Corporate Bonds

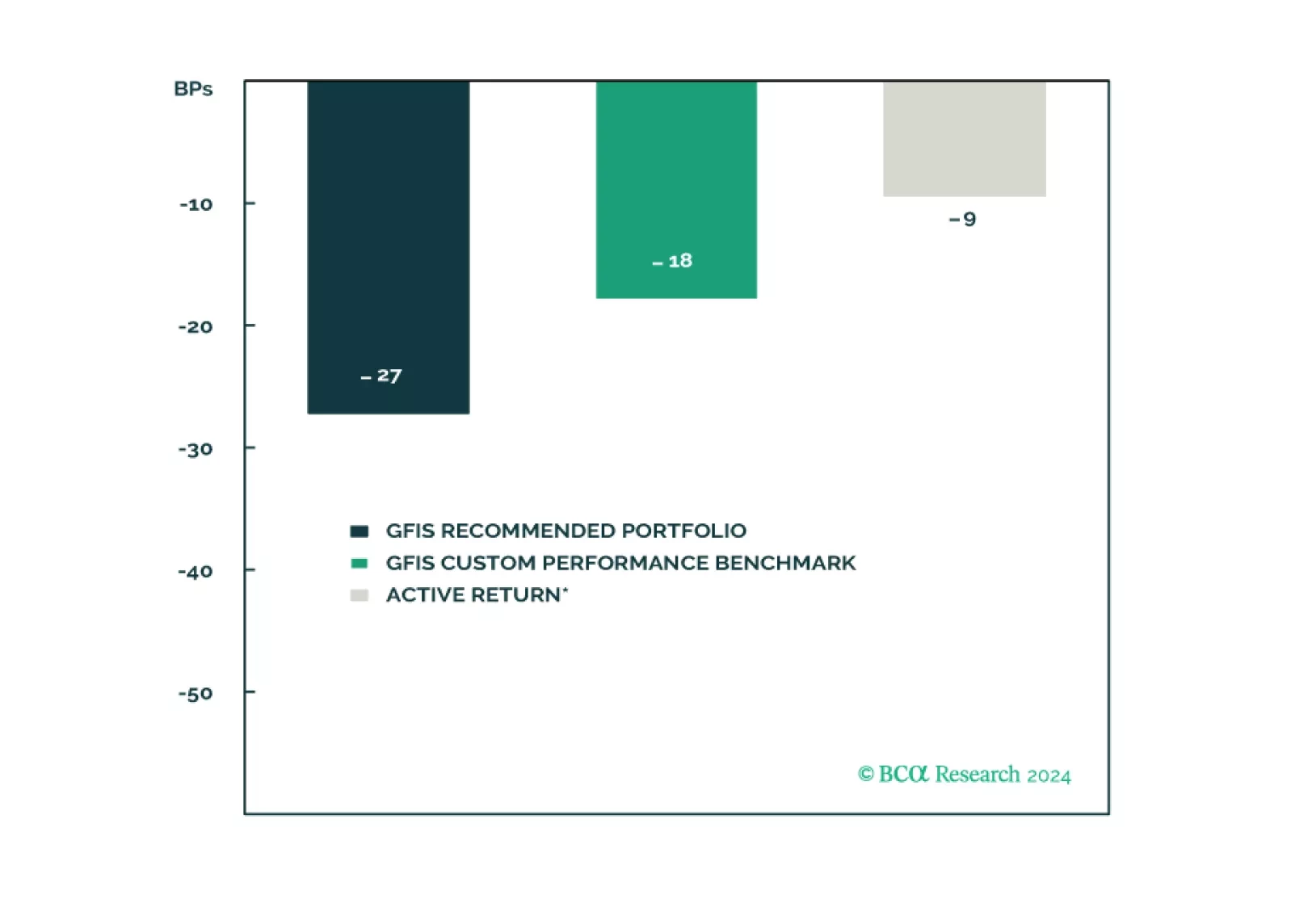

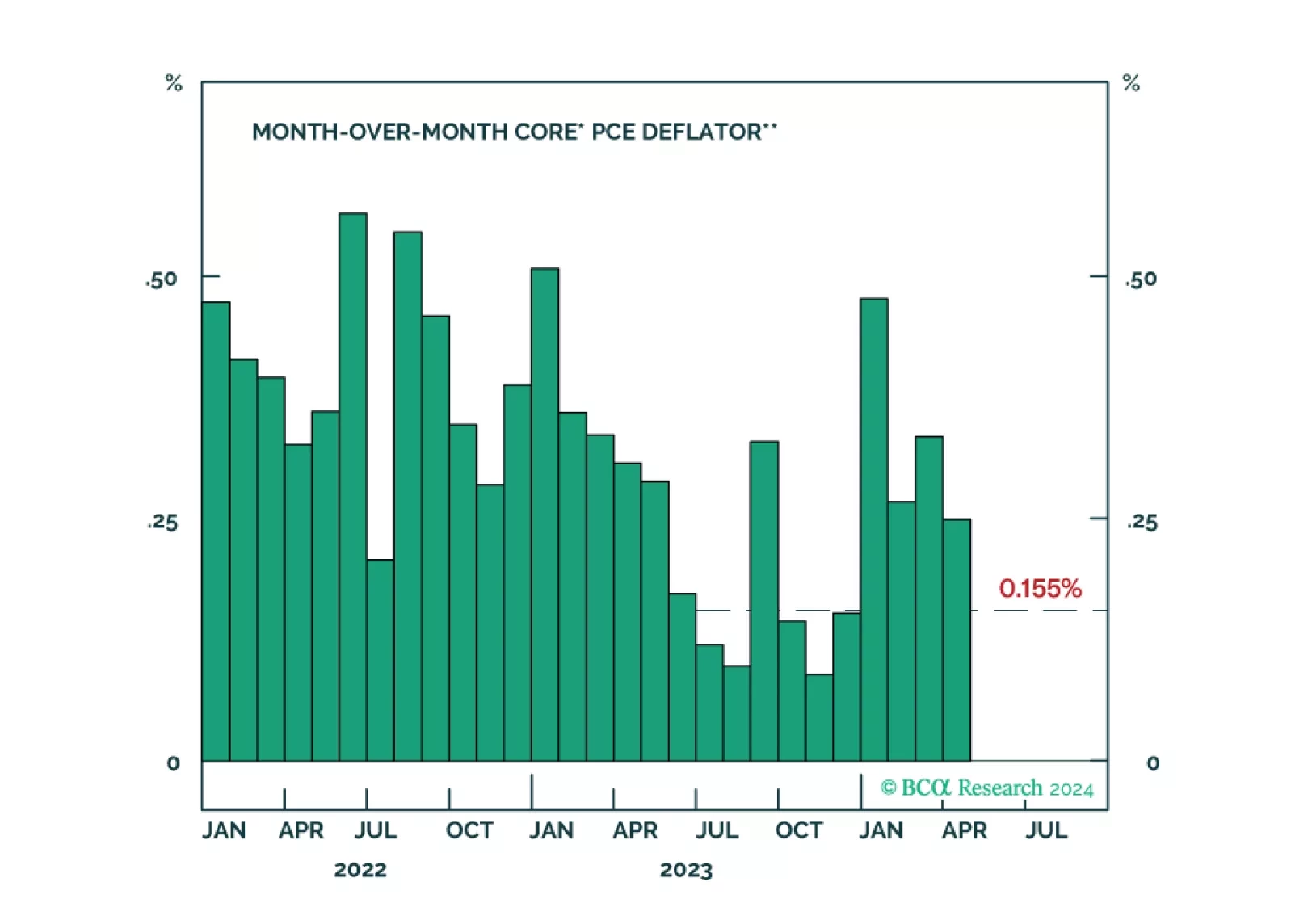

In this report, we present the quarterly review of our Model Bond Portfolio. Rebounding growth and political instability led to slightly negative portfolio performance in Q2/2024. As global growth starts to moderate, we continue to favor government bonds over credit. Maintain a defensive portfolio stance.

Our Portfolio Allocation Summary for July 2024.

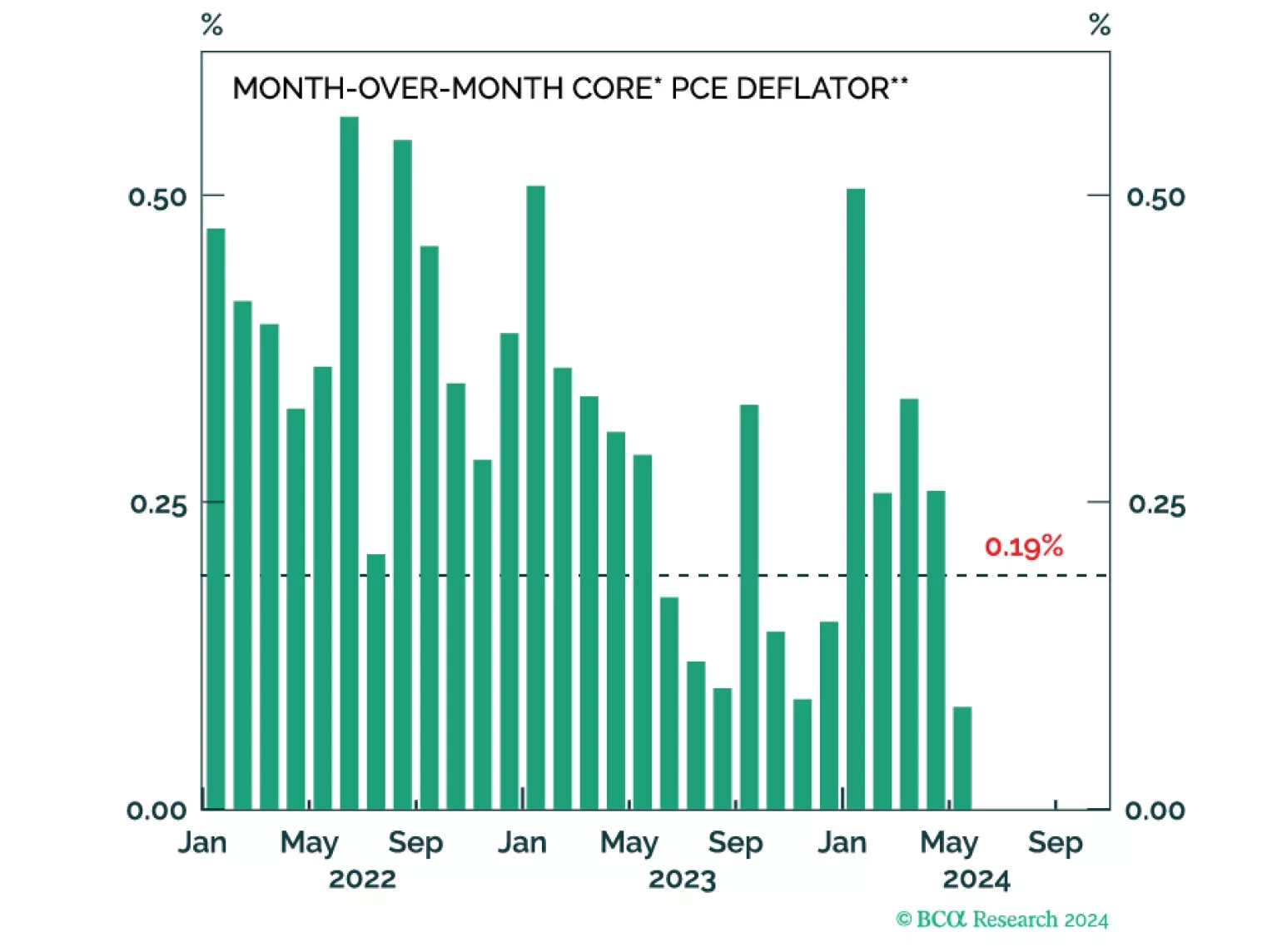

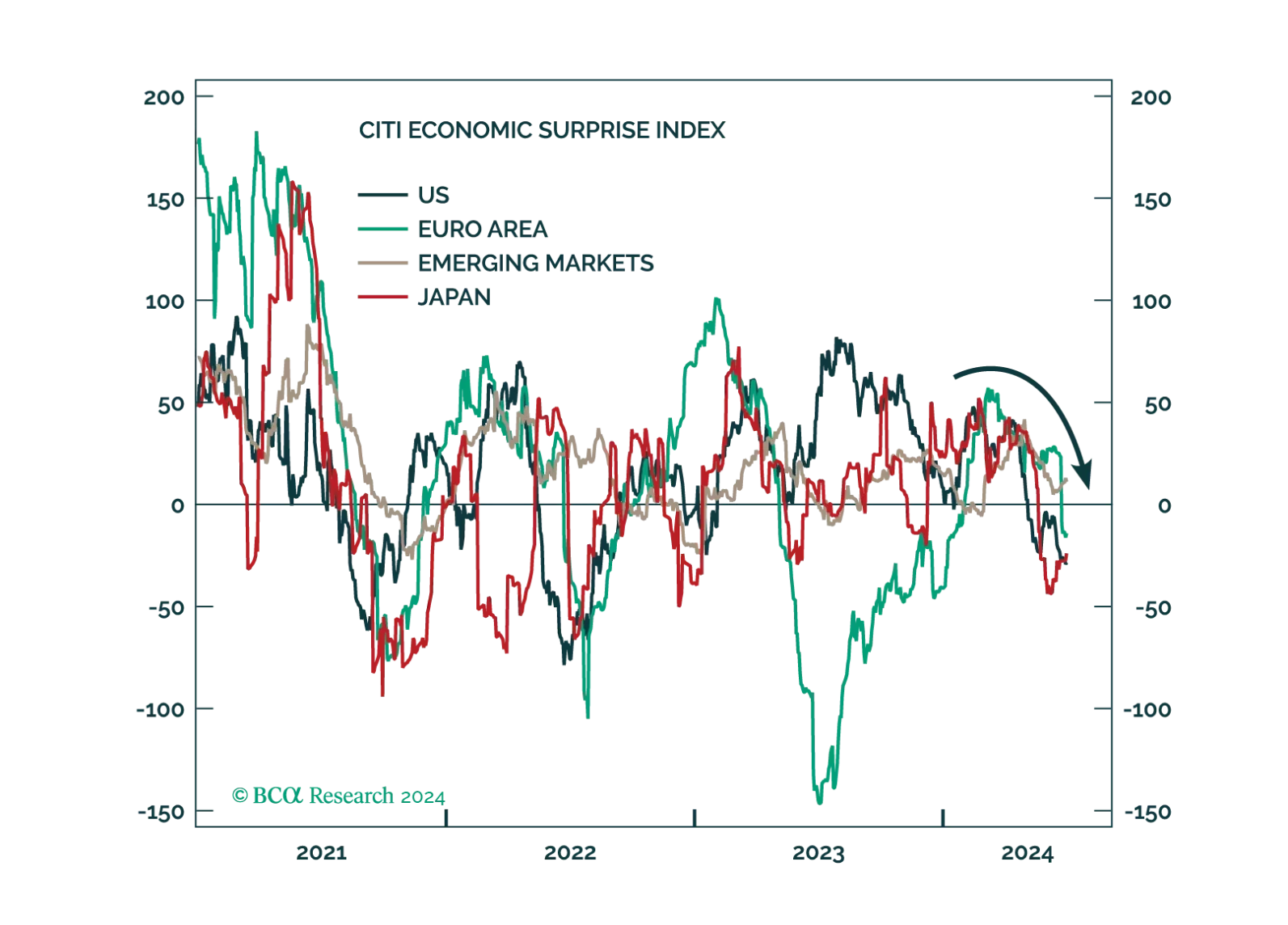

Concerns about the global economy have shifted from sticky inflation to faltering growth. Tight monetary policy is finally starting to bite. We suggest increasing portfolio defensiveness.

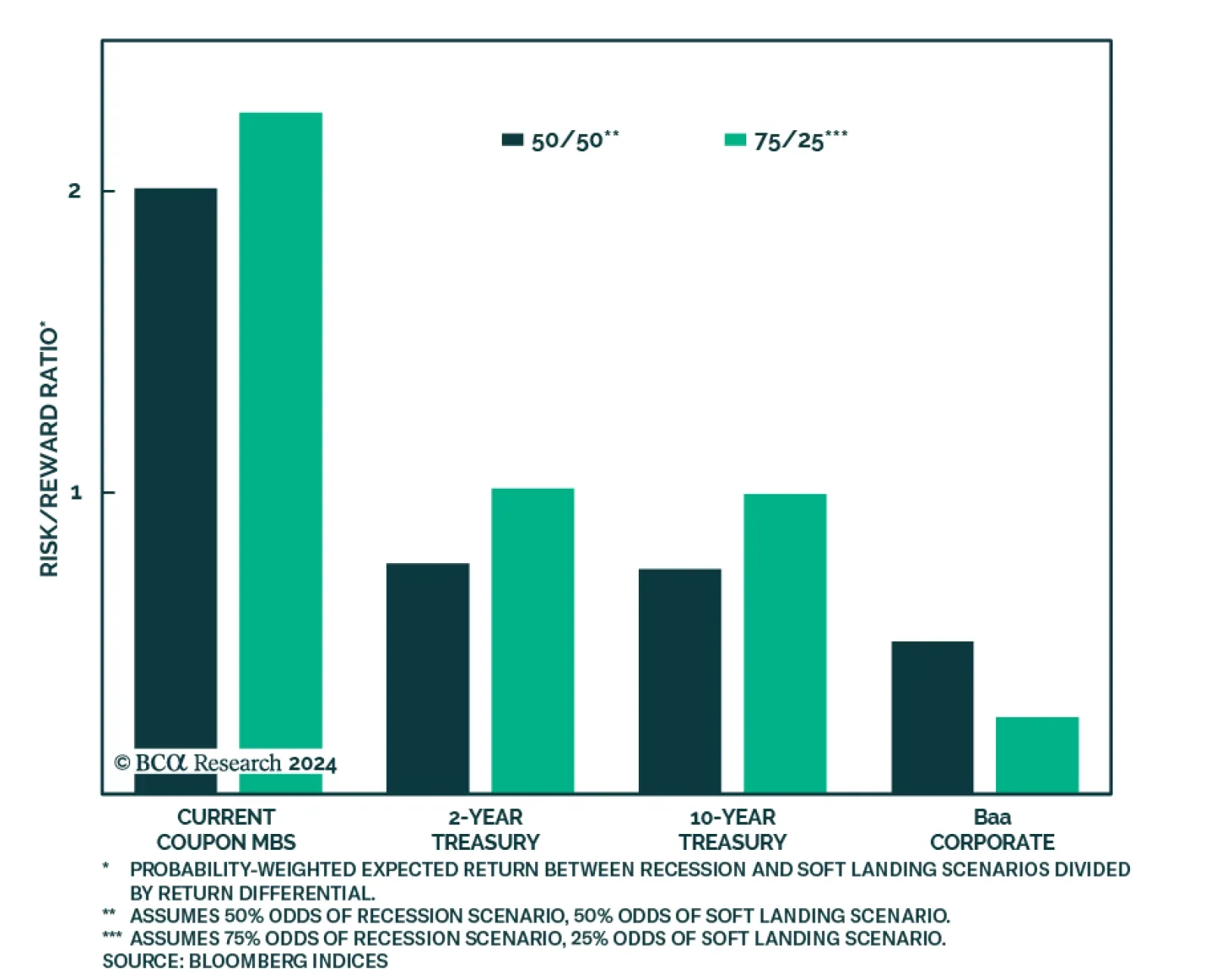

We consider the relative merits of four different fixed income investments in the current economic environment: 2-year Treasuries, 10-year Treasuries, Baa-rated corporate bonds and current coupon Agency MBS.

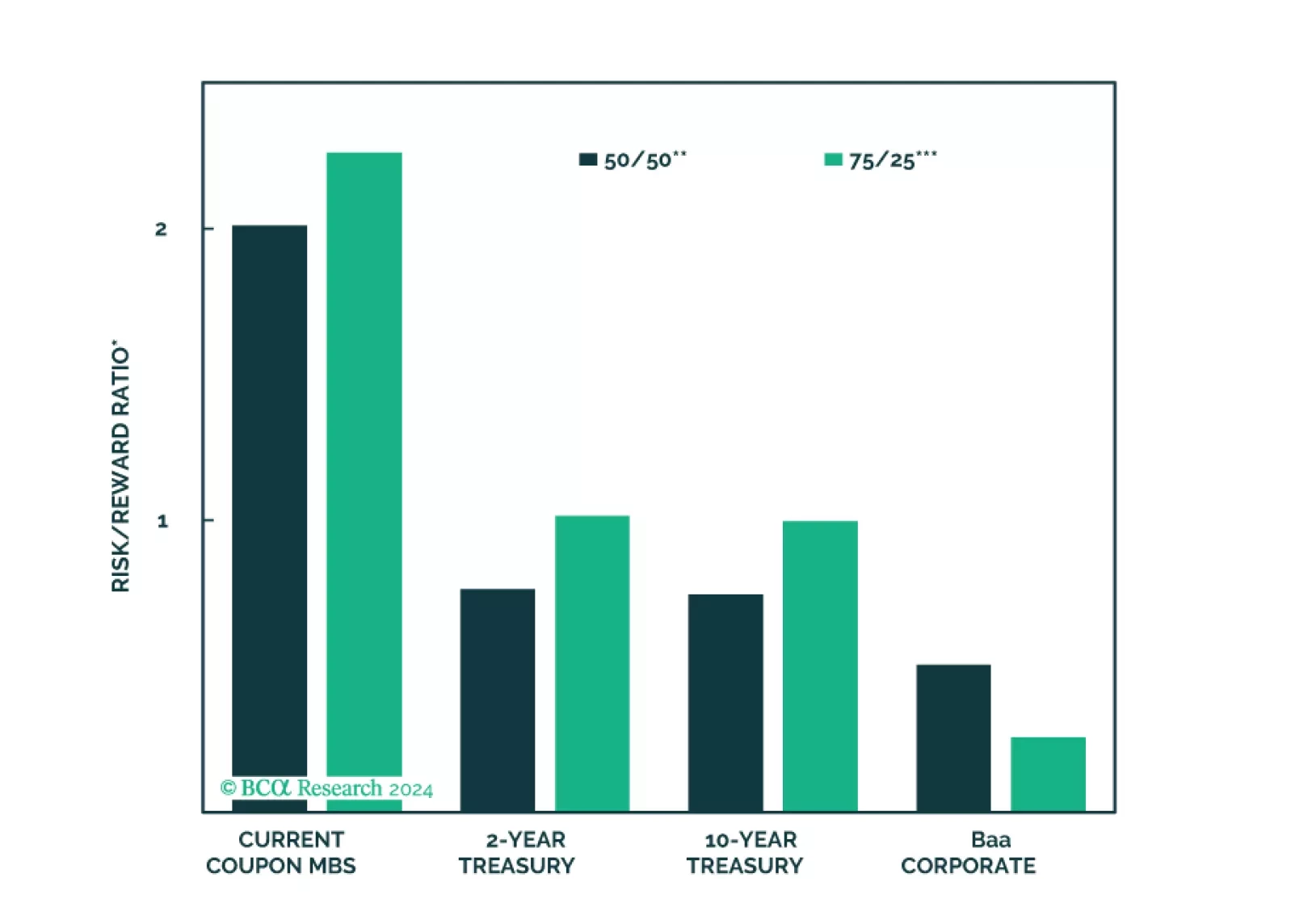

The ECB is now firmly in easing mode, even if it refuses to pre-commit to a specific rate path. What does this data dependency mean for the euro and European yields?

Our Portfolio Allocation Summary for June 2024.

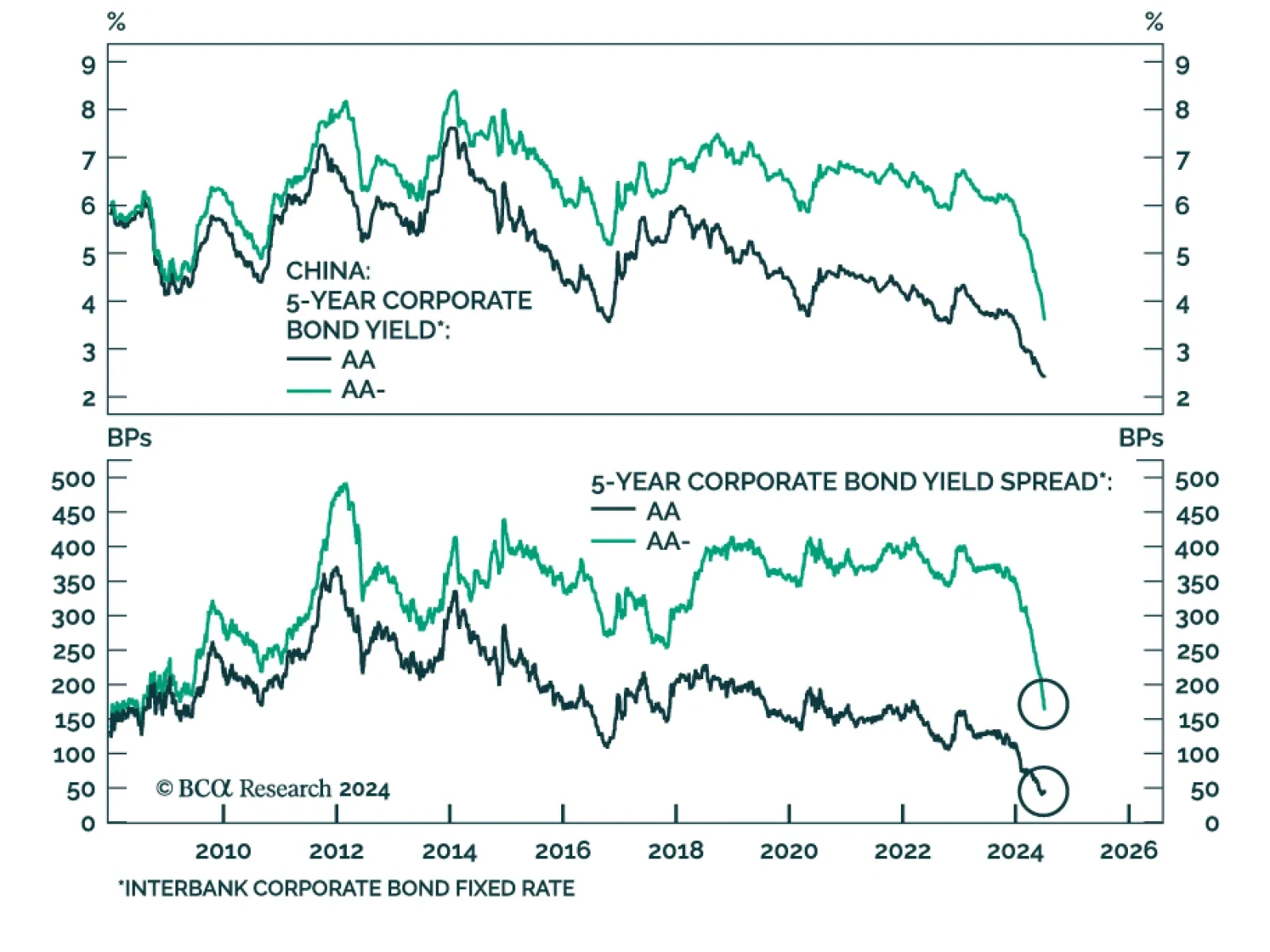

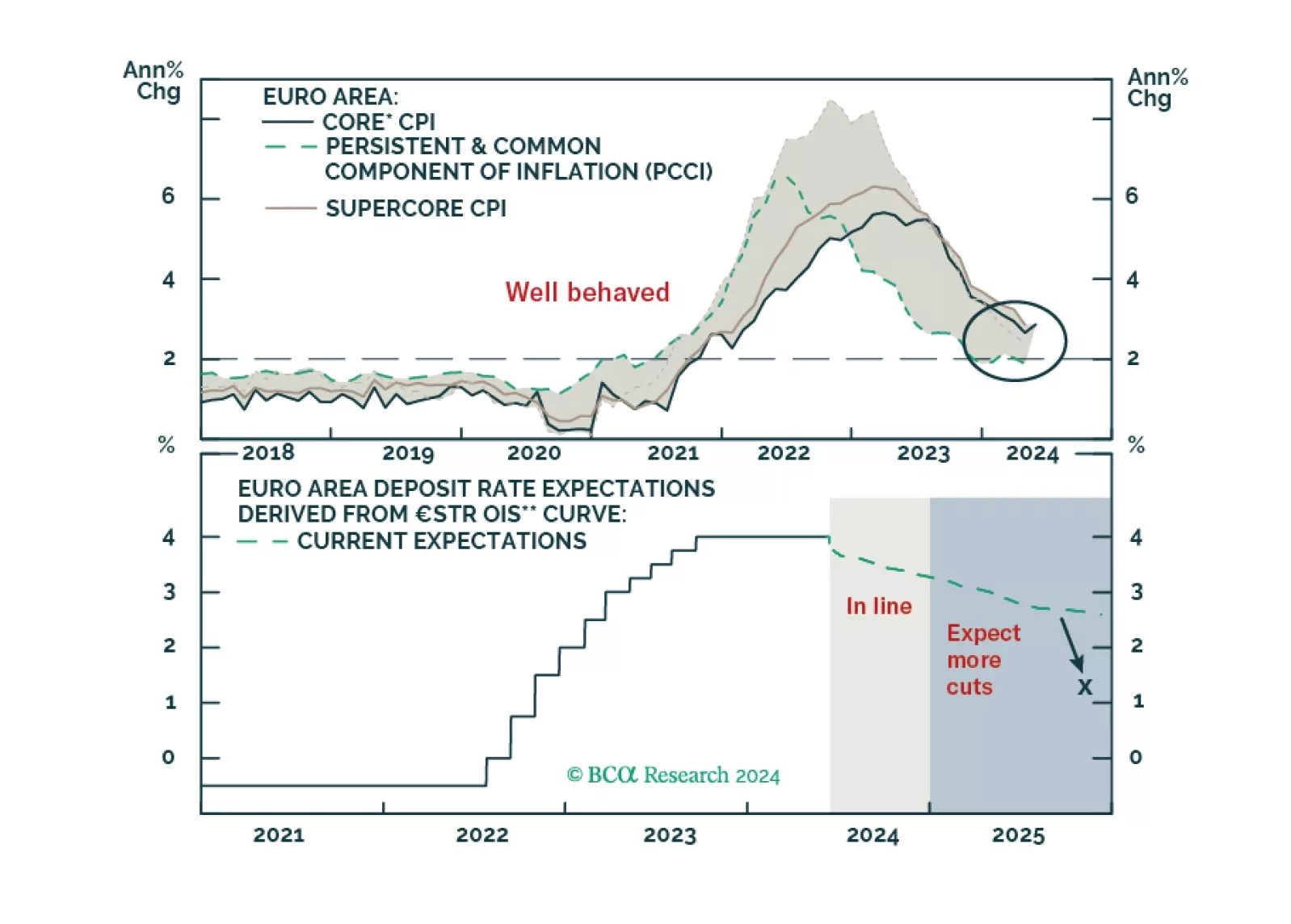

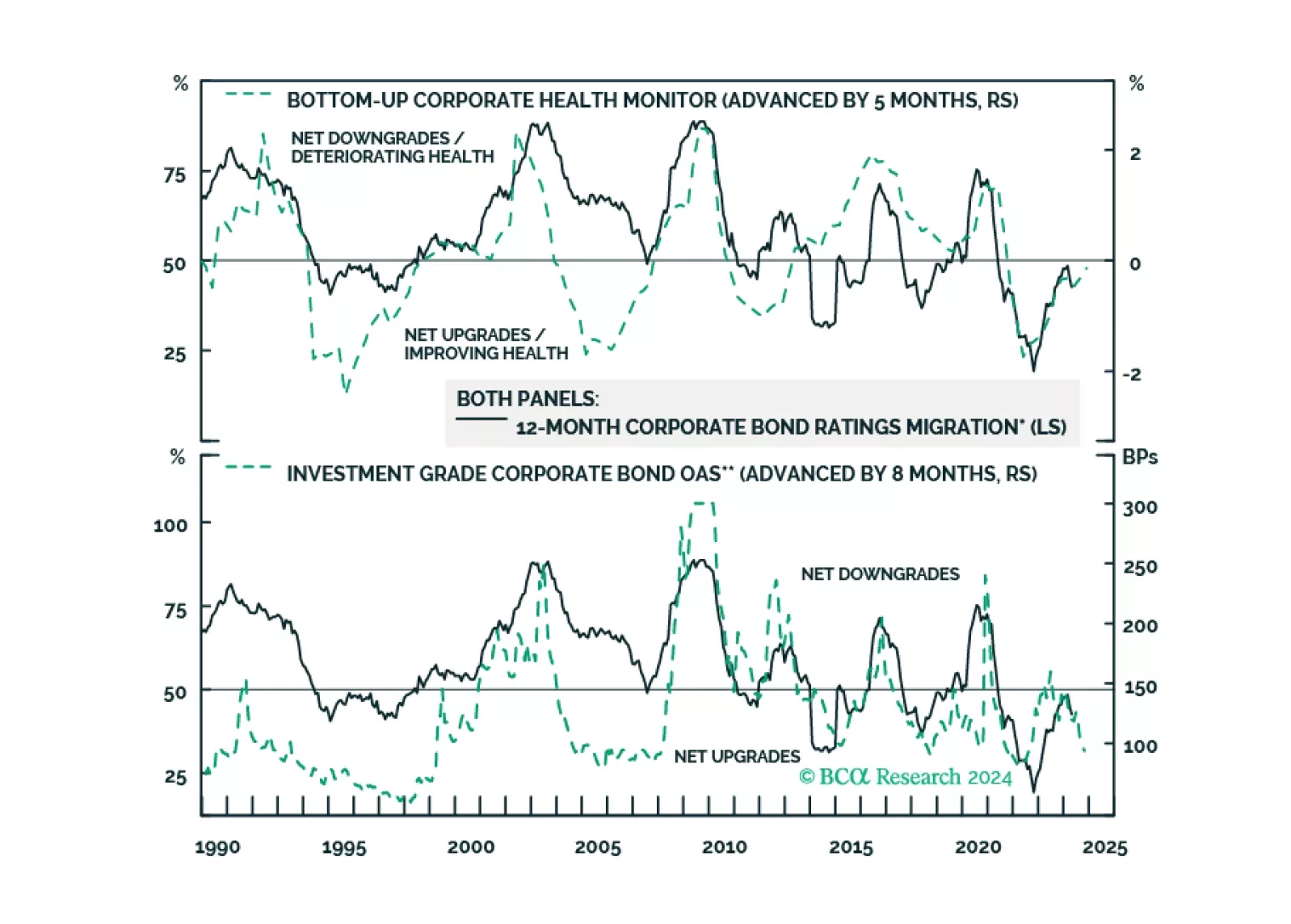

Nonfinancial corporate balance sheets are generally in good shape, but there are signs of deterioration at the bottom-end of the credit spectrum. We present evidence showing that credit deterioration at the bottom-end of the credit spectrum has a habit of migrating upwards.