all rising) that core PCE will reach 2% in the next 12 months. Corporate Bonds Chart 25High-Yield Offers Best Value In Fixed Income

Quarterly Portfolio Outlook: What Higher Rates Mean For Asset Allocation

Quarterly Portfolio Outlook: What Higher Rates Mean For Asset Allocation

Since the beginning of the year, investment-grade bonds have outperformed duration-matched Treasurys by 62 basis points, while high-yield bonds have outperformed duration-marched Treasurys by 232 basis points. In the current reflationary environment, we believe that the best strategy within fixed-income portfolios is to overweight low-duration assets and maximize credit exposure where the spread makes a large portion of the yield. Thus, we remain overweight high-yield bonds. We believe that high yield offers much better value than higher quality credits. Currently spreads for high-yield bonds are in the middle of their historical distribution – a stark contrast from their investment-grade counterparts, which are trading at very expensive levels (Chart 25, panel 1). Moreover, the reopening of the economy should help the more cyclical sectors of the bond market, where the lower credit qualities are concentrated. But could a rise in yields start hurting sub-investment-grade companies and increase their borrowing costs? We do not think this is likely for now. Most of the bonds in the US high-yield index mature in more than three years, which means that high-risk corporates will not have to finance themselves with higher rates yet (Chart 25, panel 2). On the other hand, we remain underweight investment-grade credit. Not only are these bonds expensive, but they offer very little upside in any scenario. On the one hand, these bonds should underperform further if raise continue to rise – a result of their high duration. On the other hand, if a severe recession were to hit, spreads would most likely widen, which will also result in underperformance. Commodities Chart 26Limited Upside For Oil From Here

Limited Upside For Oil From Here

Limited Upside For Oil From Here

Energy (Overweight): Despite the recent mid-March selloff, which was most likely triggered by profit taking, oil prices are still up 25% since the beginning of the year. This happened on the back of the restoration of some economic activity, the OPEC 2.0 coalition maintaining production discipline and therefore keeping supply in check, and the recovery in crude demand drawing down inventory. However, earlier forecasts of the 2021 oil demand recovery were a bit too optimistic amid continuing pandemic uncertainty. There is now, therefore, only limited upside for the oil price, at least this year. Our Commodity & Energy strategists expect the Brent crude price to average $65/bbl this year (Chart 26, panels 1 & 2). Industrial Metals (Neutral): We have previously highlighted that Chinese restocking activity in 2020 was a big factor behind the rally in industrial metals prices. As this eases, and Chinese growth slows, commodity prices might correct somewhat in the short term. However, fundamental changes in demand for alternative energy makes us ask whether we are now entering a new commodities “supercycle” for certain metals (for more analysis of this, see What Our Clients Are Asking on page 11). If history is any guide, however, the commodities bear market may have a little longer to run. Historically, commodity bear cycles lasted 17 years on average and we are only 10 years into this one (panel 3). On balance, therefore, we remain neutral on industrial metals for now. Precious Metals (Neutral): After peaking last August, the gold price has continued to tumble, down almost 19% since and 11% since the beginning of the year. We have been wary of the metal’s lofty valuation – the real price of gold remains near a historical high. The recent rise in real rates put more downside pressure on gold. However, the pullback in prices should provide investors who see gold as a long-term inflation hedge and do not buy the metal with a view to strong absolute performance over the next 12 months, with an attractive entry point. We maintain a slight overweight position to hedge against inflation and unexpected tail risks (panel 4). Currencies US Dollar Chart 27Vaccinations will help USD and GBP in 2021

Vaccinations will help USD and GBP in 2021

Vaccinations will help USD and GBP in 2021

While we still believe that the dollar is in a major bear market, the current environment could see a significant dollar countertrend. Thanks to its gargantuan fiscal stimulus as well as its relatively fast vaccination campaign, the US is likely to grow faster than the rest of the world during 2021 (Chart 27, panel 1). This dynamic should put further upward pressure on US real rates relative to the rest of the world, helping the dollar in the process. To hedge this risk, we are upgrading the US dollar from underweight to neutral in our currency portfolio. Euro The euro should experience a temporary pullback. Economic activity in Europe, particularly in the service sector is lagging the US – a consequence of Europe’s slow vaccination campaign. This sluggishness in economic activity will translate into a worse real rate differential vis-a-vis the US, dragging the euro lower in the process. Thus, we are downgrading the euro from overweight to neutral. British Pound One currency that might perform well in this environment is the British pound. Consumer spending in the UK was particularly hard hit during the pandemic, since such a high share of it is geared towards social activities like restaurants and hotels (Chart 27, panel 2). However, thanks to Britain’s successful vaccination campaign, UK consumption is likely to experience a sharp snapback. As growth expectations improve, real rates should grind higher vis-à-vis the rest of the world, pushing the pound higher. Moreover, valuations for this currency are attractive: The pound currently trades at a 10% discount to purchasing power parity fair value. As a result, we are upgrading the GBP from neutral to overweight. Alternatives Chart 28Turning More Positive On Private Equity

Turning More Positive On Private Equity

Turning More Positive On Private Equity

Return Enhancers: In last October’s Quarterly Outlook, we advised investors to prepare for new opportunities in Private Equity (PE) as fund managers look to deploy record high dry power. A gradual return to normality is likely to provide PE funds with a wider range of opportunities, while still allowing them to pick up distressed assets at attractive valuations. This is illustrated by the annualized quarterly returns of PE funds in Q2 and Q3 2020, which reached 43% and 56% respectively. PE funds raised in recession and early-cycle years tend to have a higher median net IRR than those raised in the latter stages of bull markets. This suggests that returns from the 2020 and 2021 vintages should be strong. In recent years, capital flows have increasingly gone to the longer established and larger funds, which tend to have better access to the most attractive deals and therefore record the strongest returns. This trend is likely to continue. Given the time it takes to shift allocations in private assets, we increase our recommended allocation in PE to overweight. Inflation Hedges: It is not clear that inflation will come roaring back in the next couple of years. But what is certain is that market participants are concerned about this risk, which should give a boost to inflation-hedge assets. Given this backdrop, we continue to favor commodity futures (Chart 28, panel 2). In other circumstances, real estate would also have been a beneficiary in this environment. But the slowdown in commercial real estate, as many corporate tenants review whether they need expensive city-center space, makes us remain cautious on real estate. Volatility Dampeners: We continue to favor farmland and timberland over structured products, particularly mortgage-backed securities (MBS). Farmland offers attractive yields and should continue to provide the best portfolio protection in the event of any market distress (Chart 28, panel 3). Risks To Our View The main risks to our central view are to the downside. Because global equities have risen by 55% over the past 12 months, and with the forward PE of the MSCI ACWI index at 19.5x (Chart 29), the room for price appreciation over the next 12 months is inevitably limited. There are several things that could undermine the economic recovery and equity bull market. The COVID-19 pandemic remains the greatest unknown. The vaccination rollout has been very uneven (Chart 30). New strains, especially the one first identified in Brazil, are highly contagious and people who previously had COVID-19 do not seem to have immunity against them. Behavior once COVID cases decline is also hard to predict. Will people be happy again to fly, attend events in large stadiums, and socialize in crowded bars, or will many remain wary for years? This would undermine the case for a strong rebound in consumption. Chart 29Is Perfection Priced In?

Is Perfection Priced In?

Is Perfection Priced In?

Chart 30Vaccination Has Been Spotty Vaccination Has Been Spotty

Vaccination Has Been Spotty Vaccination Has Been Spotty

Vaccination Has Been Spotty Vaccination Has Been Spotty

Chart 31China Slowing Again?

China Slowing Again?

China Slowing Again?

As often, a slowdown in China is a risk. The authorities there have signalled a pullback in stimulus, and the credit impulse has begun to slow (Chart 31). Our China strategists think the authorities will be careful not to tighten too drastically (with the fiscal thrust expected to be neutral this year), and that growth will slow only to a benign and moderate rate in the second half.9 But there is a lot of room for policy error. Finally, inflation. As we argue elsewhere in this Quarterly, it will inevitably pick up for technical reasons in March and April, and then again in late 2021 as renewed consumer demand for services (especially travel and entertainment) pushes up prices. The Fed has emphasized that these phenomena are temporary and that underlying inflation will not emerge until the economy returns to full employment. But the market might get spooked for a while when inflation jumps, pushing up long-term interest rates and triggering an equity market correction. Footnotes 1 Please see US Bond Strategy Report, “The Fed Looks Backward While Markets Look Forward,” dated March 23, 2021. 2 Please see US Bond Strategy Report, “The Fed Looks Backward While Markets Look Forward,” dated March 23, 2021, 3 Please see Global Asset Allocation Special Report, “Investors’ Guide To Inflation Hedging: How To Invest When Inflation Rises,” dated May 22, 2019. 4 Dominish, E., Florin, N. and Teske, S., 2019, Responsible Minerals Sourcing for Renewable Energy. Report prepared for Earthworks by the Institute for Sustainable Futures, University of Technology Sydney. The optimistic scenario is referred to as “total metals demand” scenario, which assumed current materials intensity and market share continues into the future without recycling or efficiency improvements. This study is based on 2018 production levels and therefore expansion of future production may vary results. 5US Geological Survey, Mineral Commodity Summaries 2021. 6 Chile is estimated to have the largest reserve of lithium. 7 Please see Global Fixed Income Strategy Report, “Harder, Better, Faster, Stronger,” dated March 16, 2021. 8 Please see Global Asset Allocation, “Quarterly Portfolio Outlook: Playing The Optionality,” dated April 1, 2020. 9 Please see China Investment Strategy Report, “National People’s Congress Sets Tone For 2021 Growth,” dated March 17, 2021. GAA Asset Allocation

Highlights Duration: The Treasury market has moved quickly to price-in expectations of a strong economic recovery, while the Fed has been more cautious about moving its own rate forecasts. We think that the market’s expectations are well founded and that the Fed will eventually move its dots higher. Stick with below-benchmark portfolio duration. Corporate Bonds: Junk spreads already embed a significant decline in the default rate during the next 12 months, but reasonable assumptions for corporate debt growth and profit growth suggest that this outcome will be achieved. Investors should continue to favor spread product over Treasuries and continue to hold a down-in-quality bias within corporate credit. Economy: Disposable personal income fell in February compared to January, but it has risen massively since last year’s passage of the CARES act. The large pool of accumulated household savings will help drive economic growth as the pandemic recedes. Feature There is widespread anticipation that the economic recovery is about to kick into high gear. To us, this anticipation seems rather well founded. The United States’ vaccination roll-out is proceeding quickly and the federal government is pitching in with a tsunami of fiscal support. But it’s important to acknowledge that this positive outlook is still a forecast, one that has not yet been validated by hard economic data. The risk for investors is obvious. Market prices have already moved to price-in a significant amount of economic optimism and they are vulnerable in a situation where that optimism doesn’t pan out. In this week’s report we look at how much economic optimism is already discounted in both the Treasury and corporate bond markets. We conclude that the most likely scenario is one where the economic data are strong enough to validate current pricing in both markets. Investors should keep portfolio duration below-benchmark and continue to favor spread product over Treasuries, with a down-in-quality bias. Optimism In The Treasury Market The most obvious way to illustrate the economic optimism currently embedded in Treasury securities is to look at the rate hike expectations priced into the yield curve relative to the Fed’s own projections (Chart 1). The market is currently looking for four 25 basis point rate hikes by the end of 2023 while only seven out of 18 FOMC participants expect any hikes at all by then. Chart 1Market More Hawkish Than Fed

Market More Hawkish Than Fed

Market More Hawkish Than Fed

We addressed the wide divergence between market and FOMC expectations in last week’s report.1 We noted that the main reason for the divergence is that while the market is focused on expectations for rapid economic growth the Fed is making a concerted effort to rely only on hard economic data. This sentiment was echoed by Fed Governor Lael Brainard in a speech last week:2 The focus on achieved outcomes rather than the anticipated outlook is central to the Committee’s guidance regarding both asset purchases and the policy rate. The emphasis on outcomes rather than the outlook corresponds to the shift in our monetary policy approach that suggests policy should be patient rather than preemptive at this stage in the recovery. The upshot of the Fed’s excessively cautious approach is that its interest rate projections will move toward the market’s as the hard economic data strengthen during the next 6-12 months, keeping the bond bear market intact. As evidence for this view, consider that the US Economic Surprise Index remains at an extremely high level, consistent with a rising 10-year Treasury yield (Chart 2). Further, 12-month core inflation rates are poised to jump significantly during the next two months as the weak monthly prints from March and April 2020 fall out of the 12-month sample (Chart 3). Then, pipeline pressures in both the goods and service sectors will ensure that inflation remains relatively high for the balance of the year (Chart 3, bottom panel).3 Chart 2Data Surprises Remain Positive

Data Surprises Remain Positive

Data Surprises Remain Positive

Chart 3Inflation About To Jump

Inflation About To Jump

Inflation About To Jump

Finally, the hard economic data still do not reflect the truly massive amount of fiscal stimulus that is about to hit the US economy. Chart 4 illustrates how large last year’s fiscal stimulus was compared to what was seen during recent recessions, and this chart does not yet incorporate the recently passed $1.9 trillion American Rescue Plan (~8.7% of GDP) or the second infrastructure focused reconciliation bill that is likely to pass this fall. Our political strategists expect 2021’s second budget bill to be similar in size to the American Rescue Plan though tax hikes will also be included and, due to the infrastructure-focused nature of the bill, the spending will be more spread out over a number of years.4 Chart 4The Era Of Big Government Is Back

That Uneasy Feeling

That Uneasy Feeling

Bottom Line: The Treasury market has moved quickly to price-in expectations of a strong economic recovery, while the Fed has been more cautious about moving its own rate forecasts. We think that the market’s expectations are well founded and that the Fed will eventually move its dots higher. Stick with below-benchmark portfolio duration. Optimism In The Corporate Bond Market Chart 5What's Priced In Junk Spreads?

What's Priced In Junk Spreads?

What's Priced In Junk Spreads?

The way we assess the amount of economic optimism baked into the corporate bond market is to calculate the 12-month default rate that is implied by the current High-Yield Index spread (Chart 5). We need to make a few assumptions to do this. First, we assume that investors require an excess spread of at least 100 bps from the index after subtracting 12-month default losses. In past research, we’ve noted that High-Yield has a strong track record of outperforming duration-matched Treasuries when the realized excess spread is above 100 bps. High-Yield underperforms Treasuries more often than it outperforms when the realized excess spread is below 100 bps.5 Second, we must assume a recovery rate for defaulted bonds. The 12-month recovery rate tends to fluctuate between 20% and 60%, with higher levels seen when the default rate is low and lower levels when the default rate is high (Chart 5, bottom panel). For this week’s analysis, we assume a range of recovery rates, from 20% to 50%, though we expect the recovery rate to be closer to the top-end of that range during the next 12 months, given our expectations for a rapid economic recovery. With these assumptions in mind, we calculate that the High-Yield Index is fairly priced for a default rate between 2.8% and 4.5% for the next 12 months (Chart 5, panel 2). If the default rate falls into that range, or below, then we would expect High-Yield bonds (and corporate credit more generally) to outperform a duration-matched position in Treasuries. If the default rate comes in above 4.5%, then we would expect Treasuries to beat High-Yield. To figure out whether the default rate will meet the market’s expectations, we turn to a simple model of the 12-month speculative grade default rate that is based on nonfinancial corporate sector gross leverage (aka total debt over pre-tax profits) and C&I lending standards (Chart 6). If we make forecasts for nonfinancial corporate 12-month debt growth and pre-tax profit growth, we can let the model tell us what default rate to anticipate. Chart 6Default Rate Model

Default Rate Model

Default Rate Model

Debt Growth Expectations We expect corporate debt growth to be quite weak during the next 12 months (Chart 7). This is mainly because firms raised a huge amount of debt last spring when the Fed and federal government made it very attractive to do so. Now, we are emerging from a recession and the nonfinancial corporate sector already holds an elevated cash balance (Chart 7, bottom panel). Debt growth was also essentially zero during the past six months, and very low (or even negative) debt growth is a common occurrence right after a peak in the default rate (Chart 7, top 2 panels). It is true that the nonfinancial corporate sector’s Financing Gap – the difference between capital expenditures and retained earnings – is no longer negative (Chart 7, panel 3). But it is also not high enough to suggest that firms need to significantly add debt. Chart 7Debt Growth Will Be Slow

Debt Growth Will Be Slow

Debt Growth Will Be Slow

For our default rate calculations, we assume that corporate debt growth will be between 0% and 8% during the next 12 months. However, our sense is that it will be closer to 0% than to 8%. Profit Growth Expectations Chart 8Profit Growth Will Surge

Profit Growth Will Surge

Profit Growth Will Surge

Our expectation is that profit growth will surge during the next 12 months, as is the typical pattern when the economy emerges from recession. Year-over-year profit growth peaked at 62% in 2002 following the 2001 recession, and it peaked at 51% in 2010 coming out of the Global Financial Crisis (Chart 8). More specifically, if we model nonfinancial corporate sector pre-tax profit growth on real GDP and then assume 6.5% real GDP growth in 2021, in line with the Fed’s median forecast, then we get a forecast for 31% profit growth in 2021. If we use a higher real GDP growth forecast of 10%, in line with our US Political Strategy service's "maximum impact" scenario, then our model forecasts pre-tax profit growth of 40% for 2021.6 Default Rate Expectations Table 1 puts together different estimates for profit growth and debt growth and maps them to a range of 12-month default rate outcomes, as implied by our Default Rate Model. For example, profit growth of 30% and debt growth between 0% and 8% in 2021 maps to a 12-month default rate of between 3.2% and 3.8%. This falls comfortably within the range of 2.8% to 4.5% that is consistent with current market pricing. Table 1Default Rate Scenarios

That Uneasy Feeling

That Uneasy Feeling

In fact, for our model to output a default rate range that is higher than what is priced into junk spreads, we need to assume 2021 profit growth of 20% or less. This is quite far below the estimates we made above based on reasonable forecasts for real GDP. Bottom Line: Junk spreads already embed a significant decline in the default rate during the next 12 months, but reasonable assumptions for corporate debt growth and profit growth suggest that this outcome will be achieved. Investors should continue to favor spread product over Treasuries and continue to hold a down-in-quality bias within corporate credit. Economy: Household Income Update Last week’s personal income and spending report showed that disposable household income was lower in February than in January, a decline that is entirely attributable to the fact that the $600 checks to individuals that were part of the December stimulus bill were mostly delivered in January. These “Economic Impact Payments” totaled $138 billion in January and only $8 billion in February. This drop-off of $130 billion almost exactly matches the $128 billion monthly decline seen in disposable personal income. Consumer spending also fell in February compared to January, a result that likely owes a lot to February’s bad weather conditions, particularly the winter storm that caused much of Texas to lose power. Though spending has recovered a lot from last year’s lows, it remains significantly below its pre-COVID trend (Chart 9). In contrast to spending, disposable income has skyrocketed since the pandemic started last March. Chart 10 shows that disposable personal income has increased 8% in the 12 months since COVID struck compared to the 12 months prior. Moreover, it shows that the increase is entirely attributable to fiscal relief. Chart 9Households Have Excess ##br##Savings

Households Have Excess Savings

Households Have Excess Savings

Chart 10Disposable Personal Income Growth And Its Drivers

That Uneasy Feeling

That Uneasy Feeling

The result of below-trend spending and a surge in income is a big jump in the savings rate. The personal savings rate was 13.6% in February, well above its average pre-COVID level (Chart 9, panel 3), as it has been since the pandemic began. This consistently elevated savings rate has led to US households building up a $1.9 trillion buffer of excess savings compared to a pre-pandemic baseline (Chart 9, bottom panel). Perhaps the biggest question for economic growth is whether households will deploy this large pool of savings as the economy re-opens or whether they will continue to hoard it. In this regard, the individual checks that were part of last year’s CARES act are the most likely to be hoarded, as these checks were distributed to all Americans making less than $99,000. The income support provisions in this month’s American Rescue Plan are much more targeted. Only individuals making below $75,000 will receive a $1,400 check and the bill also includes expanded unemployment benefits and a large amount of aid for state & local governments. All in all, we anticipate that a substantial amount of household excess savings will be spent once the vaccination effort has made enough progress that people feel safe venturing out. This will lead to strong economic growth and higher inflation in the second half of 2021. Ryan Swift US Bond Strategist rswift@bcaresearch.com Footnotes 1 Please see US Bond Strategy Weekly Report, “The Fed Looks Backward While Markets Look Forward”, dated March 23, 2021, available at usbs.bcaresearch.com 2 https://www.federalreserve.gov/newsevents/speech/brainard20210323b.htm 3 For more details on our outlook for core inflation in 2021 please see US Bond Strategy Weekly Report, “Limit Rate Risk, Load Up On Credit”, dated March 16, 2021, available at usbs.bcaresearch.com 4 Please see US Political Strategy Second Quarter Outlook 2021, “From Stimulus To Structural Reform”, dated March 24, 2021, available at usps.bcaresearch.com 5 For more details on this excess spread analysis please see US Bond Strategy / Global Fixed Income Strategy Special Report, “Trading The US Corporate Bond Market In A Time Of Crisis”, dated March 31, 2020, available at usbs.bcaresearch.com 6 The "maximum impact" scenario assumes that the full amount of authorized outlays from the American Rescue Plan will be spent, with 60% of the outlays spent in FY2021. For more details see US Political Strategy Second Quarter Outlook 2021, “From Stimulus To Structural Reform”, dated March 24, 2021, available at usps.bcaresearch.com Fixed Income Sector Performance Recommended Portfolio Specification

Dear client, Next week, in lieu of our weekly report, I will be hosting a webcast on Thursday, March 25 at 10:00 am EDT and Friday March 26 at 9:00 am HKT. I look forward to your comments and questions during the webcast. Best regards, Chester Highlights During bear markets, counter-trend rallies in the dollar are capped around 4%. This time should be no different. Meanwhile, unless the Fed tightens policy to stem the increase in aggregate demand, inflation will rise and real short rates will drop. The relative equity performance of the US is critical for the dollar. Reserve diversification out of dollars has also started to place a natural ceiling against other developed market currencies. An attractive opportunity is emerging to short the AUD/CAD cross. Feature The 1.7% rise in the US dollar this year is reinvigorating the bull case. When presenting our key views last year, we highlighted that the DXY index was at risk of a 2-4% bounce.1 We reaffirmed this view in our January report: Sizing A Potential Dollar Bounce. At the time, the DXY index was at the 90 level, suggesting the rally should fizzle around 94. Therefore, the key question is whether the nascent rise in the DXY will punch through this level, or fade as we originally expected. The short-term case for the dollar remains bullish. The currency is much oversold. Meanwhile, real interest rates are moving in favor of the US, vis-à-vis a few countries. Third and interrelated, economic momentum in the US is quite strong, compared to other G10 countries. With the rising specter of a market correction, the dollar could also benefit from safe haven flows towards the US. The Federal Reserve’s meeting yesterday certainly reaffirmed that short-term rates will remain anchored near zero, at least until 2023. The Fed does not see inflation much above 2% a couple of years out. Nevertheless, a lot can change in the coming months. Cycles, Positioning And Interest Rates The dollar tends to move in long cycles, with the latest bull and bear markets lasting about a decade or so. In other words, the dollar is a momentum currency. As such, determining which regime you are in is critical to assessing the magnitude of any rally. This is certainly the case when sentiment remains overly dollar bearish, as now. During bear markets, counter-trend rallies in the dollar are capped around 4-6%. This was what happened in the early 2000s. In bull markets, such as after the financial crisis, the dollar achieves escape velocity, with more durable rallies well into the teens (Chart I-1). So far, the current rise still fits within the narrative of a healthy reset in a longer-term bear market. Chart I-1The Dollar Rally Is Still Benign

The Dollar Rally Is Still Benign

The Dollar Rally Is Still Benign

Long interest rates have also been moving in favor of the dollar, especially relative to the euro area, Japan, and even Sweden. Currencies are driven by real interest rate differentials, and higher US yields are bullish. With the Fed giving no indication it will prevent the curve from steepening further, US interest rates could keep gaping higher. However, currencies are about relative rate differentials, and the rise in US interest rates has not been in isolation. Rates in the UK, Australia and New Zealand, countries that have managed the COVID-19 crisis pretty well, are beginning to rise faster than in the US (Chart I-2). Chart I-2A Synchronized Rise In Global Yields

A Synchronized Rise In Global Yields

A Synchronized Rise In Global Yields

US Versus World Growth The rise in US interest rates has been justified by better economic performance. Whether looking at purchasing managers’ indices, economic surprise indices, or even GDP growth expectations, the US has had the upper hand (Chart I-3). The Fed expects US growth to hit 6.5% this year. This is well above what other central banks expect for their domestic economies. The ECB expects 4%, the BoJ expects 3.9%, and the BoC expects 4.6% (Table I-1). Chart I-3AThe US Leads In Growth This Year

The US Leads In Growth This Year

The US Leads In Growth This Year

Chart I-3BThe US Leads In Growth This Year

The US Leads In Growth This Year

The US Leads In Growth This Year

Table I-1The US Leads In Growth And Inflation This Year

Arbitrating Between Dollar Bulls And Bears

Arbitrating Between Dollar Bulls And Bears