Currencies

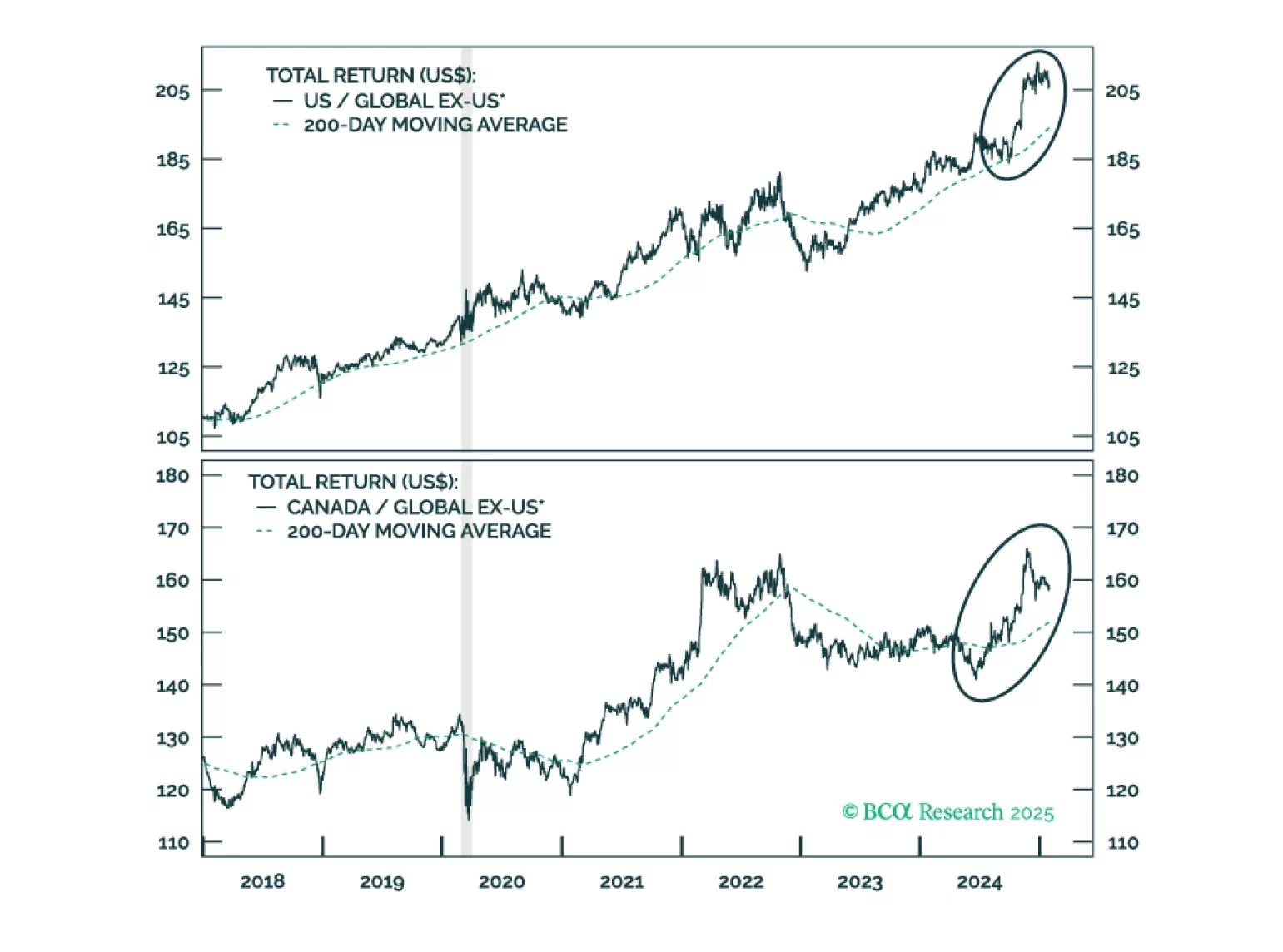

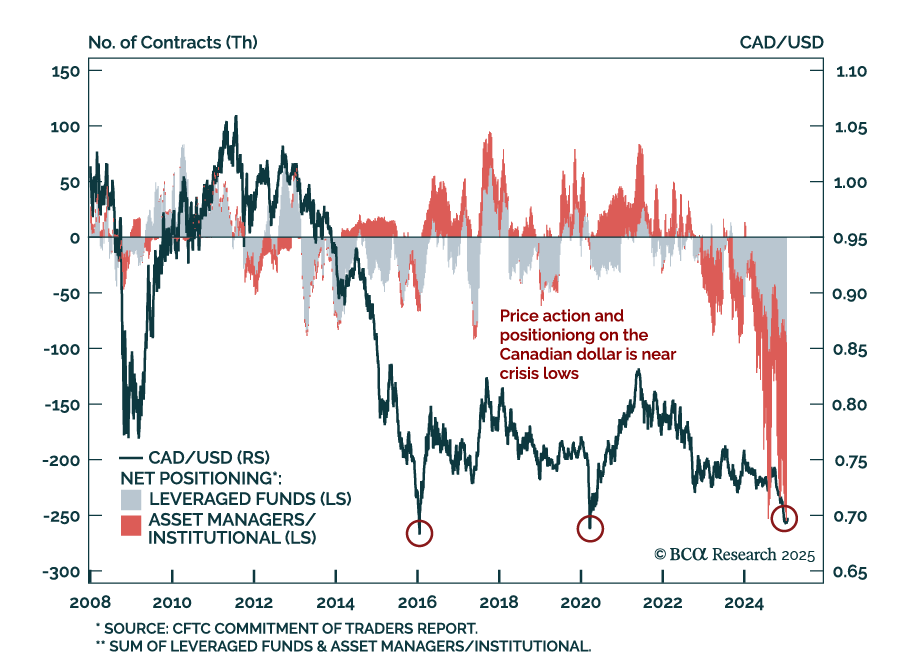

Jonathan provides an update on Canada following strong performance from Canadian stocks last year. On a tactical basis, underweight Canada versus global ex-US on the expectation of tariffs targeting Canada and Mexico. Following a sell off, or if a trade war is avoided, investors should place Canadian stocks on upgrade watch with the goal of moving to a modest overweight versus global ex-US.

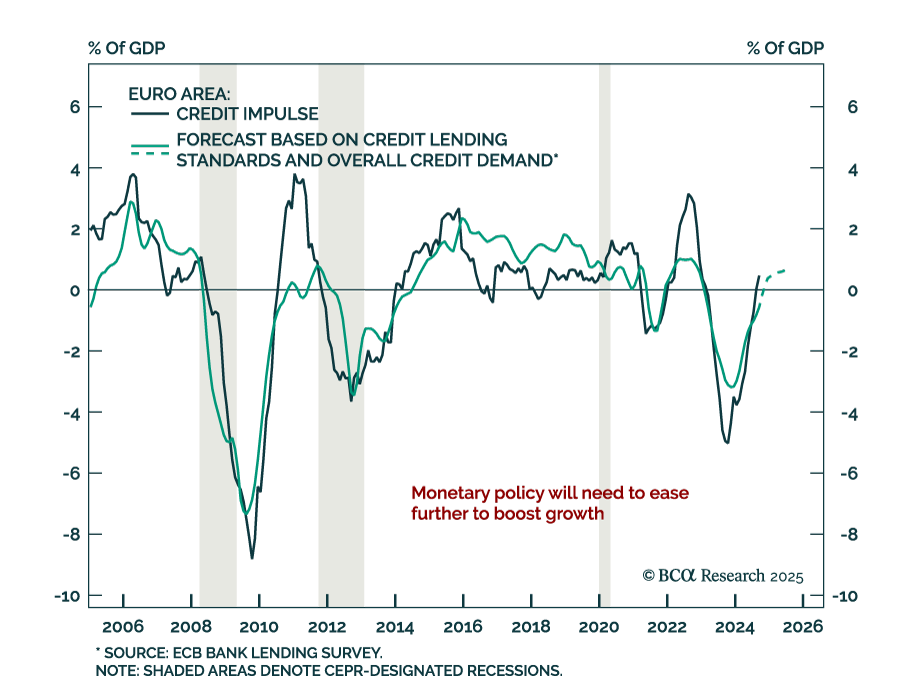

The January 2025 ECB bank lending survey saw a net tightening of credit standards in Q4 2024. Credit standards were tightened for business and consumer lending, and were roughly unchanged for home mortgage loans. Banks expect further tightening across all…

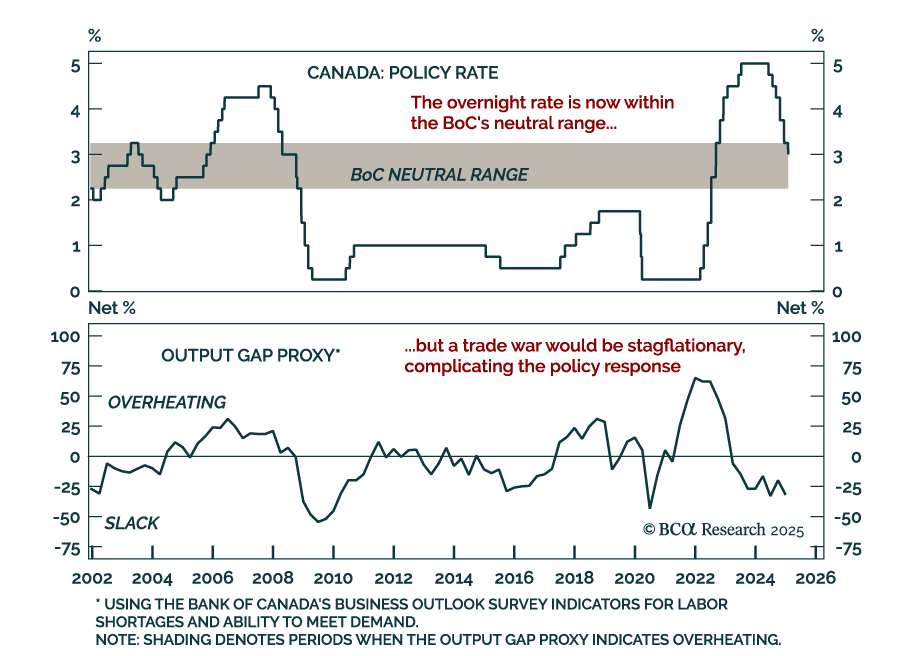

The Bank of Canada cut by 25 bps to 3% as expected, and announced the end of quantitative tightening. This sixth consecutive cut brings the policy rate further into neutral territory, estimated to be in the 2.25%-to-3.25% range. The BoC assessed…

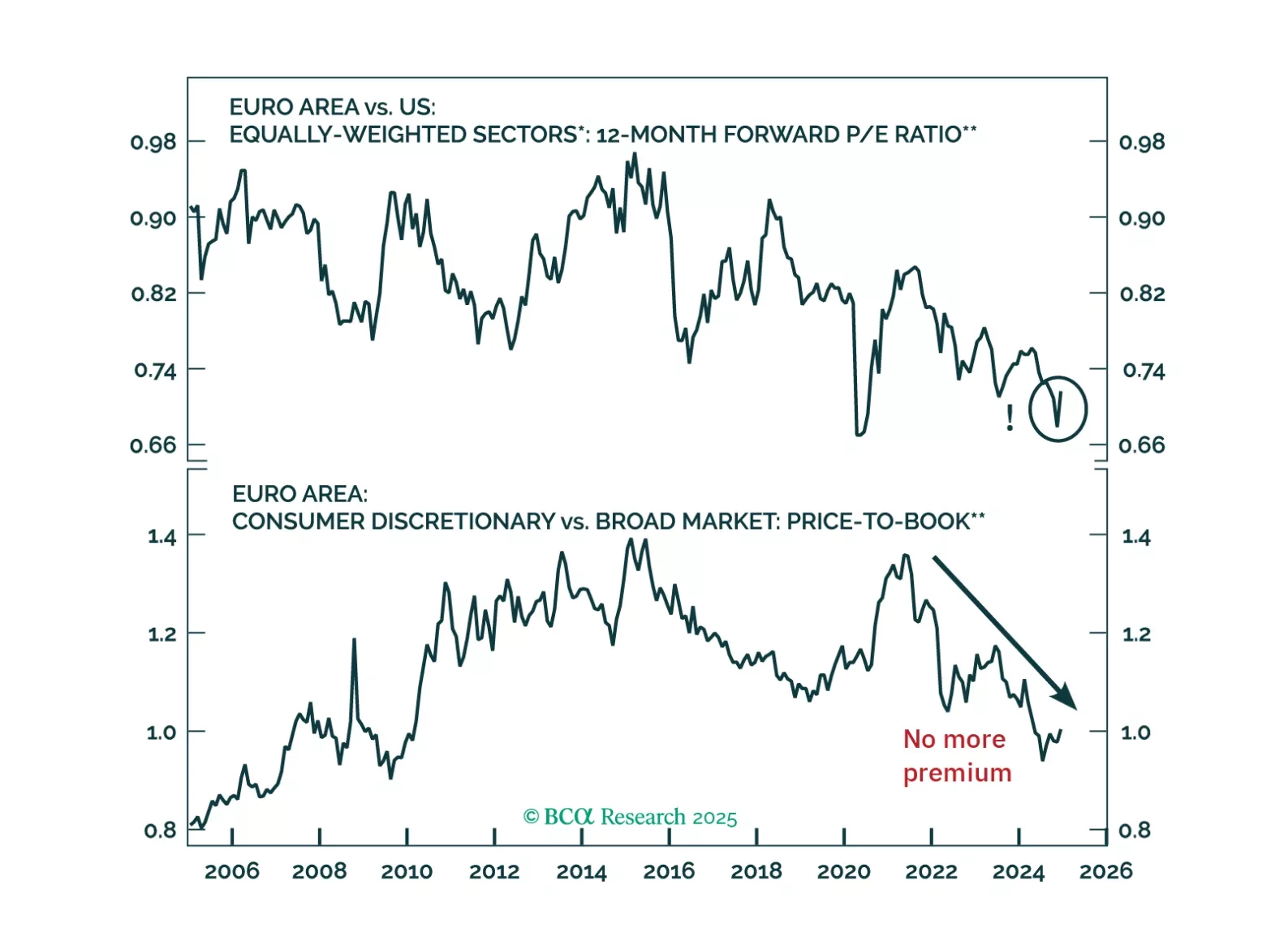

Global risk assets are engulfed in a wave of euphoria, which is pulling Europe higher along the way. However, risks still abound. How should investors adjust their allocation to Europe under these highly uncertain conditions?

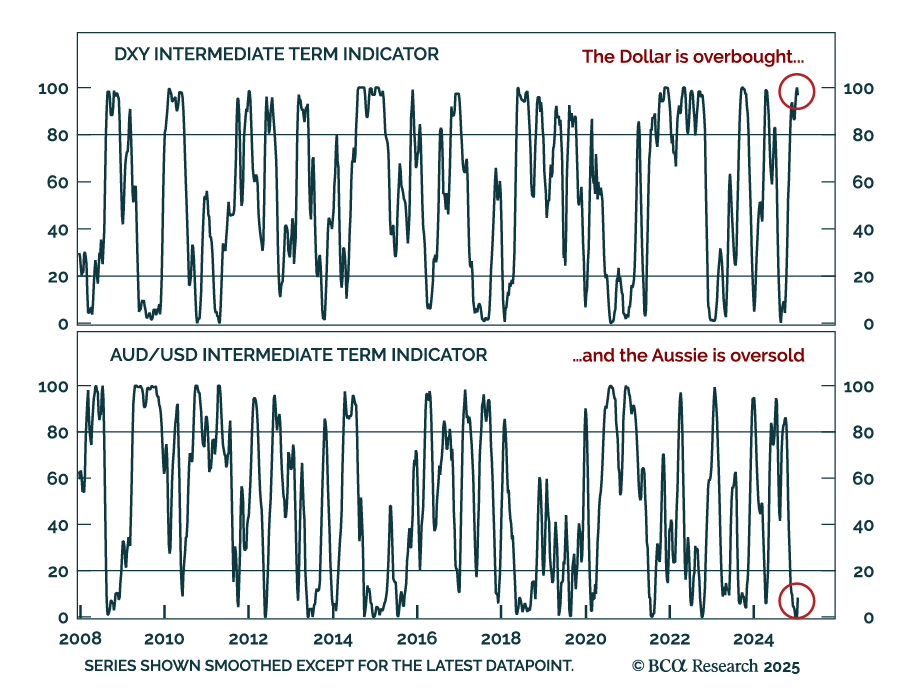

Our Foreign Exchange strategists recently provided an update on their US and Australian dollar views. The US dollar remains overbought and may continue rising as a momentum currency, but cyclical indicators suggest a capitulation phase. Our FX team…

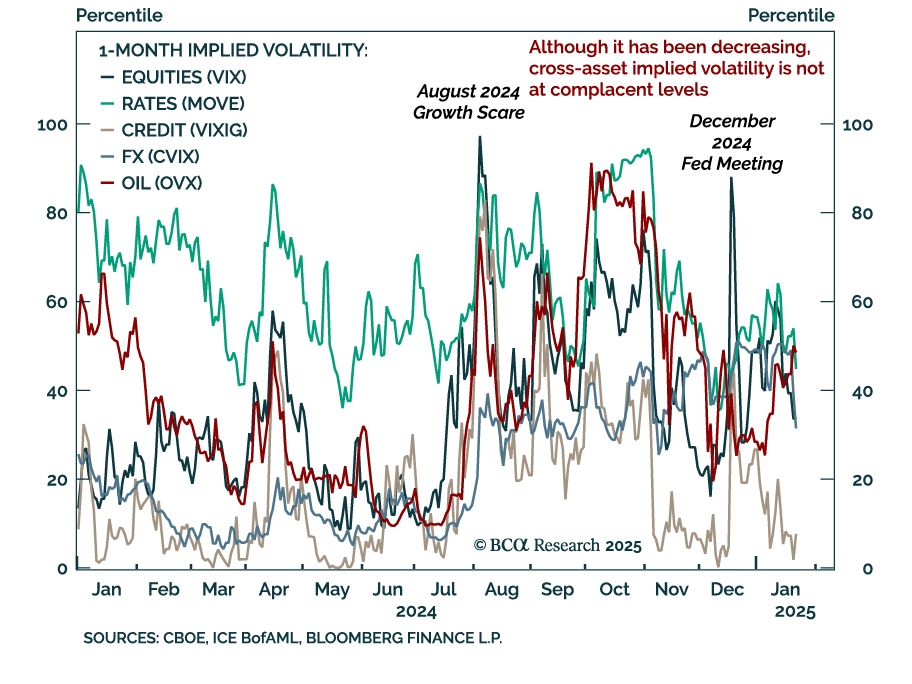

Despite the choppy price action of the last few weeks, equity sentiment remains elevated. Surveys of investor sentiment remain at the top end of the bullish spectrum, and the S&P 500 is trading over 22x forward earnings, levels only seen in the…

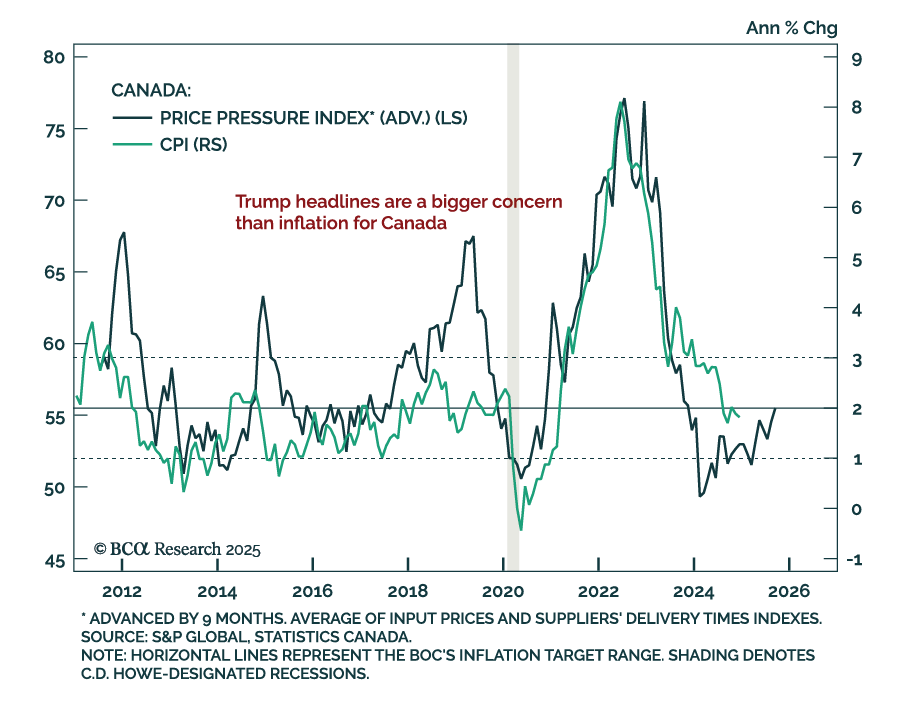

Until recently, Canada had been flying under the radar, yet it presents an interesting macro case. The Bank of Canada hiked rates in lockstep with the Fed, but it began cutting earlier due to a more fragile Canadian economy. Domestic and international…

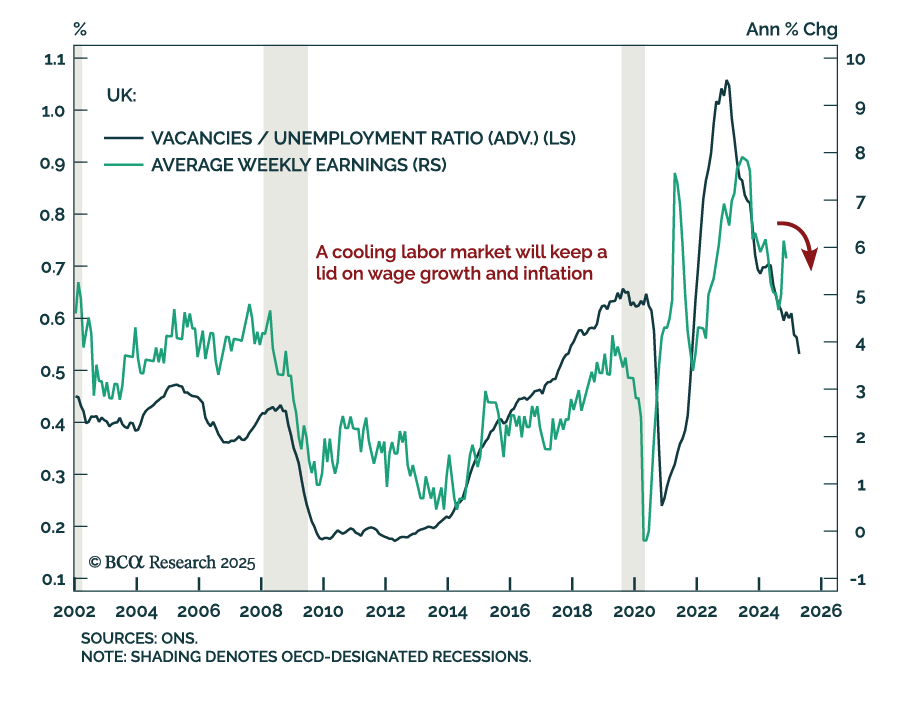

November/December UK employment data was mixed. The November unemployment rate rose 0.1% to 4.4%, in line with expectations. Payrolled employees decreased faster than expected at a 47k pace in December, surpassing the 35k contraction in November. However,…

The December Canadian CPI was roughly in line with estimates, with headline inflation ticking down to 1.8% y/y from 1.9% in November. The BoC’s core inflation measures, median and trim, also decreased from 2.6% to 2.4% and 2.5%,…

Our Emerging Markets strategists put together a hypothetical conversation between President Trump and Treasury Secretary nominee Scott Bessent on what economic policy would look like for the Trump 2.0 administration. Secretary Bessent is expected…