Cryptocurrencies

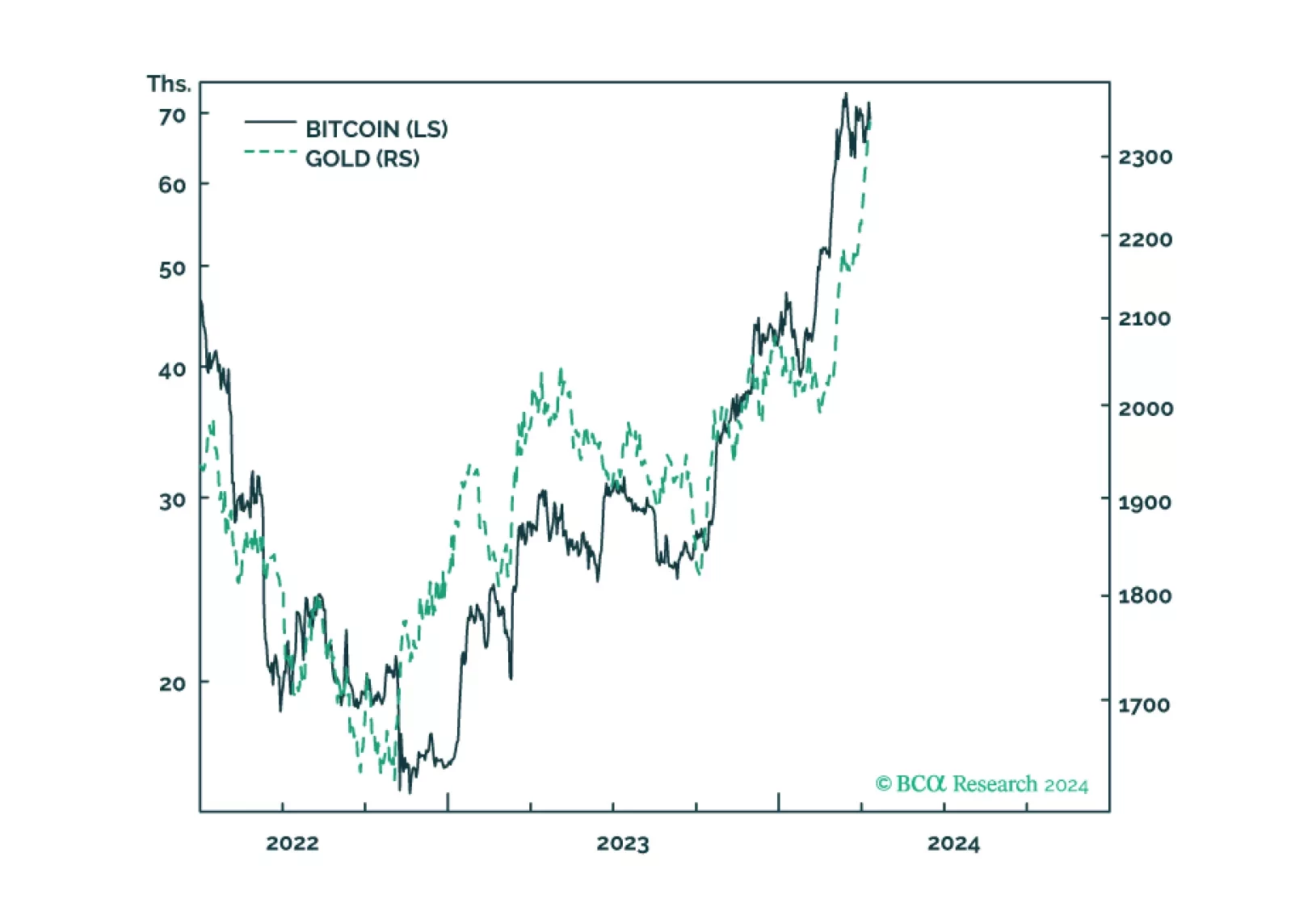

Gold and bitcoin are conceptually joined at the hip because the value of both comes from their ‘non-confiscatability’ by inflation, by bank failure, and in the case of bitcoin, by state expropriation. The sharp recent rallies in both gold and bitcoin reflect that the market has suddenly upped the value of non-confiscatability, and a plausible explanation is that recent US inflation data show that the journey to sustained 2 percent inflation has stalled, raising the risk that the Fed might balk at finishing the journey. Plus: JPM, CL, and USD/CHF are tactical reversal candidates.

The SEC has just approved bitcoin spot ETFs, but does bitcoin have any ‘intrinsic’ value? In this Special Report we explain why the answer is yes, how bitcoin compares with gold, and why the bitcoin price could ultimately head well north of $100,000.

We recommend a small structural exposure to cryptocurrencies and blockchain tokens, given their incipient real-world uses as well as their proven hedging qualities against the debasement of fiat money and in banking crises. In this Special Report, we rank the major blockchains on five factors – developer activity, adoption, decentralization, scalability, and security – from which we arrive at our top five blockchains.

There is a 50:50 chance of experiencing a major deflationary shock in the next two years, and an even greater likelihood on a longer timeframe. The good news is that several assets provide a good insurance against this risk, and that this insurance is now cheap. Plus we highlight a compelling commodity pair-trade.

In this volume of BCA Crypto we compare gold against bitcoin. We begin by dispelling some common misconceptions that investors have about gold, and why, at its core, gold is driven more by belief than by intrinsic value. We then proceed to explain why gold still serves an important role in our economy and how it differs from fiat money. Later, we explain how bitcoin is different from other cryptocurrencies, and why it could rival gold as a reserve asset in the future. Finally, we discuss the outlook for bitcoin, as well as which macro factors investor should watch.

The Web 2.0 bubble is bursting, with far-reaching consequences for US stock market behaviour, sector allocation, and global asset allocation.

Web 3.0 plays will boom in the coming decade. Play this through a diversified exposure to today’s main blockchain tokens. But the Web 2.0 oligopolies, like Amazon and Meta, are in big trouble.

Crypto broker FTX’s bankruptcy does not pose a systemic threat to markets. It did reveal something deeply unflattering about excess liquidity, however, and suggests that other private investments may come a cropper.

The kinked supply framework helps explain why US inflation rose so suddenly shortly after the pandemic began and why the economy is likely to experience a benign disinflation over the next six months.