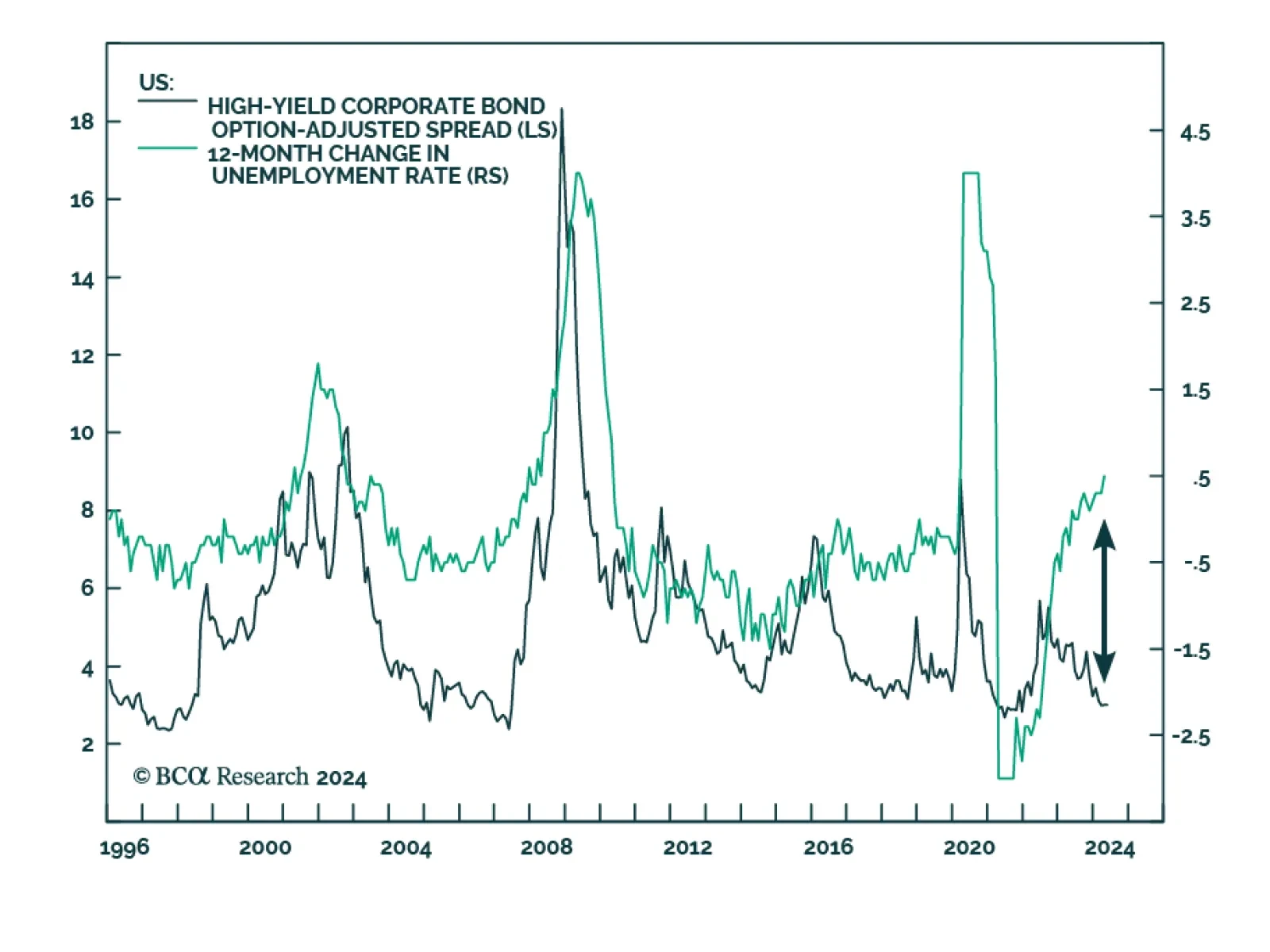

Corporate Bonds

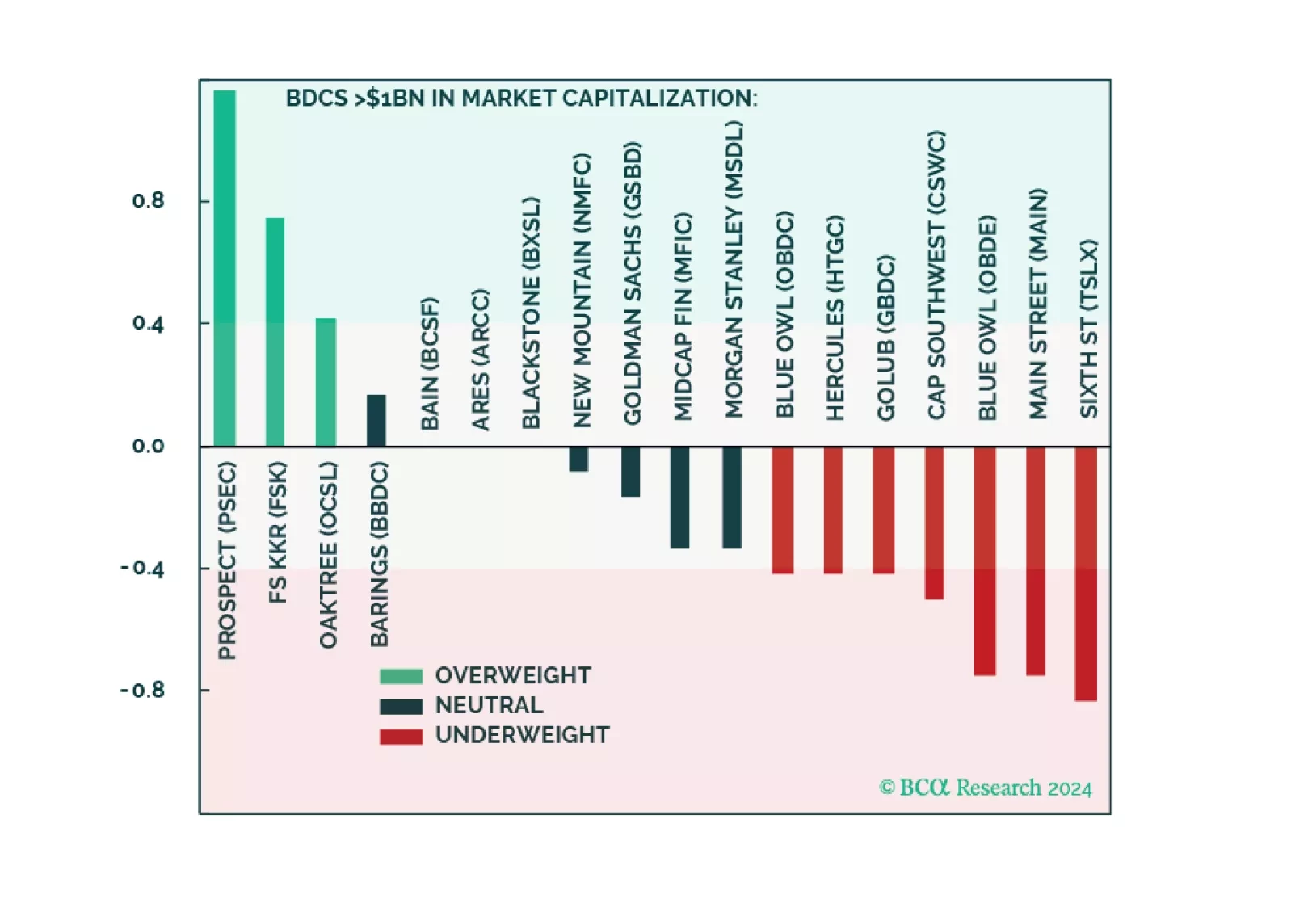

We are positive Private Credit but currently underweight Public BDCs. Today’s market pricing and sentiment in BDCs are excessively optimistic. Long-term investors should await a better entry point. Traders may find an attractive short. This report also peels back the Public BDC onion and presents over/underweights across individual BDCs via our filtering methodology.

Also included at the end of this report is an updated presentation titled 'Private Credit: Drivers Of The Boom And Understanding Risks On The Horizon,' recently presented at GII’s Private Credit Roundtable in Australia. It features updated charts and additional analysis.

Our Portfolio Allocation Summary for May 2024.

Central banks are in a dilemma whether to prioritize supporting growth or bringing inflation back to target. This is unlikely to end well. Investors should be defensively positioned.

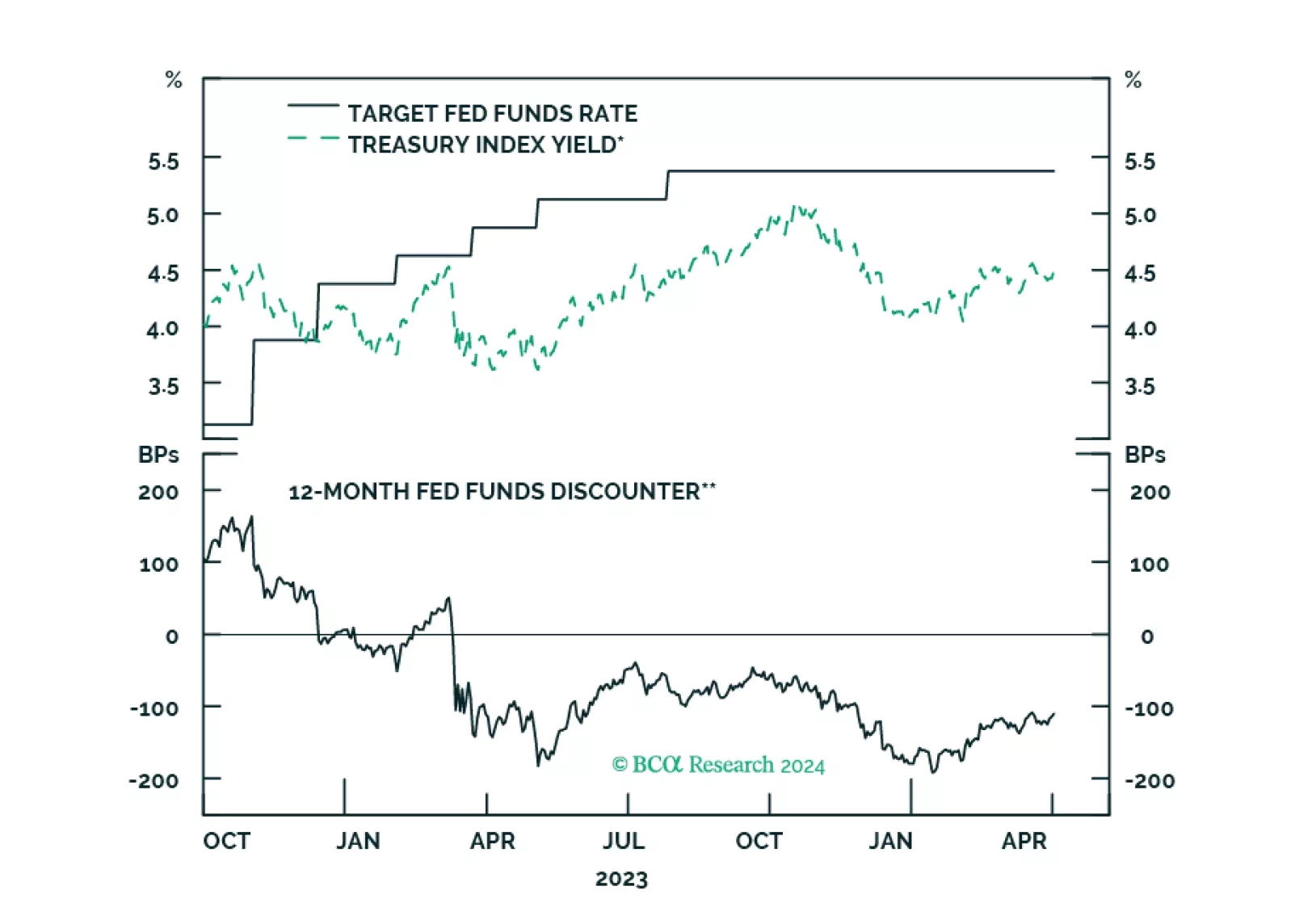

In this report, we present our quarterly review of our Model Bond Portfolio. The anti-growth bias of the portfolio allocations hurt the portfolio performance in Q1/2024 as global growth surprised to the upside. However, we anticipate some recovery of the underperformance in our base case scenario for the next six months.

Our Portfolio Allocation Summary for April 2024.

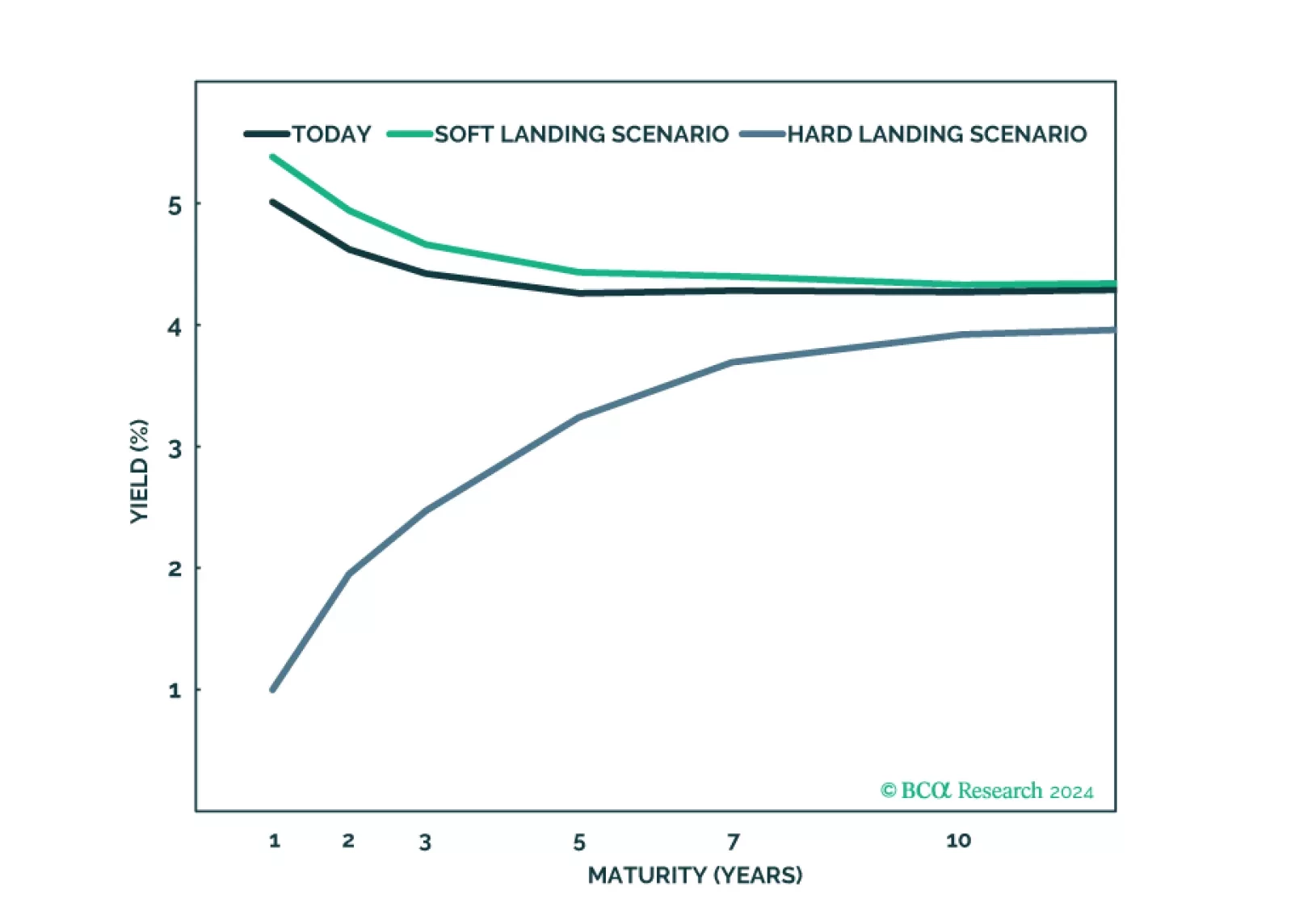

The global economy is wobbling precariously between slowing growth and reaccelerating inflation. This is unlikely to end well. Stay cautious, and hedge against both recession and inflation.

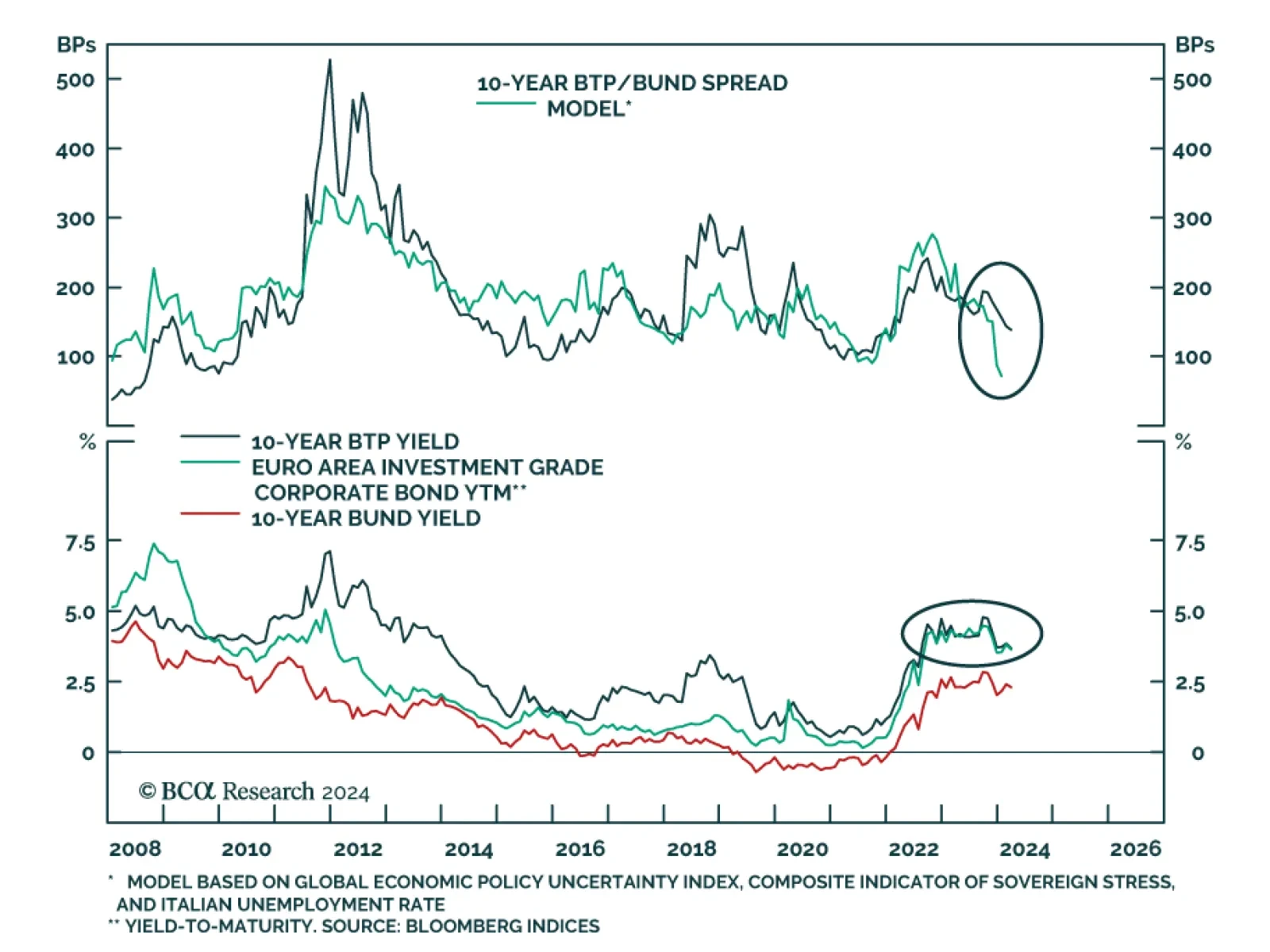

We expand our risk/reward analysis of US investment grade corporate bonds to focus on the 44 industry groups included in the Bloomberg index.

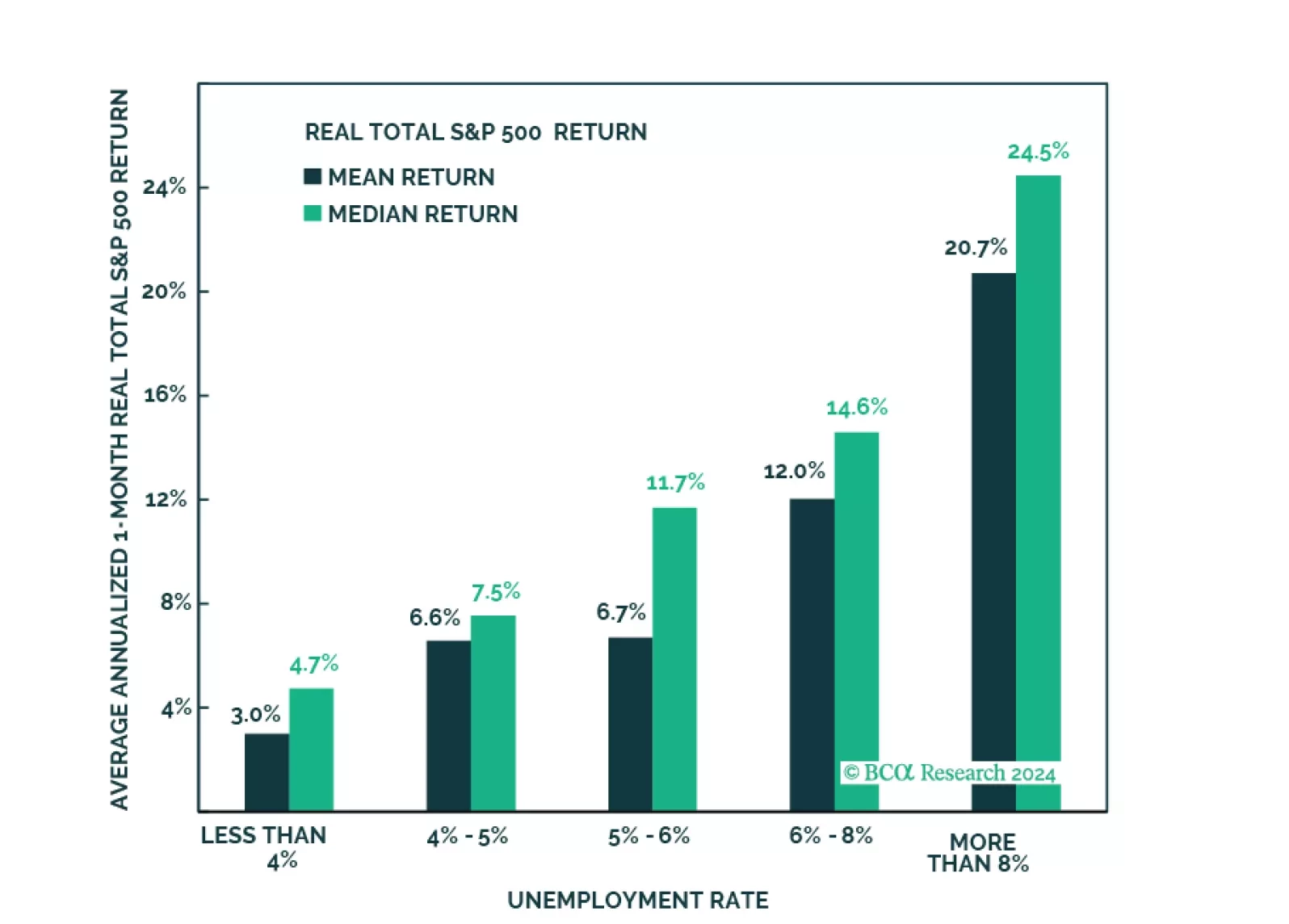

In this Strategy Outlook we examine why, contrary to popular perception, the odds of a global recession over the next 12 months are rising not falling.