Currencies

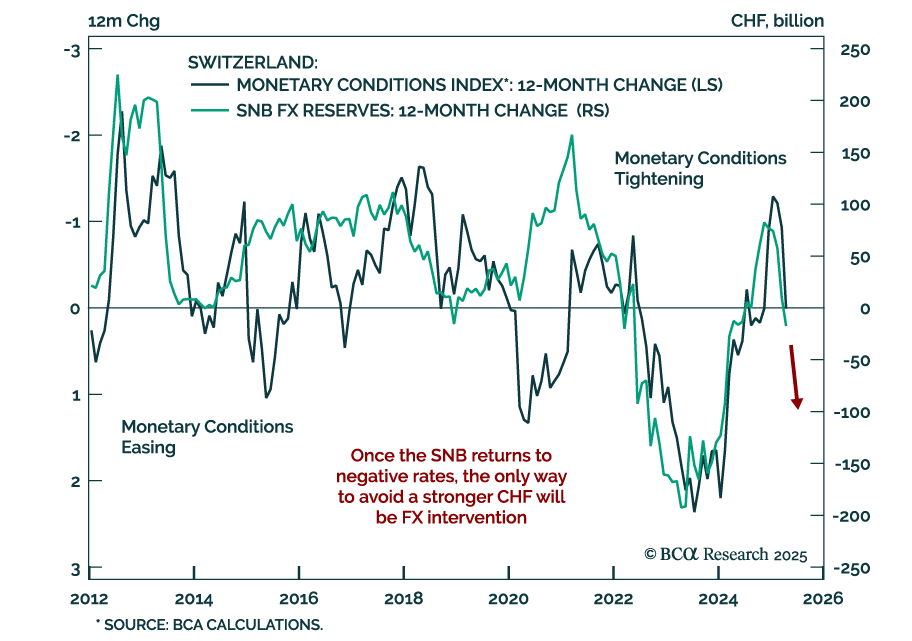

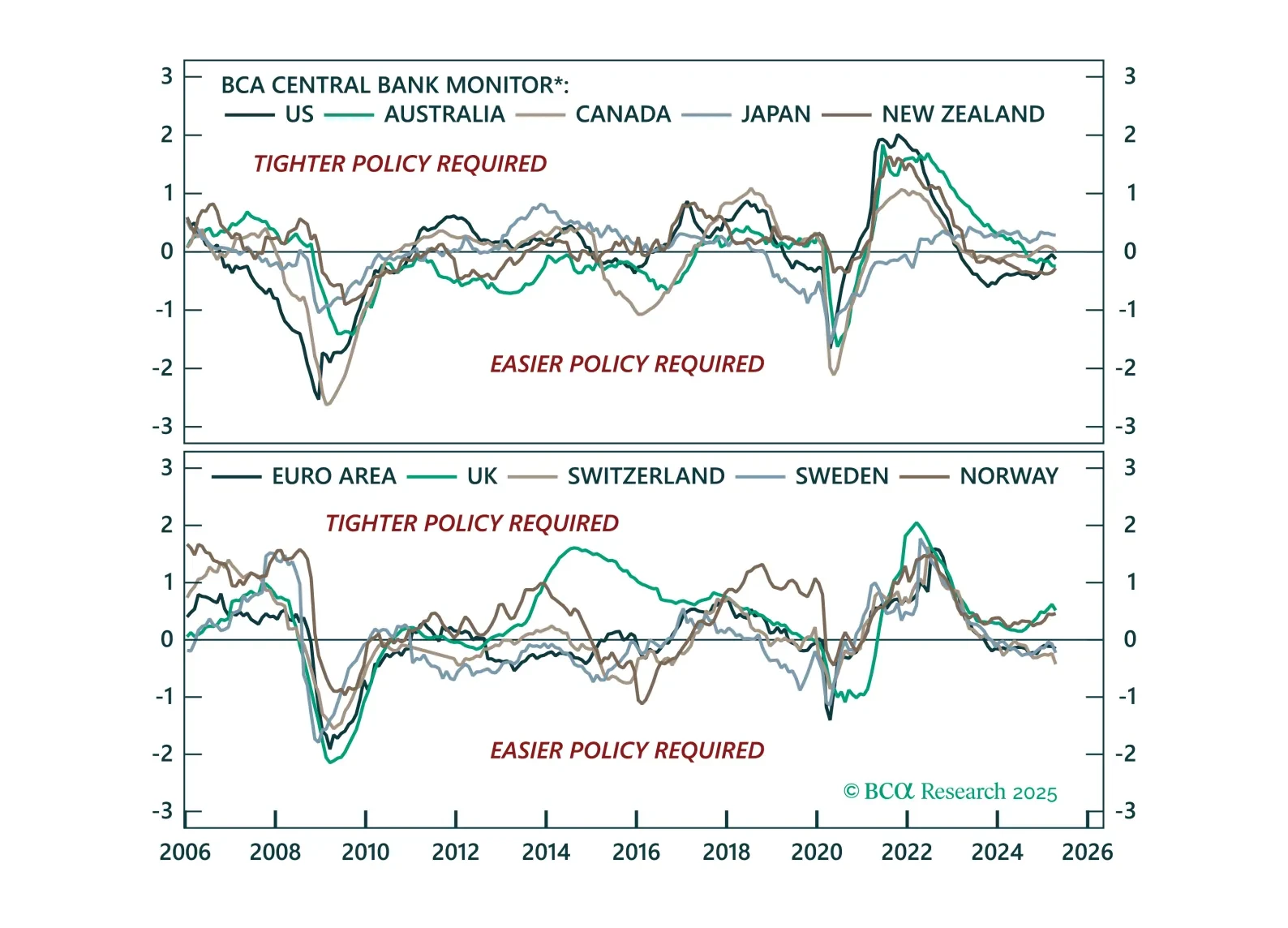

The easing bias remains, but not all central banks are equal. This Central Bank Monitor update reveals who is ready to cut more and who is still pretending not to.

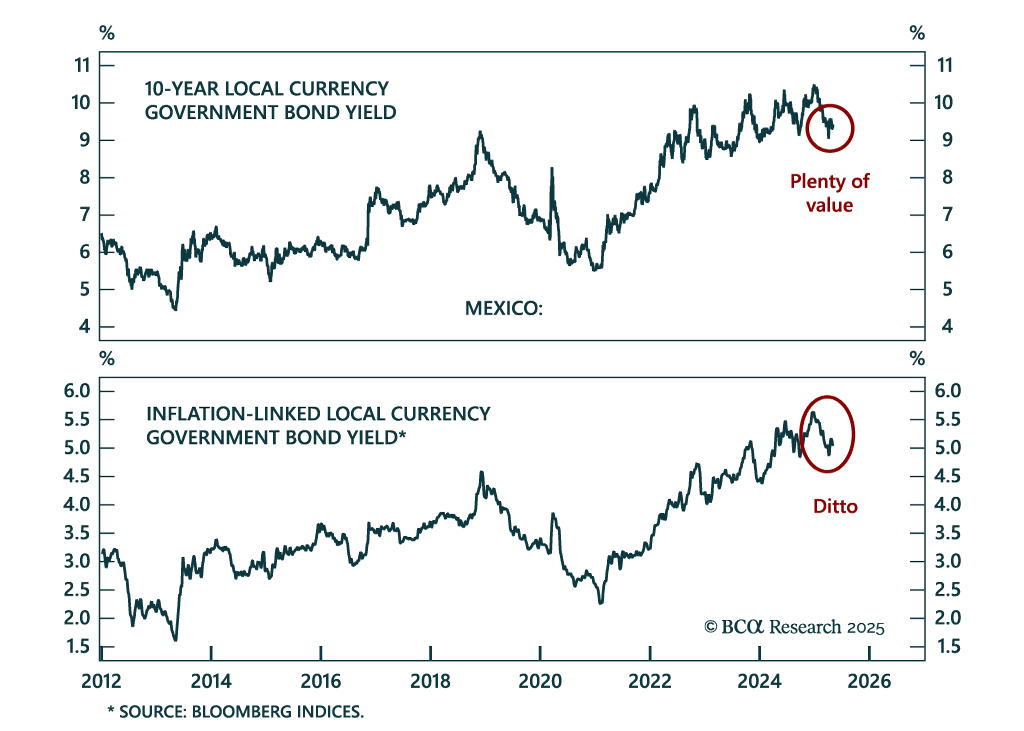

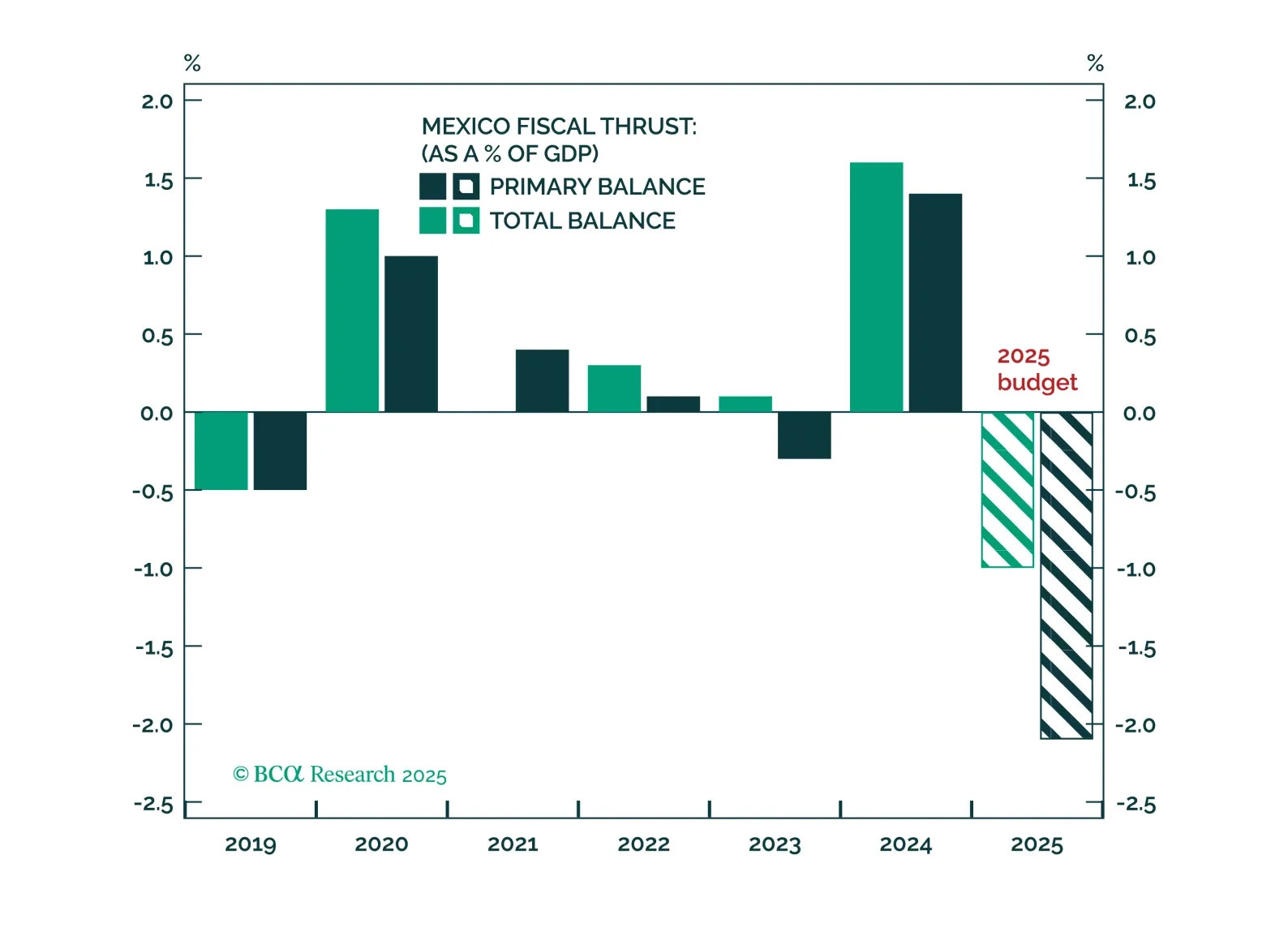

Short-term pain from Trump-related concessions, fiscal tightening amid a US and Mexican slowdown, and rising labor slack will weigh further on Mexican assets. But long-run, policy direction will capitalize on the nearshoring trend and resume the trend of Mexican asset outperformance relative to other emerging markets.

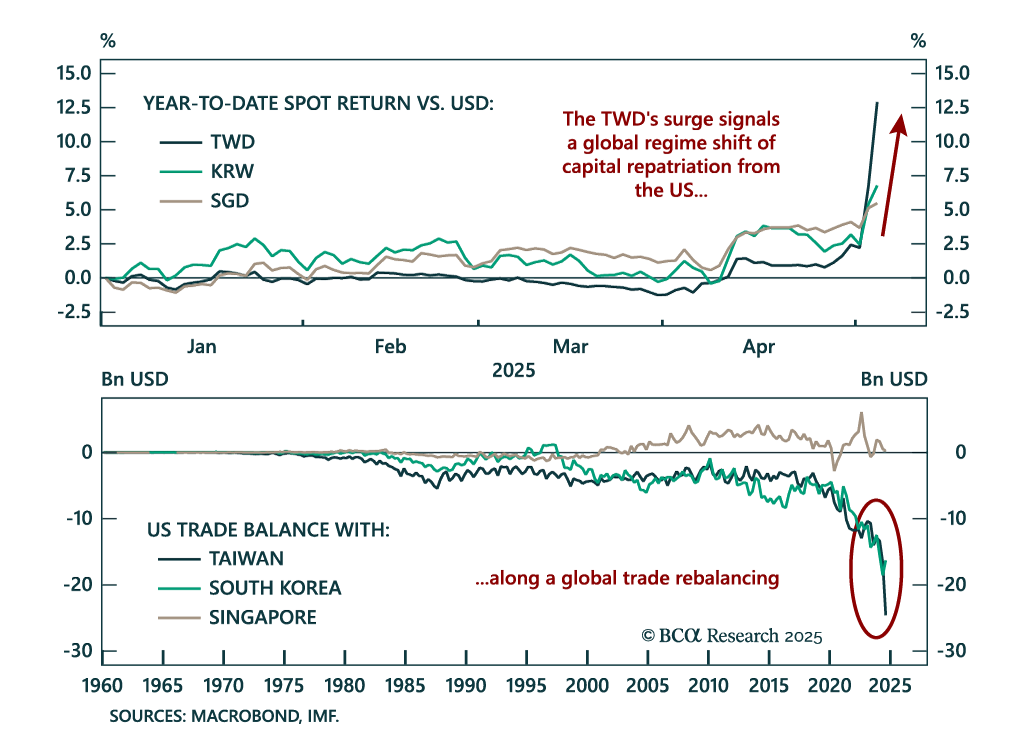

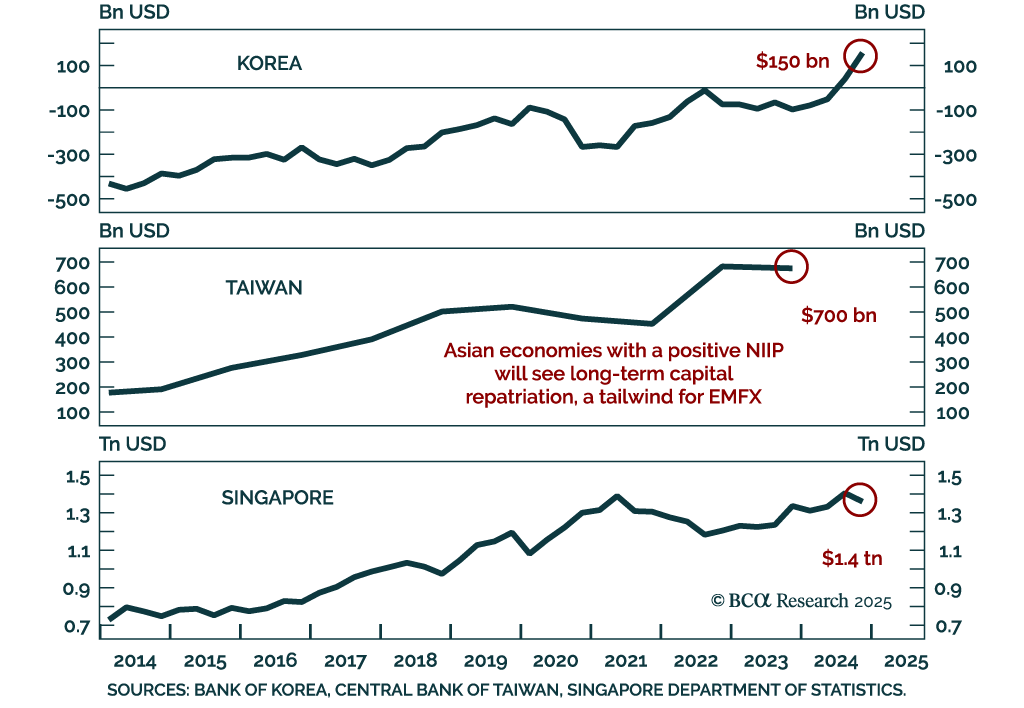

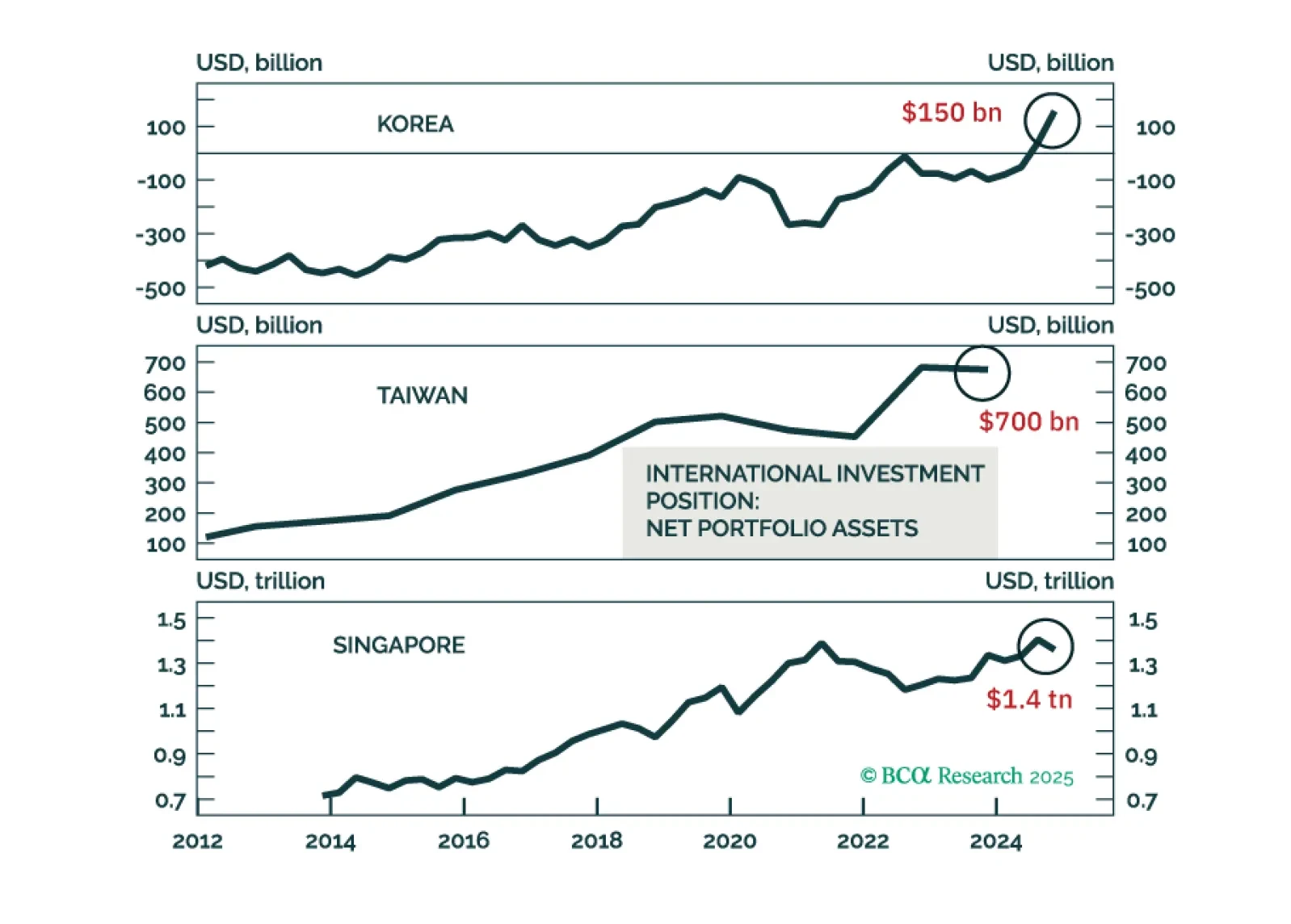

Taiwan, Singapore, and Korea's currencies might appreciate versus the USD, driven by capital repatriation from domestic private investors away from the US. This thesis is less pertinent to India, Indonesia, and the Philippines because they have large net foreign portfolio liabilities. Malaysia and Thailand fall in the middle, while China is an exception. Investors should play intensifying deflationary pressures in Asia by betting on lower interest rates in the region.