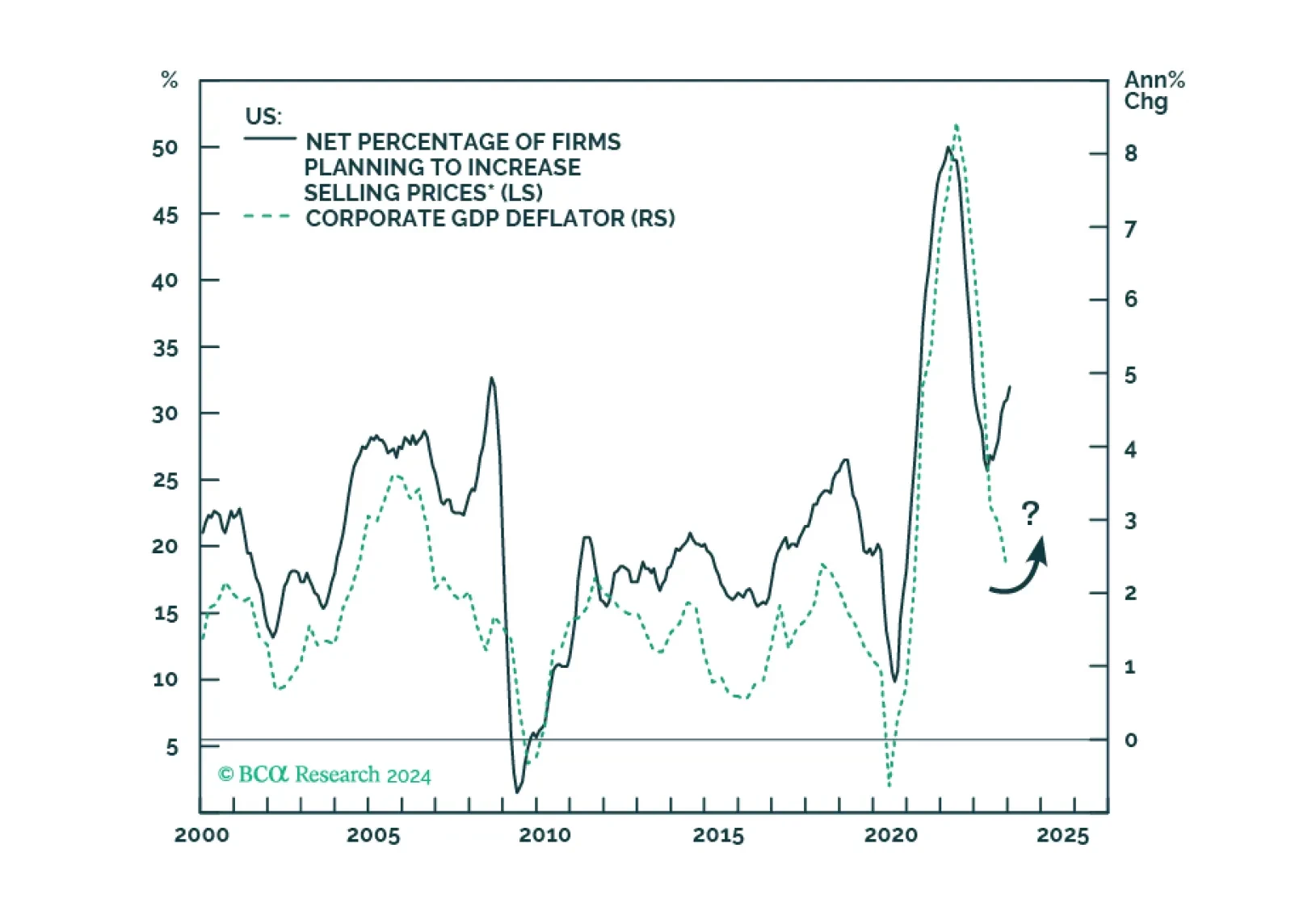

Corporate Profits

Presently, our four high-conviction themes are: (1) the US dollar will rally as US growth continues to outpace the rest of the world; (2) US equities will continue to outperform EM and European stocks until a major sell-off occurs; (3) a US profit margin squeeze is imminent; (4) EM domestic bonds and sovereign USD bonds are due for a setback.

In this BCA Special Report, we ask what policies investors should expect if Donald Trump wins the 2024 Presidential election. The answer is that a second Trump term would be much less positive for risky assets than the first. While the US will remain democratic and geopolitically preeminent no matter the outcome of the 2024 election, a second term Trump administration would likely oversee large budget deficits, continued wealth inequality, labor shortages, high import prices, and an erosion of checks and balances, possibly including at the Federal Reserve. Trade policy under a second Trump presidency represents the greatest cyclical risk to investors, and the sequencing of policies in general will be important to monitor. An early legislative priority of immigration over tax cuts, alongside the rapid imposition of new tariffs, would be the worst alignment for risky assets.

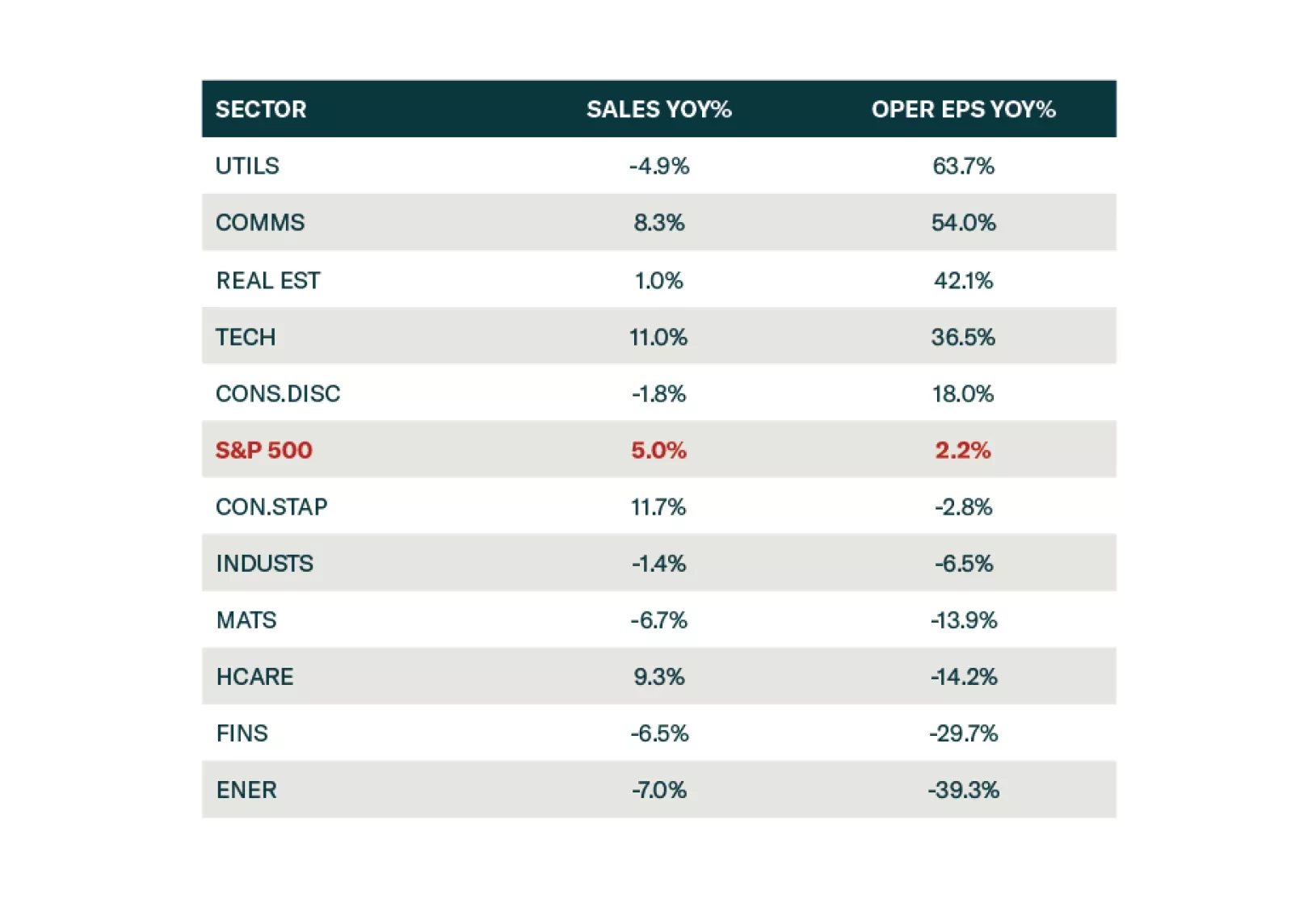

Reported earnings for Q4-2023 were rather underwhelming and prone to issues that we have identified over the past few months: Growth is concentrated in just a few sectors and companies, while the profitability of a broad swath of the equity market is under pressure from disinflation and sticky wages. Consumers are still spending, but less enthusiastically than before, while a switch from spending on services to spending on goods is in its very early innings. Downgrade Consumer Staples to neutral.